Subsea Production system Market

Subsea Production system Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700374 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

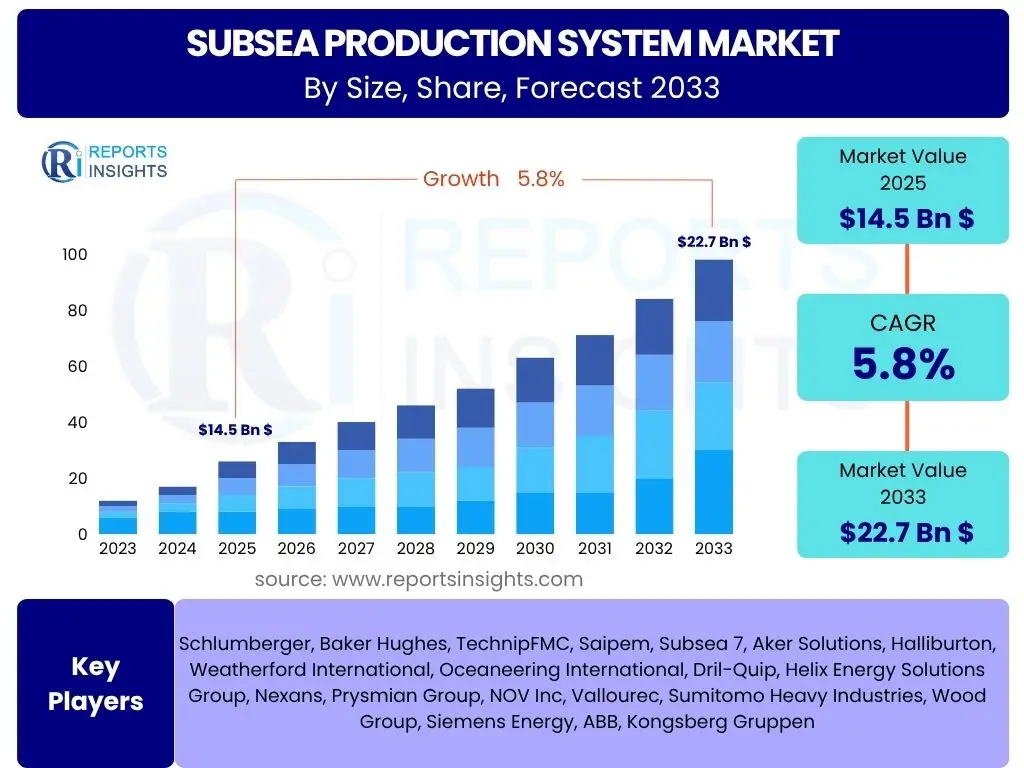

Subsea Production system Market Size

The global Subsea Production System Market is projected to exhibit robust expansion, driven by increasing offshore exploration and production activities, alongside technological advancements aimed at enhancing efficiency and reliability in challenging deepwater environments. The market's growth trajectory is a testament to the essential role subsea infrastructure plays in accessing hydrocarbon reserves located beneath the seabed. This market encompasses a wide array of equipment and services, including subsea trees, manifolds, control systems, and processing units, all designed to facilitate the extraction and transportation of oil and gas from subsea wells to surface facilities.

The complexity and capital-intensive nature of subsea projects necessitate significant investment, yet the long-term energy demand and the economic viability of deepwater fields continue to propel market expansion. Operators are increasingly focusing on optimizing existing assets through upgrades and life extension programs, further contributing to market dynamism. Furthermore, the integration of advanced digital technologies, such as artificial intelligence and real-time data analytics, is revolutionizing subsea operations, promising greater operational efficiency, reduced intervention costs, and improved safety standards across the lifecycle of subsea fields.

The Subsea Production System Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, valued at $14.5 Billion USD in 2025 and is projected to grow to $22.7 Billion USD by 2033, the end of the forecast period.

Key Subsea Production system Market Trends & Insights

The Subsea Production System Market is undergoing significant transformations, driven by evolving energy landscapes, technological breakthroughs, and a heightened focus on operational efficiency and environmental sustainability. These trends are shaping investment decisions, technological development paths, and strategic partnerships across the industry. Understanding these dynamics is crucial for stakeholders to navigate the market effectively and capitalize on emerging opportunities.

One prominent trend is the increasing adoption of subsea processing and boosting technologies, which enable hydrocarbons to be processed on the seabed, closer to the wellhead. This reduces the need for complex and costly topside facilities, improves recovery rates, and enhances overall project economics. Another key trend is the growing emphasis on digitalization and automation, integrating advanced sensors, real-time data analytics, and remote operation capabilities to optimize subsea field performance, predict equipment failures, and minimize human intervention. This shift towards intelligent subsea systems is paving the way for more autonomous operations and predictive maintenance strategies, leading to substantial cost savings and improved operational reliability. Furthermore, the industry is seeing a renewed focus on standardization and modularity in subsea equipment design, aiming to reduce project lead times, lower manufacturing costs, and enhance interchangeability across different projects, thereby increasing efficiency and mitigating project risks. The ongoing energy transition also plays a role, with some subsea capabilities being explored for carbon capture and storage (CCS) projects and offshore renewable energy infrastructure, indicating a potential diversification for subsea expertise beyond traditional oil and gas applications.

- Increasing deepwater and ultra-deepwater exploration and production activities.

- Rising adoption of subsea processing and boosting technologies.

- Growing digitalization and automation in subsea field operations.

- Emphasis on standardization and modularization of subsea equipment.

- Focus on life extension and brownfield optimization for existing assets.

- Emergence of integrated subsea solutions and all-electric subsea systems.

- Shift towards remote monitoring and predictive maintenance strategies.

- Exploration of subsea technologies for carbon capture and storage (CCS) and offshore renewables.

AI Impact Analysis on Subsea Production system

Artificial Intelligence (AI) is rapidly transforming the subsea production system market, offering unprecedented opportunities for enhanced operational efficiency, cost reduction, and safety improvements. The application of AI algorithms, machine learning models, and advanced analytics in subsea environments enables operators to derive actionable insights from vast amounts of sensor data, automate complex tasks, and optimize production processes in ways previously unimaginable. This technological integration is pivotal in tackling the inherent challenges of deepwater operations, such as extreme pressures, remote locations, and the high cost of human intervention.

AI's impact spans various aspects of subsea operations, from predictive maintenance and real-time anomaly detection to optimized well performance and autonomous system control. By analyzing historical data and live sensor feeds, AI can forecast equipment failures, schedule maintenance proactively, and reduce unscheduled downtime, thereby significantly lowering operational expenditures. Furthermore, AI-powered systems can optimize reservoir drainage, manage flow assurance, and control subsea equipment with greater precision, leading to increased hydrocarbon recovery and reduced energy consumption. The development of AI-driven autonomous underwater vehicles (AUVs) and remotely operated vehicles (ROVs) equipped with intelligent navigation and inspection capabilities is also revolutionizing subsea inspection, maintenance, and repair (IMR) activities, making them safer, faster, and more cost-effective. The integration of AI into subsea production systems is not merely an incremental improvement but a fundamental shift towards a more intelligent, efficient, and resilient offshore energy industry.

- Enhanced predictive maintenance and anomaly detection, reducing downtime.

- Optimization of well performance and reservoir management through data analytics.

- Automation of routine inspection, maintenance, and repair (IMR) tasks via intelligent ROVs/AUVs.

- Improved safety by minimizing human exposure to hazardous subsea environments.

- Real-time data processing for better decision-making and operational efficiency.

- Development of autonomous subsea control systems.

- Cost reduction through optimized asset utilization and reduced manual interventions.

Key Takeaways Subsea Production system Market Size & Forecast

- The Subsea Production System Market is projected for substantial growth, driven by deepwater E&P and technological advancements.

- A robust CAGR of 5.8% is anticipated from 2025 to 2033, indicating steady market expansion.

- Market valuation is set to increase from $14.5 Billion USD in 2025 to $22.7 Billion USD by 2033.

- Technological innovations, especially in subsea processing and digitalization, are key enablers of this growth.

- The market is seeing a strategic shift towards cost efficiency, standardization, and optimized asset management.

- AI integration is becoming critical for predictive maintenance, automation, and operational intelligence.

- The long-term outlook remains positive due to sustained global energy demand and the economic viability of subsea reserves.

Subsea Production system Market Drivers Analysis

The global Subsea Production System Market is fundamentally driven by a confluence of factors stemming from the intricate dynamics of the global energy sector and continuous technological evolution. The imperative to meet persistent energy demand, coupled with the increasing depletion of onshore and shallow-water reserves, has significantly intensified the focus on deepwater and ultra-deepwater exploration and production activities. These frontier areas, rich in hydrocarbon potential, are inaccessible without sophisticated subsea infrastructure, thus directly fueling the market's expansion.

Furthermore, technological advancements play a pivotal role in making deepwater projects economically viable and technically feasible. Innovations in subsea processing, boosting, and intelligent well technologies enhance recovery rates, reduce the need for expensive topside facilities, and improve overall operational efficiency. The industry's growing emphasis on maximizing asset lifecycle and optimizing brownfield operations also contributes significantly, as existing infrastructure requires upgrades, maintenance, and life extension services. Additionally, favorable government policies and regulatory frameworks in certain regions that incentivize offshore investment, along with strategic partnerships among oil companies, service providers, and technology developers, create an enabling environment for market growth. These drivers collectively underpin the sustained demand for subsea production systems, ensuring their critical role in the global energy supply chain.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Deepwater and Ultra-Deepwater E&P Activities | +1.5% | Brazil, West Africa, Gulf of Mexico, Norway, Canada | Long-term (2025-2033) |

| Technological Advancements in Subsea Processing & Boosting | +1.2% | Global, particularly in mature basins and new deepwater fields | Mid to Long-term (2025-2033) |

| Rising Global Energy Demand & Depleting Onshore Reserves | +1.0% | Asia Pacific, North America, Europe | Long-term (2025-2033) |

| Focus on Life Extension & Brownfield Optimization | +0.8% | North Sea, Gulf of Mexico, Southeast Asia | Mid-term (2025-2030) |

Subsea Production system Market Restraints Analysis

Despite its significant growth potential, the Subsea Production System Market faces several notable restraints that could temper its expansion. One of the most significant inhibiting factors is the inherent volatility of global crude oil and natural gas prices. Fluctuations in commodity prices directly influence the profitability of offshore projects, leading to deferrals or cancellations of new investments in subsea infrastructure during periods of low prices. The capital-intensive nature of deepwater exploration and production, coupled with the long lead times for project development, makes these ventures particularly susceptible to market uncertainties, impacting investor confidence and capital allocation.

Furthermore, stringent environmental regulations and increasing global pressure to transition towards renewable energy sources pose a long-term challenge. Governments and international bodies are imposing stricter emission standards and promoting decarbonization efforts, which could potentially slow down new offshore hydrocarbon developments. While subsea technology can offer environmental benefits compared to some onshore operations, the overarching shift in energy policy creates a cautious investment climate for fossil fuel projects. High upfront capital expenditure requirements and the complexity of subsea engineering, coupled with risks associated with deepwater operations such as equipment failures and potential environmental incidents, also act as formidable restraints, raising the financial and operational burden for market players. These combined factors necessitate careful strategic planning and risk mitigation by companies operating within the subsea production system market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Crude Oil and Gas Prices | -0.9% | Global | Short to Mid-term (2025-2028) |

| High Capital Expenditure and Project Complexity | -0.7% | Global, particularly for new deepwater developments | Long-term (2025-2033) |

| Stringent Environmental Regulations and Energy Transition Pressure | -0.6% | Europe, North America, parts of Asia Pacific | Long-term (2025-2033) |

Subsea Production system Market Opportunities Analysis

Opportunities within the Subsea Production System Market are emerging from various strategic shifts and technological advancements, presenting avenues for growth and diversification. One significant opportunity lies in the accelerating trend of digitalization and automation across the oil and gas industry. The integration of advanced analytics, artificial intelligence, and Internet of Things (IoT) sensors into subsea systems allows for real-time monitoring, predictive maintenance, and optimized operational control. This not only enhances efficiency and reduces operational costs but also opens new revenue streams for companies specializing in data management, software solutions, and remote operational services for subsea assets.

Furthermore, the growing demand for natural gas as a cleaner transitional fuel is creating new opportunities for subsea gas field developments, particularly in regions with significant untapped reserves. Subsea technology is crucial for unlocking these resources efficiently and safely. Beyond traditional hydrocarbon exploration, the expertise and infrastructure developed for subsea production systems are finding new applications in emerging sectors. These include the development of subsea infrastructure for carbon capture, utilization, and storage (CCUS) projects, where CO2 is injected and stored beneath the seabed, and the expansion of offshore renewable energy infrastructure, such as floating wind farms and wave energy converters, which may require subsea cabling and connection systems. The drive towards standardized and modular subsea systems also presents an opportunity to streamline project execution, reduce costs, and accelerate market penetration, benefiting both suppliers and operators by enhancing project predictability and scalability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Digitalization & Automation Technologies | +1.3% | Global, with strong adoption in mature markets | Mid to Long-term (2025-2033) |

| Development of New Gas Fields & Gas Infrastructure | +1.0% | Middle East, Asia Pacific, North America, Africa | Long-term (2025-2033) |

| Expansion into Carbon Capture & Storage (CCS) and Offshore Renewables | +0.8% | Europe, North America, Australia | Long-term (2028-2033) |

Subsea Production system Market Challenges Impact Analysis

The Subsea Production System Market, despite its strategic importance, faces a series of complex challenges that can impede its growth and operational efficiency. One significant hurdle is the inherently high operational expenditure and capital intensity associated with deploying and maintaining subsea infrastructure in deepwater environments. The extreme pressures, low temperatures, and corrosive nature of the subsea world demand highly specialized, robust, and often custom-engineered equipment, leading to substantial upfront investments and ongoing maintenance costs. Any unexpected failures or the need for intervention can incur significant financial penalties and operational downtime, making risk management a critical concern for operators.

Furthermore, the global supply chain for subsea components and services is often complex and susceptible to disruptions. Geopolitical tensions, trade disputes, and global events like pandemics can impact the availability of critical materials, components, and specialized vessels, leading to project delays and increased costs. Another prominent challenge is the shortage of highly skilled professionals with expertise in subsea engineering, operations, and maintenance. The specialized nature of the field requires continuous training and development, and a demographic shift in the workforce could exacerbate talent gaps, affecting project execution and innovation. Navigating the evolving regulatory landscape, which is increasingly focused on environmental protection and safety, also presents a challenge, requiring continuous adaptation of technologies and practices to ensure compliance and mitigate risks. Addressing these challenges effectively will be crucial for sustainable development and long-term success in the subsea production system market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Operational & Capital Expenditure | -0.8% | Global, especially for new projects | Long-term (2025-2033) |

| Supply Chain Vulnerabilities & Disruptions | -0.5% | Global | Short to Mid-term (2025-2028) |

| Skilled Workforce Shortage | -0.4% | North America, Europe, parts of Asia | Long-term (2025-2033) |

Subsea Production system Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Subsea Production System Market, offering critical insights into its current size, growth trajectories, and future outlook. The report meticulously examines the key trends, drivers, restraints, opportunities, and challenges shaping the industry landscape. It delves into the impact of emerging technologies, including artificial intelligence and automation, on subsea operations and market dynamics. The study encompasses a detailed segmentation analysis, regional deep-dives, and competitive landscape assessment, presenting a holistic view for stakeholders to make informed strategic decisions. The scope is designed to provide both historical context and forward-looking projections, ensuring a thorough understanding of market evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | $14.5 Billion USD |

| Market Forecast in 2033 | $22.7 Billion USD |

| Growth Rate | 5.8% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Schlumberger, Baker Hughes, TechnipFMC, Saipem, Subsea 7, Aker Solutions, Halliburton, Weatherford International, Oceaneering International, Dril-Quip, Helix Energy Solutions Group, Nexans, Prysmian Group, NOV Inc, Vallourec, Sumitomo Heavy Industries, Wood Group, Siemens Energy, ABB, Kongsberg Gruppen |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis:

The Subsea Production System Market is meticulously segmented to provide a granular understanding of its diverse components, operational contexts, and application areas. This segmentation facilitates a deeper analysis of specific market niches, identifies high-growth segments, and allows stakeholders to pinpoint areas of strategic interest. Each segment represents a critical aspect of the subsea value chain, contributing uniquely to the overall market dynamics. The careful breakdown by component, water depth, application, and type enables a comprehensive assessment of both current market structure and future growth opportunities, reflecting the specialized requirements and evolving technological landscape of offshore energy production.

The 'By Component' segmentation details the various specialized equipment crucial for subsea operations, from the foundational subsea trees to complex control systems and flow assurance technologies. The 'By Water Depth' category highlights the technical complexities and investment profiles associated with different operational environments, distinguishing between shallow, deep, and ultra-deepwater projects, each presenting unique engineering challenges and market requirements. The 'By Application' segment delineates the primary end-uses, predominantly oil and gas exploration and production, but also expanding into emerging fields like carbon capture and offshore renewables, signaling the market's potential for diversification. Finally, the 'By Type' segmentation differentiates between new field developments, existing field expansions or upgrades, and decommissioning activities, reflecting the full lifecycle of subsea assets and the varied demand patterns across these stages. This multi-dimensional segmentation provides a robust framework for market analysis and strategic planning.

- By Component:

- Subsea Trees (Vertical, Horizontal)

- Manifolds

- Risers & Flowlines

- Control Systems (Hydraulic, Electro-Hydraulic, All-Electric)

- Umbilicals

- PLETs & PIG Loops

- Subsea Pumps & Compressors

- Connectors & Jumpers

- Others (e.g., actuators, valves, instrumentation)

- By Water Depth:

- Shallow Water

- Deepwater

- Ultra-Deepwater

- By Application:

- Oil & Gas (Exploration & Production)

- Carbon Capture Utilization & Storage (CCUS)

- Offshore Renewables (e.g., offshore wind power subsea components, though nascent)

- By Type:

- New Field Development

- Field Expansion/Upgrade

- Decommissioning

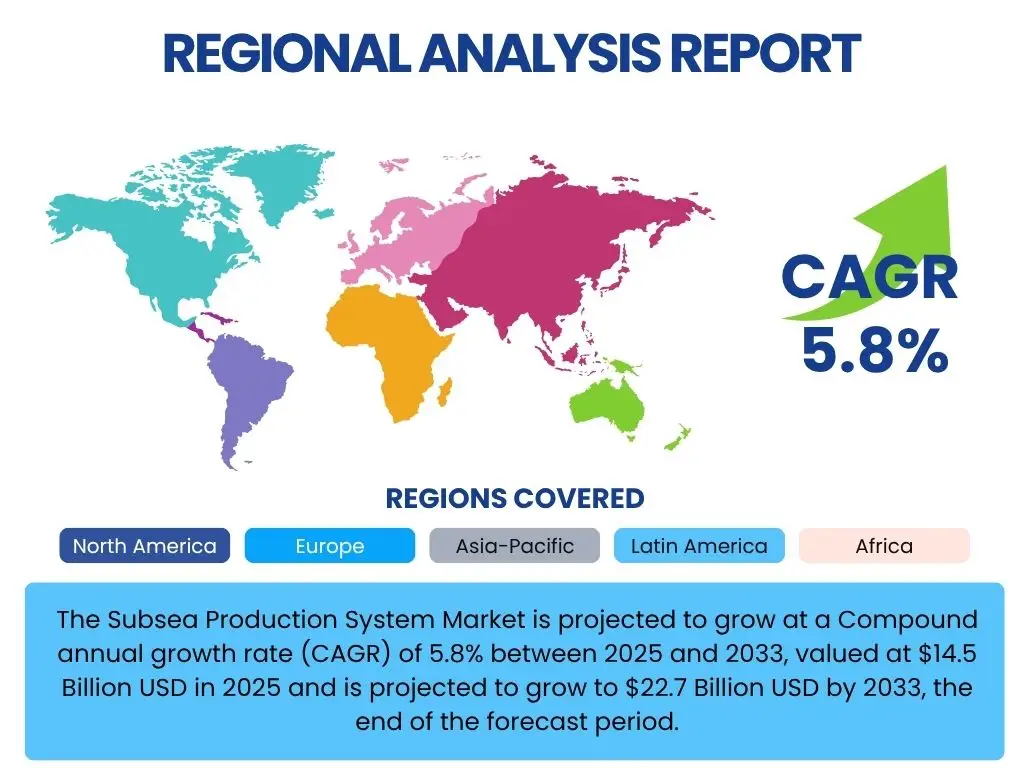

Regional Highlights

The global Subsea Production System Market exhibits distinct regional dynamics, influenced by varying levels of offshore hydrocarbon reserves, regulatory environments, technological adoption rates, and investment capacities. Understanding these regional nuances is paramount for market participants to tailor their strategies and capitalize on specific opportunities. Key regions such as North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa each present unique drivers and challenges that shape their contribution to the overall market growth. The regional analysis identifies areas of high potential and provides insights into the prevailing market conditions and future outlook in each geographical segment, reflecting the localized interplay of economic, political, and technological factors.

North America, particularly the Gulf of Mexico, remains a significant market, driven by deepwater and ultra-deepwater exploration and production, alongside technological innovation aimed at optimizing operations and reducing costs. Europe, while experiencing a decline in new oil and gas field developments in the North Sea due to energy transition policies, shows increasing opportunities in decommissioning activities and the nascent subsea infrastructure for offshore wind and carbon capture and storage. Latin America, propelled by Brazil's pre-salt discoveries, represents a robust growth region with substantial ongoing and planned deepwater projects. The Asia Pacific region is emerging as a critical growth hub, driven by increasing energy demand from developing economies like China, India, and Australia, leading to new offshore field developments and upgrades. Finally, the Middle East and Africa region, with vast untapped offshore reserves in West Africa and East Africa, coupled with a renewed focus on gas development, promises significant future investments in subsea production systems. Each region's unique blend of resource availability, operational maturity, and strategic priorities dictates its role and trajectory within the global subsea market.

- North America: This region, particularly the U.S. Gulf of Mexico, is a mature but consistently active market. It is characterized by significant deepwater and ultra-deepwater exploration and production activities, a strong emphasis on technological innovation for cost reduction and efficiency, and a robust service infrastructure. The focus is on maximizing recovery from existing fields and selectively pursuing new high-value deepwater projects.

- Europe: The European market, especially the UK and Norway in the North Sea, is transitioning. While traditional oil and gas developments are slowing, there's a strong push for life extension of existing assets, decommissioning, and the leveraging of subsea expertise for new energy applications like offshore wind and Carbon Capture and Storage (CCS). Research and development in subsea processing and all-electric systems remain strong.

- Asia Pacific (APAC): This is one of the fastest-growing regions, driven by surging energy demand from emerging economies like China, India, and Southeast Asian countries (e.g., Malaysia, Indonesia, Australia). New offshore gas field developments are prominent, along with significant investments in both shallow and deepwater projects to meet domestic energy needs, making it a key area for new installations.

- Latin America: Dominated by Brazil, this region holds vast pre-salt deepwater reserves, making it a critical growth engine for the subsea market. Significant investments are ongoing for large-scale deepwater oil and gas projects, requiring advanced subsea technologies for complex reservoirs. Countries like Mexico and Guyana are also emerging with growing offshore potential.

- Middle East and Africa (MEA): West Africa (e.g., Angola, Nigeria) remains a core deepwater market, characterized by major international oil companies' presence. East Africa (e.g., Mozambique, Tanzania) is emerging with large offshore gas discoveries. The Middle East, while traditionally onshore-focused, is increasingly exploring its offshore potential, particularly for gas, contributing to a diversified demand for subsea systems.

Top Key Players:

The market research report covers the analysis of key stake holders of the Subsea Production system Market. Some of the leading players profiled in the report include -

- Schlumberger

- Baker Hughes

- TechnipFMC

- Saipem

- Subsea 7

- Aker Solutions

- Halliburton

- Weatherford International

- Oceaneering International

- Dril-Quip

- Helix Energy Solutions Group

- Nexans

- Prysmian Group

- NOV Inc

- Vallourec

- Sumitomo Heavy Industries

- Wood Group

- Siemens Energy

- ABB

- Kongsberg Gruppen

Frequently Asked Questions:

What is a Subsea Production System?

A Subsea Production System is a collection of equipment and infrastructure installed on the seabed to extract and process hydrocarbons (oil and gas) from offshore wells. It typically includes subsea trees, manifolds, risers, flowlines, and control systems, designed to operate in challenging underwater environments and transport produced fluids to surface facilities or pipelines.

What are the primary drivers of the Subsea Production System Market?

The primary drivers include the increasing global energy demand, the depletion of onshore and shallow-water hydrocarbon reserves necessitating deepwater and ultra-deepwater exploration, and continuous technological advancements in subsea processing and boosting that make complex offshore projects economically viable and technically feasible.

How is AI impacting the Subsea Production System Market?

Artificial Intelligence (AI) is significantly impacting the market by enabling enhanced predictive maintenance, real-time data analysis for optimized well performance, automation of inspection and repair tasks via intelligent underwater vehicles, and improved safety protocols by minimizing human intervention. AI integration leads to greater operational efficiency, reduced downtime, and lower costs.

Which regions are leading in the adoption and investment in Subsea Production Systems?

Regions leading in adoption and investment include Latin America (driven by Brazil's deepwater pre-salt fields), North America (particularly the U.S. Gulf of Mexico for deepwater projects), and Asia Pacific (with growing offshore E&P in countries like China, India, and Australia). West Africa and the emerging East African gas plays also represent significant investment areas.

What are the key challenges facing the Subsea Production System Market?

Key challenges include the high capital expenditure and operational costs associated with deepwater projects, the inherent volatility of crude oil and gas prices, potential disruptions in the global supply chain, a shortage of highly skilled professionals, and the increasing stringency of environmental regulations alongside pressure from the global energy transition.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted