Sterilization Service Market

Sterilization Service Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707201 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Sterilization Service Market Size

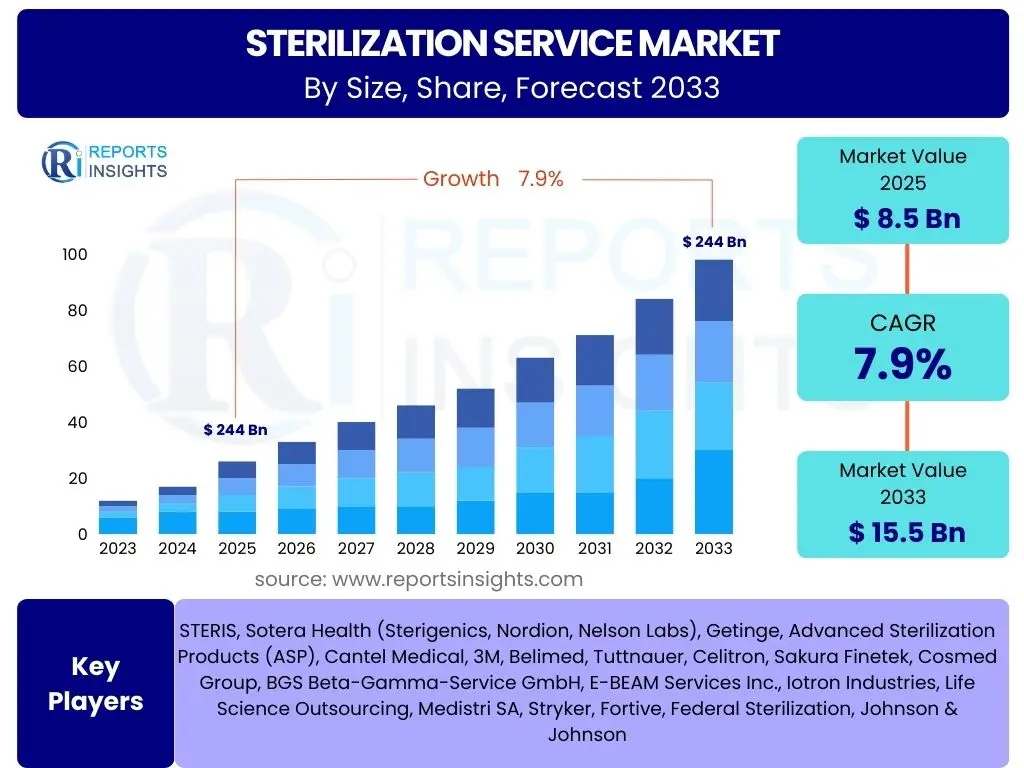

According to Reports Insights Consulting Pvt Ltd, The Sterilization Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.9% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 15.5 Billion by the end of the forecast period in 2033.

Key Sterilization Service Market Trends & Insights

The sterilization service market is experiencing dynamic shifts driven by evolving healthcare demands, technological advancements, and stringent regulatory frameworks. A prominent trend involves the increasing adoption of contract sterilization services by medical device manufacturers and pharmaceutical companies seeking to optimize operational efficiencies and ensure compliance without significant capital expenditure. This outsourcing trend is further fueled by the complexity of modern sterilization methods, which often require specialized equipment, expertise, and adherence to global standards.

Another significant insight points to the growing preference for advanced, low-temperature sterilization technologies, such as ethylene oxide (ETO), vaporized hydrogen peroxide (VHP), and e-beam irradiation. These methods are crucial for sterilizing heat-sensitive medical devices, which are becoming more prevalent with innovations in minimally invasive surgery and implantable devices. Furthermore, the market is witnessing a strong emphasis on sustainability, prompting the development and adoption of environmentally friendlier sterilization processes that minimize chemical waste and energy consumption, aligning with broader corporate social responsibility initiatives across the healthcare sector.

- Increasing outsourcing of sterilization services by healthcare and life science sectors.

- Growing demand for advanced, low-temperature sterilization methods for heat-sensitive devices.

- Rising focus on environmentally sustainable and green sterilization technologies.

- Expansion of medical device manufacturing and pharmaceutical production globally.

- Enhanced regulatory scrutiny and evolving compliance standards driving process improvements.

- Integration of digitalization and automation in sterilization processes for efficiency and traceability.

AI Impact Analysis on Sterilization Service

User queries regarding the impact of Artificial Intelligence (AI) on sterilization services frequently revolve around its potential to enhance efficiency, accuracy, and compliance, while also raising concerns about data privacy and implementation costs. AI's transformative potential lies in its capacity to optimize complex operational workflows, from predictive maintenance of sterilization equipment to real-time monitoring of critical process parameters. By analyzing vast datasets, AI algorithms can identify subtle deviations that might indicate potential failures or inefficiencies, thereby reducing downtime, improving sterilization cycle efficacy, and ensuring consistent sterility assurance levels.

Furthermore, AI can significantly contribute to quality control and regulatory adherence within the sterilization domain. Its application can streamline documentation, automate compliance checks, and provide robust traceability for sterilized products, addressing critical pain points for manufacturers and healthcare providers. While the initial investment in AI infrastructure and integration can be substantial, the long-term benefits in terms of cost reduction through optimized energy usage, reduced reprocessing rates, and minimized human error are compelling. The market anticipates AI playing a pivotal role in creating more resilient, transparent, and ultimately safer sterilization processes.

- AI optimizes sterilization cycles, reducing processing time and resource consumption.

- Predictive analytics powered by AI enhances equipment maintenance, minimizing downtime.

- AI improves quality control by detecting anomalies in sterilization parameters and product integrity.

- Enhanced traceability and automated compliance reporting through AI-driven data management.

- Increased operational efficiency and reduced human error in complex sterilization workflows.

- Potential for personalized sterilization protocols based on device type and material, guided by AI.

Key Takeaways Sterilization Service Market Size & Forecast

Analysis of user questions regarding the sterilization service market size and forecast consistently points to a strong growth trajectory, underpinned by fundamental drivers such as global healthcare expansion and escalating infection control imperatives. The significant projected growth from USD 8.5 Billion in 2025 to USD 15.5 Billion by 2033, at a CAGR of 7.9%, reflects a sustained increase in demand for outsourced sterilization solutions. This growth is not merely volumetric but also qualitative, driven by the need for specialized expertise, advanced technologies, and stringent regulatory compliance that in-house capabilities often struggle to match cost-effectively.

A crucial takeaway is the pervasive influence of regulatory bodies and international standards on market dynamics. Compliance with evolving guidelines, such as those from the FDA, EMA, and ISO, necessitates continuous investment in technology and quality systems, which often favors specialized sterilization service providers. The forecast also highlights regional disparities in growth, with emerging economies in Asia Pacific and Latin America poised for accelerated expansion due to improving healthcare infrastructures and rising medical tourism. The market's future will be characterized by a balance between technological innovation in sterilization methods and the ongoing imperative for cost-efficient, compliant, and sustainable services.

- Sterilization service market poised for robust growth, driven by increasing healthcare expenditure and surgical volumes.

- Outsourcing trend is a primary catalyst, offering cost efficiencies and access to specialized technologies.

- Regulatory stringency globally necessitates expertise and advanced facilities, benefiting service providers.

- Low-temperature sterilization methods will see increased adoption due to sensitive medical devices.

- Emerging markets offer significant growth opportunities, particularly in Asia Pacific and Latin America.

- Sustainability initiatives are shaping future sterilization practices and technology investments.

Sterilization Service Market Drivers Analysis

The Sterilization Service Market is primarily driven by the escalating demand for advanced healthcare, particularly the increasing number of surgical procedures globally, which directly translates to a greater need for sterilized medical instruments and devices. Concurrently, the rigorous and continuously evolving regulatory landscape, particularly from bodies such as the FDA, EMA, and various national health authorities, mandates strict adherence to sterilization standards. This regulatory pressure compels medical device manufacturers and healthcare facilities to either invest heavily in in-house sterilization capabilities or, more commonly, outsource to specialized service providers who possess the necessary expertise, infrastructure, and certifications.

Furthermore, the global rise in chronic diseases and the aging population are contributing to a higher volume of medical device production and usage, including complex, heat-sensitive instruments that require specialized low-temperature sterilization methods. The inherent complexities and high capital investment associated with establishing and maintaining state-of-the-art sterilization facilities make outsourcing an increasingly attractive and economically viable option for many organizations. This allows companies to focus on their core competencies while ensuring their products meet the highest safety and sterility standards before reaching patients.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Surgical Procedures Globally | +1.8% | Global, North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Stringent Regulatory Landscape for Sterility Assurance | +1.5% | Global, Developed Economies | Mid-term (2028-2031) |

| Growth in Medical Device and Pharmaceutical Manufacturing | +1.3% | Global, Asia Pacific, North America | Long-term (2025-2033) |

| Rising Incidence of Hospital-Acquired Infections (HAIs) | +1.2% | Global, Healthcare Facilities | Short-term (2025-2028) |

| Preference for Outsourced Sterilization Services | +1.0% | Global, Emerging Markets | Mid-term (2028-2031) |

Sterilization Service Market Restraints Analysis

Despite its robust growth potential, the sterilization service market faces several significant restraints that could impede its expansion. One primary concern revolves around the environmental impact and occupational health risks associated with certain widely used sterilization methods, particularly ethylene oxide (ETO). Regulatory bodies are increasingly scrutinizing ETO emissions, leading to tighter environmental controls and potentially higher operational costs for facilities that rely heavily on this method. This could force a shift towards alternative, more environmentally friendly, but potentially less versatile or cost-effective sterilization technologies.

Another major restraint is the high capital investment required for establishing and maintaining state-of-the-art sterilization facilities, especially those employing advanced technologies like E-beam or gamma irradiation. This high barrier to entry limits the number of new market participants and can constrain expansion plans for existing players, particularly in regions with less developed infrastructure or limited access to funding. Additionally, the complexity of validating new sterilization processes and the time-consuming nature of regulatory approvals can delay the adoption of innovative solutions, thereby slowing market evolution. Supply chain disruptions, as experienced recently, also pose a threat, impacting the availability of critical gases or equipment parts necessary for continuous operation, leading to potential service backlogs and increased lead times for sterilized products.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns and Regulations on Sterilants (e.g., ETO) | -1.5% | Global, North America, Europe | Mid-term (2028-2031) |

| High Capital Investment and Operating Costs | -1.2% | Global, Developing Economies | Long-term (2025-2033) |

| Strict Regulatory Compliance and Validation Challenges | -1.0% | Global | Mid-term (2028-2031) |

| Logistical Complexities and Supply Chain Vulnerabilities | -0.8% | Global, Remote Regions | Short-term (2025-2028) |

| Limited Shelf-Life of Some Sterilized Products | -0.7% | Specific Product Categories | Long-term (2025-2033) |

Sterilization Service Market Opportunities Analysis

The sterilization service market is poised for significant opportunities driven by the increasing complexity and miniaturization of medical devices, many of which are heat-sensitive and require specialized low-temperature sterilization techniques. This trend opens avenues for service providers to innovate and expand their offerings in methods like vaporized hydrogen peroxide (VHP), ozone, and advanced E-beam processes. As manufacturers continue to develop intricate devices, the demand for tailored, validated sterilization solutions that preserve device integrity while ensuring sterility will intensify, creating a niche for highly specialized contract sterilizers.

Furthermore, the burgeoning healthcare infrastructure in emerging economies, coupled with rising healthcare expenditure and a growing middle class, presents substantial market expansion opportunities. Countries in Asia Pacific, Latin America, and the Middle East are experiencing a surge in hospital construction and medical device manufacturing, often lacking the established in-house sterilization capabilities found in developed regions. This creates an immediate need for external sterilization services, enabling global players to establish new facilities or forge strategic partnerships. The increasing adoption of single-use medical devices and the reprocessing of reusable devices also offer dual-pronged opportunities, with distinct sterilization needs for each category, fueling diverse service demands.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Heat-Sensitive Medical Devices | +1.6% | Global, Developed Economies | Long-term (2025-2033) |

| Expansion into Emerging Markets with Growing Healthcare Infrastructure | +1.4% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Technological Advancements in Sterilization Methods (e.g., Plasma, Ozone) | +1.3% | Global | Mid-term (2028-2031) |

| Increasing Reprocessing of Reusable Medical Devices | +1.1% | North America, Europe | Short-term (2025-2028) |

| Integration of Automation and Digitalization in Sterilization Facilities | +0.9% | Global, Tech-Forward Companies | Mid-term (2028-2031) |

Sterilization Service Market Challenges Impact Analysis

The sterilization service market faces several critical challenges that demand robust strategic responses from service providers. One prominent challenge is navigating the increasingly complex and fragmented global regulatory landscape. Each region and often each country has its own specific set of sterilization standards, testing requirements, and environmental regulations, making it difficult for service providers to maintain universal compliance. This necessitates significant investment in regulatory intelligence, quality management systems, and personnel training, which can be particularly burdensome for smaller or new entrants to the market.

Another significant hurdle is managing the public perception and environmental concerns associated with certain sterilization chemicals, particularly ethylene oxide. Despite its efficacy, ongoing debates and potential new restrictions on ETO emissions could necessitate costly transitions to alternative methods or require substantial investments in emission control technologies. Furthermore, ensuring consistent sterility assurance levels across diverse product types and materials, especially with the proliferation of highly intricate and sensitive medical devices, presents a continuous technical challenge. Maintaining the delicate balance between effective sterilization and preserving product integrity requires advanced scientific understanding and rigorous validation processes, adding layers of complexity and cost to operations. Finally, talent acquisition and retention of skilled personnel, including microbiologists and validation engineers, remain a persistent operational challenge, as specialized expertise is crucial for high-quality sterilization services.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Evolving Regulatory Compliance | -1.4% | Global | Long-term (2025-2033) |

| Environmental and Safety Concerns of Sterilant Chemicals | -1.3% | Global, Developed Economies | Mid-term (2028-2031) |

| Ensuring Sterility of Highly Complex and Sensitive Devices | -1.1% | Global, Medical Device Sector | Long-term (2025-2033) |

| High Operating Costs and Energy Consumption | -0.9% | Global | Mid-term (2028-2031) |

| Skilled Labor Shortages and Training Requirements | -0.8% | Global, Specialized Roles | Short-term (2025-2028) |

Sterilization Service Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global sterilization service market, offering detailed insights into its size, growth trends, key drivers, restraints, opportunities, and challenges. The scope encompasses a thorough examination of various sterilization methods, applications, and end-use sectors, alongside a meticulous regional analysis to identify key growth pockets and emerging market dynamics. The report also integrates the impact of technological advancements, particularly AI, and regulatory changes, presenting a holistic view for stakeholders seeking strategic market intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 15.5 Billion |

| Growth Rate | 7.9% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | STERIS, Sotera Health (Sterigenics, Nordion, Nelson Labs), Getinge, Advanced Sterilization Products (ASP), Cantel Medical, 3M, Belimed, Tuttnauer, Celitron, Sakura Finetek, Cosmed Group, BGS Beta-Gamma-Service GmbH, E-BEAM Services Inc., Iotron Industries, Life Science Outsourcing, Medistri SA, Stryker, Fortive, Federal Sterilization, Johnson & Johnson |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The sterilization service market is comprehensively segmented by method, application, and end-use, reflecting the diverse requirements across industries and specific product types. Each segment exhibits unique growth drivers and technological preferences, contributing to the overall market dynamics. Understanding these segmentations is crucial for identifying key growth areas and tailoring service offerings to meet specific client needs, from the large-scale sterilization of medical instruments to the intricate processing of sensitive pharmaceutical components.

The method segment, encompassing technologies like Ethylene Oxide (ETO), gamma irradiation, and low-temperature plasma, illustrates the technological evolution in sterilization, driven by material compatibility and regulatory shifts. Application-based segmentation highlights the dominant role of medical devices and pharmaceuticals, though emerging sectors like food and beverage, and cosmetics, are increasingly adopting professional sterilization services for enhanced product safety and shelf-life. The end-use perspective further differentiates demand patterns between hospitals seeking on-site or outsourced solutions, and medical device manufacturers prioritizing specialized contract sterilization for large volumes and regulatory compliance.

- By Method

- Ethylene Oxide (ETO): Widely used for heat-sensitive and moisture-sensitive devices.

- Gamma Irradiation: Effective for a broad range of products, high penetration.

- E-beam Sterilization: Fast, environmentally friendly, and suitable for high-volume products.

- Steam Sterilization (Autoclave): Traditional, cost-effective for heat-stable devices.

- Dry Heat Sterilization: For heat-stable, moisture-sensitive items.

- Low-Temperature Hydrogen Peroxide Gas Plasma: Ideal for delicate, heat-sensitive instruments.

- Ozone Sterilization: Emerging method, environmentally friendly.

- Filtration Sterilization: Primarily for liquids and gases, not for solid devices.

- Vaporized Hydrogen Peroxide (VHP) Sterilization: Suitable for sensitive equipment and isolators.

- Other Methods (e.g., X-ray, Nitrogen Dioxide): Niche or experimental applications.

- By Application

- Medical Devices: Dominate the market due to stringent regulations and high volume.

- Pharmaceuticals: Essential for drug safety and compliance.

- Food & Beverage: For extending shelf-life and ensuring food safety.

- Healthcare Facilities (Hospitals, Clinics, Ambulatory Surgical Centers): For reusable instrument reprocessing.

- Academic & Research Institutions: For laboratory equipment and materials.

- Cosmetics & Personal Care: For product safety and preservation.

- Industrial Applications: Various specialized industrial processes.

- By End-Use

- Hospitals: Utilize services for surgical instruments and medical waste.

- Medical Device Companies: Outsource for pre-market and post-market sterilization.

- Pharmaceutical Companies: For drug products, APIs, and packaging.

- Contract Manufacturing Organizations (CMOs): Partner with sterilization service providers.

- Research & Development (R&D) Centers: For sterile research environments and tools.

- Food Processing Units: For packaging and product safety.

- Others: Includes veterinary clinics, dental offices, and specialized industrial facilities.

Regional Highlights

- North America: Dominates the sterilization service market due to a highly developed healthcare infrastructure, stringent regulatory frameworks from agencies like the FDA, and a high volume of medical device manufacturing. The region benefits from significant investments in advanced sterilization technologies and a strong emphasis on infection control. Outsourcing of sterilization services is a well-established practice, driven by cost-efficiency and the need for specialized expertise to navigate complex compliance requirements.

- Europe: Represents a mature market characterized by strict quality standards, a robust pharmaceutical industry, and increasing awareness of hospital-acquired infections. Countries like Germany, France, and the UK are key contributors, investing in both traditional and advanced sterilization methods. The region is also at the forefront of adopting sustainable sterilization practices, influenced by environmental regulations and corporate social responsibility initiatives.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate during the forecast period, driven by rapidly expanding healthcare expenditure, increasing medical tourism, and a burgeoning medical device and pharmaceutical manufacturing sector, particularly in China, India, and Japan. The region's large patient pool and improving access to healthcare services are fueling demand for sterile products, leading to significant opportunities for both domestic and international sterilization service providers.

- Latin America: Showing steady growth, primarily influenced by improving economic conditions, government investments in healthcare infrastructure, and rising chronic disease prevalence. Brazil and Mexico are key markets, adopting modern sterilization techniques to enhance patient safety and meet evolving international standards. The region presents opportunities for technology transfer and localized service expansion.

- Middle East and Africa (MEA): Emerging as a market with considerable untapped potential, particularly in the GCC countries due to significant healthcare infrastructure projects and a growing medical tourism industry. Increased awareness regarding infection control and government initiatives to improve healthcare quality are driving the adoption of professional sterilization services, though market penetration remains lower compared to developed regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Sterilization Service Market.- STERIS

- Sotera Health (Sterigenics, Nordion, Nelson Labs)

- Getinge

- Advanced Sterilization Products (ASP)

- Cantel Medical

- 3M

- Belimed

- Tuttnauer

- Celitron

- Sakura Finetek

- Cosmed Group

- BGS Beta-Gamma-Service GmbH

- E-BEAM Services Inc.

- Iotron Industries

- Life Science Outsourcing

- Medistri SA

- Stryker

- Fortive

- Federal Sterilization

- Johnson & Johnson

Frequently Asked Questions

Analyze common user questions about the Sterilization Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the primary growth driver for the Sterilization Service Market?

The primary growth driver for the sterilization service market is the global increase in the number of surgical procedures and the escalating demand for sterilized medical devices. As healthcare access expands and innovative medical technologies become more prevalent, the volume of instruments and devices requiring stringent sterilization processes has surged. This, coupled with the rising incidence of hospital-acquired infections (HAIs), necessitates robust and reliable sterilization solutions to ensure patient safety and adherence to public health standards.

Furthermore, the increasingly complex and stringent regulatory landscape, particularly from bodies like the FDA and ISO, compels medical device manufacturers and healthcare facilities to prioritize comprehensive sterilization. Many organizations find outsourcing to specialized service providers to be a cost-effective and compliant solution, as these providers possess the necessary expertise, advanced equipment, and validated processes to meet rigorous global standards. This trend of outsourcing further amplifies market growth, allowing core businesses to focus on innovation and patient care while ensuring sterility assurance.

Which sterilization method is currently the most widely used, and why?

Ethylene Oxide (ETO) sterilization is currently one of the most widely used methods in the sterilization service market, particularly for heat-sensitive and moisture-sensitive medical devices, which constitute a significant portion of modern medical instrumentation. Its broad material compatibility and high penetrability make it highly effective for sterilizing complex devices, including those with intricate lumens, plastics, and electronics that cannot withstand high temperatures or steam. This versatility ensures the integrity and functionality of delicate medical products while achieving a high sterility assurance level.

While ETO remains dominant for certain applications, the market is also seeing increasing adoption of alternatives like gamma irradiation and E-beam sterilization for high-volume products, due to their efficiency and environmental profiles. Steam sterilization, or autoclaving, continues to be a standard for heat-stable devices in healthcare settings due to its cost-effectiveness and rapid cycle times. The choice of method largely depends on the device material, design, and regulatory requirements, driving a diversified portfolio of services within the market.

How do regulatory changes impact the sterilization service industry?

Regulatory changes profoundly impact the sterilization service industry by dictating the standards, processes, and technologies that must be employed to ensure product sterility and patient safety. Agencies such as the U.S. FDA, European Medicines Agency (EMA), and various international organizations like ISO continually update guidelines for sterilization validation, monitoring, and quality management systems. These updates often lead to more stringent requirements, compelling service providers to invest in advanced equipment, implement more rigorous testing protocols, and enhance their documentation and traceability capabilities.

For instance, increased scrutiny on specific sterilant emissions, such as ethylene oxide, has driven investments in environmental controls and exploration of alternative sterilization methods. Compliance with these evolving regulations is not optional; it is fundamental to market access and maintaining operational licenses. This constant need for adaptation and investment often favors larger, more resourceful service providers who can absorb the costs and expertise required, thereby contributing to market consolidation and specialization.

What are the key opportunities for growth in emerging markets?

Key opportunities for growth in emerging markets, particularly within the Asia Pacific, Latin America, and Middle East & Africa regions, stem from their rapidly expanding healthcare infrastructures and increasing healthcare expenditure. Many of these economies are witnessing a significant rise in hospital construction, medical device manufacturing, and pharmaceutical production, often without a corresponding development of in-house, state-of-the-art sterilization capabilities. This creates a substantial demand for outsourced sterilization services, as local manufacturers and healthcare providers seek to meet international quality and safety standards.

Furthermore, these regions are experiencing a growing middle class and increasing health awareness, leading to higher utilization of medical services and a greater demand for sterile medical products. International sterilization service providers can leverage this by establishing new facilities, forming strategic partnerships with local entities, and offering cost-effective, high-quality sterilization solutions tailored to regional needs. The lower operating costs in some emerging markets can also make them attractive hubs for global sterilization operations, supporting overall market expansion.

How is AI transforming the efficiency and accuracy of sterilization processes?

Artificial Intelligence (AI) is transforming the efficiency and accuracy of sterilization processes by enabling advanced automation, predictive analytics, and enhanced quality control. AI algorithms can analyze vast amounts of data from sterilization cycles, including temperature, pressure, and humidity, to identify optimal parameters and detect anomalies in real-time. This capability leads to more precise process control, reduced cycle times, and minimization of resource consumption, thereby significantly improving operational efficiency and reducing costs associated with reprocessing or product damage.

In terms of accuracy, AI-driven systems can monitor equipment performance and predict potential maintenance needs before failures occur, ensuring continuous and reliable operation. Furthermore, AI contributes to robust quality assurance by automating compliance checks, generating detailed audit trails, and identifying deviations from established sterility assurance levels. This data-driven approach not only enhances the consistency and reliability of sterilization but also provides comprehensive traceability, which is crucial for regulatory adherence and overall product safety within the healthcare and life sciences sectors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted