Stem Cell Manufacturing Market

Stem Cell Manufacturing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708394 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

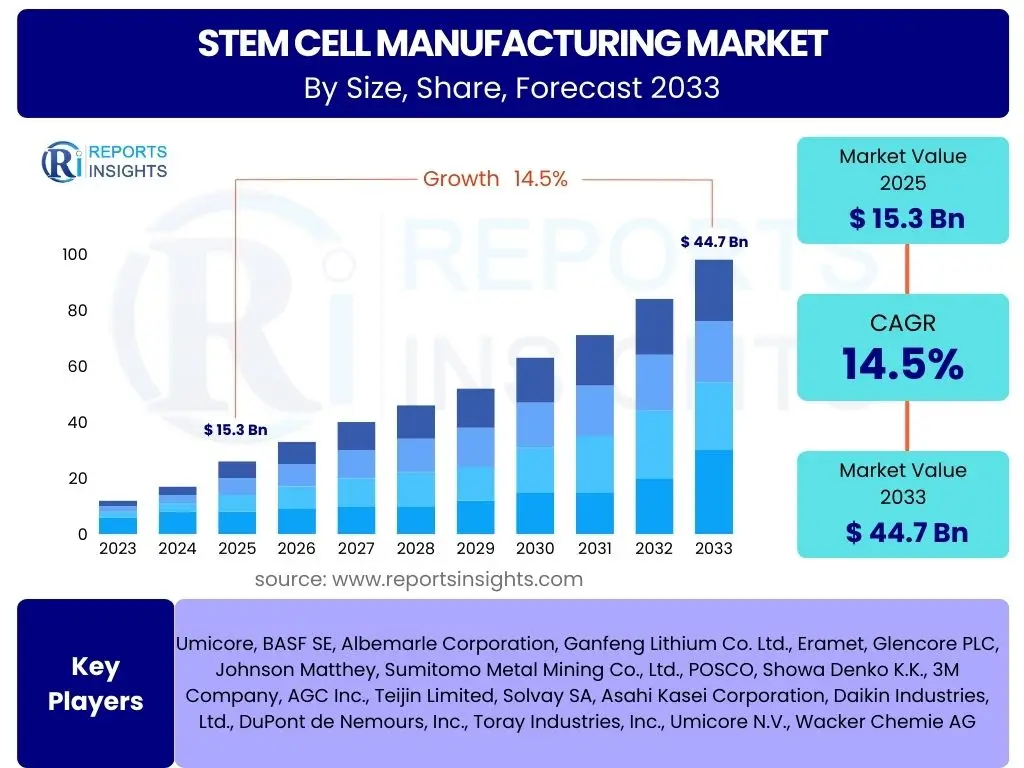

Stem Cell Manufacturing Market Size

According to Reports Insights Consulting Pvt Ltd, The Stem Cell Manufacturing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% between 2025 and 2033. The market is estimated at USD 15.3 Billion in 2025 and is projected to reach USD 44.7 Billion by the end of the forecast period in 2033.

Key Stem Cell Manufacturing Market Trends & Insights

User inquiries frequently highlight the rapid evolution of stem cell research and its translation into therapeutic applications. A significant trend observed is the increasing adoption of induced pluripotent stem cells (iPSCs) due to their ethical advantages and potential for patient-specific therapies, alongside advancements in gene-editing technologies like CRISPR. Furthermore, the market is witnessing a shift towards automated and closed manufacturing systems to enhance scalability, reduce contamination risks, and improve cost-efficiency. These trends collectively underscore a move towards more accessible, personalized, and robust stem cell-based treatments.

Another area of consistent interest concerns the expansion of regenerative medicine applications beyond conventional areas. This includes a growing focus on neurological disorders, cardiovascular diseases, and diabetes, driving demand for specialized stem cell lines and manufacturing protocols. The integration of advanced biomanufacturing techniques, such as 3D bioprinting for tissue engineering and organoids, also represents a pivotal trend, promising to revolutionize drug discovery and therapeutic development. This convergence of technologies indicates a future where stem cell manufacturing is more integrated, efficient, and versatile.

- Increasing adoption of Induced Pluripotent Stem Cells (iPSCs) for therapeutic and research applications.

- Integration of advanced gene-editing technologies, such as CRISPR, to enhance stem cell functionality and safety.

- Development and implementation of automated and closed manufacturing systems for scalability and cost reduction.

- Expansion of regenerative medicine applications into new therapeutic areas, including neurological and cardiovascular diseases.

- Growing emphasis on 3D bioprinting and organoid development for drug screening and tissue engineering.

- Rise in demand for allogeneic stem cell therapies due to their off-the-shelf availability and cost-effectiveness.

AI Impact Analysis on Stem Cell Manufacturing

User queries regarding AI's impact on stem cell manufacturing frequently revolve around its potential to accelerate research, improve process efficiency, and ensure product quality. There is strong interest in how AI can optimize cell culture conditions, predict cell behavior, and automate complex laboratory procedures, thereby reducing human error and resource consumption. Users are keen to understand AI's role in areas like image analysis for cell characterization, data interpretation from high-throughput screening, and the design of novel manufacturing protocols, all aimed at achieving more consistent and effective stem cell products.

Furthermore, concerns and expectations often touch upon AI's capacity to personalize stem cell therapies and streamline regulatory pathways. The ability of AI to analyze vast datasets, including patient-specific genetic information, could lead to more tailored treatment approaches, while its application in predictive modeling might assist in foreseeing potential manufacturing bottlenecks or quality deviations. The overarching expectation is that AI will serve as a transformative tool, driving innovation, enhancing precision, and ultimately making stem cell therapies more widely available and successful. However, challenges related to data security, algorithmic bias, and the need for specialized expertise are also frequently highlighted.

- AI optimizes cell culture media and conditions, enhancing proliferation and differentiation efficiency.

- Machine learning algorithms predict cell behavior and viability, improving process consistency and yield.

- AI-powered image analysis automates quality control, ensuring cell purity and morphology standards.

- Robotics and AI enable high-throughput screening and automation of complex manufacturing steps.

- Predictive analytics supports supply chain optimization and demand forecasting for stem cell products.

- AI assists in analyzing genomic data for personalized stem cell therapy development and patient stratification.

Key Takeaways Stem Cell Manufacturing Market Size & Forecast

A primary takeaway highlighted by user inquiries is the robust growth trajectory of the Stem Cell Manufacturing Market, driven by advancements in regenerative medicine and increasing investment in biopharmaceutical research. Stakeholders are keen to understand the core factors contributing to the projected market expansion, particularly the rise in chronic diseases, the aging global population, and the continuous flow of R&D funding into stem cell therapies. The market's significant financial growth signifies a maturing industry with substantial potential for therapeutic breakthroughs.

Another crucial insight pertains to the strategic importance of technological innovation and regulatory landscapes. Users frequently seek information on how new manufacturing techniques, such as automation and closed systems, are enabling scalability, while evolving regulatory guidelines are shaping market access and product development. The forecast indicates that companies capable of navigating these complex technical and regulatory environments efficiently will be best positioned to capitalize on the market's expansion, solidifying their competitive advantage through innovation and compliance. The shift towards personalized and allogeneic therapies further underscores the need for adaptable and efficient manufacturing platforms.

- The market is poised for significant growth, exceeding a 14% CAGR, driven by scientific advancements and unmet medical needs.

- Investments in automated manufacturing and process optimization are critical for achieving scalability and cost-effectiveness.

- Induced Pluripotent Stem Cells (iPSCs) and mesenchymal stem cells (MSCs) are emerging as key therapeutic assets.

- Regenerative medicine applications across various disease areas will fuel demand for specialized stem cell products.

- Collaboration between academia, biotech firms, and regulatory bodies is essential for accelerating market development.

- North America and Europe will remain dominant, but Asia Pacific is expected to exhibit the highest growth rate.

Stem Cell Manufacturing Market Drivers Analysis

The Stem Cell Manufacturing Market is propelled by several robust drivers, fundamentally rooted in the global health landscape and scientific progress. A paramount driver is the escalating prevalence of chronic diseases, including cardiovascular disorders, neurodegenerative conditions, and autoimmune diseases, which often lack effective conventional treatments. Stem cell therapies offer a promising alternative, driving significant demand for their manufacturing and development. This unmet medical need creates a substantial market for innovative regenerative solutions.

Another key driver is the continuous advancement in stem cell research and technology. Breakthroughs in gene editing, cell culture techniques, and differentiation protocols are expanding the potential applications of stem cells beyond traditional boundaries. Furthermore, increasing public and private funding for regenerative medicine research and development plays a crucial role. Governments and venture capitalists are recognizing the transformative potential of stem cell therapies, leading to more investment in research infrastructure, clinical trials, and manufacturing capabilities, thereby accelerating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Chronic Diseases | +2.1% | Global, particularly North America, Europe, APAC | Long-term (2025-2033) |

| Advancements in Regenerative Medicine and Gene Therapy | +1.8% | Global | Mid-to-Long term (2025-2033) |

| Growing Funding for Stem Cell Research & Development | +1.5% | North America, Europe, China, Japan | Mid-term (2025-2030) |

| Rising Geriatric Population and Associated Conditions | +1.2% | Europe, Japan, North America | Long-term (2025-2033) |

| Technological Innovations in Cell Culture & Bioreactor Systems | +1.0% | Global | Short-to-Mid term (2025-2028) |

Stem Cell Manufacturing Market Restraints Analysis

Despite significant growth potential, the Stem Cell Manufacturing Market faces several notable restraints that could temper its expansion. One of the most prominent challenges is the high cost associated with stem cell research, development, and manufacturing. Producing clinical-grade stem cells often requires expensive specialized equipment, highly skilled personnel, and stringent quality control measures, leading to high production costs that can translate into prohibitive treatment prices for patients and healthcare systems. This financial barrier limits the widespread adoption of stem cell therapies.

Another significant restraint involves the complex and evolving regulatory landscape. The ethical considerations surrounding certain types of stem cells, coupled with the novelty and intricate nature of these therapies, necessitate rigorous and lengthy approval processes by regulatory bodies worldwide. Inconsistent regulations across different regions can further complicate global market entry and product commercialization. Furthermore, technical complexities related to cell viability, purity, and scalability in large-scale manufacturing pose significant hurdles, requiring continuous innovation and substantial investment to overcome.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Stem Cell Research and Manufacturing | -1.5% | Global | Long-term (2025-2033) |

| Stringent and Evolving Regulatory Frameworks | -1.2% | North America, Europe, Asia Pacific | Mid-to-Long term (2025-2033) |

| Ethical Concerns Associated with Certain Stem Cell Types | -0.8% | Global, particularly Western countries | Long-term (2025-2033) |

| Technical Challenges in Scalability and Standardization | -0.7% | Global | Mid-term (2025-2030) |

| Limited Reimbursement Policies for Stem Cell Therapies | -0.5% | North America, Europe | Short-to-Mid term (2025-2028) |

Stem Cell Manufacturing Market Opportunities Analysis

The Stem Cell Manufacturing Market is rich with opportunities, driven by scientific advancements and an expanding understanding of cell biology. A significant opportunity lies in the burgeoning field of personalized medicine, where patient-specific stem cells can be manufactured to treat a wide array of diseases with greater efficacy and reduced immunological rejection. This approach promises to revolutionize therapeutic strategies, particularly for conditions currently lacking adequate treatment options, thereby creating a high-value niche for specialized manufacturing services.

Furthermore, the convergence of stem cell technology with gene therapy and immunotherapy presents immense potential for developing highly advanced and targeted treatments. Combining the regenerative capabilities of stem cells with the precision of gene editing or the power of immune modulation can lead to synergistic therapeutic effects. Emerging economies in Asia Pacific and Latin America also represent vast untapped markets. These regions are increasingly investing in healthcare infrastructure and biotechnology, offering new avenues for market penetration and growth through localized manufacturing and research initiatives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Personalized and Autologous Therapies | +1.7% | Global | Mid-to-Long term (2025-2033) |

| Integration with Gene Therapy and Immunotherapy | +1.5% | North America, Europe, Asia Pacific | Mid-term (2025-2030) |

| Untapped Markets in Emerging Economies | +1.3% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Development of Off-the-Shelf Allogeneic Therapies | +1.0% | Global | Mid-term (2025-2030) |

| Strategic Partnerships and Collaborations | +0.8% | Global | Short-to-Mid term (2025-2028) |

Stem Cell Manufacturing Market Challenges Impact Analysis

The Stem Cell Manufacturing Market faces several critical challenges that require strategic solutions to sustain its growth trajectory. One of the primary challenges is achieving consistent product quality and standardization across different manufacturing batches and facilities. Variations in cell sourcing, processing protocols, and culture conditions can lead to heterogeneity in the final product, affecting therapeutic efficacy and patient safety. Establishing robust quality control mechanisms and industry-wide standards is paramount but complex.

Another significant hurdle involves the scalability of manufacturing processes to meet increasing clinical and commercial demand. While laboratory-scale production is feasible, translating these processes to industrial scales while maintaining cell viability, purity, and functionality is technically demanding and capital-intensive. This often requires significant investment in automated bioreactor systems and process optimization. Furthermore, securing adequate funding for late-stage clinical trials and navigating the intricate market access and reimbursement landscapes remain substantial challenges for companies striving to bring stem cell therapies to patients.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Standardization and Reproducibility | -1.4% | Global | Long-term (2025-2033) |

| Scalability of Manufacturing for Commercial Production | -1.1% | Global | Mid-to-Long term (2025-2033) |

| Ensuring Cell Viability and Purity During Transport & Storage | -0.9% | Global | Short-to-Mid term (2025-2028) |

| High Capital Investment and Operational Costs | -0.7% | Global | Long-term (2025-2033) |

| Workforce Shortage with Specialized Expertise | -0.5% | North America, Europe | Mid-term (2025-2030) |

Stem Cell Manufacturing Market - Updated Report Scope

This report provides a detailed analysis of the Stem Cell Manufacturing Market, covering historical performance from 2019 to 2023, with a comprehensive forecast extending from 2025 to 2033. It elucidates market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The scope encompasses an in-depth assessment of technological advancements, competitive landscape, and strategic developments shaping the industry, offering a holistic view for stakeholders seeking to understand market dynamics and future prospects.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.3 Billion |

| Market Forecast in 2033 | USD 44.7 Billion |

| Growth Rate | 14.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lonza Group AG, Thermo Fisher Scientific Inc., Danaher Corporation, Merck KGaA, FUJIFILM Diosynth Biotechnologies, Sartorius AG, STEMCELL Technologies Inc., Miltenyi Biotec GmbH, CellGenix GmbH, Cook Medical LLC, Takara Bio Inc., Pluristem Therapeutics Inc., Osiris Therapeutics Inc., Mesoblast Ltd., Advanced Cell Technology Inc., Takeda Pharmaceutical Company Limited, Astellas Pharma Inc., Cynata Therapeutics Limited, AlloSource, DiscGenics Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Stem Cell Manufacturing Market is meticulously segmented to provide a granular understanding of its diverse components, reflecting the varied needs and applications within the broader regenerative medicine landscape. This segmentation allows for a detailed analysis of market dynamics across different product types, cell sources, therapeutic applications, and end-user categories. Understanding these distinct segments is crucial for identifying key growth areas, assessing competitive pressures, and formulating targeted market strategies for both established players and new entrants.

Each segment is characterized by unique drivers, challenges, and opportunities, influenced by technological advancements, regulatory frameworks, and specific end-user requirements. For instance, the consumables segment is driven by the continuous demand for cell culture media and reagents, while the software segment benefits from the increasing need for data management and analysis in research and manufacturing. Similarly, the application segments highlight where the most significant therapeutic breakthroughs and commercial adoptions are occurring, directing strategic investments and research efforts. This comprehensive segmentation ensures a thorough market assessment.

- By Product:

- Instruments

- Consumables

- Software

- Services

- By Type:

- Adult Stem Cells

- Induced Pluripotent Stem Cells (iPSCs)

- Embryonic Stem Cells

- Mesenchymal Stem Cells (MSCs)

- Hematopoietic Stem Cells (HSCs)

- By Application:

- Regenerative Medicine

- Drug Discovery & Development

- Cancer Research

- Toxicology Testing

- Gene Therapy

- Cell & Tissue Banking

- By End-User:

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutions

- Hospitals & Clinics

- Contract Research Organizations (CROs)

- Cell Banks

Regional Highlights

- North America: This region consistently leads the global Stem Cell Manufacturing Market, primarily due to substantial investments in research and development, the presence of major biopharmaceutical companies, and a supportive regulatory environment. High prevalence of chronic diseases, advanced healthcare infrastructure, and increasing adoption of personalized medicine further contribute to its dominance. The United States accounts for the largest share within North America, driven by robust funding and a strong innovation ecosystem.

- Europe: Europe represents a significant market share, characterized by strong governmental support for scientific research, particularly in countries like Germany, the UK, and France. The region benefits from a well-established academic and research base, coupled with a growing number of biotechnology startups focused on regenerative therapies. Harmonization of regulatory guidelines across the European Union is expected to further streamline market access and foster growth.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest CAGR during the forecast period. This rapid growth is attributed to increasing healthcare expenditure, a large patient pool, improving healthcare infrastructure, and rising awareness of stem cell therapies. Countries like China, Japan, South Korea, and India are investing heavily in biotechnology and stem cell research, driven by government initiatives and a burgeoning private sector. The availability of skilled labor at competitive costs also attracts manufacturing investments.

- Latin America: This region is an emerging market, driven by increasing healthcare awareness, improving economic conditions, and growing interest in medical tourism for advanced therapies. While smaller in market size compared to developed regions, countries like Brazil and Mexico are witnessing nascent developments in stem cell research and clinical applications, presenting future growth opportunities.

- Middle East and Africa (MEA): The MEA market is still in its early stages but shows potential, particularly in countries with high oil revenues investing in diversifying their economies, including healthcare and biotechnology. Initiatives to build modern medical facilities and research centers, alongside a growing burden of chronic diseases, are expected to gradually propel market expansion in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Stem Cell Manufacturing Market.- Lonza Group AG

- Thermo Fisher Scientific Inc.

- Danaher Corporation

- Merck KGaA

- FUJIFILM Diosynth Biotechnologies

- Sartorius AG

- STEMCELL Technologies Inc.

- Miltenyi Biotec GmbH

- CellGenix GmbH

- Cook Medical LLC

- Takara Bio Inc.

- Pluristem Therapeutics Inc.

- Osiris Therapeutics Inc.

- Mesoblast Ltd.

- Advanced Cell Technology Inc.

- Takeda Pharmaceutical Company Limited

- Astellas Pharma Inc.

- Cynata Therapeutics Limited

- AlloSource

- DiscGenics Inc.

Frequently Asked Questions

Analyze common user questions about the Stem Cell Manufacturing market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary types of stem cells used in manufacturing?

The primary types of stem cells utilized in manufacturing include Adult Stem Cells (such as Mesenchymal Stem Cells and Hematopoietic Stem Cells), Induced Pluripotent Stem Cells (iPSCs), and Embryonic Stem Cells. Each type offers distinct advantages for various therapeutic and research applications, with iPSCs gaining prominence due to their pluripotency and ethical advantages.

How do automation and AI impact stem cell manufacturing processes?

Automation and Artificial Intelligence (AI) significantly enhance stem cell manufacturing by improving efficiency, reproducibility, and scalability. They enable precise control over cell culture conditions, automate complex processing steps, and facilitate high-throughput screening. AI-powered analytics also aid in quality control, predictive modeling, and optimization of manufacturing protocols, ultimately reducing costs and accelerating development.

What are the main applications driving demand in the stem cell manufacturing market?

The main applications fueling demand in the stem cell manufacturing market are regenerative medicine, drug discovery and development, and cancer research. Stem cells are crucial for developing therapies for chronic diseases, modeling human diseases for drug screening, and understanding cancer biology. Gene therapy and toxicology testing also represent significant and growing application areas.

What are the key challenges in scaling up stem cell manufacturing for commercial use?

Key challenges in scaling up stem cell manufacturing for commercial use include maintaining consistent cell viability, purity, and functionality across large batches, establishing robust standardization and quality control protocols, and overcoming the high capital investment required for automated bioreactor systems. Additionally, navigating complex regulatory pathways and securing sufficient funding for late-stage clinical trials remain significant hurdles.

Which regions are leading the stem cell manufacturing market, and why?

North America, particularly the United States, and Europe are currently leading the stem cell manufacturing market. This dominance is attributed to substantial R&D investments, the presence of major biopharmaceutical companies, advanced healthcare infrastructure, and supportive government funding and regulatory frameworks. The high prevalence of chronic diseases and strong academic-industry collaborations also contribute to their leadership.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted