Styrenic Block Copolymer Market

Styrenic Block Copolymer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703354 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

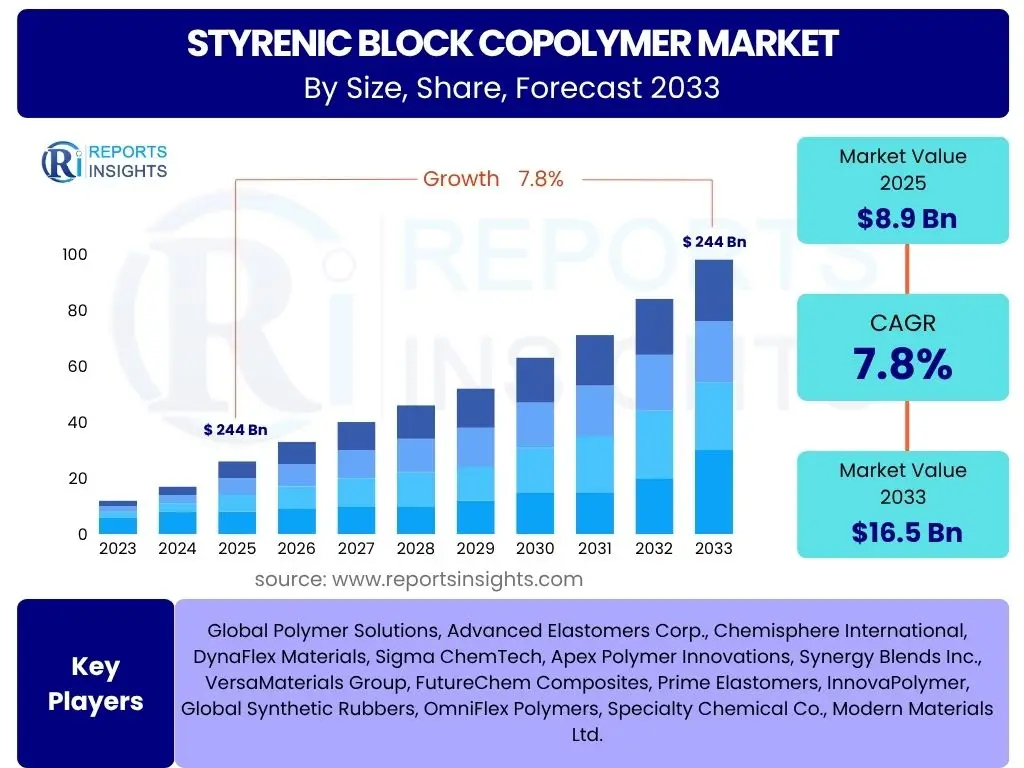

Styrenic Block Copolymer Market Size

According to Reports Insights Consulting Pvt Ltd, The Styrenic Block Copolymer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 8.9 billion in 2025 and is projected to reach USD 16.5 billion by the end of the forecast period in 2033.

Key Styrenic Block Copolymer Market Trends & Insights

The Styrenic Block Copolymer (SBC) market is experiencing significant shifts driven by evolving industrial demands and technological advancements. A prominent trend is the increasing demand for sustainable and bio-based SBCs, as industries seek to reduce their environmental footprint and comply with stringent regulations. This push for sustainability is prompting manufacturers to invest in research and development for renewable raw material sources and more eco-friendly production processes, appealing to a growing segment of environmentally conscious consumers and businesses. Furthermore, the expansion of applications in specialized fields such as medical devices, electric vehicle components, and advanced packaging solutions is also shaping market dynamics. These applications often require specific performance characteristics from SBCs, including enhanced elasticity, durability, and processing efficiency.

Another key trend involves the rising adoption of SBCs in various high-performance applications, largely due to their unique combination of elasticity and strength, which makes them ideal for replacing traditional materials like rubber and PVC. The automotive industry, for instance, is increasingly utilizing SBCs for lightweight components, interior trim, and vibration damping, contributing to fuel efficiency and improved vehicle performance. Similarly, the footwear industry continues to rely on SBCs for durable and comfortable soles, while the adhesives and sealants sector benefits from their excellent bonding properties. The continuous innovation in polymerization techniques and compound formulations is also enabling the development of SBCs with tailored properties, further expanding their utility and market reach across diverse sectors globally.

- Growing demand for sustainable and bio-based SBC solutions.

- Increasing adoption in lightweight automotive components for fuel efficiency.

- Expansion into specialized medical and healthcare applications.

- Technological advancements in polymerization and compounding.

- Rising demand for high-performance adhesives and sealants.

- Shift towards more durable and comfortable materials in footwear.

AI Impact Analysis on Styrenic Block Copolymer

Artificial Intelligence (AI) is poised to revolutionize various aspects of the Styrenic Block Copolymer (SBC) industry by enhancing efficiency, optimizing processes, and accelerating innovation. Manufacturers are exploring AI-driven solutions for predictive maintenance of production equipment, which can significantly reduce downtime and improve operational reliability. AI algorithms can analyze vast datasets from sensors and historical performance records to identify potential failures before they occur, allowing for proactive interventions. Furthermore, AI is increasingly being applied in quality control, utilizing machine vision and deep learning to detect defects in SBC products with greater accuracy and speed than traditional methods, thereby ensuring consistent product quality and reducing waste. This proactive approach to production management minimizes operational costs and enhances overall manufacturing output.

Beyond manufacturing, AI holds substantial promise in the research and development (R&D) of new SBC formulations and properties. AI-powered simulations and material informatics can rapidly screen potential chemical combinations, predict material behaviors, and optimize compound designs for specific applications, dramatically shortening the product development cycle. This capability allows researchers to explore a wider range of possibilities for bio-based SBCs or specialized high-performance variants, accelerating the introduction of innovative products to the market. Moreover, AI can optimize supply chain logistics by predicting demand fluctuations, managing inventory, and streamlining distribution networks, leading to more resilient and responsive supply chains for raw materials and finished SBC products. The integration of AI tools is expected to foster a more agile, cost-effective, and innovative SBC market landscape.

- Enhanced predictive maintenance and operational efficiency in manufacturing.

- Improved quality control and defect detection using machine vision.

- Accelerated research and development of new SBC formulations.

- Optimized supply chain management and demand forecasting.

- Reduced material waste through precise process control.

- Data-driven insights for strategic market expansion.

Key Takeaways Styrenic Block Copolymer Market Size & Forecast

The Styrenic Block Copolymer (SBC) market is poised for robust growth, primarily driven by its expanding applications across diverse end-use industries and the continuous innovation in material properties. A significant takeaway is the strong demand originating from the automotive, construction, and footwear sectors, where SBCs are valued for their lightweight, flexible, and durable characteristics. This widespread adoption, coupled with the increasing preference for high-performance and sustainable materials, underscores the market's resilience and future potential. The forecast indicates a steady upward trajectory, highlighting the industry's capacity to adapt to evolving consumer preferences and regulatory landscapes, particularly concerning environmental sustainability.

Another crucial insight is the increasing emphasis on research and development to create advanced SBCs with enhanced thermal stability, chemical resistance, and processability. This innovation is vital for opening new market avenues, especially in specialized segments such as medical tubing, protective coatings, and advanced packaging films. Geographically, Asia Pacific is anticipated to remain a dominant force, fueled by rapid industrialization and escalating demand from emerging economies. Companies are strategically focusing on capacity expansion and developing customized solutions to cater to specific regional requirements, reinforcing the market's dynamic nature and competitive intensity. The overall outlook remains highly positive, with significant opportunities for stakeholders to capitalize on emerging trends and technological advancements.

- Consistent growth projected across diverse end-use industries.

- Strong demand driven by automotive, construction, and footwear sectors.

- Increasing focus on sustainable and high-performance SBC variants.

- Technological advancements are expanding application areas.

- Asia Pacific remains a key growth engine for the market.

- Innovation in specialized SBC formulations is crucial for market expansion.

Styrenic Block Copolymer Market Drivers Analysis

The Styrenic Block Copolymer (SBC) market is significantly propelled by the increasing demand from various end-use industries, particularly the automotive, construction, and footwear sectors. In the automotive industry, SBCs are extensively used for lightweighting vehicle components, interior parts, and vibration damping, which directly contributes to fuel efficiency and reduced carbon emissions. The construction sector utilizes SBCs in asphalt modification for roofing and paving, enhancing durability and performance, as well as in adhesives and sealants for improved bonding and flexibility. These applications underscore the versatility and superior performance characteristics of SBCs compared to traditional materials, driving their sustained adoption.

Furthermore, the growing global population and rising disposable incomes are fueling demand for consumer goods, including footwear, where SBCs are crucial for comfortable, lightweight, and durable soles. The continuous innovation in polymer science and material engineering is also a key driver, leading to the development of novel SBC grades with tailored properties for specific high-performance applications. This includes enhanced elasticity, tensile strength, and processing efficiency, which opens new avenues in medical devices, wire and cable insulation, and advanced packaging solutions. The ability of SBCs to offer a superior balance of properties like flexibility, impact strength, and transparency makes them an attractive choice across a wide spectrum of manufacturing processes.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Automotive Industry | +1.5% | North America, Europe, Asia Pacific (China, Japan) | 2025-2033 (Mid to Long-term) |

| Growth in Construction & Paving Sector | +1.2% | Asia Pacific (India, China), Middle East | 2025-2033 (Mid to Long-term) |

| Rising Adoption in Footwear & Consumer Goods | +0.9% | Asia Pacific, Latin America | 2025-2030 (Short to Mid-term) |

| Technological Advancements & Product Innovation | +0.8% | Global | 2025-2033 (Continuous) |

| Demand for High-Performance Adhesives & Sealants | +0.7% | North America, Europe, Asia Pacific | 2025-2030 (Short to Mid-term) |

Styrenic Block Copolymer Market Restraints Analysis

The Styrenic Block Copolymer (SBC) market faces significant restraints, primarily due to the volatility of raw material prices, which can directly impact production costs and profit margins for manufacturers. Key raw materials such as styrene, butadiene, and isoprene are petrochemical derivatives, and their prices are subject to fluctuations in crude oil prices, geopolitical tensions, and supply-demand imbalances. This unpredictability makes it challenging for manufacturers to maintain stable pricing strategies and can lead to increased operational expenses, potentially hindering market growth. Companies must develop robust supply chain management strategies and hedging mechanisms to mitigate these risks, often leading to complex procurement processes.

Another notable restraint is the increasing environmental scrutiny and stringent regulations surrounding the use of synthetic polymers and their disposal. While SBCs are recyclable, their non-biodegradable nature raises concerns regarding plastic waste and pollution. Growing public and regulatory pressure for sustainable alternatives and stricter waste management policies can lead to increased compliance costs for manufacturers. Additionally, the availability of alternative materials, such as thermoplastic polyurethanes (TPUs) and thermoplastic olefins (TPOs), which offer similar performance characteristics for certain applications, can pose a competitive threat, especially in price-sensitive markets. These factors necessitate continuous innovation in sustainable formulations and recycling technologies to maintain market competitiveness.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -1.0% | Global | 2025-2033 (Continuous) |

| Stringent Environmental Regulations | -0.7% | Europe, North America | 2026-2033 (Mid to Long-term) |

| Availability of Substitute Materials | -0.5% | Global | 2025-2030 (Short to Mid-term) |

| High Energy Consumption in Production | -0.3% | Global | 2025-2033 (Long-term) |

Styrenic Block Copolymer Market Opportunities Analysis

The Styrenic Block Copolymer (SBC) market presents significant opportunities driven by the growing demand for sustainable and bio-based polymer solutions. As environmental concerns intensify and regulatory frameworks become more stringent, manufacturers are actively investing in the development of SBCs derived from renewable resources, such as bio-butadiene or bio-isoprene. This shift towards sustainable alternatives not only addresses ecological concerns but also opens new market segments for eco-conscious consumers and industries. Innovations in green chemistry and polymerization processes are making these bio-based SBCs more economically viable and performance-competitive, positioning them as a key area for future growth and differentiation within the market.

Furthermore, the expansion of electric vehicle (EV) manufacturing globally offers a substantial opportunity for SBCs. EVs require lightweight, durable, and vibration-damping materials for various components, including battery housings, interior parts, and charging cables. SBCs, with their excellent flexibility, impact resistance, and sound dampening properties, are ideally suited for these applications, contributing to both vehicle performance and passenger comfort. The burgeoning medical and healthcare sector also represents a lucrative opportunity, as SBCs are increasingly utilized in applications requiring biocompatibility, clarity, and sterilization capabilities, such as medical tubing, IV bags, and drug delivery systems. The ongoing research into advanced composites and additive manufacturing processes further broadens the scope for SBC applications, enabling customized and intricate designs for diverse industrial needs.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based SBCs | +1.3% | Europe, North America, Asia Pacific | 2027-2033 (Mid to Long-term) |

| Increasing Adoption in Electric Vehicles (EVs) | +1.1% | Asia Pacific (China), Europe, North America | 2025-2033 (Mid to Long-term) |

| Expansion in Medical & Healthcare Sector | +0.9% | North America, Europe | 2025-2030 (Short to Mid-term) |

| Advancements in Additive Manufacturing | +0.6% | Global | 2028-2033 (Long-term) |

| Untapped Potential in Emerging Economies | +0.5% | Latin America, Southeast Asia, Africa | 2025-2033 (Long-term) |

Styrenic Block Copolymer Market Challenges Impact Analysis

The Styrenic Block Copolymer (SBC) market faces several challenges that can impede its growth trajectory. One significant challenge is the intense competition within the specialty chemicals and polymers sector. The market is characterized by the presence of a few large, established players alongside numerous smaller regional manufacturers, leading to aggressive pricing strategies and continuous innovation demands. Companies must consistently invest in research and development to differentiate their products and maintain a competitive edge, which can be resource-intensive. This competitive pressure often leads to compressed profit margins, especially for standardized SBC grades, compelling manufacturers to focus on higher-value, specialized applications.

Another major challenge is managing complex and global supply chains, particularly for raw materials derived from petroleum. Geopolitical instability, trade disputes, and natural disasters can disrupt the supply of styrene, butadiene, and isoprene, leading to supply shortages and price spikes. Ensuring a stable and cost-effective supply of these critical inputs requires sophisticated logistics and risk management strategies. Furthermore, the industry faces the challenge of adapting to rapidly evolving regulatory landscapes concerning environmental impact and product safety. Compliance with stricter emission standards, chemical restrictions, and waste management directives requires significant investments in cleaner production technologies and sustainable product development, posing a considerable hurdle for market players, especially smaller enterprises. Overcoming these challenges necessitates a blend of technological innovation, strategic partnerships, and robust operational resilience.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition | -0.8% | Global | 2025-2033 (Continuous) |

| Supply Chain Disruptions & Volatility | -0.6% | Global | 2025-2030 (Short to Mid-term) |

| Evolving Regulatory Landscape & Compliance Costs | -0.5% | Europe, North America, East Asia | 2026-2033 (Mid to Long-term) |

| High R&D Investment for New Formulations | -0.4% | Global | 2025-2033 (Continuous) |

| Consumer Preference for Sustainable Alternatives | -0.3% | Europe, North America | 2027-2033 (Long-term) |

Styrenic Block Copolymer Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Styrenic Block Copolymer (SBC) market, offering a detailed analysis of its current size, historical performance, and future growth projections from 2025 to 2033. It provides an in-depth examination of key market trends, significant drivers, restraining factors, emerging opportunities, and critical challenges that shape the industry landscape. The report segments the market extensively by type, application, and end-use industry, providing granular insights into demand patterns and growth prospects across various segments. Furthermore, it highlights regional market dynamics, identifying key growth regions and countries, and features profiles of leading market participants, offering a holistic view for strategic decision-making in the SBC industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.9 billion |

| Market Forecast in 2033 | USD 16.5 billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Polymer Solutions, Advanced Elastomers Corp., Chemisphere International, DynaFlex Materials, Sigma ChemTech, Apex Polymer Innovations, Synergy Blends Inc., VersaMaterials Group, FutureChem Composites, Prime Elastomers, InnovaPolymer, Global Synthetic Rubbers, OmniFlex Polymers, Specialty Chemical Co., Modern Materials Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Styrenic Block Copolymer (SBC) market is segmented to provide a granular understanding of its diverse applications and market dynamics. This segmentation facilitates a detailed analysis of growth drivers and trends within specific product categories and end-use sectors. The market is broadly categorized by type, which includes Styrene-Butadiene-Styrene (SBS), Styrene-Isoprene-Styrene (SIS), Styrene-Ethylene-Butylene-Styrene (SEBS), and other specialized variants. Each type exhibits unique properties, making them suitable for distinct applications and influencing their market share. For instance, SBS is widely used in footwear and asphalt modification due to its cost-effectiveness and good processing characteristics, while SEBS offers enhanced heat resistance and UV stability, making it preferred for high-performance applications like automotive parts and medical devices.

Further segmentation by application highlights the varied industrial demands for SBCs. Key applications include adhesives and sealants, asphalt modification, footwear components, and automotive parts, among others. The end-use industry segmentation provides insight into the major sectors driving demand, such as Building & Construction, Automotive, Footwear, Packaging, and Medical & Healthcare. This multi-faceted approach to segmentation allows for a comprehensive assessment of the market's structure, identifying lucrative niches and areas of significant growth potential. Understanding these segments is crucial for manufacturers to tailor their product offerings, develop targeted marketing strategies, and allocate resources effectively across the global market.

- By Type:

- Styrene-Butadiene-Styrene (SBS)

- Styrene-Isoprene-Styrene (SIS)

- Styrene-Ethylene-Butylene-Styrene (SEBS)

- Styrene-Ethylene-Propylene-Styrene (SEPS)

- Other SBCs (e.g., S-SBCs, Hard Styrenics)

- By Application:

- Adhesives & Sealants

- Asphalt Modification (Paving & Roofing)

- Footwear

- Compounds & Blends

- Wire & Cable

- Automotive Components

- Medical Devices

- Consumer Goods

- Others

- By End-Use Industry:

- Building & Construction

- Automotive

- Footwear

- Packaging

- Electrical & Electronics

- Medical & Healthcare

- Consumer Products

- Industrial

- Others

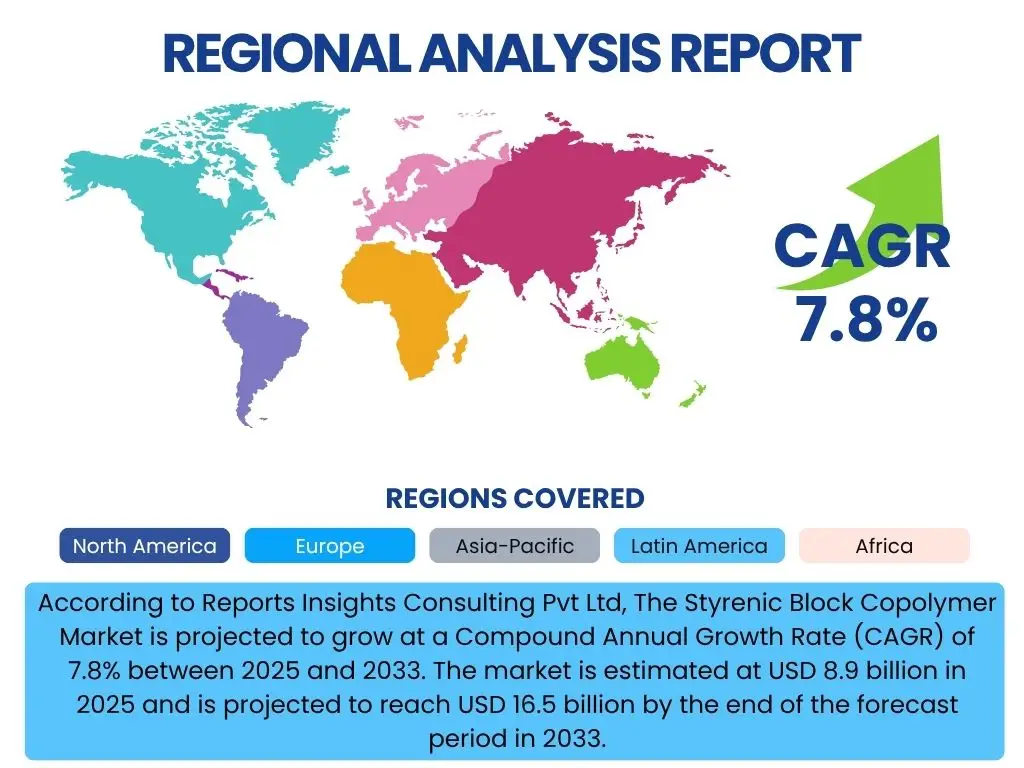

Regional Highlights

- Asia Pacific: This region is anticipated to be the largest and fastest-growing market for Styrenic Block Copolymers, primarily due to rapid industrialization, burgeoning manufacturing sectors, and increasing demand from developing economies such as China, India, and Southeast Asian countries. The strong growth in automotive production, infrastructure development, and consumer goods manufacturing in this region drives significant consumption of SBCs for various applications, including footwear, adhesives, and paving.

- North America: The North American market for SBCs is characterized by significant demand from the automotive, construction, and medical industries. The region's focus on technological advancements, lightweight materials for vehicles, and high-performance adhesives contributes to steady market growth. Strict regulatory standards for product quality and environmental performance also influence product development and adoption.

- Europe: Europe represents a mature but innovation-driven market for SBCs. Key drivers include the stringent environmental regulations promoting sustainable and recyclable materials, and the robust automotive and construction sectors. There is a strong emphasis on developing high-performance, specialized SBC grades for advanced applications and a growing adoption of bio-based solutions.

- Latin America: This region is expected to show moderate growth, driven by increasing construction activities, expanding automotive manufacturing, and rising disposable incomes leading to higher demand for consumer goods. Brazil and Mexico are key contributors to the market in this region, with opportunities for market penetration in various end-use sectors.

- Middle East and Africa (MEA): The MEA region offers emerging opportunities, especially in construction and infrastructure development projects, which drive demand for SBCs in asphalt modification and sealants. Growing industrialization and diversifying economies in countries like Saudi Arabia and UAE are also contributing to market expansion, albeit from a smaller base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Styrenic Block Copolymer Market.- Global Polymer Solutions

- Advanced Elastomers Corp.

- Chemisphere International

- DynaFlex Materials

- Sigma ChemTech

- Apex Polymer Innovations

- Synergy Blends Inc.

- VersaMaterials Group

- FutureChem Composites

- Prime Elastomers

- InnovaPolymer

- Global Synthetic Rubbers

- OmniFlex Polymers

- Specialty Chemical Co.

- Modern Materials Ltd.

- Elite Polymer Corp.

- HydroCarbon Specialties

- Quantum Elastomers

- ChemPoly Solutions

- Universal Polymers Inc.

Frequently Asked Questions

Analyze common user questions about the Styrenic Block Copolymer market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current market size of Styrenic Block Copolymer (SBC)?

The global Styrenic Block Copolymer market is estimated at USD 8.9 billion in 2025.

What is the projected growth rate for the SBC market?

The SBC market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033.

Which industries are the primary drivers of SBC demand?

The automotive, construction, footwear, and adhesives & sealants industries are key drivers of SBC demand due to their need for flexible, durable, and high-performance materials.

What are the key types of Styrenic Block Copolymers?

The main types include Styrene-Butadiene-Styrene (SBS), Styrene-Isoprene-Styrene (SIS), and Styrene-Ethylene-Butylene-Styrene (SEBS), each offering distinct properties for various applications.

What are the major challenges facing the SBC market?

Key challenges include volatile raw material prices, intense market competition, stringent environmental regulations, and complexities in managing global supply chains.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted