TFT LCD Market

TFT LCD Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706641 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

TFT LCD Market Size

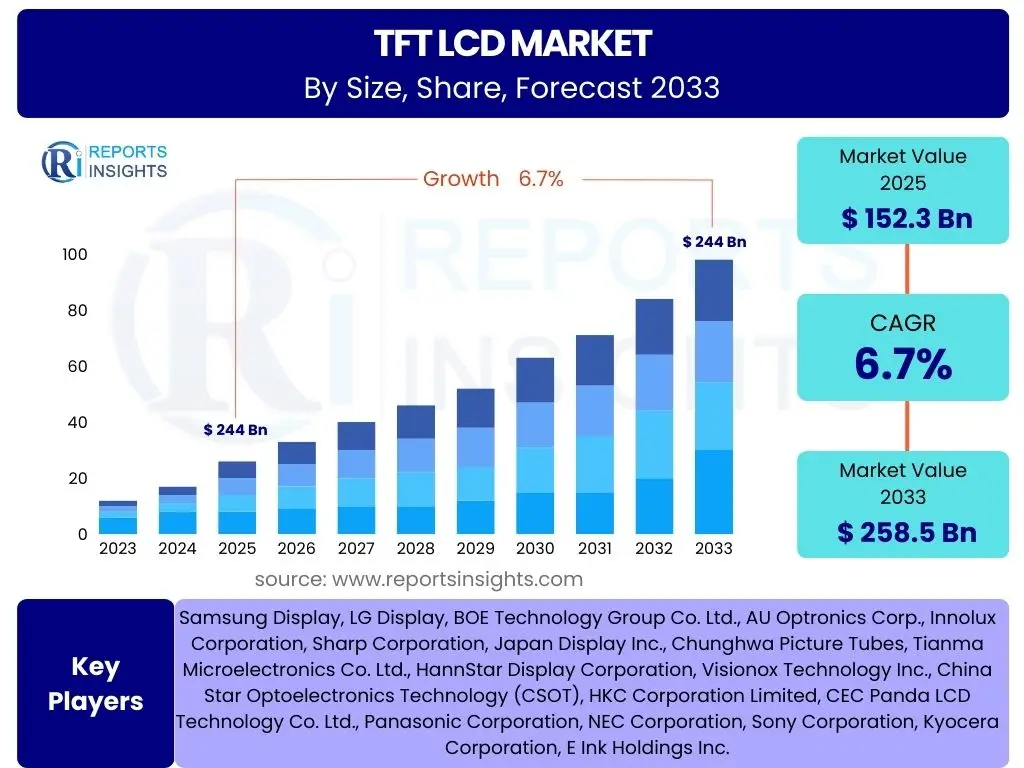

According to Reports Insights Consulting Pvt Ltd, The TFT LCD Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 152.3 billion in 2025 and is projected to reach USD 258.5 billion by the end of the forecast period in 2033. This growth trajectory reflects the expanding applications of TFT LCD technology across diverse industries and the continuous innovation in display manufacturing processes, enhancing performance characteristics such as resolution, brightness, and energy efficiency. The consistent demand from consumer electronics, coupled with emerging opportunities in automotive and industrial sectors, underpins this positive market outlook.

Key TFT LCD Market Trends & Insights

The TFT LCD market is currently undergoing significant transformation, driven by evolving consumer preferences and technological advancements. A prominent trend involves the pursuit of higher display resolutions, with 4K and 8K panels becoming increasingly common in televisions and large-format displays, catering to the demand for immersive visual experiences. Simultaneously, advancements in panel efficiency and thinness are enabling the development of more portable and aesthetically pleasing devices. The integration of enhanced touch capabilities and wider viewing angles also marks a key area of innovation, improving user interaction and display versatility across various applications, from smartphones to interactive digital signage.

Another critical insight reveals a growing emphasis on specialized display solutions tailored for specific industries. The automotive sector, for instance, is seeing a surge in demand for robust, high-brightness, and wide-temperature-range TFT LCDs for infotainment systems, digital dashboards, and heads-up displays. Similarly, industrial and medical applications require displays with exceptional reliability, long operational lifespans, and precise color reproduction. This diversification in demand is pushing manufacturers to develop customized TFT LCD solutions, moving beyond general-purpose panels to meet the stringent requirements of niche markets, thereby sustaining market growth even as other display technologies emerge.

- Increased adoption of high-resolution (4K/8K) panels in large-format displays.

- Development of thinner, more energy-efficient displays for portable devices.

- Expansion of specialized TFT LCDs for automotive, industrial, and medical applications.

- Integration of advanced touch and interactive functionalities.

- Shift towards more sustainable manufacturing processes and materials.

AI Impact Analysis on TFT LCD

Artificial Intelligence (AI) is beginning to exert a transformative influence across the entire TFT LCD value chain, from design and manufacturing to quality control and user experience. In the manufacturing process, AI-powered systems are being deployed for predictive maintenance of production equipment, optimizing operational uptime and reducing costly downtimes. Machine learning algorithms analyze vast datasets from production lines to identify subtle defects early, leading to improved yield rates and reduced waste. This integration of AI significantly enhances the efficiency and precision of complex fabrication steps, such as coating, etching, and assembly, ensuring consistent quality and accelerating production cycles.

Beyond manufacturing, AI contributes to the enhancement of TFT LCD display performance and user interaction. AI algorithms can be employed to dynamically adjust display parameters such as brightness, contrast, and color temperature based on ambient lighting conditions or content being displayed, optimizing visual comfort and energy consumption. For example, in smart televisions or monitors, AI can analyze video content to upscale resolution or enhance image clarity in real time. Furthermore, AI-driven analytics can inform future display designs by identifying user preferences and performance bottlenecks, leading to the development of more intelligent and responsive display technologies that cater directly to evolving consumer needs and application demands.

- AI-driven optimization of manufacturing processes, including yield enhancement and defect detection.

- Predictive maintenance for display production equipment, reducing operational downtime.

- Real-time image and video processing for enhanced display quality and adaptive visuals.

- AI-powered backlight control for improved energy efficiency and contrast.

- Data analytics for new product development and market trend identification.

Key Takeaways TFT LCD Market Size & Forecast

The TFT LCD market is positioned for sustained growth through the forecast period, driven by its established position as a versatile and cost-effective display technology. Despite the emergence of alternative display solutions, TFT LCD continues to dominate a significant share of the display market due to its widespread adoption across a multitude of consumer and commercial applications. The market's resilience is further bolstered by ongoing innovations in manufacturing processes and materials, which enhance performance parameters such as brightness, color accuracy, and energy efficiency, ensuring its continued relevance in a competitive landscape.

A crucial takeaway from the market forecast is the increasing importance of specialized applications in propelling future growth. While traditional consumer electronics remain a foundational segment, the burgeoning demand from sectors like automotive, industrial automation, and healthcare for rugged, reliable, and high-performance displays is opening new avenues for market expansion. This diversification mitigates reliance on any single application segment, fostering a more robust and adaptable market. Moreover, regional economic developments and technological infrastructure investments, particularly in Asia Pacific, are expected to play a pivotal role in shaping the market's trajectory, solidifying the region's dominance in both production and consumption.

- Sustained market growth driven by broad application across consumer and industrial sectors.

- Technological advancements in resolution, energy efficiency, and durability continue to enhance product appeal.

- Increasing demand from automotive, industrial, and medical segments provides significant growth impetus.

- Asia Pacific remains a dominant force in both manufacturing and consumption of TFT LCDs.

- Cost-effectiveness and established supply chains contribute to the technology's enduring market relevance.

TFT LCD Market Drivers Analysis

The global TFT LCD market is significantly propelled by the relentless expansion of the consumer electronics industry. The ubiquitous presence of smartphones, televisions, laptops, and tablets, all of which heavily rely on TFT LCD technology for their displays, creates a foundational and continuously growing demand base. As consumers increasingly upgrade their devices to models featuring higher resolutions, larger screens, and improved visual fidelity, the demand for advanced TFT LCD panels escalates. This trend is not limited to new device sales; the replacement cycle for existing electronics also contributes substantially to market volume, ensuring a consistent need for display components.

Beyond traditional consumer gadgets, the robust growth in specialized application areas such as automotive infotainment, industrial control systems, and medical diagnostics equipment is serving as a powerful secondary driver. Modern vehicles integrate multiple large-format displays for navigation, entertainment, and driver information, demanding displays that can withstand harsh environmental conditions and offer superior clarity. Similarly, industrial and medical devices require high-reliability, long-lifecycle displays with precise color reproduction and wide viewing angles. These professional applications often command higher prices and have longer product lifecycles, providing stable revenue streams and fostering innovation in specialized TFT LCD panel development, thereby diversifying and strengthening the overall market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for consumer electronics (smartphones, TVs, laptops) | +2.1% | Global, particularly Asia Pacific | 2025-2033 |

| Expansion of automotive display applications (infotainment, dashboards) | +1.8% | North America, Europe, Asia Pacific (China, Japan) | 2025-2033 |

| Increasing adoption in industrial and medical devices | +1.5% | North America, Europe, select APAC countries | 2025-2033 |

| Rising demand for digital signage and advertising displays | +1.0% | Global, major urban centers | 2025-2033 |

| Technological advancements improving display performance and cost-efficiency | +0.8% | Key manufacturing hubs (China, South Korea, Taiwan, Japan) | 2025-2033 |

TFT LCD Market Restraints Analysis

Despite robust growth, the TFT LCD market faces significant restraints, primarily stemming from intense competition with emerging display technologies, particularly Organic Light-Emitting Diodes (OLEDs). OLEDs offer superior contrast ratios, true blacks, faster response times, and thinner form factors, making them increasingly attractive for premium smartphones, high-end televisions, and wearable devices. While TFT LCDs retain a cost advantage, the technological superiority of OLEDs in certain performance aspects leads to market share erosion in high-value segments. This competitive pressure forces TFT LCD manufacturers to innovate continuously, often at significant R&D cost, to maintain their market position and competitiveness, which can constrain profit margins.

Another notable restraint is the cyclical nature of the consumer electronics market and the potential for oversupply. Display manufacturing requires substantial capital investment, and historically, periods of high demand have led to significant capacity expansion. However, if demand growth slows or new capacities come online faster than consumption, it can lead to oversupply, price erosion, and reduced profitability for manufacturers. Additionally, increasing environmental regulations and the rising cost of raw materials, particularly specialized glass substrates and chemicals, present ongoing challenges. Manufacturers must navigate these external pressures, investing in more sustainable practices and efficient material utilization, which can add to operational costs and act as a limiting factor on market expansion and profitability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense competition from alternative display technologies (OLED, Micro-LED) | -1.5% | Global | 2025-2033 |

| Fluctuations in raw material prices and supply chain disruptions | -0.9% | Global, particularly Asian manufacturing hubs | 2025-2033 |

| Mature market in some traditional applications (e.g., standard TVs) | -0.7% | Developed economies (North America, Western Europe) | 2025-2029 |

| Environmental regulations and disposal concerns | -0.4% | Europe, North America, parts of Asia | 2025-2033 |

| High capital expenditure required for manufacturing facilities | -0.3% | Global, affecting new market entrants | 2025-2033 |

TFT LCD Market Opportunities Analysis

Significant opportunities for the TFT LCD market lie in the burgeoning demand for specialized and larger-format displays across various sectors. The automotive industry, undergoing a digital transformation, is increasingly incorporating multiple, complex TFT LCD panels for digital cockpits, rear-seat entertainment, and advanced heads-up displays. These applications require displays that are highly durable, operate reliably across extreme temperatures, and offer exceptional clarity and brightness, presenting a premium segment for TFT LCD manufacturers. Similarly, the expansion of industrial automation, smart retail, and healthcare technology is creating new niches for robust, long-lifecycle TFT LCDs, which often prioritize stability and functionality over ultra-thin form factors, distinguishing them from consumer-grade panels.

Further opportunities emerge from the ongoing technological advancements within TFT LCD manufacturing itself, specifically in areas like Oxide TFT (e.g., IGZO) and Low-Temperature Polycrystalline Silicon (LTPS) TFT technologies. These advancements enable higher pixel densities, improved power efficiency, and faster response times, making TFT LCDs more competitive in applications traditionally dominated by or moving towards OLEDs. Furthermore, the development of flexible and transparent TFT LCDs, though still nascent, opens entirely new application possibilities in areas like smart windows, architectural displays, and advanced wearables. As manufacturing costs for these advanced TFT LCD variants decrease, their broader commercialization could unlock substantial new market segments and sustain long-term growth for the industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of flexible and transparent TFT LCD applications | +1.3% | Global, R&D focused regions (Japan, South Korea, US) | 2028-2033 |

| Increased integration in smart home devices and IoT ecosystems | +1.1% | North America, Europe, Asia Pacific (China) | 2025-2033 |

| Growth in gaming monitors and high-refresh-rate displays | +0.9% | Global, particularly North America, Europe, and Asia Pacific | 2025-2033 |

| Untapped potential in educational technology and professional displays | +0.7% | Emerging economies, education-focused initiatives | 2025-2033 |

| Advancements in Oxide TFT (IGZO) and LTPS technologies | +0.5% | Key manufacturing hubs (China, South Korea, Taiwan, Japan) | 2025-2033 |

TFT LCD Market Challenges Impact Analysis

The TFT LCD market faces persistent challenges from aggressive price competition, particularly within the commodity segments of consumer electronics. The mature nature of TFT LCD technology means that manufacturing processes are highly optimized, leading to a crowded market with numerous players vying for market share. This fierce competition often results in pricing pressures, which can erode profit margins for manufacturers, especially those focusing on standard or lower-end panels. Maintaining profitability in such an environment necessitates continuous cost reduction strategies, including process automation, material efficiency, and economies of scale, all while striving to differentiate products through incremental innovations in performance or features.

Another significant challenge is the rapid pace of technological obsolescence and the need for constant innovation. While TFT LCD remains dominant, the display industry is characterized by continuous research and development into next-generation technologies like Micro-LED and advanced Quantum Dot displays, which promise even higher performance metrics. This constant evolution pressures TFT LCD manufacturers to invest heavily in R&D to improve existing technology (e.g., LTPS, IGZO) and explore new applications, ensuring their offerings remain competitive. Failure to innovate risks losing market share to newer technologies or more advanced TFT LCD variants, making strategic investment in technology and product diversification critical for long-term sustainability in this dynamic market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense price competition in commodity display segments | -1.2% | Global | 2025-2033 |

| High R&D costs for next-generation TFT LCD technologies | -0.8% | Key manufacturing hubs (China, South Korea, Taiwan, Japan) | 2025-2033 |

| Saturated market for certain applications in developed regions | -0.6% | North America, Europe, Japan | 2025-2029 |

| Geopolitical tensions impacting global supply chains and trade | -0.5% | Global, impacting trade routes and raw material sourcing | 2025-2033 |

| Recycling and waste management of display panels | -0.3% | Europe, North America | 2025-2033 |

TFT LCD Market - Updated Report Scope

This market insights report offers a comprehensive analysis of the TFT LCD market, detailing its historical performance, current landscape, and future projections from 2025 to 2033. It encompasses a granular examination of market drivers, restraints, opportunities, and challenges, alongside a thorough segmentation analysis by application, size, technology, resolution, and end-use industry. The report also provides regional insights, highlighting key growth areas and competitive dynamics, and profiles leading market players to offer a holistic understanding of the industry's structure and outlook.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 152.3 Billion |

| Market Forecast in 2033 | USD 258.5 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Display, LG Display, BOE Technology Group Co. Ltd., AU Optronics Corp., Innolux Corporation, Sharp Corporation, Japan Display Inc., Chunghwa Picture Tubes, Tianma Microelectronics Co. Ltd., HannStar Display Corporation, Visionox Technology Inc., China Star Optoelectronics Technology (CSOT), HKC Corporation Limited, CEC Panda LCD Technology Co. Ltd., Panasonic Corporation, NEC Corporation, Sony Corporation, Kyocera Corporation, E Ink Holdings Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The TFT LCD market is intricately segmented to provide a detailed view of its diverse applications and technological nuances. This comprehensive segmentation allows for a granular understanding of demand drivers and market dynamics across various product types and end-use industries. The distinctions in application areas, display sizes, underlying panel technologies, and resolution capabilities each contribute uniquely to the market's overall growth trajectory and competitive landscape, highlighting both mature segments and emerging high-growth opportunities.

- By Application: This segment categorizes TFT LCDs based on their primary use, encompassing high-volume consumer devices such as Smartphones, Televisions, Laptops & Tablets, alongside specialized and professional applications like Automotive Displays for infotainment and digital dashboards, Industrial Displays for control panels and machinery, Medical Devices for diagnostic and monitoring equipment, Wearable Devices for smartwatches and fitness trackers, Digital Signage for advertising and information dissemination, and displays for Avionics & Military purposes.

- By Size: This segmentation broadly divides the market into Small & Medium Displays, typically characterized as under 10 inches and prevalent in smartphones, wearables, and smaller industrial devices, and Large Displays, which are 10 inches and above, commonly found in televisions, laptops, monitors, and automotive central consoles.

- By Technology: This segment delves into the core material technologies underpinning TFT LCDs, including Amorphous Silicon (a-Si) TFT-LCD, which is widely used due to its cost-effectiveness and mature manufacturing processes; Low-Temperature Polycrystalline Silicon (LTPS) TFT-LCD, known for enabling higher pixel densities and more compact designs, often found in high-end smartphones; and Oxide TFT-LCD, specifically Indium Gallium Zinc Oxide (IGZO) TFT-LCD, which offers superior electron mobility, leading to higher resolution, lower power consumption, and improved touch sensitivity.

- By Resolution: Categorization by resolution includes standard definitions like HD (High Definition) and Full HD, progressing to higher pixel counts such as Quad HD, 4K UHD (Ultra High Definition), and the most advanced 8K UHD, reflecting the market's trend towards greater visual clarity and immersive experiences.

- By End-Use Industry: This segmentation groups the market by the industry consuming the TFT LCD panels, ranging from the vast Consumer Electronics sector to the rapidly expanding Automotive industry, the critical Healthcare sector, diverse Industrial applications, the Retail industry for point-of-sale and digital signage, the Education sector for interactive whiteboards and learning devices, and specialized applications in Aerospace & Defense.

Regional Highlights

The Asia Pacific (APAC) region continues to be the dominant force in the global TFT LCD market, both in terms of manufacturing capacity and consumption. Countries like China, South Korea, Taiwan, and Japan host the world's largest display panel fabrication facilities, benefiting from robust governmental support, significant investments in advanced manufacturing technologies, and a highly skilled labor force. China, in particular, has emerged as a powerhouse, with massive investments leading to significant capacity expansion and technological advancements, catering to its huge domestic market for consumer electronics and exporting extensively. South Korea and Taiwan, while facing increased competition from China, continue to drive innovation in high-end and specialized TFT LCD panels, leveraging their strong R&D capabilities and established supply chains. This region's large population, increasing disposable incomes, and rapid urbanization contribute to a burgeoning demand for display-integrated devices across various sectors.

North America and Europe represent significant markets for TFT LCD consumption, driven by high demand for premium consumer electronics, automotive displays, and advanced industrial and medical applications. In North America, the early adoption of smart technologies, coupled with the presence of major technology companies, fuels the demand for high-performance and innovative display solutions. The automotive sector in both regions is a key growth area, with the increasing integration of sophisticated in-car display systems. Europe, known for its stringent quality standards and focus on industrial automation, also exhibits strong demand for robust and reliable TFT LCD panels in manufacturing, healthcare, and digital signage. While these regions are not primary manufacturing hubs for large-scale panel production, they are crucial for driving product innovation, setting market trends, and adopting cutting-edge display technologies.

Latin America, the Middle East, and Africa (MEA) are emerging markets for TFT LCDs, characterized by growing economies, increasing internet penetration, and a rising middle class. The demand in these regions is primarily driven by the expanding consumer electronics market, particularly affordable smartphones and televisions. Governments in some MEA countries are also investing in smart city initiatives and digital infrastructure, which could spur demand for digital signage and public displays. While these regions currently represent a smaller share of the global market, their potential for future growth is considerable as economic development and technological adoption continue to accelerate, offering new opportunities for manufacturers and distributors of TFT LCD products.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the TFT LCD Market.- Samsung Display Co. Ltd.

- LG Display Co. Ltd.

- BOE Technology Group Co. Ltd.

- AU Optronics Corp. (AUO)

- Innolux Corporation

- Sharp Corporation

- Japan Display Inc. (JDI)

- Tianma Microelectronics Co. Ltd.

- HannStar Display Corporation

- Visionox Technology Inc.

- China Star Optoelectronics Technology (CSOT)

- HKC Corporation Limited

- Chunghwa Picture Tubes (CPT)

- CEC Panda LCD Technology Co. Ltd.

- Panasonic Corporation

- NEC Corporation

- Sony Corporation

- Kyocera Corporation

- E Ink Holdings Inc.

Frequently Asked Questions

What is the projected growth rate of the TFT LCD market?

The TFT LCD market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033, reaching an estimated value of USD 258.5 billion by 2033 from USD 152.3 billion in 2025.

What are the primary drivers for the TFT LCD market?

Key drivers include the expanding demand for consumer electronics like smartphones and televisions, the increasing integration of displays in automotive systems, and rising adoption in industrial, medical, and digital signage applications.

How is AI impacting the TFT LCD industry?

AI is enhancing TFT LCD manufacturing efficiency through predictive maintenance and improved defect detection, while also optimizing display performance and user experience through real-time image processing and adaptive parameter adjustments.

Which region dominates the TFT LCD market?

The Asia Pacific (APAC) region dominates the TFT LCD market, driven by its extensive manufacturing capabilities in countries like China, South Korea, and Taiwan, as well as its large consumer base and rapid technological adoption.

What are the key technological trends in TFT LCDs?

Major technological trends include the proliferation of high-resolution (4K/8K) panels, advancements in thinner and more energy-efficient designs, and the development of specialized TFT LCDs using LTPS and Oxide TFT (IGZO) technologies for enhanced performance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted