Structured Cabling System Market

Structured Cabling System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708124 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Structured Cabling System Market Size

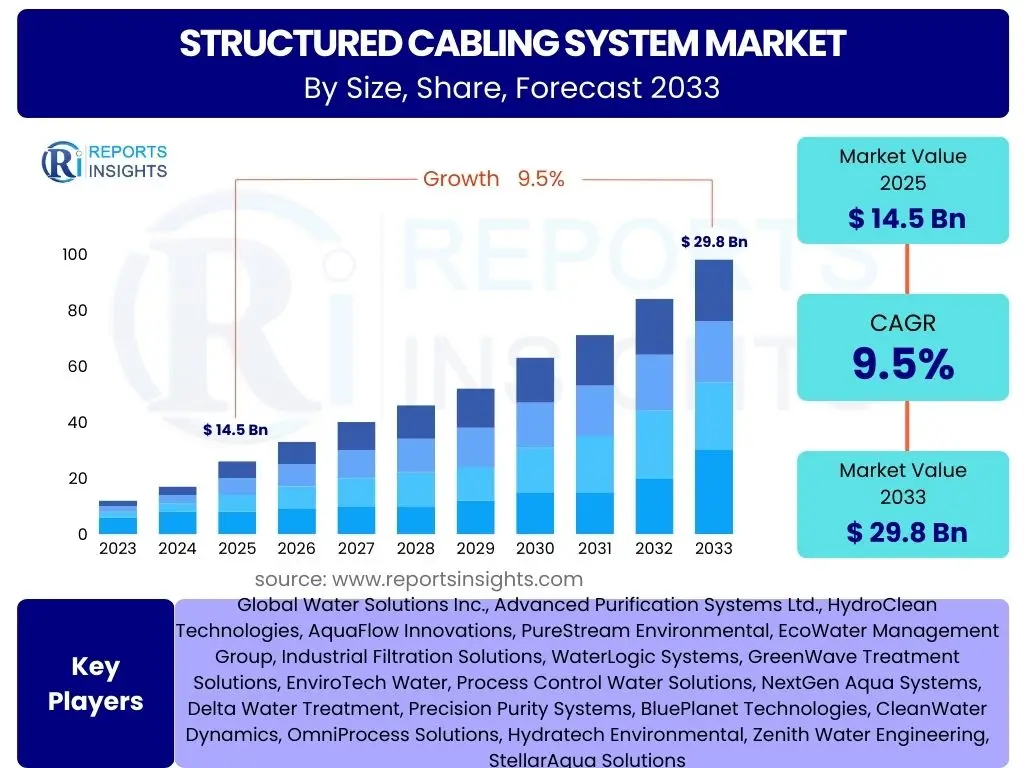

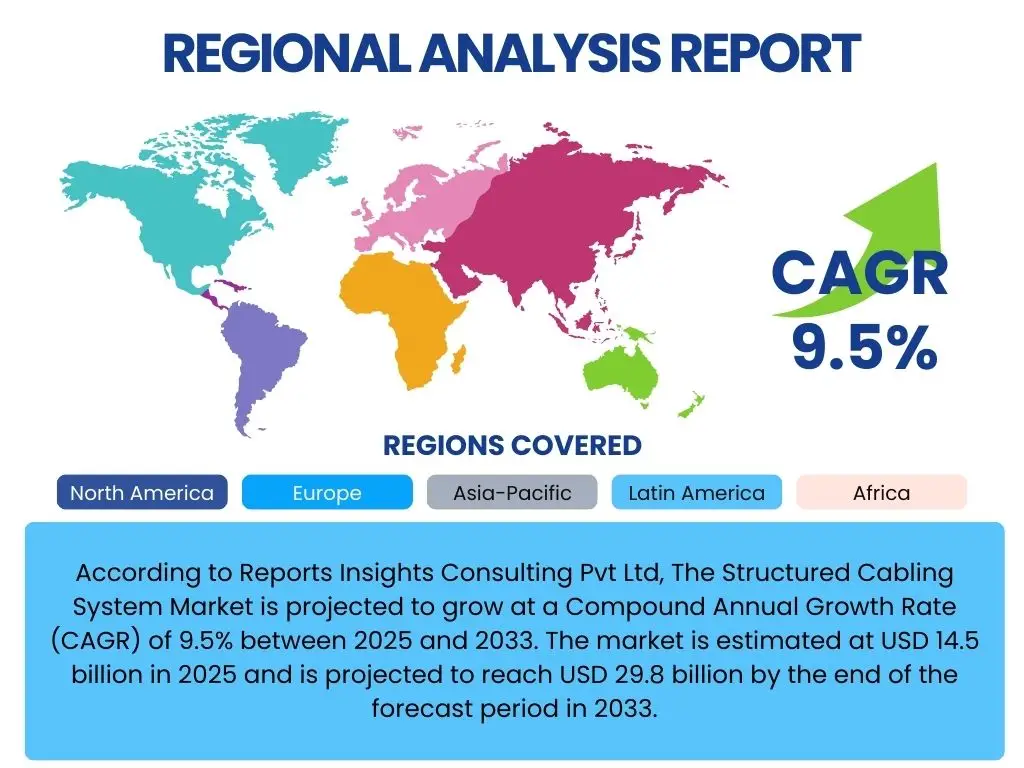

According to Reports Insights Consulting Pvt Ltd, The Structured Cabling System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 14.5 billion in 2025 and is projected to reach USD 29.8 billion by the end of the forecast period in 2033.

Key Structured Cabling System Market Trends & Insights

The Structured Cabling System market is currently experiencing significant shifts driven by the escalating demand for high-speed, reliable network infrastructure. Key trends revolve around the continuous evolution of Ethernet standards, the proliferation of data centers, and the pervasive adoption of IoT devices, all necessitating more robust and scalable cabling solutions. There is a growing emphasis on future-proofing installations, particularly with the transition to higher bandwidth requirements like 100GbE and beyond, pushing the adoption of Category 6A and fiber optic solutions.

Further insights indicate a strong movement towards integrated physical infrastructure management (IPIM) systems that offer better visibility, control, and efficiency for network administrators. Sustainability and energy efficiency are also emerging as crucial considerations, influencing the design and material choices in structured cabling. The global shift towards remote work and cloud computing has underscored the importance of resilient and high-performance network backbones, driving investments in upgrades and new installations across various sectors.

- Increased adoption of Category 6A and Category 8 cabling for enhanced bandwidth.

- Rising demand for fiber optic solutions in data centers and backbone networks.

- Integration of Power over Ethernet (PoE) technologies for powering IoT devices and smart building systems.

- Growth in intelligent infrastructure management (IIM) for automated network administration.

- Emphasis on modular and flexible cabling solutions to support evolving network requirements.

- Surge in hyperscale and edge data center deployments driving cabling infrastructure expansion.

- Development of sustainable and eco-friendly cabling materials and installation practices.

AI Impact Analysis on Structured Cabling System

Artificial intelligence is profoundly influencing the structured cabling system market by creating an imperative for more advanced, high-density, and low-latency network infrastructures. The computational demands of AI workloads, particularly in data centers and enterprise environments, necessitate robust cabling systems capable of handling massive data flows at unprecedented speeds. Users are keenly interested in how existing infrastructure can be optimized or upgraded to support AI-driven applications without incurring exorbitant costs, and how future cabling designs can inherently accommodate AI's evolving requirements.

Moreover, AI is not just a consumer of structured cabling but also a potential enabler. AI-powered analytics can optimize network performance, predict maintenance needs, and enhance the security of cabling infrastructure by monitoring anomalies. Concerns often revolve around the cooling requirements for high-density AI equipment, which directly impacts cable routing and thermal management within racks and data center aisles. Expectations are high for cabling solutions that offer improved thermal characteristics, greater flexibility for future upgrades, and seamless integration with intelligent building management systems that leverage AI for operational efficiency.

- Increased demand for higher bandwidth and lower latency cabling to support AI/ML workloads.

- Requirement for denser cabling solutions to accommodate high-performance AI hardware.

- Driving factor for adoption of fiber optics, particularly single-mode fiber, in AI-centric data centers.

- Enhanced focus on thermal management in cabling designs due to increased heat generation from AI servers.

- AI-driven network monitoring and predictive maintenance for cabling infrastructure.

- Integration of AI-powered smart building systems leveraging structured cabling for sensor and device connectivity.

- Potential for AI algorithms to optimize cable routing and network design for efficiency.

Key Takeaways Structured Cabling System Market Size & Forecast

The structured cabling system market is poised for robust growth, driven by the digital transformation across industries and the continuous evolution of network technologies. A primary takeaway is the non-negotiable need for high-performance and future-proof cabling solutions, as the reliance on data-intensive applications and IoT devices shows no signs of abatement. This sustained demand underlines significant investment opportunities for manufacturers and service providers in developing and deploying advanced cabling infrastructure.

Furthermore, the market's trajectory indicates a strong shift towards more intelligent, manageable, and sustainable cabling systems. End-users are increasingly prioritizing solutions that offer not only superior performance but also enhanced operational efficiency, reduced total cost of ownership, and environmental responsibility. The forecast highlights that regions undergoing rapid urbanization and technological adoption, particularly in Asia Pacific, will be key growth engines, while mature markets will focus on upgrades and specialized solutions for emerging technologies like 5G and edge computing.

- Significant market expansion driven by increased data consumption and network dependency.

- Strong emphasis on upgrading existing infrastructure to meet future bandwidth demands.

- Fiber optic cabling solutions are critical for backbone networks and data centers.

- Integration with smart technologies (IoT, AI) is a key growth catalyst.

- Sustainability and energy efficiency are becoming vital considerations in purchasing decisions.

- Emerging markets in Asia Pacific are expected to exhibit the highest growth rates.

- Opportunities exist in providing comprehensive, end-to-end cabling solutions and managed services.

Structured Cabling System Market Drivers Analysis

The Structured Cabling System market is propelled by a confluence of technological advancements and increasing demands for robust digital infrastructure. A significant driver is the widespread adoption of cloud computing and virtualization technologies, which necessitate high-speed, reliable data transmission capabilities within data centers and enterprise networks. This paradigm shift requires more sophisticated cabling solutions that can handle increased traffic density and ensure minimal latency, thereby fueling investments in advanced fiber optic and copper cabling systems.

Another crucial driver is the exponential growth of the Internet of Things (IoT) and the subsequent proliferation of connected devices across various sectors, including smart homes, smart cities, and industrial automation. These devices often rely on Power over Ethernet (PoE) for both data and power, demanding cabling infrastructure that can support higher power delivery while maintaining data integrity. The development of smart buildings and intelligent infrastructure further reinforces this trend, integrating diverse systems such as security, HVAC, and lighting onto a unified cabling backbone.

Furthermore, the continuous evolution of Ethernet standards, pushing towards 10GbE, 25GbE, 40GbE, and even 100GbE and beyond, directly mandates the deployment of higher-performance cabling. Organizations are under constant pressure to upgrade their networks to accommodate these faster speeds, driven by data-intensive applications, high-definition video streaming, and real-time communication. This relentless pursuit of speed and efficiency ensures a steady demand for new installations and significant upgrades of structured cabling systems globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Bandwidth Applications (e.g., 4K/8K video, AI, Big Data) | +2.1% | Global, particularly North America, Europe, Asia Pacific | Short- to Mid-term (2025-2030) |

| Proliferation of IoT Devices and Smart Building Technologies | +1.8% | Global, especially urban areas in developed and developing nations | Mid- to Long-term (2027-2033) |

| Expansion of Data Centers and Cloud Computing Infrastructure | +2.5% | Global, significant in APAC and North America | Short- to Long-term (2025-2033) |

| Growing Adoption of Power over Ethernet (PoE) | +1.5% | Global, prevalent in enterprise and commercial sectors | Short- to Mid-term (2025-2030) |

| Technological Advancements in Networking Standards (e.g., 5G, Wi-Fi 6/7) | +1.9% | Global, driving upgrades in telecommunications and enterprise | Mid-term (2026-2031) |

Structured Cabling System Market Restraints Analysis

Despite the robust growth drivers, the Structured Cabling System market faces several significant restraints that could impede its expansion. One prominent restraint is the high initial investment cost associated with deploying advanced structured cabling infrastructure, particularly fiber optic solutions. For small and medium-sized enterprises (SMEs) or organizations with tight budgets, the upfront capital expenditure for high-performance cabling, along with installation and associated equipment, can be prohibitive, leading them to defer upgrades or opt for less advanced, albeit cheaper, alternatives.

Another challenge stems from the increasing prevalence of wireless technologies, such as Wi-Fi 6/7 and 5G. While structured cabling remains indispensable for backbone networks and high-density environments, the advancements in wireless capabilities offer an alternative for certain last-mile connectivity and device access scenarios. This might lead some users to reduce the scope of new wired installations in favor of robust wireless networks, especially in environments where mobility and flexibility are prioritized over absolute wired speed for every endpoint.

Furthermore, the complexity of planning and installing sophisticated structured cabling systems, especially in older buildings or challenging architectural environments, poses a restraint. Integrating new systems with legacy infrastructure, adhering to stringent building codes, and managing the disruption during installation can be time-consuming and costly. This complexity often requires specialized expertise, which can be scarce, further exacerbating project timelines and budgets, and potentially deterring organizations from undertaking necessary upgrades.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Installation Costs | -1.5% | Global, particularly impacting SMEs and budget-constrained sectors | Short- to Mid-term (2025-2030) |

| Advancements in Wireless Technologies (e.g., Wi-Fi 6/7, 5G) | -1.2% | Global, mainly in enterprise and commercial sectors for endpoint connectivity | Short- to Long-term (2025-2033) |

| Complexity of Installation and Maintenance of Advanced Systems | -0.8% | Global, especially in regions with older infrastructure | Short- to Mid-term (2025-2030) |

| Shortage of Skilled Labor for Installation and Troubleshooting | -0.7% | North America, Europe, parts of Asia Pacific | Mid-term (2026-2031) |

| Legacy Infrastructure and Interoperability Challenges | -0.5% | Developed regions with extensive existing networks | Mid- to Long-term (2027-2033) |

Structured Cabling System Market Opportunities Analysis

The Structured Cabling System market presents numerous opportunities for growth, primarily stemming from the increasing global digitalization and the demand for more sophisticated networking solutions. One significant opportunity lies in the burgeoning smart cities and smart infrastructure projects worldwide. These initiatives integrate various technologies like intelligent transportation systems, smart grids, and public safety networks, all of which require extensive, reliable, and high-performance structured cabling backbones to connect a multitude of sensors, cameras, and communication devices.

Another key area of opportunity is the continuous expansion and upgrade cycles within the data center segment, including hyperscale, enterprise, and increasingly, edge data centers. As organizations migrate more operations to the cloud and embrace data-intensive applications like AI and big data analytics, the demand for ultra-high-density fiber optic cabling and high-speed copper solutions within these facilities is skyrocketing. This ongoing evolution ensures a steady stream of projects for both new constructions and significant retrofits.

Furthermore, the rising adoption of Power over Ethernet (PoE) technologies creates an important avenue for market expansion. With the proliferation of IoT devices, VoIP phones, wireless access points, LED lighting, and security cameras, PoE-capable structured cabling simplifies deployment by delivering both power and data over a single cable. This convenience and cost-efficiency drive its adoption across commercial, industrial, and even residential applications, offering providers an opportunity to deliver integrated and future-ready solutions that consolidate network and power infrastructure.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Smart City and Smart Building Infrastructure Development | +1.9% | Global, prominent in emerging economies and developed urban centers | Mid- to Long-term (2027-2033) |

| Expansion of Hyperscale and Edge Data Centers | +2.3% | North America, Asia Pacific, Europe | Short- to Long-term (2025-2033) |

| Growing Demand for Power over Ethernet (PoE) Applications | +1.7% | Global, across commercial, residential, and industrial sectors | Short- to Mid-term (2025-2030) |

| Upgrade and Modernization of Legacy Network Infrastructure | +1.4% | Developed regions (North America, Europe) | Short- to Mid-term (2025-2030) |

| Emergence of Industry 4.0 and Industrial IoT (IIoT) | +1.6% | Manufacturing hubs in Europe, Asia Pacific, North America | Mid-term (2026-2031) |

Structured Cabling System Market Challenges Impact Analysis

The Structured Cabling System market faces several inherent challenges that require innovative solutions and strategic planning. A significant challenge is the rapid pace of technological obsolescence, where new networking standards and higher bandwidth requirements emerge frequently. This constant evolution pressures organizations to continuously upgrade their cabling infrastructure, leading to increased costs and the potential for premature obsolescence of recently installed systems. Ensuring that new installations are future-proof for at least a decade becomes a complex design and investment decision.

Another critical challenge involves maintaining interoperability and standardization across diverse vendors and evolving technologies. As the market sees a variety of proprietary and open standards for different components—from connectors to cable types—ensuring seamless integration and optimal performance can be difficult. This complexity often leads to compatibility issues, extended troubleshooting times, and potential vendor lock-in, which complicates procurement and system management for end-users and installers alike.

Furthermore, the environmental impact and sustainability concerns associated with structured cabling pose a growing challenge. The manufacturing of cables and components, their installation, and eventual disposal contribute to resource consumption and waste. With increasing regulatory pressures and corporate social responsibility initiatives, there is a demand for more eco-friendly materials, energy-efficient designs, and robust recycling programs. Addressing these concerns while maintaining performance and cost-effectiveness requires significant innovation in material science and manufacturing processes within the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Need for Constant Upgrades | -1.3% | Global, particularly high-tech sectors | Short- to Long-term (2025-2033) |

| Ensuring Interoperability and Standardization Across Vendors | -0.9% | Global, across all market segments | Mid-term (2026-2031) |

| Environmental and Sustainability Concerns of Materials and Waste | -0.6% | Europe, North America, increasingly Asia Pacific | Mid- to Long-term (2027-2033) |

| Rising Copper Prices and Volatility in Raw Material Costs | -0.4% | Global, impacting cost of copper-based cabling solutions | Short-term (2025-2027) |

| Cybersecurity Threats on Network Infrastructure | -0.5% | Global, critical for all connected environments | Short- to Long-term (2025-2033) |

Structured Cabling System Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Structured Cabling System market, offering detailed insights into market dynamics, segmentation, regional landscapes, and competitive intelligence. The scope encompasses a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry's growth trajectory from 2025 to 2033. It also includes a detailed impact analysis of artificial intelligence on the market, providing a forward-looking perspective for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 billion |

| Market Forecast in 2033 | USD 29.8 billion |

| Growth Rate | 9.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CommScope, Panduit, Corning Inc., Belden Inc., Legrand, Nexans, R&M, The Siemon Company, D-Link Corporation, Schneider Electric, Leviton Manufacturing Co. Inc., Furukawa Electric Co. Ltd., TE Connectivity, Excel Networking Solutions, Paige Electric Co. LP, Sumitomo Electric Industries, Ltd., Hubbell Incorporated, Brand-Rex Ltd., Optical Cable Corporation, Prysmian Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Structured Cabling System market is meticulously segmented to provide a granular understanding of its diverse components, applications, and end-user landscapes. This segmentation allows for a detailed analysis of market dynamics within specific niches, highlighting growth opportunities and competitive strategies tailored to each segment. The component segment differentiates between various types of cables—copper and fiber optic, along with essential hardware such as connectors, patch panels, and cable management solutions, reflecting the technological backbone of network infrastructure.

The application segment categorizes the market based on where structured cabling systems are deployed, including data centers, commercial, residential, and industrial infrastructures. Each application area has unique demands regarding bandwidth, environmental conditions, and scalability, driving specific product preferences and installation practices. Data centers, for instance, demand ultra-high-density fiber solutions, while commercial buildings might prioritize a blend of copper for endpoint connectivity and fiber for backbone.

Furthermore, the end-user segment breaks down the market by the industries leveraging structured cabling, such as IT & Telecommunications, Government & Education, Healthcare, Manufacturing, Retail, and BFSI. This categorization reveals how different industry verticals adopt and utilize structured cabling systems based on their specific operational needs, regulatory compliance, and digital transformation initiatives. For example, healthcare facilities require reliable, low-latency networks for critical medical equipment and patient data, whereas the manufacturing sector focuses on supporting industrial IoT and automation.

- By Component:

- Cables: Copper (Category 5e, Category 6, Category 6A, Category 7, Category 7A, Category 8), Fiber Optic (Single-Mode, Multi-Mode)

- Connectors

- Patch Panels

- Wall Outlets

- Racks & Enclosures

- Cable Management Accessories

- By Application:

- Data Centers

- Commercial Infrastructure

- Residential Infrastructure

- Industrial Infrastructure

- By End-User:

- IT & Telecommunications

- Government & Education

- Healthcare

- Manufacturing

- Retail

- BFSI (Banking, Financial Services, and Insurance)

- Others

Regional Highlights

- North America: A mature market characterized by early adoption of advanced networking technologies, significant presence of hyperscale data centers, and continuous infrastructure upgrades in enterprise and government sectors.

- Europe: Driven by smart city initiatives, robust industrial automation, and stringent data protection regulations, fostering demand for secure and high-performance cabling solutions across various industries.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid urbanization, massive investments in digital infrastructure, increasing cloud adoption, and the expansion of IT and telecommunications sectors in countries like China, India, and Southeast Asia.

- Latin America: Emerging market with increasing internet penetration, growing data center investments, and demand for reliable connectivity in commercial and residential developments.

- Middle East & Africa (MEA): Experiencing substantial growth due to smart city projects (e.g., NEOM in Saudi Arabia), diversification from oil-based economies, and rising digital transformation efforts across governments and businesses.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Structured Cabling System Market.- CommScope

- Panduit

- Corning Inc.

- Belden Inc.

- Legrand

- Nexans

- R&M (Reichle & De-Massari AG)

- The Siemon Company

- D-Link Corporation

- Schneider Electric

- Leviton Manufacturing Co. Inc.

- Furukawa Electric Co. Ltd.

- TE Connectivity

- Excel Networking Solutions

- Paige Electric Co. LP

- Sumitomo Electric Industries, Ltd.

- Hubbell Incorporated

- Brand-Rex Ltd.

- Optical Cable Corporation

- Prysmian Group

Frequently Asked Questions

What is a Structured Cabling System?

A Structured Cabling System is a complete system of cabling and associated hardware that provides a comprehensive telecommunications infrastructure. This infrastructure typically serves a wide range of uses, such as providing telephone service or transmitting data through a computer network. It is the backbone for voice, data, and video communications within a building or campus, designed to be organized, scalable, and adaptable to future technological changes.

Why is structured cabling important for modern businesses?

Structured cabling is crucial for modern businesses because it provides a reliable, high-performance, and flexible foundation for all communication and data needs. It supports current high-bandwidth applications, simplifies network management and troubleshooting, and offers scalability for future growth and technological advancements like IoT and AI, ensuring business continuity and operational efficiency.

What are the primary types of cables used in structured cabling?

The primary types of cables used in structured cabling are copper cables and fiber optic cables. Copper cables, such as Category 6A or Category 8, are commonly used for horizontal runs to workstations and PoE applications. Fiber optic cables, available in single-mode and multi-mode variants, are preferred for backbone connections, data centers, and long-distance transmissions due to their higher bandwidth and immunity to electromagnetic interference.

How does structured cabling support Power over Ethernet (PoE)?

Structured cabling supports Power over Ethernet (PoE) by using standard Ethernet cables (typically Category 5e, 6, or 6A) to transmit both data and electrical power to networked devices. This eliminates the need for separate power outlets for devices like IP cameras, VoIP phones, and wireless access points, simplifying installation, reducing cabling clutter, and offering greater flexibility in device placement. Higher category cables are often recommended for higher-power PoE applications.

What are the future trends impacting the Structured Cabling System market?

Future trends impacting the Structured Cabling System market include the increasing demand for higher bandwidth driven by AI and Big Data, the widespread adoption of IoT and smart building technologies, and the expansion of hyperscale and edge data centers. There is also a growing focus on sustainable cabling solutions, enhanced physical infrastructure management, and the integration of cabling with evolving wireless standards like Wi-Fi 7 and 5G to create hybrid networks.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted