System Integration Service Market

System Integration Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703977 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

System Integration Service Market Size

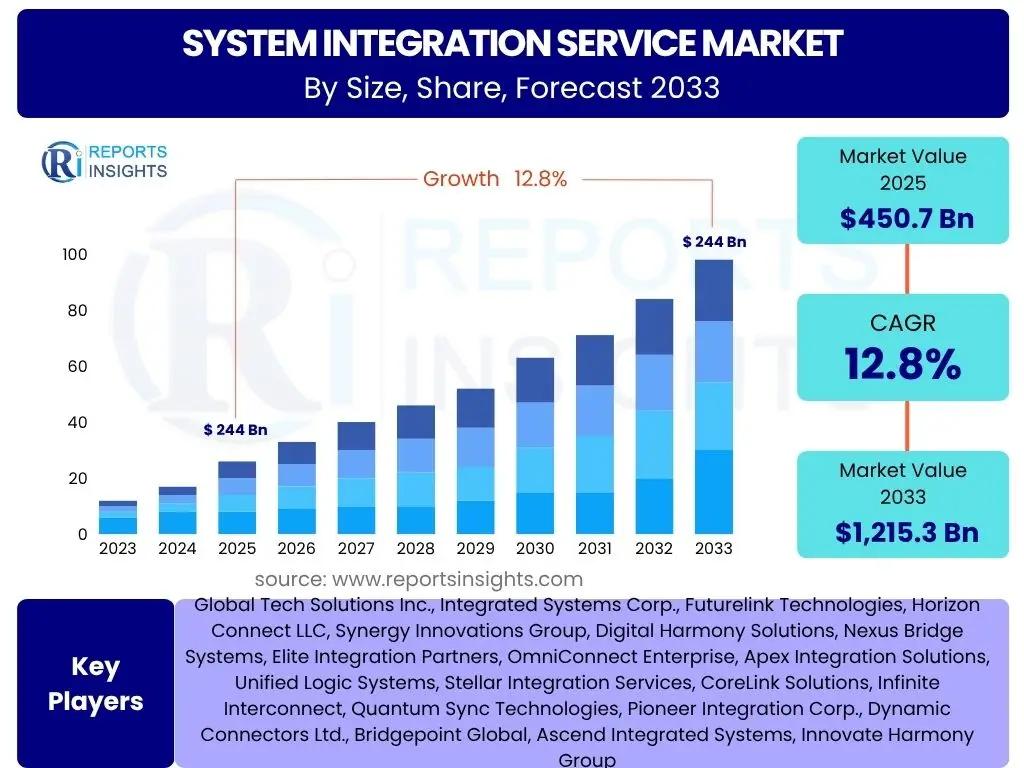

According to Reports Insights Consulting Pvt Ltd, The System Integration Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 450.7 Billion in 2025 and is projected to reach USD 1,215.3 Billion by the end of the forecast period in 2033.

Key System Integration Service Market Trends & Insights

The System Integration Service market is undergoing significant transformation driven by the escalating complexity of enterprise IT environments and the relentless pace of digital innovation. Common user inquiries often revolve around the most impactful technological shifts, such as the widespread adoption of cloud-native architectures, the proliferation of Internet of Things (IoT) devices, and the increasing reliance on data analytics. Enterprises are actively seeking solutions that can seamlessly connect disparate systems, applications, and data sources to enhance operational efficiency, improve decision-making, and create superior customer experiences. The drive towards hyper-automation and intelligent workflows is also a dominant theme, pushing organizations to integrate robotic process automation (RPA) and artificial intelligence (AI) capabilities into their core business processes.

Another prominent trend attracting user interest is the shift towards microservices architecture and API-first development. This modular approach allows for greater flexibility, scalability, and faster deployment cycles compared to traditional monolithic systems. Organizations are recognizing that a robust API strategy is foundational for effective system integration, enabling smooth communication between internal and external services. Furthermore, the imperative for enhanced cybersecurity within integrated environments is growing. As more systems connect, the attack surface expands, leading to increased demand for security integration services that embed protective measures at every layer of the IT infrastructure. This includes identity and access management, data encryption, and threat intelligence integration.

The rise of industry-specific platforms and vertical integration solutions is also a notable trend. Businesses in sectors such as healthcare, finance, and manufacturing are seeking highly specialized integration services that cater to their unique regulatory requirements, data formats, and operational workflows. This customization allows for deeper optimization and ensures compliance, driving the demand for integrators with specific domain expertise. The market is also seeing a greater emphasis on outcome-based service models, where clients prioritize business results over traditional input-based contracts, fostering a more collaborative and strategic partnership with integration service providers.

- Increased adoption of cloud-native and hybrid cloud integration.

- Growth in demand for API-led connectivity and microservices architecture.

- Heightened focus on cybersecurity integration within complex IT landscapes.

- Proliferation of IoT devices necessitating robust data integration frameworks.

- Emphasis on hyper-automation and intelligent process integration.

- Shift towards industry-specific and vertical integration solutions.

- Demand for real-time data integration and analytics capabilities.

AI Impact Analysis on System Integration Service

The integration of Artificial Intelligence (AI) is fundamentally reshaping the System Integration Service market, addressing critical user concerns regarding efficiency, complexity, and predictive capabilities. Users frequently inquire about how AI can automate integration tasks, reduce human error, and accelerate project timelines. AI-powered tools are now being deployed to analyze system logs, identify data discrepancies, and even generate integration code snippets, significantly streamlining the development and deployment process. Furthermore, AI's ability to learn from vast datasets enables integrators to predict potential system conflicts or performance bottlenecks before they occur, shifting the paradigm from reactive troubleshooting to proactive maintenance and optimization.

A key aspect of AI's impact is its role in enhancing data integration and quality. User questions often highlight the challenges of unifying disparate data sources and ensuring data accuracy for advanced analytics. AI algorithms are proving invaluable in this domain, offering intelligent data mapping, transformation, and validation capabilities. Machine learning models can automatically identify patterns in diverse data structures, suggest optimal data flows, and cleanse data, ensuring a higher level of data integrity essential for business intelligence and operational excellence. This intelligent data handling capability is crucial for organizations striving to leverage big data for strategic insights.

Moreover, AI is facilitating the creation of more intelligent and adaptive integrated systems, addressing user expectations for dynamic and self-optimizing IT infrastructures. AI-driven orchestration platforms can monitor system performance, intelligently route workloads, and even autonomously scale resources based on real-time demands. This enables a more resilient and efficient IT ecosystem, reducing the need for manual intervention and improving overall system reliability. The convergence of AI with other emerging technologies, such as edge computing and blockchain, is also opening new avenues for complex, distributed system integrations that can operate with unprecedented levels of autonomy and security, representing a significant leap forward for the industry.

- Automated data mapping, transformation, and validation processes.

- Predictive analytics for identifying integration risks and bottlenecks.

- Enhanced intelligent process automation (IPA) and robotic process automation (RPA).

- Optimization of resource allocation and workload management in integrated environments.

- Facilitation of cognitive integration and self-optimizing systems.

- Improved anomaly detection and security posture through AI-driven insights.

Key Takeaways System Integration Service Market Size & Forecast

Common user questions regarding the System Integration Service market forecast emphasize understanding the driving forces behind its robust growth and the strategic implications for businesses. A primary takeaway is the indispensable role of system integration in enabling digital transformation initiatives across all sectors. As enterprises continue to adopt cloud computing, IoT, AI, and other advanced technologies, the complexity of their IT landscapes escalates, making seamless integration a critical success factor rather than an optional add-on. The projected significant growth underscores that businesses are increasingly prioritizing comprehensive integration strategies to unlock efficiency, innovation, and competitive advantage.

Another crucial insight from the market forecast is the shift towards agile and flexible integration methodologies. Users are keen to understand how the market is adapting to rapid technological evolution. The strong CAGR indicates a move away from traditional, lengthy integration projects towards more modular, API-driven approaches that allow for faster deployment and easier scalability. This flexibility is essential for organizations seeking to quickly adapt to market changes and implement new digital services without disrupting existing operations. The forecast reflects a growing recognition that effective integration reduces technical debt and accelerates time-to-market for new products and services.

Finally, the forecast highlights the increasing specialization within the system integration service domain. While general integration services remain vital, the market is seeing a surge in demand for expertise in specific areas such as cybersecurity integration, industry-specific platform integration, and data analytics integration. This specialization reflects the nuanced needs of various industries and the evolving threat landscape. The projected market size signifies a mature yet rapidly expanding market where service providers with deep vertical knowledge and proficiency in cutting-edge technologies will be best positioned for success, offering tailored solutions that deliver tangible business outcomes.

- Digital transformation is the primary growth catalyst, making integration non-negotiable.

- The market exhibits robust and sustained growth, signaling high demand for connectivity.

- Shift towards agile, API-first, and cloud-native integration approaches is accelerating.

- Specialized integration services (e.g., cybersecurity, AI, industry-specific) are gaining prominence.

- Investment in integration solutions is key for operational efficiency and competitive advantage.

- Market expansion is driven by complexity reduction and value creation for enterprises.

System Integration Service Market Drivers Analysis

The System Integration Service market is propelled by several robust drivers, primarily stemming from the pervasive digital transformation initiatives across industries. The relentless pursuit of operational efficiency and competitive differentiation compels organizations to integrate disparate systems, applications, and data sources. The widespread adoption of cloud computing, including hybrid and multi-cloud environments, necessitates sophisticated integration solutions to ensure seamless data flow and application interoperability between on-premise infrastructure and various cloud platforms. This fundamental shift in IT architecture is a core driver for integration services, as businesses seek to leverage the scalability and flexibility of the cloud without creating data silos or operational friction.

Furthermore, the exponential growth of data generated from diverse sources, such as IoT devices, customer interactions, and enterprise applications, mandates advanced data integration capabilities. Organizations are increasingly aware of the strategic value hidden within their data, driving demand for services that can consolidate, transform, and analyze this information for actionable insights. The imperative for enhanced cybersecurity also acts as a significant driver; as systems become more interconnected, the attack surface expands, leading to a critical need for integrated security solutions that provide comprehensive threat protection and compliance management. Compliance with evolving regulatory frameworks, such as GDPR and industry-specific mandates, further drives the need for robust data governance and security integration.

The increasing complexity of modern IT landscapes, characterized by a mix of legacy systems, new applications, and third-party solutions, inherently drives the demand for integration expertise. Enterprises often struggle with interoperability issues and data inconsistencies, making professional integration services essential for creating a cohesive and functional IT ecosystem. The need for real-time information exchange and intelligent automation, fueled by advancements in AI and Machine Learning, also contributes significantly to market growth. Businesses are seeking to automate processes and enable intelligent decision-making, which fundamentally relies on seamless, real-time integration of data and applications across the enterprise value chain.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Transformation Initiatives | +3.5% | Global, particularly North America, Europe, Asia Pacific | Short to Long Term (2025-2033) |

| Cloud Adoption and Hybrid IT Environments | +2.8% | Global, all major economies | Short to Medium Term (2025-2029) |

| Proliferation of IoT and Data Volume Growth | +2.2% | Asia Pacific, North America, Europe | Medium to Long Term (2026-2033) |

| Demand for Enhanced Cybersecurity & Compliance | +1.8% | Global, highly relevant in regulated industries | Short to Medium Term (2025-2030) |

| Complexity of Enterprise IT Landscapes | +1.5% | All developed and emerging markets | Short to Long Term (2025-2033) |

System Integration Service Market Restraints Analysis

Despite robust growth, the System Integration Service market faces several significant restraints that can impede its full potential. One primary challenge is the high initial cost and complexity associated with large-scale integration projects. Organizations, particularly Small and Medium-sized Enterprises (SMEs), may find the upfront investment in integrating diverse systems prohibitive, leading to delayed adoption or a preference for fragmented, point solutions. The extensive planning, custom development, and testing required for complex integrations contribute to these substantial costs and project durations, which can be a deterrent for budget-conscious entities.

Another major restraint is the pervasive concern regarding data security and privacy during the integration process. Merging data from multiple sources often involves handling sensitive information, raising fears of data breaches, compliance violations, and intellectual property theft. Enterprises are hesitant to expose critical data during transit or within integrated environments, leading to increased scrutiny and extended due diligence periods that slow down project execution. This issue is compounded by the evolving landscape of data privacy regulations worldwide, requiring integrators to navigate complex legal and ethical considerations.

Furthermore, the scarcity of skilled integration professionals with expertise across various platforms, technologies, and industry verticals presents a significant bottleneck. The demand for professionals proficient in areas such as cloud integration, API management, and cybersecurity integration often outstrips supply, leading to higher labor costs and delays in project implementation. This talent gap can compel organizations to either outsource extensively or compromise on the quality of integration, ultimately hindering the market's expansion. Vendor lock-in issues, where reliance on specific proprietary systems makes integration with other platforms difficult and costly, also pose a considerable restraint, limiting flexibility and interoperability for businesses.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Costs and Project Complexity | -1.5% | Global, impacts SMEs more significantly | Short to Medium Term (2025-2029) |

| Data Security and Privacy Concerns | -1.2% | Global, highly relevant in regulated industries | Short to Long Term (2025-2033) |

| Lack of Skilled Integration Professionals | -1.0% | Global, prominent in emerging markets | Medium Term (2026-2030) |

| Legacy System Modernization Challenges | -0.8% | Mature markets with extensive legacy infrastructure | Short to Medium Term (2025-2030) |

System Integration Service Market Opportunities Analysis

The System Integration Service market is poised for significant growth driven by several emerging opportunities that capitalize on technological advancements and evolving business needs. The expansion of the Internet of Things (IoT) across various sectors, from smart manufacturing to connected healthcare, creates a substantial opportunity for integrators. Each IoT deployment generates vast amounts of data that must be seamlessly integrated with enterprise systems for analysis and automation, requiring specialized services to connect diverse devices, platforms, and applications. This represents a nascent but rapidly expanding segment within the integration landscape, offering new revenue streams for service providers capable of handling distributed and real-time data flows.

Another compelling opportunity lies in the increasing adoption of Artificial Intelligence (AI) and Machine Learning (ML) within enterprise operations. Integrating AI/ML capabilities into existing business processes and applications allows organizations to unlock advanced analytics, predictive insights, and intelligent automation. This extends beyond simple data integration to encompass the integration of AI models, algorithms, and cognitive services, enabling smarter decision-making and operational efficiencies. Service providers adept at leveraging AI for intelligent process automation (IPA) and cognitive integration are well-positioned to meet this growing demand, driving innovation across various industries.

Furthermore, the rising demand for industry-specific and vertical-focused integration solutions presents a lucrative opportunity. While horizontal integration addresses general IT needs, businesses are increasingly seeking tailored integration services that cater to their unique regulatory requirements, operational workflows, and domain-specific applications. This includes specialized integration for healthcare systems, financial trading platforms, smart city infrastructure, and advanced manufacturing execution systems. By developing deep expertise in specific verticals, integrators can offer higher-value, customized solutions that address precise business challenges and foster stronger, long-term client relationships. The shift towards managed integration services and platform-as-a-service (PaaS) models also offers opportunities for recurring revenue and scalable solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in IoT and Edge Computing Integration | +2.5% | Global, strong in manufacturing, smart cities, healthcare | Medium to Long Term (2026-2033) |

| Increasing AI/ML Integration for Intelligent Automation | +2.0% | Global, particularly in technologically advanced regions | Medium to Long Term (2026-2033) |

| Demand for Industry-Specific and Vertical Solutions | +1.8% | Global, driven by sector-specific digital transformation | Short to Long Term (2025-2033) |

| Managed Integration Services and iPaaS Adoption | +1.5% | North America, Europe, rapidly growing in APAC | Short to Medium Term (2025-2030) |

System Integration Service Market Challenges Impact Analysis

The System Integration Service market faces several formidable challenges that can impact its growth trajectory and operational efficiency. One significant hurdle is the persistent issue of integrating diverse legacy systems with modern cloud-native applications and microservices. Many organizations operate with deeply embedded, monolithic legacy infrastructure that lacks modern APIs or documentation, making seamless integration incredibly complex, time-consuming, and prone to errors. Overcoming these interoperability challenges often requires extensive custom development and workarounds, driving up project costs and increasing the risk of delays, thereby impacting the perceived value and ROI of integration projects.

Another critical challenge is ensuring robust data governance and security across a multitude of integrated systems. As data flows between various applications, databases, and cloud environments, maintaining consistent data quality, compliance with regulations (such as GDPR, HIPAA), and protection against cyber threats becomes increasingly difficult. The risk of data breaches, unauthorized access, and non-compliance rises with each additional integration point, demanding sophisticated security measures, stringent access controls, and comprehensive auditing capabilities. Addressing these concerns adds layers of complexity and cost to integration projects, requiring specialized expertise in data security and regulatory compliance.

Furthermore, managing vendor fragmentation and avoiding vendor lock-in poses a significant challenge. The integration landscape is characterized by a multitude of software vendors, platform providers, and service providers, each offering proprietary solutions and APIs. Organizations often find themselves locked into specific technologies, which can hinder future flexibility, increase switching costs, and complicate efforts to integrate with new or alternative systems. This requires integrators to possess broad expertise across various vendor ecosystems and develop strategies to minimize dependencies, ensuring client agility. The rapid pace of technological change also presents a continuous challenge, requiring integration service providers to constantly update their skills and adopt new methodologies to remain relevant and effective.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Legacy System Integration & Interoperability Issues | -1.8% | Mature markets (North America, Europe) with older infrastructures | Short to Long Term (2025-2033) |

| Data Governance and Security Complexities | -1.5% | Global, critical in highly regulated sectors | Short to Long Term (2025-2033) |

| Vendor Fragmentation and Lock-in | -1.0% | Global, especially prevalent in competitive markets | Medium Term (2026-2030) |

| Rapid Pace of Technological Change | -0.7% | Global, impacts service provider agility | Short to Long Term (2025-2033) |

System Integration Service Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global System Integration Service Market, covering market size estimations, historical data from 2019-2023, and detailed forecasts up to 2033. It examines key market trends, drivers, restraints, opportunities, and challenges influencing market dynamics. The report offers a granular segmentation analysis across various service types, deployment models, organization sizes, and industry verticals, providing detailed insights into sub-segments. Furthermore, it highlights regional market performance and profiles leading market players, offering a holistic view for stakeholders seeking to understand market potential, strategic insights, and competitive landscapes within the system integration sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450.7 Billion |

| Market Forecast in 2033 | USD 1,215.3 Billion |

| Growth Rate | 12.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Tech Solutions Inc., Integrated Systems Corp., Futurelink Technologies, Horizon Connect LLC, Synergy Innovations Group, Digital Harmony Solutions, Nexus Bridge Systems, Elite Integration Partners, OmniConnect Enterprise, Apex Integration Solutions, Unified Logic Systems, Stellar Integration Services, CoreLink Solutions, Infinite Interconnect, Quantum Sync Technologies, Pioneer Integration Corp., Dynamic Connectors Ltd., Bridgepoint Global, Ascend Integrated Systems, Innovate Harmony Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The System Integration Service market is broadly segmented to provide a detailed understanding of its diverse applications and operational models. This segmentation allows for a granular analysis of specific market dynamics, technological preferences, and industry-specific demands across various verticals. By categorizing the market based on service type, deployment model, organization size, and vertical, the report offers comprehensive insights into where integration efforts are concentrated and how different market participants are responding to evolving business and technological landscapes. This multi-dimensional view aids in identifying high-growth areas and understanding the varied needs of end-users.

The segmentation by service type reflects the wide array of integration solutions available, from foundational infrastructure and application integration to advanced data and cloud integration, and specialized services like security and business process integration. Deployment model segmentation highlights the ongoing shift towards cloud-based and hybrid solutions, while organization size analysis differentiates between the integration needs and spending patterns of SMEs versus large enterprises. Lastly, the vertical segmentation underscores the critical role of industry-specific knowledge in delivering tailored and effective integration solutions, catering to the unique challenges and opportunities within sectors such as BFSI, healthcare, manufacturing, and IT & Telecom.

- By Service Type: This segment includes Consulting, Infrastructure Integration, Application Integration, Data Integration, Business Process Integration, Cloud Integration, Network Integration, Security Integration, and Managed Services, reflecting the comprehensive nature of integration offerings.

- By Deployment Model: Categorized into On-Premise, Cloud-Based, and Hybrid, illustrating the varied architectural preferences of enterprises.

- By Organization Size: Divided into Small & Medium Enterprises (SMEs) and Large Enterprises, highlighting distinct market needs and investment capacities.

- By Vertical: Encompasses diverse industries such as Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecommunications, Manufacturing, Retail and E-commerce, Government and Public Sector, Energy and Utilities, Media and Entertainment, and Transportation and Logistics, recognizing industry-specific integration demands.

Regional Highlights

- North America: This region is a leading market for system integration services, driven by early adoption of advanced technologies like cloud computing, AI, and IoT, coupled with significant investments in digital transformation across various industries. The presence of a large number of enterprises and technology providers, along with robust IT infrastructure, contributes to its dominant market share. High demand from sectors like BFSI, healthcare, and IT & telecom fuels continuous growth.

- Europe: Characterized by stringent data privacy regulations (e.g., GDPR) and a strong focus on industrial automation and smart manufacturing (Industry 4.0), Europe exhibits a substantial demand for secure and compliant system integration services. Countries like Germany, the UK, and France are at the forefront of adopting complex integration solutions, especially in manufacturing, automotive, and public sectors.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market, primarily due to rapid digitalization across emerging economies like China, India, and Southeast Asian countries. Increasing investments in IT infrastructure, burgeoning manufacturing and retail sectors, and the widespread adoption of cloud services and mobile technologies are propelling the demand for system integration. Government initiatives supporting digital transformation also play a crucial role.

- Latin America: While a developing market, Latin America is experiencing increasing adoption of cloud services and digital solutions, leading to a growing need for system integration. Countries like Brazil and Mexico are key contributors, driven by modernization efforts in BFSI, retail, and public sectors, though economic volatilities can influence market pace.

- Middle East and Africa (MEA): This region is witnessing steady growth in system integration, largely due to government-led digital initiatives, smart city projects, and diversification efforts away from oil-dependent economies. Significant investments in IT and telecom infrastructure, particularly in the UAE, Saudi Arabia, and South Africa, are creating substantial opportunities for integration service providers, focusing on sectors like government, energy, and healthcare.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the System Integration Service Market.- Global Tech Solutions Inc.

- Integrated Systems Corp.

- Futurelink Technologies

- Horizon Connect LLC

- Synergy Innovations Group

- Digital Harmony Solutions

- Nexus Bridge Systems

- Elite Integration Partners

- OmniConnect Enterprise

- Apex Integration Solutions

- Unified Logic Systems

- Stellar Integration Services

- CoreLink Solutions

- Infinite Interconnect

- Quantum Sync Technologies

- Pioneer Integration Corp.

- Dynamic Connectors Ltd.

- Bridgepoint Global

- Ascend Integrated Systems

- Innovate Harmony Group

Frequently Asked Questions

What is System Integration Service and why is it important?

System Integration Service involves connecting various IT systems, applications, and data sources within an organization to enable them to function as a unified, cohesive whole. It is crucial for enhancing operational efficiency, streamlining workflows, improving data accuracy, and supporting digital transformation initiatives by breaking down information silos and ensuring seamless communication across an enterprise's technological landscape.

What are the primary drivers of the System Integration Service market growth?

The key drivers include the escalating complexity of enterprise IT environments, the widespread adoption of cloud computing (hybrid and multi-cloud), the proliferation of IoT devices, the imperative for digital transformation, and the increasing demand for enhanced cybersecurity and data governance across interconnected systems. These factors necessitate expert integration to achieve business objectives.

How is AI impacting the System Integration Service market?

AI is profoundly impacting the market by enabling intelligent automation of integration tasks, enhancing data mapping and transformation processes, providing predictive analytics for potential system issues, and facilitating the development of self-optimizing integrated environments. AI-driven solutions are improving efficiency, reducing errors, and accelerating integration project timelines.

What challenges does the System Integration Service market face?

Major challenges include the high initial costs and complexity of large-scale integration projects, persistent issues with integrating legacy systems, significant concerns regarding data security and privacy during data exchange, the scarcity of skilled integration professionals, and vendor fragmentation leading to potential lock-in. These factors can hinder project execution and adoption.

Which industries are showing the highest demand for System Integration Services?

Industries demonstrating high demand include Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecommunications, Manufacturing, and Retail and E-commerce. These sectors are undergoing significant digital transformation, requiring extensive integration to modernize operations, improve customer experience, and ensure regulatory compliance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted