Sulphur Recovery Market

Sulphur Recovery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706026 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

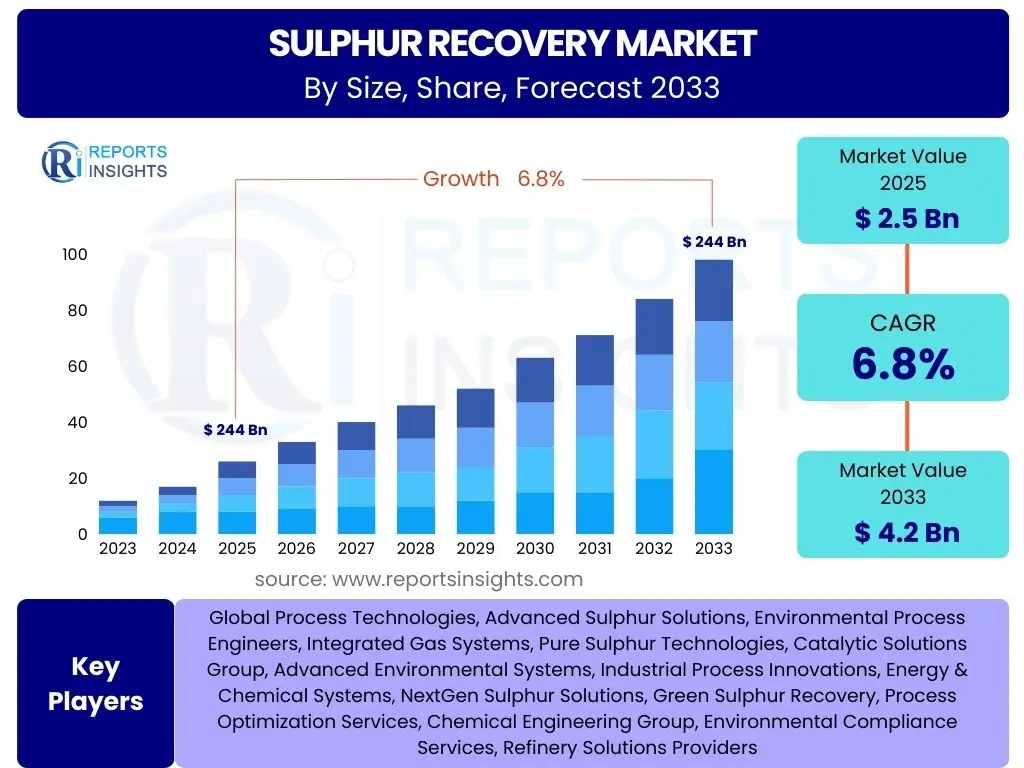

Sulphur Recovery Market Size

According to Reports Insights Consulting Pvt Ltd, The Sulphur Recovery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 4.2 Billion by the end of the forecast period in 2033.

Key Sulphur Recovery Market Trends & Insights

The Sulphur Recovery Market is experiencing significant transformation driven by evolving environmental mandates, technological advancements, and shifts in global energy production. Common user inquiries often focus on how regulatory pressures are shaping market demand, the impact of new technologies on efficiency and emissions, and the influence of the energy transition towards cleaner fuels. These discussions highlight a collective interest in sustainable solutions and operational excellence within the industry.

Furthermore, users frequently explore the integration of sulphur recovery with broader industrial processes, particularly in the oil and gas sector, and its relevance in the context of circular economy principles. The emphasis is on identifying trends that not only ensure compliance but also offer economic advantages through improved resource utilization and reduced operational costs. This indicates a strategic shift towards more holistic and integrated approaches to sulphur management.

- Increasingly stringent global environmental regulations, particularly concerning sulfur dioxide (SO2) emissions, are driving demand for advanced recovery technologies.

- Growth in natural gas processing and sour crude oil refining necessitates efficient sulphur recovery units to meet environmental standards.

- Technological advancements in Claus process optimization and tail gas treatment systems are improving recovery efficiencies and reducing atmospheric releases.

- The focus on valorization of recovered sulphur into marketable products, such as sulphuric acid or elemental sulphur for agricultural use, is gaining traction.

- Digitalization and automation are being adopted to enhance process control, predictive maintenance, and overall operational safety in sulphur recovery units.

AI Impact Analysis on Sulphur Recovery

User queries regarding the impact of Artificial intelligence (AI) on sulphur recovery systems frequently center on its potential to optimize complex chemical processes, enhance operational efficiency, and improve predictive maintenance capabilities. There is a strong interest in understanding how AI algorithms can analyze vast datasets from plant operations to identify subtle inefficiencies, anticipate equipment failures, and recommend real-time adjustments, thereby minimizing downtime and maximizing sulphur recovery rates. Expectations are high for AI to deliver significant improvements in process stability and environmental performance.

Concerns often revolve around the initial investment required for AI integration, the need for specialized data scientists and engineers, and the cybersecurity implications of connecting operational technology (OT) with IT systems. However, users also express optimism about AI's ability to address the complexities of varying feedstock compositions and fluctuating operating conditions, which are critical challenges in conventional sulphur recovery. The consensus is that AI, while demanding a careful implementation strategy, holds transformative potential for making sulphur recovery more robust, efficient, and compliant.

- AI-driven predictive maintenance can reduce unscheduled downtime by forecasting equipment failures in pumps, compressors, and catalytic converters within sulphur recovery units.

- Real-time process optimization using AI algorithms can adjust parameters (e.g., air-to-acid gas ratio) to maximize sulphur conversion efficiency and minimize emissions.

- Enhanced safety through AI-powered anomaly detection, identifying deviations in operational parameters that could lead to hazardous conditions.

- Improved troubleshooting and operational support by providing data-driven insights to operators for quicker problem resolution.

- Optimization of energy consumption by AI systems through intelligent control of heating and cooling cycles within the recovery process.

Key Takeaways Sulphur Recovery Market Size & Forecast

The Sulphur Recovery Market is poised for substantial growth over the next decade, primarily propelled by increasingly stringent global environmental regulations and the continued expansion of industries that produce sulfur-containing emissions. A key takeaway is the non-negotiable demand for efficient sulfur removal technologies from sectors such as oil and gas refining, natural gas processing, and various chemical manufacturing operations. This regulatory push ensures a consistent and growing market for advanced sulphur recovery solutions.

Another significant insight is the market's trajectory towards technological innovation, particularly in enhancing recovery efficiency and reducing operational costs. The projected growth reflects not just an expansion in volume but also a qualitative shift towards more sophisticated, automated, and environmentally compliant systems. This indicates that future market success will hinge on the adoption of best available technologies and strategic investments in research and development to meet evolving industrial and environmental requirements.

- The market exhibits robust growth potential, driven by global environmental mandates to reduce sulfur emissions.

- Oil and gas refining, along with natural gas processing, remain the primary demand drivers for sulphur recovery technologies.

- Technological innovation, especially in process optimization and tail gas treatment, is crucial for market competitiveness and growth.

- Investments in digitalization and automation are expected to enhance operational efficiency and safety across the recovery value chain.

- The Asia Pacific region is anticipated to be a significant growth hub due to rapid industrialization and increasing energy demand.

Sulphur Recovery Market Drivers Analysis

The Sulphur Recovery Market is primarily driven by the escalating global emphasis on environmental protection and public health. Stricter air quality regulations, particularly those targeting sulfur dioxide (SO2) emissions from industrial sources, compel industries to adopt advanced sulphur recovery technologies. This regulatory landscape creates a continuous demand for efficient and compliant sulphur management solutions, ensuring that industrial operations adhere to national and international emission standards.

Furthermore, the growing global demand for refined petroleum products and natural gas leads to an increase in sour crude oil processing and sour gas production. As these feedstocks contain high levels of sulfur compounds, their processing necessitates effective sulphur recovery to prevent environmental pollution. The expansion of oil and gas refining capacities and the discovery of new sour gas reserves directly correlate with the market growth for sulphur recovery units, as these facilities are mandated to remove sulfur prior to product distribution and atmospheric release.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | +2.1% | Global, particularly North America, Europe, China | 2025-2033 (Long-term) |

| Increasing Sour Crude Processing & Natural Gas Production | +1.8% | North America, Middle East, Asia Pacific | 2025-2033 (Long-term) |

| Growing Industrialization & Chemical Production | +1.5% | Asia Pacific, Latin America, Africa | 2025-2033 (Long-term) |

| Technological Advancements in Recovery Processes | +0.8% | Global | 2025-2033 (Mid to Long-term) |

Sulphur Recovery Market Restraints Analysis

The Sulphur Recovery Market faces significant challenges primarily due to the substantial capital expenditure required for installing and upgrading sulphur recovery units (SRUs). The complexity of these systems, involving intricate chemical processes and specialized equipment, translates into high upfront investment costs, which can be a deterrent for smaller refiners or those operating with limited budgets. This economic barrier often delays or prevents the adoption of advanced recovery technologies, particularly in regions with less stringent environmental enforcement.

Another key restraint is the operational complexity and high maintenance requirements associated with SRUs. These units operate under demanding conditions, dealing with corrosive sulfur compounds and high temperatures, which necessitates frequent maintenance and skilled labor. The need for specialized operators and technicians, coupled with the ongoing costs of catalysts and chemicals, adds to the operational burden, potentially impacting the profitability and efficiency of sulphur recovery efforts. Furthermore, fluctuations in crude oil prices and global economic downturns can impact investment decisions in new refinery projects or upgrades, thereby indirectly constraining market growth for sulphur recovery solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure (CAPEX) | -1.2% | Global, particularly developing economies | 2025-2033 (Long-term) |

| Operational Complexity & Maintenance Costs | -0.9% | Global | 2025-2033 (Long-term) |

| Fluctuating Raw Material Prices (e.g., Oil & Gas) | -0.7% | Global | 2025-2028 (Short to Mid-term) |

| Availability of Skilled Workforce | -0.5% | Emerging markets, niche technology areas | 2025-2033 (Long-term) |

Sulphur Recovery Market Opportunities Analysis

Significant opportunities in the Sulphur Recovery Market arise from the continuous advancements in process technologies aimed at enhancing efficiency and reducing the environmental footprint. The development of next-generation Claus catalysts, advanced tail gas treatment processes, and innovative gas-liquid contacting technologies offers pathways to achieve higher sulphur recovery efficiencies, often exceeding 99.9%, while simultaneously lowering energy consumption and operational costs. These innovations present avenues for industries to not only meet stringent environmental regulations but also gain a competitive edge through improved resource utilization.

Furthermore, the increasing focus on the circular economy and resource valorization creates new market potential for recovered sulfur. Beyond traditional uses in sulfuric acid and fertilizer production, opportunities are emerging for utilizing elemental sulfur in novel applications, such as sulfur concrete, batteries, and advanced materials. This diversification of end-uses can transform sulfur from a waste product into a valuable commodity, driving investments in recovery technologies and fostering sustainable industrial practices. The growth of economies in Asia Pacific and Latin America, coupled with rising environmental awareness, also opens up new geographical markets for sulphur recovery solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced & Efficient Technologies | +1.5% | Global | 2025-2033 (Mid to Long-term) |

| Growing Demand for Value-Added Sulphur Products | +1.0% | Global | 2025-2033 (Long-term) |

| Expansion in Emerging Economies (e.g., APAC) | +0.8% | Asia Pacific, Latin America, Africa | 2025-2033 (Long-term) |

| Integration with Carbon Capture, Utilization, and Storage (CCUS) | +0.5% | North America, Europe, Middle East | 2028-2033 (Long-term) |

Sulphur Recovery Market Challenges Impact Analysis

The Sulphur Recovery Market is confronted with significant challenges primarily stemming from the continually evolving and increasingly stringent regulatory landscape. Companies must navigate a complex web of national and international environmental laws that demand higher sulphur recovery efficiencies and lower emission limits. Achieving compliance often requires substantial investments in new technologies or costly upgrades to existing infrastructure, which can strain operational budgets and require extensive technical expertise. The dynamic nature of these regulations necessitates continuous monitoring and adaptation, posing a constant challenge for industrial operators.

Another major challenge is the inherent complexity and high energy consumption of sulphur recovery processes. These units typically involve multiple reaction stages, high temperatures, and the handling of hazardous materials, demanding precise control and robust design. The energy intensity contributes significantly to operational costs and the overall carbon footprint of the facility. Additionally, managing the byproducts and waste streams, such as spent catalysts and acid gas residues, presents disposal challenges and requires environmentally responsible solutions, further adding to the operational complexities and costs within the sulphur recovery ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent & Evolving Regulatory Compliance | -1.0% | Global | 2025-2033 (Long-term) |

| High Energy Consumption & Operational Costs | -0.8% | Global | 2025-2033 (Long-term) |

| Management of Waste Byproducts | -0.6% | Global | 2025-2033 (Long-term) |

| Integration with Existing Infrastructure | -0.4% | Developed regions with aging facilities | 2025-2030 (Mid-term) |

Sulphur Recovery Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Sulphur Recovery Market, covering historical trends, current market dynamics, and future projections. The scope encompasses detailed segmentation by technology, application, and end-use, along with a thorough regional assessment to identify key growth areas and competitive landscapes. It also includes an impact analysis of emerging technologies such as Artificial Intelligence and a robust evaluation of market drivers, restraints, opportunities, and challenges affecting the industry's trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Process Technologies, Advanced Sulphur Solutions, Environmental Process Engineers, Integrated Gas Systems, Pure Sulphur Technologies, Catalytic Solutions Group, Advanced Environmental Systems, Industrial Process Innovations, Energy & Chemical Systems, NextGen Sulphur Solutions, Green Sulphur Recovery, Process Optimization Services, Chemical Engineering Group, Environmental Compliance Services, Refinery Solutions Providers |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Sulphur Recovery Market is comprehensively segmented to provide granular insights into its various facets, enabling a detailed understanding of market dynamics across different technologies, applications, and end-use products. This segmentation allows for the analysis of specific market niches, identifying dominant segments and areas with high growth potential, which is crucial for strategic planning and investment decisions within the industry. Each segment contributes uniquely to the overall market landscape, influenced by varying regulatory pressures, technological requirements, and industrial demands.

The "By Process" segment highlights the prevalence of the Claus process and its derivatives, alongside the growing importance of advanced tail gas treatment and emerging biological methods, reflecting the industry's pursuit of higher efficiency and lower emissions. The "By Application" segment showcases the critical role of sulphur recovery in the oil & gas and natural gas processing sectors, emphasizing its indispensability in modern energy production. Lastly, the "By End-Use Product" segment sheds light on the valorization of recovered sulphur into elemental sulfur and sulphuric acid, underpinning its economic significance beyond environmental compliance.

- By Process:

- Claus Process: This traditional thermal process remains the cornerstone of sulphur recovery, further segmented into direct oxidation and sub-dewpoint variations for enhanced efficiency. It accounts for the majority of sulphur recovered globally.

- Tail Gas Treatment: Essential for achieving ultra-low SO2 emissions, these processes (e.g., SCOT, CBA, Wet Scrubbing) are employed downstream of the Claus unit to capture residual sulfur compounds.

- Biological Processes: Emerging as environmentally friendly alternatives, these methods utilize microorganisms for H2S removal, gaining traction for specific applications or lower sulfur content streams.

- Other Technologies: Includes a range of specialized processes like direct oxidation to sulfuric acid, or adsorption-based systems.

- By Application:

- Oil & Gas Refining: The largest application segment, driven by the desulfurization of crude oil to meet clean fuel standards.

- Natural Gas Processing: Critical for removing hydrogen sulfide from sour natural gas before pipeline transmission and end-use.

- Metals & Mining: Used in smelters to capture sulfur emissions from ore processing.

- Chemical Processing: Various chemical industries produce sulfur-containing waste gases requiring recovery.

- Power Generation: Desulfurization of flue gases from power plants, particularly coal-fired, to reduce SO2 emissions.

- Other Industrial Applications: Includes pulp and paper, waste incineration, and other industrial activities.

- By End-Use Product:

- Elemental Sulphur: The most common recovered product, used in various industrial applications including fertilizers, chemicals, and rubber.

- Sulphuric Acid: Directly produced in some recovery processes or by further oxidation of elemental sulfur, serving as a vital industrial chemical.

- Other Sulphur Derivatives: Includes various specialty sulfur compounds for niche applications.

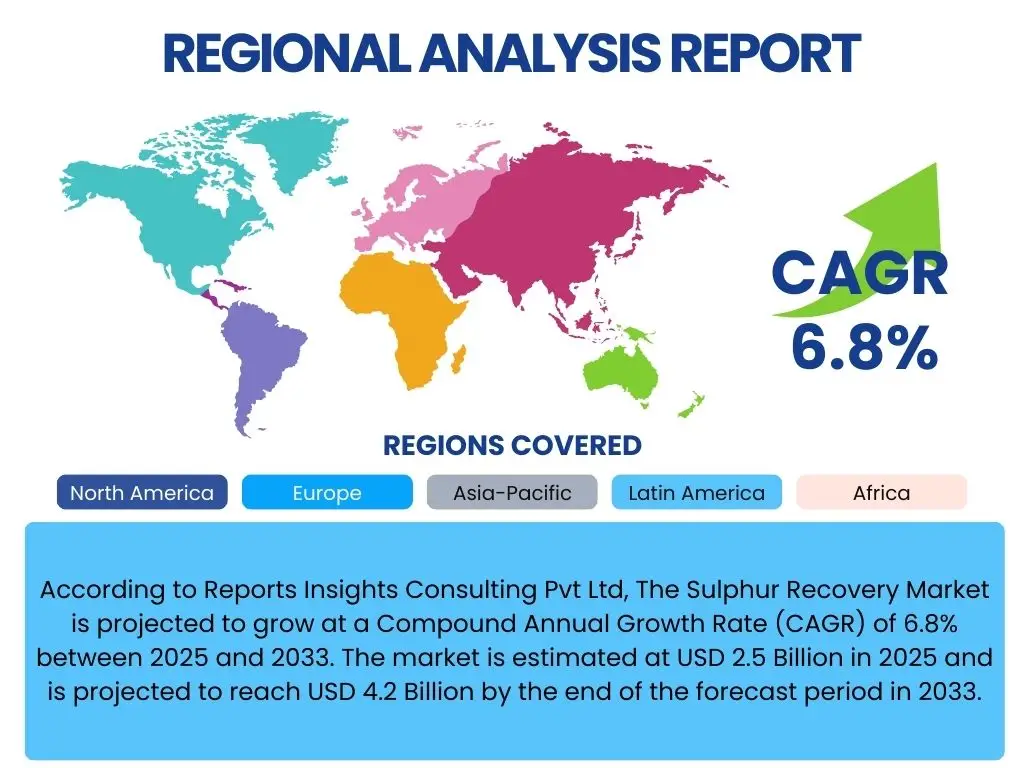

Regional Highlights

The global Sulphur Recovery Market exhibits diverse dynamics across different geographical regions, primarily influenced by regional environmental regulations, the concentration of heavy industries, and the availability of natural resources. North America and Europe, characterized by stringent environmental policies and mature industrial infrastructure, are leading in the adoption of advanced sulphur recovery technologies and have significant installed capacities. These regions often drive innovation in emissions reduction and operational efficiency, setting benchmarks for global compliance.

Asia Pacific is emerging as the fastest-growing market, propelled by rapid industrialization, increasing energy demand, and growing environmental awareness in countries like China, India, and Southeast Asian nations. The expansion of refining capacities and the discovery of new sour gas fields in this region are creating substantial demand for new sulphur recovery units. Meanwhile, the Middle East and Africa, with their vast oil and gas reserves, continue to be crucial markets, focusing on maximizing production while adhering to evolving environmental standards, especially in countries with significant export-oriented refining operations.

- North America: A mature market with established refining and natural gas processing sectors. Stringent environmental regulations, particularly from the EPA, drive continuous investment in upgrading and optimizing sulphur recovery units. The region is a key adopter of advanced technologies.

- Europe: Characterized by highly restrictive environmental policies aimed at reducing industrial emissions. Emphasis on sustainable practices and circular economy principles drives demand for high-efficiency sulphur recovery and valorization technologies.

- Asia Pacific (APAC): The fastest-growing market, fueled by rapid industrialization, increasing energy consumption, and expanding refining and petrochemical capacities in China, India, and Southeast Asian countries. Growing awareness and stricter local environmental regulations are boosting adoption.

- Latin America: Exhibiting moderate growth, driven by increasing oil and gas exploration and production activities, particularly in Brazil, Mexico, and Argentina. Investment in new and upgraded refineries to process sour crude contributes to market expansion.

- Middle East & Africa (MEA): A significant market due to its immense oil and gas reserves and large-scale refining operations. The region focuses on optimizing existing facilities and developing new ones to meet both production targets and environmental compliance.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Sulphur Recovery Market.- Global Process Technologies

- Advanced Sulphur Solutions

- Environmental Process Engineers

- Integrated Gas Systems

- Pure Sulphur Technologies

- Catalytic Solutions Group

- Advanced Environmental Systems

- Industrial Process Innovations

- Energy & Chemical Systems

- NextGen Sulphur Solutions

- Green Sulphur Recovery

- Process Optimization Services

- Chemical Engineering Group

- Environmental Compliance Services

- Refinery Solutions Providers

Frequently Asked Questions

What is sulphur recovery and why is it important?

Sulphur recovery is a process that removes sulfur compounds, primarily hydrogen sulfide (H2S), from industrial gas streams and converts them into elemental sulfur or other usable forms. It is crucial for environmental protection, preventing the release of sulfur dioxide (SO2) into the atmosphere, which causes acid rain and respiratory issues. It also recovers a valuable commodity from waste streams.

What are the main technologies used for sulphur recovery?

The primary technology for sulphur recovery is the Claus process, which converts H2S into elemental sulfur. It is often followed by a Tail Gas Treatment (TGT) unit, such as SCOT or CBA, to achieve ultra-high recovery efficiencies and meet stringent emission limits. Biological processes are also used in specific applications for H2S removal.

Which industries are the primary users of sulphur recovery systems?

The main industries driving the demand for sulphur recovery systems include oil and gas refining, natural gas processing, chemical manufacturing, metals and mining (smelters), and, in some cases, power generation (flue gas desulfurization). These sectors produce significant sulfur-containing waste gases that require treatment.

What are the key drivers for the Sulphur Recovery Market growth?

Key drivers include increasingly stringent global environmental regulations on sulfur dioxide emissions, the rising global demand for cleaner fuels (requiring desulfurization of crude oil and natural gas), and expanding industrialization, particularly in emerging economies with growing refining and chemical sectors.

What are the future trends in sulphur recovery technology?

Future trends include the development of more energy-efficient and compact sulphur recovery units, increased integration of automation and artificial intelligence for process optimization and predictive maintenance, a focus on valorizing recovered sulfur into diverse commercial products, and the exploration of novel biological or advanced catalytic processes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted