Synchronous Buck Converter Market

Synchronous Buck Converter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678201 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

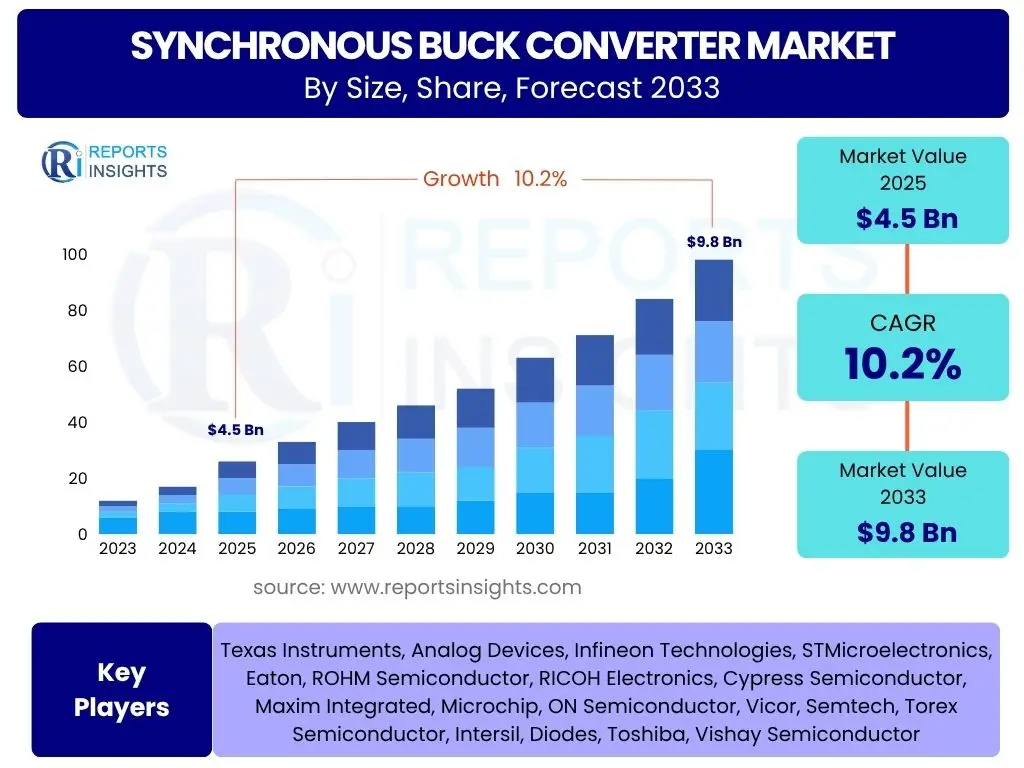

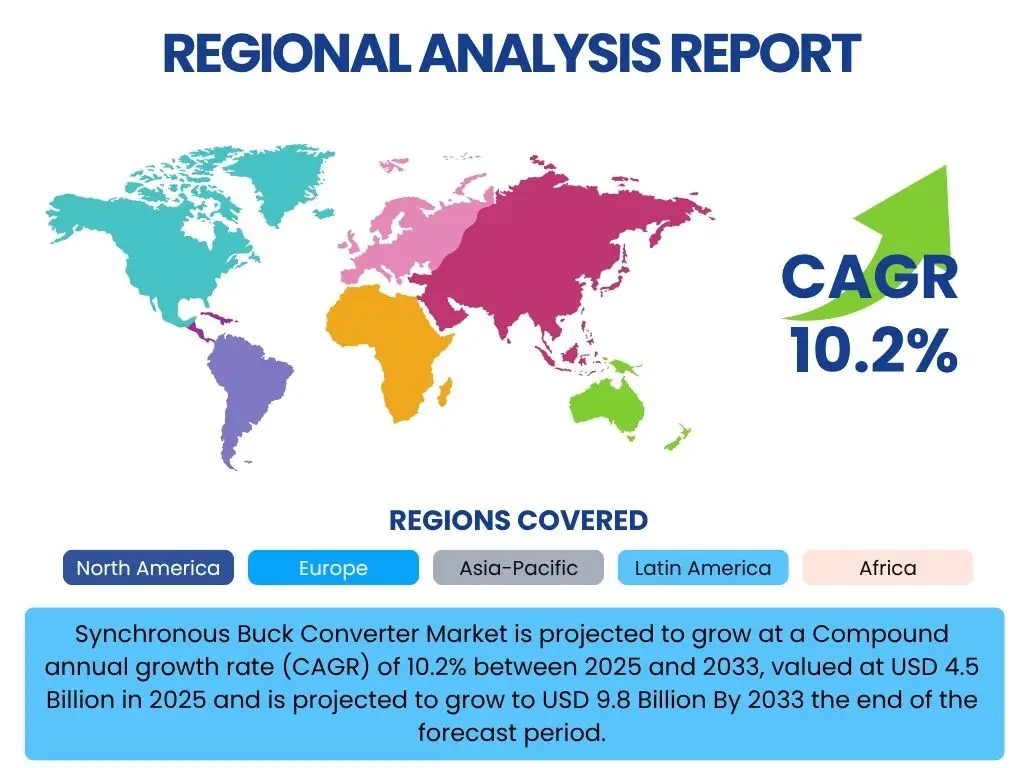

Synchronous Buck Converter Market is projected to grow at a Compound annual growth rate (CAGR) of 10.2% between 2025 and 2033, valued at USD 4.5 Billion in 2025 and is projected to grow to USD 9.8 Billion By 2033 the end of the forecast period.

Key Synchronous Buck Converter Market Trends & Insights

The synchronous buck converter market is experiencing robust growth driven by several pervasive technological advancements and shifting industry demands. A significant trend is the relentless pursuit of higher power efficiency across all electronic devices, from consumer gadgets to industrial machinery. Synchronous buck converters inherently offer superior efficiency compared to their asynchronous counterparts, making them indispensable in applications where minimizing power loss and heat dissipation is critical. This efficiency gain translates directly into longer battery life for portable devices and reduced operational costs for large-scale systems, establishing a fundamental market pull. Miniaturization is another dominant trend, with consumers and industries demanding smaller, lighter, and more compact electronic solutions. Manufacturers of synchronous buck converters are continuously innovating to reduce the form factor of these components while maintaining or even improving performance, often integrating more functionalities into a single chip. The rise of new high-power density materials like Gallium Nitride (GaN) and Silicon Carbide (SiC) is revolutionizing converter design, enabling higher switching frequencies, greater efficiency, and smaller overall footprints. These materials are particularly impactful in high-power applications such as electric vehicles, renewable energy systems, and data centers. The proliferation of the Internet of Things (IoT) devices, wearable technology, and advanced driver-assistance systems (ADAS) in automotive applications further fuels the demand for compact, efficient, and reliable power management solutions, positioning synchronous buck converters at the forefront of these technological waves.

- Increased demand for energy-efficient power management solutions.

- Miniaturization and integration of components for compact designs.

- Adoption of wide-bandgap materials like GaN and SiC for higher performance.

- Growing application in automotive electronics, particularly EVs and ADAS.

- Expansion of IoT devices and smart infrastructure requiring precise power delivery.

- Focus on higher power density and reduced thermal footprint.

- Development of intelligent power management ICs with digital control.

- Surge in demand from data centers and cloud computing infrastructure.

- Evolution towards higher switching frequencies for smaller magnetics.

- Enhanced reliability and thermal management solutions for demanding environments.

AI Impact Analysis on Synchronous Buck Converter

Artificial Intelligence (AI) is exerting a transformative impact on the synchronous buck converter market, influencing both the demand for these components and their design and optimization. The proliferation of AI-driven systems, ranging from advanced processors in data centers to edge AI devices and sophisticated automotive infotainment units, inherently requires highly efficient, stable, and precise power delivery. AI accelerators, often operating at very low core voltages but drawing significant current, necessitate power supplies that can respond rapidly to dynamic load changes without compromising efficiency. Synchronous buck converters are ideally suited for these applications due to their ability to deliver high current with low ripple and excellent transient response, making them a critical enabler for the widespread adoption of AI hardware. Furthermore, AI is increasingly being leveraged within the design and manufacturing processes of the converters themselves. Machine learning algorithms can optimize control loops, predict component failures, and even automate aspects of circuit layout, leading to more robust, efficient, and cost-effective converter designs. This integration of AI not only enhances the performance characteristics of the converters but also accelerates their development cycle, allowing manufacturers to bring innovative power solutions to market more quickly.

- Increased demand for high-efficiency, high-current power delivery in AI accelerators and processors.

- AI and machine learning optimizing converter design for efficiency and transient response.

- Enhanced power management in edge AI devices and intelligent systems.

- Development of adaptive power solutions for dynamic AI workload requirements.

- AI-driven testing and quality control improving converter reliability.

- Predictive maintenance for power systems utilizing synchronous buck converters.

- Integration of digital control with AI algorithms for smarter power regulation.

- Growth in AI-powered data centers driving demand for efficient power conversion.

- New application areas emerging with the rise of AI in robotics, autonomous vehicles, and smart cities.

Key Takeaways Synchronous Buck Converter Market Size & Forecast

- The global Synchronous Buck Converter Market is projected to reach USD 9.8 Billion by 2033, growing from USD 4.5 Billion in 2025.

- The market is expected to exhibit a robust Compound Annual Growth Rate (CAGR) of 10.2% from 2025 to 2033.

- Key growth drivers include the escalating demand for energy-efficient portable electronics, the expansion of electric vehicles (EVs) and hybrid electric vehicles (HEVs), and the rapid deployment of cloud infrastructure and data centers.

- Technological advancements in wide-bandgap materials such as Gallium Nitride (GaN) and Silicon Carbide (SiC) are significantly enhancing converter performance and driving market expansion.

- Miniaturization trends across consumer electronics and industrial applications are fostering the adoption of compact and highly integrated synchronous buck converter solutions.

- Asia Pacific is anticipated to remain the dominant region, driven by strong manufacturing bases for consumer electronics and automotive industries.

- Challenges such as design complexity and cost pressures from competitive solutions may temper growth, yet opportunities in emerging applications and regions persist.

- The market forecast indicates sustained demand for precise, reliable, and high-density power conversion solutions across diverse end-use industries.

Synchronous Buck Converter Market Drivers Impact Analysis

The synchronous buck converter market is significantly influenced by a confluence of powerful drivers that are pushing the boundaries of power management technology. The overarching demand for energy efficiency across all electronic devices, from smartphones to industrial machinery, stands as a primary catalyst. Synchronous buck converters, by their nature, minimize power loss and heat generation, making them essential components in green electronics initiatives and for extending battery life in portable applications. The rapid expansion of automotive electronics, particularly in the realm of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), creates substantial demand for robust and efficient power solutions. These applications require precise voltage regulation for various subsystems, including infotainment, lighting, and sensor arrays, where synchronous buck converters excel. Moreover, the global proliferation of Internet of Things (IoT) devices, smart home appliances, and wearable technology, each demanding compact, low-power, and reliable power conversion, further fuels market growth. The ongoing build-out of data centers and cloud computing infrastructure also contributes significantly, as these facilities require highly efficient power delivery to optimize energy consumption and reduce operational costs. Lastly, advancements in semiconductor materials and manufacturing processes are enabling higher performance and smaller form factors, making synchronous buck converters even more attractive for diverse applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Energy-Efficient Devices | +2.5% | Global, especially North America, Europe, Asia Pacific | Long-term |

| Expansion of Automotive Electronics (EVs, ADAS) | +2.0% | Europe, Asia Pacific (China, Japan, South Korea), North America | Medium to Long-term |

| Proliferation of IoT Devices and Wearables | +1.8% | Global, high concentration in Asia Pacific (manufacturing) and North America (adoption) | Medium-term |

| Increased Investment in Data Centers and Cloud Infrastructure | +1.5% | North America, Europe, Asia Pacific (especially China, India) | Medium to Long-term |

| Advancements in Semiconductor Manufacturing Technologies (e.g., GaN, SiC) | +1.2% | Global, driven by technology hubs in North America, Europe, Asia Pacific (Taiwan, Japan, South Korea) | Short to Medium-term |

| Rise of Portable and Battery-Powered Devices | +1.0% | Global, with high consumer electronics production in Asia Pacific | Long-term |

| Growing Demand for Industrial Automation and Robotics | +0.8% | Europe, North America, Asia Pacific (China, Japan, South Korea, Germany) | Medium-term |

Synchronous Buck Converter Market Restraints Impact Analysis

While the synchronous buck converter market benefits from numerous growth drivers, several restraints could impede its expansion. One significant challenge is the inherent design complexity associated with these converters, particularly when optimizing for high efficiency, compact size, and specific thermal profiles. Achieving optimal performance often requires sophisticated control algorithms and careful component selection, increasing design time and potentially development costs. The increasing cost of raw materials and specialized components, such as high-frequency switching transistors or advanced magnetics, can also put upward pressure on the manufacturing cost of synchronous buck converters, making them less competitive against simpler, albeit less efficient, power solutions in certain price-sensitive applications. Furthermore, intense price competition within the highly fragmented power management IC market can limit profit margins for manufacturers and hinder investment in research and development for cutting-edge technologies. The potential for supply chain disruptions, as recently experienced globally, can also severely impact production capabilities and lead to delays or shortages, affecting market stability. Lastly, the presence of alternative power conversion technologies, though often less efficient for specific applications, can present competition, particularly when design simplicity or cost is prioritized over peak efficiency.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Design Complexity and Integration Challenges | -1.2% | Global | Long-term |

| High Manufacturing Costs of Advanced Components | -1.0% | Global, particularly affecting high-volume markets | Medium-term |

| Intense Price Competition from Alternatives and Mature Technologies | -0.8% | Global, most pronounced in consumer electronics | Long-term |

| Supply Chain Volatility and Geopolitical Tensions | -0.7% | Global, with specific regional impacts on manufacturing hubs | Short to Medium-term |

| Thermal Management Issues in High Power Density Applications | -0.5% | Global | Medium-term |

Synchronous Buck Converter Market Opportunities Impact Analysis

Despite existing restraints, the synchronous buck converter market is ripe with significant opportunities that can accelerate its growth trajectory. The continued global push for renewable energy sources, such as solar and wind power, presents a vast opportunity. These systems require highly efficient and reliable power conversion from various voltage levels, where synchronous buck converters play a crucial role in optimizing energy harvesting and distribution. The burgeoning market for medical devices, particularly portable diagnostic equipment and implantable devices, demands ultra-low power consumption and miniature power management solutions, perfectly aligning with the core strengths of synchronous buck converters. Furthermore, the development of advanced smart infrastructure, including smart cities, smart grids, and industrial automation systems, necessitates sophisticated and efficient power delivery at every node. These systems often operate on distributed power architectures, where individual modules require dedicated, efficient buck converters. The ongoing advancements in power semiconductor materials like Gallium Nitride (GaN) and Silicon Carbide (SiC) open doors for creating even more compact, efficient, and higher-frequency converters, enabling new applications and enhancing existing ones. Lastly, emerging markets in developing countries, with their rapidly growing industrial and consumer electronics sectors, offer substantial untapped potential for synchronous buck converter adoption.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Renewable Energy Systems (Solar, Wind) | +1.8% | Global, strong in Europe, North America, Asia Pacific (China, India) | Long-term |

| Expanding Market for Medical and Healthcare Devices | +1.5% | North America, Europe, Asia Pacific (Japan, South Korea) | Medium to Long-term |

| Development of Smart Infrastructure and IoT Ecosystems | +1.3% | Global | Medium-term |

| Further Advancements in GaN and SiC Technology Integration | +1.0% | Global, driven by semiconductor innovation hubs | Short to Medium-term |

| Untapped Potential in Emerging Economies and Developing Regions | +0.8% | Asia Pacific (Southeast Asia, India), Latin America, Africa | Long-term |

Synchronous Buck Converter Market Challenges Impact Analysis

The synchronous buck converter market faces several enduring challenges that require continuous innovation and strategic adaptation from manufacturers. The pervasive issue of technological obsolescence is a constant threat; as new power management architectures and materials emerge, existing buck converter designs may become less competitive unless continuously updated. This necessitates significant ongoing investment in research and development to stay abreast of the latest advancements. Intellectual property (IP) disputes and the complexities of patent landscapes within the highly innovative semiconductor industry can also pose significant hurdles, leading to costly litigation or hindering market entry for new players. The increasing global focus on environmental regulations and sustainability, while also an opportunity, presents a challenge as manufacturers must ensure their products adhere to strict guidelines regarding hazardous substances and energy consumption, which can increase compliance costs and design constraints. Additionally, a persistent challenge is the talent gap in power electronics engineering; the highly specialized skills required for designing and optimizing advanced synchronous buck converters are in high demand but short supply, potentially slowing innovation and production. Lastly, global economic downturns or recessions can significantly impact consumer spending on electronics and industrial investment, leading to reduced demand for power management components across the board, thus affecting market stability and growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Obsolescence and Rapid Innovation Cycle | -1.0% | Global | Long-term |

| Intellectual Property (IP) Litigation and Patent Landscape Complexities | -0.8% | North America, Europe, Asia Pacific (major innovation hubs) | Medium to Long-term |

| Stringent Environmental Regulations and Compliance Costs | -0.7% | Europe, North America, and countries with strict environmental policies | Long-term |

| Shortage of Skilled Power Electronics Engineers | -0.5% | Global, especially in developed economies | Long-term |

| Global Economic Volatility and Recessions | -0.4% | Global | Short-term (cyclical) |

Synchronous Buck Converter Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Synchronous Buck Converter Market, offering a detailed overview of its current landscape, growth trajectory, and future outlook. It includes thorough segmentation analysis, regional insights, competitive landscape profiling, and impact assessments of key market dynamics such as drivers, restraints, opportunities, and challenges. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making in this evolving market.

| Report Attributes | Report Details |

|---|---|

| Report Name | Synchronous Buck Converter Market |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 9.8 Billion |

| Growth Rate | CAGR of 2025 to 2033 10.2% |

| Number of Pages | 200 |

| Key Companies Covered | Texas Instruments, Analog Devices, Infineon Technologies, STMicroelectronics, Eaton, ROHM Semiconductor, RICOH Electronics, Cypress Semiconductor, Maxim Integrated, Microchip, ON Semiconductor, Vicor, Semtech, Torex Semiconductor, Intersil, Diodes, Toshiba, Vishay Semiconductor |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

: Market Product Type Segmentation:-- AC Synchronous Buck Converter

- DC Synchronous Buck Converter

- Industrial Use

- Medical

- Home Use

- Others

Regional Highlights

The global synchronous buck converter market demonstrates distinct regional dynamics, with specific countries and zones playing pivotal roles due to their technological advancements, manufacturing capabilities, and consumption patterns. Asia Pacific (APAC) is currently the leading region and is anticipated to maintain its dominance throughout the forecast period. This is primarily attributed to the presence of major electronics manufacturing hubs in countries like China, Japan, South Korea, and Taiwan, which are primary producers of consumer electronics, automotive components, and industrial equipment. Rapid industrialization, increasing disposable income, and government initiatives promoting smart cities and renewable energy also contribute significantly to the demand for efficient power management solutions in this region, notably in India and Southeast Asian countries. North America holds a substantial share of the market, driven by robust investments in data centers, cloud computing infrastructure, advanced automotive technologies, and a thriving aerospace and defense sector. The presence of key technology innovators and early adopters of cutting-edge electronics fuels consistent demand. Europe is another significant market, characterized by its strong automotive industry, particularly in Germany, and a leading position in industrial automation and renewable energy initiatives. Strict energy efficiency regulations across the European Union further encourage the adoption of high-performance synchronous buck converters. Latin America and the Middle East & Africa (MEA) are emerging markets, showing gradual growth driven by increasing electrification, urbanization, and the adoption of portable electronic devices and industrial applications, albeit at a slower pace compared to the developed regions. These regions present long-term growth opportunities as their technological infrastructure matures.

- Asia Pacific (APAC): Dominates the market due to the concentration of electronics manufacturing hubs (China, Japan, South Korea, Taiwan) and strong demand from consumer electronics, automotive, and industrial sectors. Rapid urbanization and government support for technological advancements further propel growth.

- North America: A significant market driven by substantial investments in data centers, cloud computing, advanced automotive electronics (EVs, ADAS), and a robust R&D ecosystem. High adoption rates of advanced technologies contribute to strong demand for high-efficiency converters.

- Europe: A key market with a strong presence in the automotive industry (especially Germany), industrial automation, and renewable energy sectors. Stringent energy efficiency regulations and a focus on green technologies accelerate the adoption of synchronous buck converters.

- Latin America: An emerging market experiencing gradual growth, fueled by increasing industrialization, urbanization, and rising adoption of consumer electronics. Investments in infrastructure development and telecommunications are also contributing factors.

- Middle East & Africa (MEA): Shows growing potential driven by increasing electrification projects, rising demand for consumer electronics, and investments in smart infrastructure. However, market growth is comparatively slower, largely dependent on economic diversification efforts.

Top Key Players:

The market research report covers the analysis of key stake holders of the Synchronous Buck Converter Market. Some of the leading players profiled in the report include -:- Texas Instruments

- Analog Devices

- Infineon Technologies

- STMicroelectronics

- Eaton

- ROHM Semiconductor

- RICOH Electronics

- Cypress Semiconductor

- Maxim Integrated

- Microchip

- ON Semiconductor

- Vicor

- Semtech

- Torex Semiconductor

- Intersil

- Diodes

- Toshiba

- Vishay Semiconductor

Frequently Asked Questions:

What is a synchronous buck converter and why is it important?

A synchronous buck converter is a type of DC-DC converter that efficiently steps down (reduces) a higher input voltage to a lower output voltage. It utilizes a synchronous rectifier (a MOSFET) instead of a diode, which significantly reduces power losses and improves efficiency, especially at low output voltages and high currents. This efficiency is crucial for extending battery life in portable devices, reducing heat dissipation in compact electronics, and minimizing energy consumption in large-scale systems like data centers and electric vehicles.

What are the primary applications of synchronous buck converters?

Synchronous buck converters find widespread applications across various industries due to their high efficiency and compact size. Key applications include portable electronic devices (smartphones, laptops, tablets, wearables), automotive electronics (electric vehicles, infotainment systems, ADAS), industrial equipment (automation, robotics, power tools), telecommunications infrastructure (base stations, networking equipment), data centers and cloud computing, and renewable energy systems (solar inverters, battery management systems).

What factors are driving the growth of the synchronous buck converter market?

The synchronous buck converter market growth is primarily driven by the increasing global demand for energy-efficient electronic devices, the rapid expansion of electric vehicles and advanced driver-assistance systems (ADAS) in the automotive sector, and the proliferation of IoT devices and smart infrastructure. Additionally, significant investments in data centers and cloud computing facilities, along with advancements in semiconductor materials like GaN and SiC, are further propelling market expansion.

How does AI impact the synchronous buck converter market?

AI influences the synchronous buck converter market in two key ways: firstly, by driving demand for these converters in AI-powered hardware (e.g., AI processors, edge AI devices) that require highly efficient and stable power delivery. Secondly, AI and machine learning are increasingly used in the design and optimization of synchronous buck converters themselves, enabling more efficient control algorithms, predictive maintenance, and faster development cycles for next-generation power solutions.

What is the projected market size and growth rate for synchronous buck converters?

The Synchronous Buck Converter Market is projected to grow from USD 4.5 Billion in 2025 to USD 9.8 Billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 10.2% during the forecast period. This robust growth is indicative of the critical role these converters play in the evolving landscape of power management across diverse and expanding industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted