Structural Steel Market

Structural Steel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708554 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

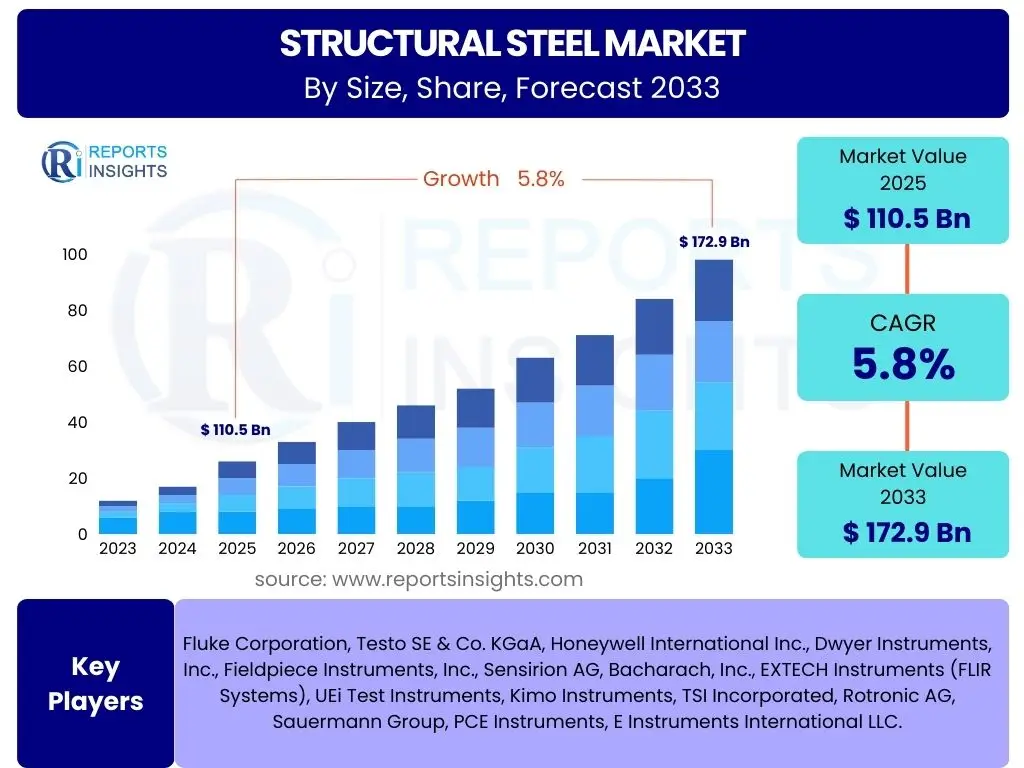

Structural Steel Market Size

According to Reports Insights Consulting Pvt Ltd, The Structural Steel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 110.5 Billion in 2025 and is projected to reach USD 172.9 Billion by the end of the forecast period in 2033.

Key Structural Steel Market Trends & Insights

The structural steel market is currently shaped by several transformative trends driven by evolving construction practices, environmental concerns, and technological advancements. Users frequently inquire about the shift towards sustainable construction methods, the impact of modular and prefabricated building techniques, and the increasing demand for high-strength, lightweight steel solutions. Furthermore, the role of digitalization in design and fabrication processes, alongside a growing focus on infrastructure development in emerging economies, represents significant areas of interest for market participants seeking to understand future growth trajectories and operational efficiencies within the sector. These trends collectively underscore a market moving towards greater efficiency, sustainability, and innovation.

- Sustainable and Green Building Initiatives: Increasing adoption of eco-friendly construction practices and materials.

- Modular and Prefabricated Construction: Growing preference for off-site fabrication to reduce construction time and costs.

- Digitalization and BIM (Building Information Modeling): Enhanced design accuracy, collaboration, and project management.

- High-Strength and Lightweight Steel Grades: Demand for materials offering improved performance and reduced material usage.

- Infrastructure Development: Significant investments in transportation, energy, and urban infrastructure globally.

- Urbanization and Population Growth: Driving new residential, commercial, and industrial construction projects.

- Advanced Welding and Fabrication Techniques: Improving structural integrity and efficiency.

AI Impact Analysis on Structural Steel

The integration of Artificial Intelligence (AI) is poised to revolutionize the structural steel industry, addressing common user questions related to efficiency, safety, and predictive capabilities. Users are keen to understand how AI can optimize design processes, enhance manufacturing precision, and improve supply chain logistics. The application of AI in predictive maintenance for steel structures and machinery is another key area of interest, promising reduced downtime and operational costs. Furthermore, inquiries often revolve around AI's role in ensuring quality control and safety on construction sites, indicating a clear expectation for technology to mitigate risks and improve project outcomes. These AI-driven advancements are expected to foster a more data-centric and automated approach throughout the structural steel value chain, from raw material sourcing to final assembly.

AI's influence extends to various stages of structural steel production and application. In the design phase, generative AI can rapidly explore countless structural configurations, optimizing for material use, strength, and cost, thereby significantly reducing design cycles. During manufacturing, AI-powered robotics and vision systems can enhance precision in cutting, bending, and welding, minimizing waste and improving quality. On the construction site, AI can analyze real-time data from sensors and drones to monitor progress, detect potential safety hazards, and optimize logistics for material delivery and crane operations. The ability of AI to process vast datasets for predictive analytics also means better forecasting of material demand, market trends, and even potential structural failures, enabling proactive interventions. This comprehensive impact underscores AI as a critical enabler for innovation and efficiency in the structural steel sector.

- Design Optimization: AI algorithms accelerate structural design, optimizing material use and performance.

- Predictive Maintenance: AI analyzes sensor data to forecast equipment failures and structural wear, reducing downtime.

- Supply Chain Management: AI enhances logistics, inventory management, and demand forecasting for raw materials and finished products.

- Manufacturing Automation: AI-powered robotics for precision cutting, welding, and fabrication.

- Quality Control: AI vision systems detect defects in steel components with higher accuracy and speed.

- Safety Monitoring: AI analyzes site data to identify potential hazards and ensure worker safety.

- Resource Efficiency: AI optimizes energy consumption in steel production and reduces material waste.

- Project Management: AI tools improve scheduling, risk assessment, and resource allocation for construction projects.

Key Takeaways Structural Steel Market Size & Forecast

The structural steel market is poised for robust growth over the forecast period, driven by a confluence of global development trends and technological advancements. Key insights indicate a consistent expansion fueled by escalating demand for infrastructure and building construction across both developed and emerging economies. Users frequently seek concise summaries of the market's trajectory, emphasizing the underlying factors contributing to its resilience and growth. The forecast highlights sustained investment in urban development, industrial expansion, and the adoption of modern construction techniques as primary catalysts. Furthermore, the market's evolving landscape suggests a strong emphasis on sustainable practices and innovative material solutions, which are becoming integral to long-term market viability.

A crucial takeaway from the market analysis is the increasing importance of regional economic dynamics, with Asia Pacific expected to remain a dominant force due to rapid industrialization and urbanization. The steady Compound Annual Growth Rate (CAGR) reflects a stable yet progressive industry adapting to new challenges and opportunities. Stakeholders should note the growing demand for specialized structural steel products tailored for specific applications, such as high-rise buildings and long-span bridges. The market is also characterized by a shift towards more efficient and environmentally friendly production processes, driven by stricter regulations and corporate sustainability goals. These factors collectively paint a picture of a dynamic market with considerable potential for innovation and expansion in the coming years.

- Significant Growth Projected: Market expected to reach USD 172.9 Billion by 2033 with a 5.8% CAGR.

- Infrastructure Development is Key: Government spending on infrastructure remains a primary growth driver.

- Urbanization Fuels Demand: Rapid growth in urban centers worldwide necessitates new construction.

- Technological Integration: Digitalization, automation, and AI are transforming industry practices.

- Sustainability Focus: Increasing demand for green building materials and sustainable construction methods.

- Asia Pacific Dominance: Region projected to hold the largest market share due to economic development.

- Evolving Product Landscape: Demand for high-strength and lightweight steel grades is on the rise.

Structural Steel Market Drivers Analysis

The structural steel market's expansion is fundamentally propelled by the sustained global impetus on infrastructure development. Governments worldwide are allocating substantial funds towards renovating existing infrastructure and constructing new transportation networks, urban utilities, and public buildings. This includes ambitious projects such as high-speed rail lines, extensive road networks, modern port facilities, and advanced energy infrastructure, all of which heavily rely on structural steel for their robust and durable construction. The inherent strength, durability, and versatility of structural steel make it an indispensable material for these large-scale endeavors, ensuring long-term stability and safety. This continuous investment serves as a foundational driver, creating a consistent demand across diverse regions.

Beyond public infrastructure, rapid urbanization and industrialization, particularly in emerging economies, are significant demand generators. As populations migrate to urban centers, there is an escalating need for new residential complexes, commercial spaces, and industrial facilities, all of which benefit from structural steel’s efficiency and speed of construction. The ability of structural steel to facilitate quicker project completion times and provide design flexibility makes it a preferred choice for developers keen on meeting the demands of burgeoning urban populations. Furthermore, the growth of the manufacturing sector, including automotive and machinery production, also contributes to demand, as structural steel is vital for factory buildings and equipment frameworks. These intertwined socio-economic and industrial forces collectively underpin the robust growth trajectory of the structural steel market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Infrastructure Development | +1.5% to +2.0% | Asia Pacific, North America, Europe | Medium-Long Term (2025-2033) |

| Rapid Urbanization and Industrialization | +1.2% to +1.8% | Asia Pacific, Latin America, MEA | Medium-Long Term (2025-2033) |

| Growth in Non-Residential Construction | +0.8% to +1.3% | Global | Medium Term (2025-2030) |

| Advancements in Construction Techniques | +0.5% to +1.0% | Developed Economies | Short-Medium Term (2025-2028) |

| Increasing Focus on Sustainable Building | +0.4% to +0.8% | Europe, North America | Medium-Long Term (2025-2033) |

Structural Steel Market Restraints Analysis

The structural steel market faces significant restraints primarily due to the inherent volatility and fluctuations in raw material prices. Iron ore, coking coal, and scrap steel are critical components in steel production, and their prices are subject to global supply-demand dynamics, geopolitical events, and currency exchange rates. Any sharp increase in these input costs directly impacts the production expenses for structural steel manufacturers, leading to higher selling prices. This can subsequently reduce project profitability for construction companies and other end-users, potentially causing delays or shifts towards more cost-effective, alternative materials. The unpredictability of these costs makes long-term project planning challenging and can erode profit margins across the value chain, thus impeding market growth.

Environmental regulations and the associated compliance costs also present a substantial restraint for the structural steel industry. Steel production is an energy-intensive process that historically has a significant carbon footprint. As global environmental consciousness grows and governments implement stricter emission standards, manufacturers are compelled to invest heavily in advanced pollution control technologies, energy-efficient processes, and sustainable practices. These investments, while necessary for long-term sustainability, add to operational costs, which can either be passed on to consumers, making steel less competitive, or absorb into profit margins. Furthermore, lengthy and complex approval processes for new steel manufacturing facilities or expansions, driven by environmental impact assessments, can slow down market response to demand fluctuations and hinder capacity growth, particularly in regions with stringent environmental policies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8% to -1.5% | Global | Short-Medium Term (2025-2028) |

| Stringent Environmental Regulations | -0.5% to -1.0% | Europe, North America, China | Medium-Long Term (2025-2033) |

| Competition from Alternative Materials | -0.3% to -0.7% | Global | Medium Term (2025-2030) |

| High Energy Consumption in Production | -0.2% to -0.5% | Global | Short-Medium Term (2025-2028) |

| Skilled Labor Shortages | -0.1% to -0.4% | Developed Economies | Long Term (2025-2033) |

Structural Steel Market Opportunities Analysis

The structural steel market is presented with significant opportunities, particularly from the burgeoning demand for green and sustainable construction practices. As environmental concerns escalate and regulatory frameworks push towards decarbonization, structural steel, with its high recyclability rate and potential for reduced embodied carbon through efficient production methods, is uniquely positioned to capitalize on this shift. Developers and architects are increasingly prioritizing materials with lower environmental impacts, and innovations in steel manufacturing, such as the use of electric arc furnaces (EAFs) and hydrogen-based steelmaking, offer pathways to produce "green steel." This trend provides manufacturers with an avenue to differentiate their products and gain market share by aligning with global sustainability goals, appealing to eco-conscious consumers and project stakeholders. The focus on life cycle assessments and circular economy principles further enhances steel's appeal as a sustainable building material, driving demand for innovative, environmentally responsible solutions.

Another major opportunity lies in the continued growth of modular and prefabricated construction techniques. These methods involve manufacturing structural components off-site in controlled factory environments, which are then transported and assembled at the construction site. Structural steel is ideally suited for prefabrication due to its strength, consistency, and ease of fabrication. This approach offers numerous benefits, including reduced construction time, lower labor costs, enhanced quality control, and minimized on-site waste. As the construction industry grapples with labor shortages and the need for faster project delivery, the adoption of modular construction is expanding rapidly across residential, commercial, and industrial sectors. This trend opens up new markets for structural steel suppliers who can provide customized, precision-engineered components, fostering innovation in design and manufacturing processes and creating a demand for standardized, high-quality steel sections compatible with modern construction methodologies. Furthermore, smart city initiatives and the development of disaster-resilient infrastructure also present substantial avenues for growth, requiring robust and adaptable materials like structural steel for long-term urban development and safety.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Green Building and Sustainable Construction | +0.9% to +1.4% | Europe, North America, Asia Pacific | Medium-Long Term (2025-2033) |

| Growth in Modular and Prefabricated Construction | +0.7% to +1.2% | Global | Medium Term (2025-2030) |

| Developing Economies and Emerging Markets | +0.6% to +1.1% | Asia Pacific, Latin America, MEA | Long Term (2025-2033) |

| Smart City and Disaster-Resilient Infrastructure | +0.5% to +0.9% | Global | Medium-Long Term (2025-2033) |

| Renovation and Retrofitting of Existing Structures | +0.3% to +0.6% | Developed Economies | Short-Medium Term (2025-2028) |

Structural Steel Market Challenges Impact Analysis

The structural steel market faces significant challenges, particularly concerning global supply chain disruptions. Geopolitical tensions, trade disputes, natural disasters, and pandemics can severely impact the availability and timely delivery of raw materials (like iron ore and coking coal), intermediate steel products, and finished structural components. These disruptions lead to increased lead times, higher logistics costs, and production delays, ultimately affecting project schedules and budgets for end-users. Manufacturers struggle to maintain consistent production levels and meet demand when faced with unpredictable supply flows, which can lead to price volatility and a loss of market confidence. The complexity of global supply networks means that even localized issues can have cascading effects across the entire value chain, posing a substantial hurdle to stable market growth and operational efficiency.

Another prominent challenge is the increasing competition from alternative building materials. While structural steel offers superior strength and ductility, materials such as reinforced concrete, timber, and composite materials are constantly evolving and gaining traction in specific applications. Advancements in concrete technology, including ultra-high-performance concrete, offer comparable structural integrity for certain projects, sometimes at a lower cost or with different aesthetic properties. Timber, especially engineered wood products like cross-laminated timber (CLT), is increasingly preferred for its sustainability credentials and lighter weight, particularly in mid-rise and even high-rise construction. This growing array of viable alternatives necessitates continuous innovation from the structural steel industry to maintain its competitive edge, requiring investment in research and development for new steel grades, fabrication techniques, and cost-effective solutions. Furthermore, meeting increasingly stringent building codes and evolving design standards adds complexity and cost to manufacturing and construction processes, demanding continuous adaptation and compliance from industry participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions | -0.6% to -1.2% | Global | Short-Medium Term (2025-2028) |

| Competition from Alternative Building Materials | -0.4% to -0.9% | Global | Medium-Long Term (2025-2033) |

| Evolving Building Codes and Design Standards | -0.3% to -0.7% | Developed Economies | Medium Term (2025-2030) |

| High Capital Investment for Modernization | -0.2% to -0.5% | Global | Long Term (2025-2033) |

| Cybersecurity Risks in Digitalized Operations | -0.1% to -0.3% | Global | Short-Medium Term (2025-2028) |

Structural Steel Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global structural steel market, covering historical performance, current trends, and future projections. The scope encompasses detailed segmentation by type, product, end-use industry, and application, offering a granular view of market dynamics. It further delves into regional market insights, competitive landscapes, and the impact of key market drivers, restraints, opportunities, and challenges. The report aims to furnish stakeholders with critical intelligence for strategic decision-making, investment planning, and understanding the evolving technological and regulatory environment influencing the structural steel sector from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 110.5 Billion |

| Market Forecast in 2033 | USD 172.9 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, Nippon Steel Corporation, POSCO, Baowu Steel Group, JFE Steel Corporation, Tata Steel, Hyundai Steel, ThyssenKrupp AG, Gerdau S.A., Nucor Corporation, Commercial Metals Company (CMC), EVRAZ plc, Severstal, Steel Dynamics Inc., SSAB, China Baowu Steel Group, US Steel Corporation, Sumitomo Metal Industries, Vallourec S.A., Bluescope Steel Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The structural steel market is broadly segmented to provide a detailed understanding of its diverse applications and product types, allowing for precise market analysis and strategic planning. These segmentations help in identifying niche markets, understanding consumer preferences, and evaluating the growth potential across various dimensions. The comprehensive categorization by type, product, end-use industry, and application highlights the versatility of structural steel and its critical role in numerous sectors. This granular approach ensures that the market dynamics are thoroughly explored, from the raw material composition to the final structural use in a wide array of construction and industrial projects.

Each segment contributes uniquely to the overall market landscape. For instance, the "By Type" segment differentiates between heavy and light structural steel, catering to projects requiring different load-bearing capacities and aesthetic considerations. The "By Product" segment delineates specific forms such as beams, columns, and plates, which are foundational components in any steel structure. The "By End-Use Industry" segmentation clearly illustrates the market's reliance on sectors like building and construction, infrastructure, and energy, demonstrating where the majority of demand originates. Finally, the "By Application" segment further refines this view by detailing how structural steel is specifically utilized, whether for framing, reinforcement, or support structures, thereby offering a holistic perspective on its functional deployment within the global economy.

- By Type:

- Heavy Structural Steel

- Light Structural Steel

- By Product:

- Beams (I-Beam, H-Beam, W-Beam)

- Columns (Hollow Structural Sections - HSS)

- Plates (Flat, Checker)

- Rebars (Deformed, Plain)

- Angles

- Channels

- Other Profiles

- By End-Use Industry:

- Building & Construction

- Residential

- Commercial

- Industrial

- Infrastructure

- Bridges

- Roads & Railways

- Airports & Ports

- Energy

- Oil & Gas

- Power Generation

- Renewables

- Automotive

- Manufacturing & Industrial

- Other Industries

- Building & Construction

- By Application:

- Framing

- Reinforcement

- Support Structures

- Trusses

- Pre-Engineered Metal Buildings (PEMB)

Regional Highlights

- Asia Pacific: Expected to dominate the market share due to rapid urbanization, industrial growth, and significant government investments in infrastructure development, particularly in countries like China, India, and Southeast Asian nations. The region's expanding manufacturing sector and high population density continue to drive demand for both residential and commercial construction.

- North America: Driven by substantial infrastructure renewal projects, increasing demand for sustainable building solutions, and technological advancements in construction. The region benefits from a robust economy and a focus on replacing aging infrastructure, alongside growth in industrial and commercial construction.

- Europe: Characterized by a strong emphasis on green building standards, renovation of existing structures, and the adoption of prefabricated construction techniques. Strict environmental regulations are also pushing for the use of more sustainable and recycled steel, fostering innovation in the sector.

- Latin America: Emerging as a growth hub with increasing investments in infrastructure and construction projects, particularly in Brazil, Mexico, and Argentina. Economic development and urbanization initiatives are contributing to a steady rise in demand for structural steel.

- Middle East and Africa (MEA): Witnessing significant growth propelled by oil and gas infrastructure development, diversification projects away from oil dependency, and large-scale urban development plans, especially in the GCC countries and parts of Africa. Investments in tourism and commercial infrastructure are also key drivers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Structural Steel Market.- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- Baowu Steel Group

- JFE Steel Corporation

- Tata Steel

- Hyundai Steel

- ThyssenKrupp AG

- Gerdau S.A.

- Nucor Corporation

- Commercial Metals Company (CMC)

- EVRAZ plc

- Severstal

- Steel Dynamics Inc.

- SSAB

- US Steel Corporation

- Sumitomo Metal Industries

- Vallourec S.A.

- Bluescope Steel Limited

Frequently Asked Questions

Analyze common user questions about the Structural Steel market and generate a concise list of summarized FAQsreflecting key topics and concerns.What is structural steel and what are its primary uses?

Structural steel is a category of steel specifically designed for use in construction. It is produced with a precise chemical composition and mechanical properties to meet specific strength, ductility, and durability requirements. Its primary uses include constructing frameworks for buildings, bridges, infrastructure, industrial facilities, and various support structures due to its high strength-to-weight ratio and recyclability.

What factors are driving the growth of the structural steel market?

The structural steel market's growth is primarily driven by global infrastructure development, rapid urbanization, and industrialization, particularly in emerging economies. Increasing investments in residential and commercial building construction, coupled with the adoption of sustainable and modular construction techniques, also significantly contribute to market expansion.

What are the key challenges facing the structural steel industry?

The structural steel industry faces challenges such as volatility in raw material prices, stringent environmental regulations increasing production costs, intense competition from alternative building materials like concrete and timber, and global supply chain disruptions. Additionally, the industry must contend with high energy consumption during production and the need for significant capital investment in modernization.

How is sustainability impacting the structural steel market?

Sustainability is profoundly impacting the structural steel market by driving demand for eco-friendly construction practices and materials. Structural steel is highly recyclable, and advancements in "green steel" production (e.g., using electric arc furnaces or hydrogen) are making it a more environmentally appealing choice. This focus on sustainability is fostering innovation and new market opportunities for steel manufacturers.

Which region holds the largest share in the structural steel market, and why?

The Asia Pacific region currently holds the largest share in the structural steel market. This dominance is attributed to rapid urbanization, robust industrial growth, and extensive government spending on infrastructure development in key countries like China, India, and Southeast Asian nations. The region's booming construction sector and manufacturing base fuel high demand for structural steel.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted