Supercomputer Market

Supercomputer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709675 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

Supercomputer Market Size

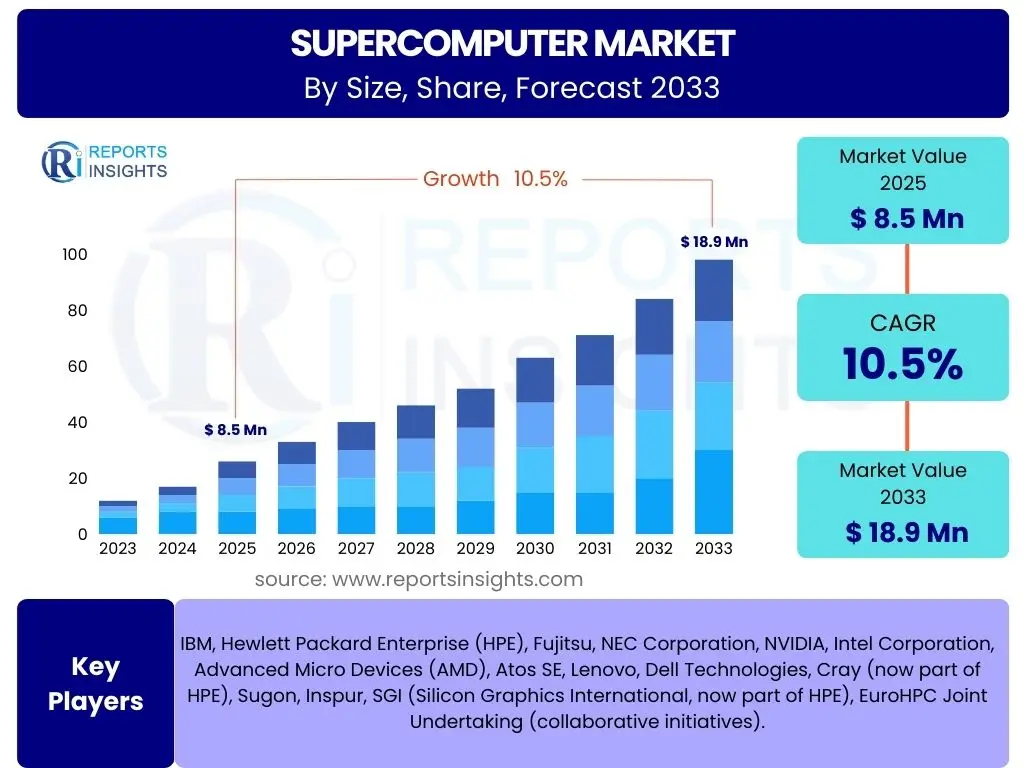

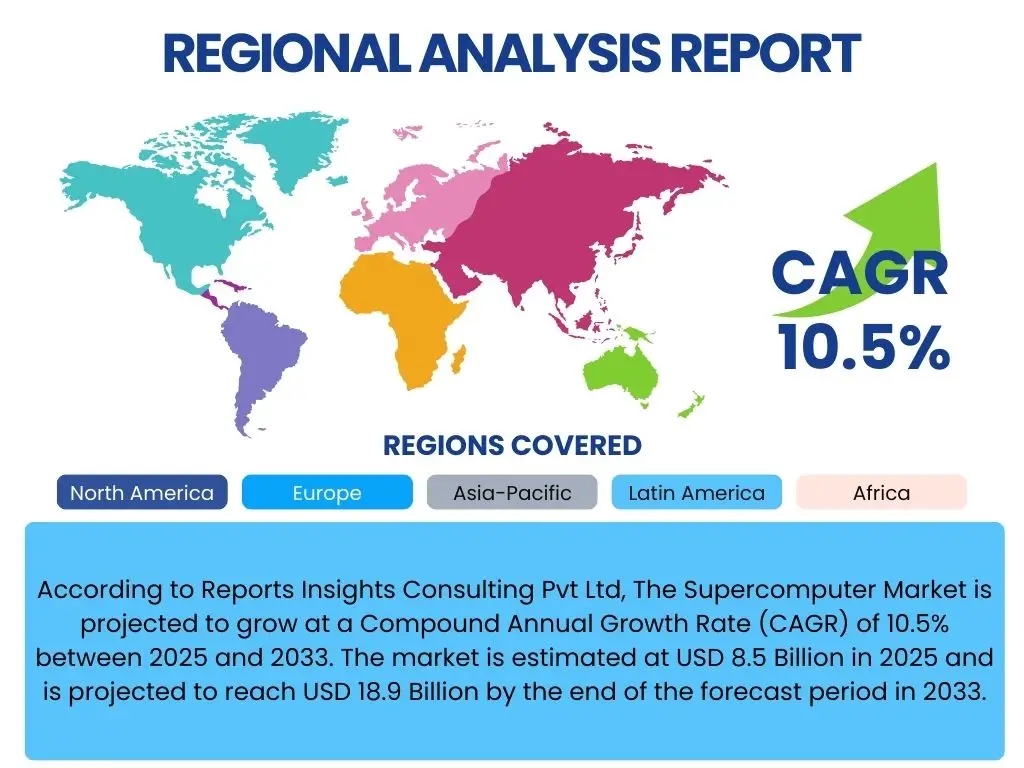

According to Reports Insights Consulting Pvt Ltd, The Supercomputer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 18.9 Billion by the end of the forecast period in 2033.

Key Supercomputer Market Trends & Insights

The supercomputer market is experiencing dynamic shifts driven by advancements in computational requirements across various sectors. User inquiries frequently highlight the escalating demand for higher performance and energy efficiency, alongside the integration of emerging technologies. Key discussions revolve around the push towards exascale computing, the deepening synergy with artificial intelligence, and the increasing adoption of cloud-based HPC solutions, all pointing to a future of more accessible and powerful computational resources.

Furthermore, there is significant interest in the architectural innovations that support these demands, including heterogeneous computing environments leveraging diverse processor types like GPUs, FPGAs, and specialized accelerators. The focus on sustainable supercomputing, addressing the immense power consumption, also emerges as a critical trend. These trends collectively indicate a market moving towards greater specialization, efficiency, and broader application of high-performance computing capabilities.

- Exascale computing initiatives are driving the development of next-generation systems capable of quintillions of calculations per second.

- Increasing integration of Artificial Intelligence (AI) and Machine Learning (ML) workloads, demanding specialized hardware and software optimization.

- Rising adoption of cloud-based High-Performance Computing (HPC) solutions, offering flexibility and accessibility.

- Focus on energy efficiency and sustainable supercomputing designs to mitigate environmental impact and operational costs.

- Development of heterogeneous architectures, combining CPUs, GPUs, and other accelerators for optimized performance.

- Growing emphasis on data analytics and processing capabilities to handle massive datasets generated by scientific research and industrial applications.

- Emergence of quantum computing research and its potential synergy with classical supercomputing infrastructure.

AI Impact Analysis on Supercomputer

User queries regarding the impact of AI on supercomputers frequently center on whether AI will diminish or amplify the need for traditional HPC. The consensus indicates that AI's rapid evolution is a primary catalyst for supercomputing growth, not a replacement. AI models, particularly large language models and deep learning networks, require immense computational power for training and inference, tasks uniquely suited for supercomputer architectures. This symbiotic relationship is driving innovation in both fields, pushing the boundaries of what is possible in data processing and scientific discovery.

The convergence of AI and supercomputing is also shaping the development of new hardware and software paradigms. There is a clear expectation that future supercomputers will be designed with AI workloads in mind, incorporating specialized AI accelerators and optimized software stacks. This integration is expected to democratize access to advanced AI capabilities, making high-performance AI accessible to a broader range of researchers and industries. Concerns about the energy consumption of these integrated systems are also prevalent, underscoring the ongoing push for more efficient designs.

- AI model training, especially for deep learning and large language models, significantly drives demand for supercomputing resources.

- Supercomputers provide the massive parallel processing capabilities essential for handling complex AI algorithms and vast datasets.

- Integration of specialized AI accelerators (GPUs, TPUs, ASICs) into supercomputer architectures enhances performance for AI workloads.

- AI is utilized within supercomputing systems for optimizing resource allocation, scheduling, and system management.

- The development of hybrid AI-HPC workflows enables new scientific discoveries and industrial applications.

- Increased investment in AI research directly translates to a greater need for advanced supercomputing infrastructure.

- AI is facilitating the analysis and interpretation of the colossal datasets generated by supercomputing simulations.

Key Takeaways Supercomputer Market Size & Forecast

Analysis of user questions regarding the supercomputer market size and forecast reveals a strong emphasis on understanding the underlying drivers of growth and the long-term sustainability of this expansion. Key insights suggest that the market is poised for robust growth, primarily fueled by the insatiable demand for processing power in scientific research, advanced data analytics, and the burgeoning field of artificial intelligence. Governments and research institutions continue to be significant investors, alongside a growing commercial interest in leveraging HPC for competitive advantage.

Furthermore, the forecast indicates a strategic shift towards more energy-efficient and scalable architectures, with exascale computing serving as a major milestone. Stakeholders are particularly interested in the technological advancements that will enable this growth, including innovations in processor technology, interconnects, and cooling solutions. The market's resilience is also highlighted, demonstrating continuous innovation despite challenges like high operational costs and the need for specialized expertise.

- The supercomputer market is set for substantial expansion, with a CAGR exceeding 10% through 2033, reflecting rising global computational needs.

- Exascale computing projects represent a major technological frontier and growth driver, pushing performance boundaries.

- Artificial Intelligence and Machine Learning applications are pivotal in creating new demand and use cases for supercomputing.

- Significant investments from governmental bodies, defense sectors, and research institutions underpin market stability and innovation.

- The trend towards more power-efficient designs and sustainable HPC solutions is critical for future market development.

- Commercial enterprises are increasingly adopting supercomputing for complex simulations, data modeling, and product development.

Supercomputer Market Drivers Analysis

The supercomputer market is profoundly influenced by several key drivers that continuously propel its growth and technological evolution. A primary driver is the ever-increasing demand for high-performance computing (HPC) across diverse sectors, ranging from intricate scientific research to complex industrial simulations. This growing need for superior computational capabilities is fundamental to solving problems that are intractable for conventional computing systems, thereby fostering innovation and competitive advantages.

Another significant driver stems from the rapid advancements in Artificial Intelligence (AI) and Machine Learning (ML). These fields require unprecedented processing power for training sophisticated models and handling vast datasets, directly boosting the demand for high-end supercomputing infrastructure. Additionally, substantial government and private sector investments in research and development, particularly for national supercomputing centers and defense applications, play a crucial role in funding new projects and supporting technological breakthroughs, ensuring sustained market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for High-Performance Computing (HPC) | +3.0% | Global, particularly North America, Europe, Asia Pacific | Short to Long Term (2025-2033) |

| Advancements in AI and Machine Learning | +2.5% | Global, especially USA, China, European Union | Short to Mid Term (2025-2030) |

| Government and Private Sector Investments in R&D | +2.0% | USA, China, Japan, Germany, UK | Mid to Long Term (2026-2033) |

| Increasing Complexity of Scientific Simulations and Data Analytics | +1.5% | Global, focused on Academia and Research Labs | Short to Long Term (2025-2033) |

| Emergence of Exascale Computing Projects | +1.5% | USA, EU, China, Japan | Mid to Long Term (2027-2033) |

Supercomputer Market Restraints Analysis

Despite its significant growth trajectory, the supercomputer market faces several formidable restraints that can impede its expansion and adoption. One of the most prominent challenges is the exceedingly high initial investment required to acquire and deploy supercomputing systems. These sophisticated machines demand substantial capital outlays, making them accessible primarily to well-funded governmental agencies, large research institutions, and major corporations, thus limiting broader market penetration.

Furthermore, the operational costs associated with supercomputers are considerable, largely driven by their immense power consumption and the complex cooling infrastructure necessary to maintain optimal performance. These recurring expenses add to the total cost of ownership, posing a financial barrier. Additionally, the scarcity of a highly skilled workforce proficient in programming, optimizing, and managing these complex parallel architectures represents a significant human capital restraint, hindering the efficient utilization and expansion of supercomputing capabilities across various potential applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Operational Costs | -1.8% | Global, particularly developing economies | Short to Long Term (2025-2033) |

| Significant Power Consumption and Cooling Requirements | -1.5% | Global, especially dense urban data centers | Short to Mid Term (2025-2030) |

| Skilled Workforce Shortage for Programming and Management | -1.2% | Global, prominent in emerging tech hubs | Mid Term (2026-2031) |

| Complexity of Software Development and Optimization | -1.0% | Global, particularly for new architectural paradigms | Short to Long Term (2025-2033) |

Supercomputer Market Opportunities Analysis

The supercomputer market is rich with opportunities that promise to drive innovation and expand its application landscape significantly. A key opportunity lies in the continued integration of supercomputing with cloud platforms, offering High-Performance Computing as a Service (HPCaaS). This model democratizes access to powerful computational resources, enabling smaller businesses and research groups to leverage supercomputing capabilities without the prohibitive upfront investment and operational overhead, thus broadening the market base.

Another compelling opportunity emerges from the active research and development in quantum computing. While nascent, the synergy between classical supercomputers and nascent quantum systems presents avenues for hybrid solutions that could tackle previously unsolvable problems, opening entirely new domains of application. Furthermore, a concerted global focus on developing more energy-efficient designs and sustainable supercomputing practices presents not only an environmental benefit but also a significant economic opportunity by reducing operational costs and appealing to green initiatives, alongside the expansion of supercomputing into new application areas like personalized medicine and smart city development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Cloud Computing for HPC as a Service | +2.0% | Global, particularly North America, Europe | Short to Mid Term (2025-2030) |

| Development of Quantum Computing Capabilities and Hybrid Architectures | +1.8% | USA, China, Europe, Japan (leading research nations) | Mid to Long Term (2028-2033) |

| Focus on Energy-Efficient Designs and Sustainable Supercomputing | +1.5% | Global, driven by environmental regulations and cost-saving initiatives | Short to Long Term (2025-2033) |

| Expansion into New Application Areas (e.g., Personalized Medicine, Smart Cities) | +1.2% | Global, with specific regional needs | Mid Term (2026-2031) |

Supercomputer Market Challenges Impact Analysis

The supercomputer market, while experiencing significant growth, is not without its considerable challenges that necessitate continuous innovation and strategic planning. A critical technical challenge is managing the immense heat dissipation generated by high-density processing units, requiring advanced and often costly cooling infrastructures. This directly impacts system design, operational expenditure, and overall physical footprint, especially as systems scale towards exascale performance levels.

Moreover, effectively managing and storing the colossal volumes of data generated by exascale computations presents a monumental challenge. Traditional data storage and retrieval methods often fall short, necessitating breakthroughs in high-throughput storage systems and intelligent data management strategies. Furthermore, the inherent sensitivity of the data processed on supercomputers, ranging from national security secrets to proprietary research, makes these systems prime targets for sophisticated cybersecurity threats. Safeguarding these assets requires constant vigilance and advanced security protocols, while potential supply chain disruptions for specialized components add another layer of complexity and risk to supercomputer development and deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Heat Dissipation and Cooling Infrastructure | -1.7% | Global, affecting all large-scale deployments | Short to Long Term (2025-2033) |

| Data Management and Storage at Exascale | -1.5% | Global, especially for data-intensive scientific applications | Mid to Long Term (2026-2033) |

| Cybersecurity Threats to Sensitive Data | -1.3% | Global, critical for government and defense sectors | Short to Long Term (2025-2033) |

| Supply Chain Disruptions for Critical Components | -1.0% | Global, impacting manufacturing and deployment timelines | Short to Mid Term (2025-2030) |

Supercomputer Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global supercomputer market, encompassing a detailed review of its current size, historical performance, and future growth projections. It offers a meticulous examination of market trends, drivers, restraints, opportunities, and challenges, alongside a thorough impact assessment of artificial intelligence on the sector. The scope includes a granular segmentation analysis by component, application, end-user, and processor type, providing a holistic view of the market landscape and its evolving dynamics across key regions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 18.9 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | IBM, Hewlett Packard Enterprise (HPE), Fujitsu, NEC Corporation, NVIDIA, Intel Corporation, Advanced Micro Devices (AMD), Atos SE, Lenovo, Dell Technologies, Cray (now part of HPE), Sugon, Inspur, SGI (Silicon Graphics International, now part of HPE), EuroHPC Joint Undertaking (collaborative initiatives). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global supercomputer market is meticulously segmented to provide a granular understanding of its diverse components, applications, and end-users. This detailed segmentation highlights the various facets contributing to the market's growth and allows for targeted analysis of specific industry dynamics. Understanding these segments is crucial for identifying key growth areas, emerging technologies, and strategic investment opportunities across the supercomputing landscape.

Each segment, from the fundamental hardware components to specialized software and comprehensive services, plays a vital role in the supercomputing ecosystem. The application-based segmentation showcases the wide array of industries benefiting from supercomputing capabilities, while the end-user categories distinguish between governmental, academic, and commercial deployments. Furthermore, the segmentation by processor type underscores the architectural diversity and technological innovation driving performance improvements in supercomputers worldwide.

- By Component: This segment includes the essential building blocks of supercomputing systems, comprising Hardware (such as Processors, Memory modules, Storage solutions, and high-speed Interconnects), Software (including specialized Operating Systems, Middleware for parallel processing, Compilers, and various Development Tools), and a range of Services (covering Installation, ongoing Maintenance, expert Consulting, and crucial Training programs).

- By Application: Supercomputing finds extensive use across numerous applications, notably in fundamental Research (both Academic institutions and Government Laboratories), various Industrial sectors (suchtaining Oil & Gas exploration, Manufacturing design, Aerospace & Defense simulations, Automotive engineering, complex Financial Services modeling, critical Weather Forecasting & Climate Modeling, advanced Entertainment & Media content creation, and pioneering Life Sciences & Healthcare research), and broad Scientific Discovery initiatives.

- By End-User: The primary users of supercomputers are categorized into Government & Defense agencies, Academic & Research institutions, and Commercial Enterprises (spanning industries like Manufacturing, Energy, Finance, and Healthcare), each leveraging HPC for their unique high-computational demands.

- By Processor Type: This segmentation reflects the diverse architectures powering supercomputers, encompassing Central Processing Units (CPUs) for general computing tasks, Graphics Processing Units (GPUs) for parallel processing, Field-Programmable Gate Arrays (FPGAs) for customizable hardware acceleration, Application-Specific Integrated Circuits (ASICs) for highly optimized specific tasks, and the emerging class of Quantum Processors for future computational paradigms.

Regional Highlights

- North America: The United States remains a dominant force in the supercomputer market, driven by extensive government funding for national labs, a robust defense sector, and significant private sector investments in AI and research. Canada also contributes with growing academic and industrial HPC adoption.

- Europe: Countries like Germany, France, and the United Kingdom are key players, supported by the EuroHPC Joint Undertaking which fosters collaboration and investment in pan-European supercomputing infrastructure. Focus areas include scientific research, industrial innovation, and climate modeling.

- Asia Pacific (APAC): This region, particularly China and Japan, shows immense growth. China is a leader in deploying top-tier supercomputers, fueled by national strategic initiatives and massive R&D investments. Japan is prominent in scientific research and industrial applications, especially in manufacturing and advanced materials.

- Latin America: Emerging market with increasing adoption in academic research and oil & gas exploration, though still smaller in scale compared to other regions. Brazil and Mexico are leading the modest investments in HPC infrastructure.

- Middle East and Africa (MEA): Growth is primarily driven by oil & gas exploration, academic research, and government initiatives to diversify economies. Countries like Saudi Arabia and the UAE are investing in supercomputing for scientific and industrial development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Supercomputer Market.- IBM

- Hewlett Packard Enterprise (HPE)

- Fujitsu

- NEC Corporation

- NVIDIA

- Intel Corporation

- Advanced Micro Devices (AMD)

- Atos SE

- Lenovo

- Dell Technologies

- Sugon

- Inspur

- Cray (now part of HPE)

- SGI (Silicon Graphics International, now part of HPE)

- EuroHPC Joint Undertaking (collaborative initiatives and consortia)

Frequently Asked Questions

What is a supercomputer and what is it used for?

A supercomputer is a high-performance computing system designed to perform at or near the highest operational rate possible for the current technology. It is utilized for highly complex computational tasks that require massive processing power, such as advanced scientific simulations, weather forecasting, cryptographic analysis, nuclear research, and the training of artificial intelligence models. These systems enable breakthroughs in fields ranging from medicine to climate science.

How is AI impacting the supercomputer market?

Artificial Intelligence (AI) is significantly boosting the supercomputer market by driving demand for immense computational power, especially for training large-scale deep learning models and performing complex data analysis. AI workloads are increasingly integrated into supercomputer designs, leading to the development of specialized hardware like GPUs and AI accelerators, and fostering hybrid computing architectures that combine classical HPC with AI-specific capabilities. This synergy is accelerating innovation in both domains.

What are the main challenges in supercomputing?

The supercomputer market faces several key challenges, including the high initial investment and operational costs, particularly due to significant power consumption and the need for sophisticated cooling infrastructures. Other challenges involve managing vast amounts of data at exascale, developing and optimizing complex software for parallel architectures, ensuring robust cybersecurity against advanced threats, and addressing a global shortage of highly skilled professionals capable of managing and programming these intricate systems.

Which regions lead the supercomputer market?

North America, particularly the United States, and the Asia Pacific region, led by China and Japan, are the dominant forces in the supercomputer market. These regions benefit from substantial governmental funding, robust academic research ecosystems, strong industrial demand, and significant investments in developing national supercomputing capabilities. Europe also maintains a strong presence through collaborative initiatives like the EuroHPC Joint Undertaking, fostering widespread supercomputing adoption and innovation.

What is the future outlook for supercomputing?

The future outlook for supercomputing is exceptionally positive, characterized by sustained robust growth driven by advancements in AI, the push towards exascale computing, and the increasing complexity of scientific and industrial challenges. Key trends indicate a focus on energy efficiency, the integration of quantum computing capabilities, and the expansion of cloud-based HPC services to broaden accessibility. Supercomputing will continue to be a critical enabler for innovation and discovery across virtually all sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted