Sustained Release Ocular Drug Delivery System Market

Sustained Release Ocular Drug Delivery System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710022 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

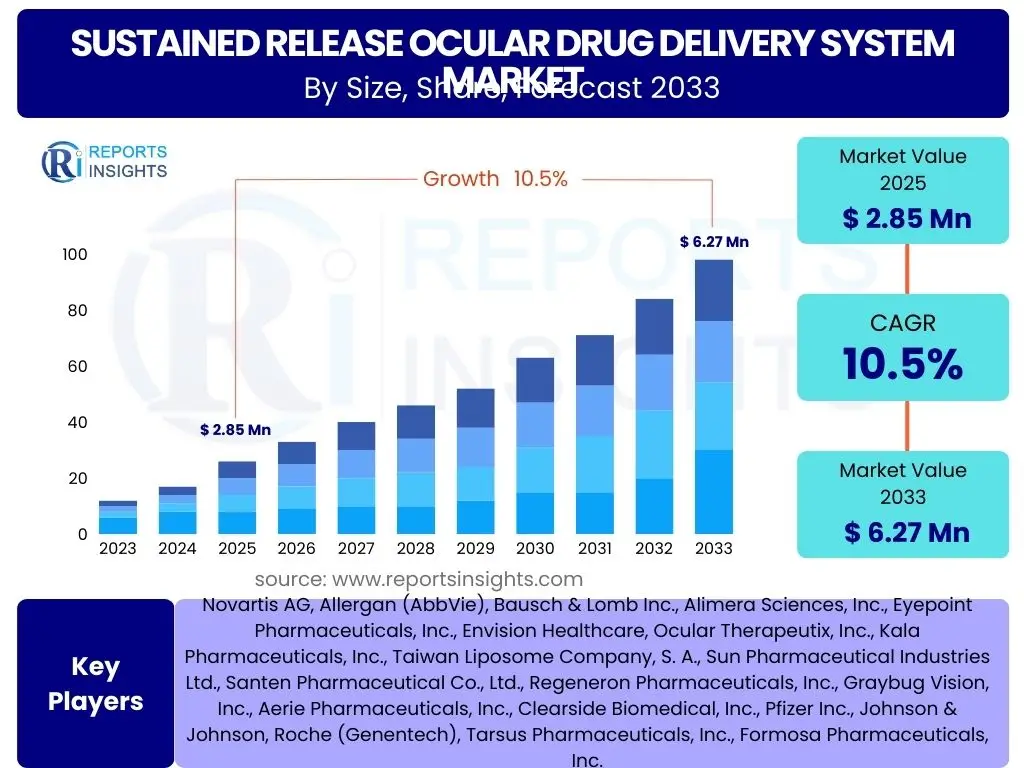

Sustained Release Ocular Drug Delivery System Market Size

According to Reports Insights Consulting Pvt Ltd, The Sustained Release Ocular Drug Delivery System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 6.27 billion by the end of the forecast period in 2033.

Key Sustained Release Ocular Drug Delivery System Market Trends & Insights

The Sustained Release Ocular Drug Delivery System market is experiencing dynamic shifts driven by advancements in material science and pharmaceutical formulation, alongside a growing global burden of chronic eye diseases. Key inquiries from stakeholders often center on the long-term viability of current technologies, the emergence of novel delivery methods, and the impact of regulatory changes on market adoption. There is a strong emphasis on understanding how patient compliance and convenience are influencing the development of next-generation solutions, moving beyond traditional methods to provide more effective and less invasive treatment options.

Furthermore, the market is characterized by a push towards personalized medicine approaches and the integration of smart drug delivery platforms. Users frequently seek information on how these trends are translating into tangible product developments and what implications they hold for clinical practice and patient outcomes. The ongoing research into biodegradable implants, nanotechnology-based systems, and gene therapy delivery within the ocular space signifies a broader trend towards innovative solutions that offer extended therapeutic effects and improved bioavailability, addressing critical unmet needs in ophthalmology.

- Shift towards biodegradable and biocompatible implants for reduced invasiveness.

- Growing adoption of nanotechnology and nanocarriers for enhanced drug penetration and targeting.

- Increased focus on gene therapy and cell-based delivery systems for chronic conditions.

- Development of smart contact lenses and inserts for continuous, controlled drug release.

- Expansion of telemedicine and remote patient monitoring influencing home-based drug administration.

- Rising demand for combination therapies delivered through single sustained release platforms.

- Emphasis on improving patient adherence and reducing treatment burden.

AI Impact Analysis on Sustained Release Ocular Drug Delivery System

The integration of Artificial Intelligence (AI) into the Sustained Release Ocular Drug Delivery System market is a frequently discussed topic, with users exploring its potential to revolutionize drug discovery, formulation, and patient management. Key concerns revolve around AI's capacity to accelerate the identification of new therapeutic targets and optimize drug design, particularly for complex sustained-release formulations where precise kinetics are crucial. Stakeholders are interested in how AI algorithms can predict drug efficacy, toxicity, and release profiles, thereby reducing development timelines and costs associated with extensive clinical trials. The expectation is that AI will streamline R&D processes, making the development of novel ocular drug delivery systems more efficient and targeted.

Moreover, user inquiries often highlight AI's role in personalizing treatment regimens and improving patient outcomes. AI-powered diagnostics can identify suitable candidates for specific sustained-release systems, while predictive analytics can monitor treatment adherence and anticipate potential complications. There is also a strong interest in how AI can be utilized in manufacturing to enhance quality control and optimize production processes for these intricate delivery systems. The overall consensus is that AI will serve as a powerful tool to not only innovate product development but also to refine patient stratification, therapy monitoring, and overall market dynamics by fostering more intelligent and responsive drug delivery solutions.

- AI-driven acceleration in drug discovery for ocular diseases, identifying novel compounds and targets.

- Optimization of sustained release formulation design through AI-powered predictive modeling of drug kinetics.

- Enhanced personalized medicine by AI algorithms matching patients to optimal ocular drug delivery systems.

- Improved clinical trial design and patient recruitment using AI analytics to identify suitable candidates.

- Real-time monitoring and dosage adjustment capabilities through AI-integrated smart delivery devices.

- Streamlining manufacturing processes and quality control for complex ocular implants and inserts.

- Predictive analytics for early detection of treatment non-compliance or adverse events in patients.

Key Takeaways Sustained Release Ocular Drug Delivery System Market Size & Forecast

Stakeholders frequently inquire about the core implications of the market size and forecast for Sustained Release Ocular Drug Delivery Systems. The primary takeaway centers on the significant, consistent growth anticipated, driven largely by an aging global population and the escalating prevalence of chronic ocular conditions such as glaucoma, macular degeneration, and diabetic retinopathy. This sustained growth underscores a critical shift from traditional, frequent dosing regimens to more patient-friendly, long-acting solutions, which address issues of compliance and therapeutic efficacy. The market's expansion is not merely incremental but reflective of a fundamental reorientation in ophthalmic treatment paradigms, promising substantial opportunities for innovation and investment.

A secondary, yet crucial, takeaway is the increasing demand for advanced technological solutions that offer superior drug bioavailability and prolonged therapeutic windows. The forecast indicates that market participants who invest in cutting-edge research and development, particularly in areas like nanotechnology, biodegradable polymers, and gene-editing therapies delivered via sustained release, are poised for significant market capture. The competitive landscape will likely favor companies capable of navigating complex regulatory pathways and demonstrating robust clinical outcomes, while simultaneously catering to the evolving needs of both patients and healthcare providers seeking more effective, less burdensome treatment options for progressive eye diseases.

- Robust and consistent market growth, exceeding the general pharmaceutical market, due to unmet medical needs.

- Aging global demographics and rising prevalence of chronic eye diseases are primary market accelerators.

- Shift towards long-acting formulations driven by improved patient compliance and reduced treatment burden.

- Significant investment opportunities in novel technologies like nanotechnology and biodegradable implants.

- Increased R&D focus on gene therapy and biologics delivery for complex ocular conditions.

- Geographic expansion in emerging markets contributing substantially to future revenue streams.

- Premium pricing potential for innovative, clinically proven sustained release ocular therapies.

Sustained Release Ocular Drug Delivery System Market Drivers Analysis

The sustained release ocular drug delivery system market is primarily propelled by the escalating global burden of chronic eye diseases, a direct consequence of the aging population worldwide. Conditions such as glaucoma, age-related macular degeneration, diabetic retinopathy, and dry eye syndrome necessitate long-term, often daily, medication, which frequently leads to poor patient adherence due to the inconvenience and discomfort of frequent eye drop administration. Sustained release systems offer a compelling solution by reducing the frequency of dosing, thereby improving patient compliance, enhancing therapeutic outcomes, and mitigating peak-trough drug fluctuations that can occur with conventional treatments. This inherent advantage drives significant demand across various ophthalmic indications, pushing pharmaceutical companies towards developing more sophisticated and patient-friendly delivery mechanisms.

Furthermore, technological advancements in material science and biomaterials play a crucial role in enabling the development of innovative sustained release platforms. The advent of biocompatible and biodegradable polymers, micro- and nanotechnologies, and hydrogel-based systems has expanded the possibilities for delivering a wide array of therapeutic agents to both the anterior and posterior segments of the eye for extended periods. These innovations not only address the anatomical and physiological barriers of the eye but also offer improved drug bioavailability and targeted delivery, minimizing systemic side effects. The continuous research and development in these areas, coupled with a strong clinical need for better ophthalmic treatments, forms a robust foundation for the sustained growth of this market segment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Prevalence of Chronic Ocular Diseases | +3.2% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Improved Patient Compliance and Adherence | +2.8% | Global | 2025-2033 |

| Technological Advancements in Drug Delivery Systems | +2.5% | North America, Europe, Japan, South Korea | 2025-2033 |

| Increasing Healthcare Expenditure on Ophthalmology | +1.5% | Developed Nations, Emerging Economies | 2025-2033 |

| Growing Demand for Minimally Invasive Treatments | +0.5% | Global | 2025-2033 |

Sustained Release Ocular Drug Delivery System Market Restraints Analysis

Despite the promising growth trajectory, the sustained release ocular drug delivery system market faces significant restraints that can impede its expansion. One of the primary challenges involves the complex and stringent regulatory approval processes required for novel ophthalmic devices and drug-device combination products. Regulators demand extensive preclinical and clinical data demonstrating long-term safety, efficacy, and biocompatibility, particularly for implantable or intraocular systems. The high cost and lengthy timelines associated with navigating these regulatory hurdles act as a substantial barrier to market entry for new players and can delay the commercialization of innovative solutions, thereby slowing overall market growth. This regulatory burden often discourages smaller companies and limits the pace of product innovation.

Another critical restraint is the high cost associated with the development, manufacturing, and ultimately, the pricing of these advanced sustained release systems. Research and development in this specialized field require significant capital investment for sophisticated technologies, specialized materials, and complex manufacturing processes. These elevated costs often translate into high market prices for the end-products, which can limit their accessibility, especially in developing regions or for patients without adequate insurance coverage. Furthermore, the invasive nature of certain sustained release systems, such as intravitreal implants, introduces potential risks like infection, inflammation, or retinal detachment, which can create patient apprehension and further restrain widespread adoption despite their therapeutic advantages.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Approval Processes | -1.8% | North America, Europe, Japan | 2025-2033 |

| High Development and Manufacturing Costs | -1.5% | Global | 2025-2033 |

| Potential for Invasive Procedures & Associated Risks | -1.0% | Global | 2025-2033 |

| Limited Patient Acceptance due to Complexity | -0.8% | Global | 2025-2033 |

| Reimbursement Challenges in Certain Regions | -0.5% | Europe, Asia Pacific | 2025-2033 |

Sustained Release Ocular Drug Delivery System Market Opportunities Analysis

The Sustained Release Ocular Drug Delivery System market presents substantial opportunities driven by the growing demand for improved therapeutic outcomes and enhanced patient quality of life in ophthalmology. A significant opportunity lies in the development of drug delivery systems for currently untreatable or poorly managed ocular conditions, such as advanced forms of dry age-related macular degeneration, complex retinal detachments, or inherited retinal dystrophies. Innovations in gene therapy and stem cell therapy, when coupled with sustained release delivery mechanisms, hold immense potential to revolutionize treatments for these challenging diseases, offering long-term therapeutic benefits from a single administration. This area represents a frontier for high-value product development and market penetration.

Another major opportunity stems from the expansion into emerging economies. As healthcare infrastructure improves and disposable incomes rise in regions like Asia Pacific and Latin America, the accessibility and affordability of advanced ophthalmic treatments will increase. These regions represent large untapped patient populations with a growing awareness of and need for chronic eye disease management. Companies that can develop cost-effective, culturally sensitive, and easy-to-administer sustained release systems tailored to these markets will find significant growth avenues. Furthermore, strategic collaborations and partnerships between pharmaceutical companies, biotech firms, and academic institutions to pool resources and expertise can accelerate research, reduce development risks, and capitalize on these emerging market demands, fostering an environment ripe for innovation and market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development for Untreatable Ocular Conditions | +2.5% | Global | 2025-2033 |

| Expansion into Emerging Markets | +2.0% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Integration with Gene and Cell Therapies | +1.8% | North America, Europe | 2025-2033 |

| Strategic Partnerships and Collaborations | +1.2% | Global | 2025-2033 |

| Personalized Medicine Approaches | +1.0% | Developed Nations | 2025-2033 |

Sustained Release Ocular Drug Delivery System Market Challenges Impact Analysis

The Sustained Release Ocular Drug Delivery System market faces several inherent challenges that can significantly impact its growth and widespread adoption. One critical challenge is overcoming the complex anatomical and physiological barriers of the eye. The unique structure of the eye, including the blood-retinal barrier and tear film dynamics, presents a formidable hurdle for drug delivery, often requiring invasive procedures to achieve therapeutic concentrations in posterior segments. Developing systems that can bypass these barriers effectively, safely, and non-invasively while maintaining sustained release profiles remains a significant technical and scientific challenge. This necessitates advanced material science and engineering, which adds to the complexity and cost of R&D.

Another substantial challenge involves the potential for adverse events and long-term safety concerns associated with implantable or long-acting devices. While sustained release offers benefits, the prolonged presence of a foreign body or drug reservoir in the eye introduces risks such as inflammation, infection, device migration, or chronic toxicity. Ensuring the long-term biocompatibility and stability of these systems, along with predictable degradation profiles for biodegradable implants, requires extensive and costly pre-clinical and clinical testing. Addressing these safety concerns and gaining ophthalmologist and patient trust is paramount for market acceptance, creating a continuous need for robust post-market surveillance and continuous improvement in device design and material science. Balancing innovation with patient safety remains a delicate and ongoing challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Overcoming Ocular Anatomical & Physiological Barriers | -1.5% | Global | 2025-2033 |

| Managing Potential Adverse Events and Safety Concerns | -1.2% | Global | 2025-2033 |

| High Development Costs for Complex Formulations | -1.0% | Global | 2025-2033 |

| Need for Specialized Surgical Skills for Implants | -0.8% | Global | 2025-2033 |

| Manufacturing Scalability for Novel Technologies | -0.5% | Global | 2025-2033 |

Sustained Release Ocular Drug Delivery System Market - Updated Report Scope

This report provides a comprehensive analysis of the Sustained Release Ocular Drug Delivery System market, offering detailed insights into market size, growth trends, and future projections from 2025 to 2033. It meticulously examines market drivers, restraints, opportunities, and challenges, providing a holistic view of the factors influencing market dynamics. The scope includes an in-depth segmentation analysis across various product types, technologies, applications, and end-users, along with a thorough regional breakdown to highlight key geographical contributions and growth pockets. Furthermore, the report assesses the competitive landscape by profiling leading market players and their strategic initiatives, ensuring a complete understanding of the market's current state and anticipated evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 6.27 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Novartis AG, Allergan (AbbVie), Bausch & Lomb Inc., Alimera Sciences, Inc., Eyepoint Pharmaceuticals, Inc., Envision Healthcare, Ocular Therapeutix, Inc., Kala Pharmaceuticals, Inc., Taiwan Liposome Company, S. A., Sun Pharmaceutical Industries Ltd., Santen Pharmaceutical Co., Ltd., Regeneron Pharmaceuticals, Inc., Graybug Vision, Inc., Aerie Pharmaceuticals, Inc., Clearside Biomedical, Inc., Pfizer Inc., Johnson & Johnson, Roche (Genentech), Tarsus Pharmaceuticals, Inc., Formosa Pharmaceuticals, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Sustained Release Ocular Drug Delivery System market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This comprehensive segmentation allows for a detailed analysis of various product types, technologies, applications, and end-users, reflecting the multifaceted nature of ophthalmic treatments. By dissecting the market into these specific categories, stakeholders can identify key growth areas, understand competitive positioning, and discern emerging trends that are shaping the future landscape of ocular drug delivery. The segmentation highlights the evolution from traditional methods to advanced, long-acting solutions that cater to a broad spectrum of eye conditions.

Each segment is critically examined for its market share, growth potential, and the factors driving its adoption. For instance, the product type segmentation distinguishes between various physical forms of sustained release systems, from implants to contact lenses, each offering unique advantages for different therapeutic needs. Similarly, the technology segmentation delves into the underlying scientific principles, such as nanoparticle or polymer-based delivery, which are instrumental in achieving prolonged drug release and targeted action. This level of detail is crucial for strategic planning, product development, and investment decisions, providing a roadmap for navigating the complexities and opportunities within the sustained release ocular drug delivery market.

- By Product Type: Inserts, Implants, In Situ Gels, Punctal Plugs, Contact Lenses, Nanoparticles, Liposomes, Others

- By Technology: Liposomal Drug Delivery, Nanoparticle Drug Delivery, Microemulsion Drug Delivery, Polymer-Based Drug Delivery, Ion-Exchange Resins, Sol-Gel Based Drug Delivery

- By Route of Administration: Anterior Segment, Posterior Segment

- By Application: Glaucoma, Macular Degeneration, Diabetic Retinopathy, Dry Eye Syndrome, Cataract, Uveitis, Conjunctivitis, Others

- By End-User: Hospitals, Ophthalmic Clinics, Ambulatory Surgical Centers, Homecare Settings, Research Institutes

Regional Highlights

- North America: Dominates the market due to robust healthcare infrastructure, high prevalence of chronic eye diseases, significant R&D investments, and rapid adoption of advanced technologies. The presence of major pharmaceutical and biotech companies, coupled with favorable reimbursement policies, further drives market expansion.

- Europe: A significant market contributor, characterized by an aging population, rising awareness about eye health, and strong governmental support for healthcare innovation. Germany, France, and the UK are key countries due to advanced research capabilities and a high incidence of ocular conditions.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate during the forecast period, driven by a large patient pool, improving healthcare accessibility, increasing healthcare expenditure, and a growing focus on ophthalmic care in countries like China, India, and Japan. Economic development and rising disposable incomes also contribute to market expansion.

- Latin America: Presents emerging opportunities with increasing awareness of eye health, improving healthcare systems, and a growing geriatric population. Brazil and Mexico are key markets due to their large populations and developing economies.

- Middle East and Africa (MEA): A developing market with increasing investment in healthcare infrastructure and rising prevalence of eye disorders. The market growth is gradual, with significant potential as healthcare access expands and advanced treatments become more available.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Sustained Release Ocular Drug Delivery System Market.- Novartis AG

- Allergan (AbbVie)

- Bausch & Lomb Inc.

- Alimera Sciences, Inc.

- Eyepoint Pharmaceuticals, Inc.

- Envision Healthcare

- Ocular Therapeutix, Inc.

- Kala Pharmaceuticals, Inc.

- Taiwan Liposome Company, S. A.

- Sun Pharmaceutical Industries Ltd.

- Santen Pharmaceutical Co., Ltd.

- Regeneron Pharmaceuticals, Inc.

- Graybug Vision, Inc.

- Aerie Pharmaceuticals, Inc.

- Clearside Biomedical, Inc.

- Pfizer Inc.

- Johnson & Johnson

- Roche (Genentech)

- Tarsus Pharmaceuticals, Inc.

- Formosa Pharmaceuticals, Inc.

Frequently Asked Questions

What are sustained release ocular drug delivery systems?

Sustained release ocular drug delivery systems are advanced pharmaceutical formulations designed to deliver therapeutic agents to the eye over an extended period, ranging from weeks to months, from a single administration. They aim to improve patient compliance, reduce dosing frequency, and maintain consistent drug levels at the target site, addressing various chronic eye conditions like glaucoma, macular degeneration, and dry eye syndrome.

How do sustained release systems improve treatment for chronic eye diseases?

These systems significantly enhance treatment by ensuring continuous drug availability, which is crucial for conditions requiring long-term therapy. They overcome issues of patient non-adherence associated with frequent eye drop application, reduce fluctuations in drug concentration, and minimize systemic side effects, ultimately leading to more stable and effective therapeutic outcomes for chronic eye diseases.

What are the primary technologies used in sustained release ocular drug delivery?

Key technologies include polymer-based systems (biodegradable and non-biodegradable implants or inserts), nanotechnology (nanoparticles, liposomes, microemulsions), and in situ gelling systems. These technologies are engineered to control drug release kinetics, improve drug solubility and penetration, and ensure biocompatibility within the ocular environment.

What are the main challenges in developing these drug delivery systems?

Major challenges involve overcoming the eye's natural anatomical and physiological barriers (e.g., tear film, blood-retinal barrier), ensuring long-term safety and biocompatibility of implantable devices, and navigating stringent regulatory approval processes. High development and manufacturing costs, along with the need for specialized surgical skills for certain implants, also present significant hurdles.

Which regions are leading in the adoption and innovation of sustained release ocular drug delivery?

North America and Europe are currently leading in adoption and innovation due to advanced healthcare infrastructure, substantial R&D investments, and a high prevalence of chronic eye diseases. However, the Asia Pacific region is rapidly emerging as a high-growth market, driven by increasing healthcare access, a large patient population, and rising disposable incomes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted