Sputtering Target Market

Sputtering Target Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704543 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Sputtering Target Market Size

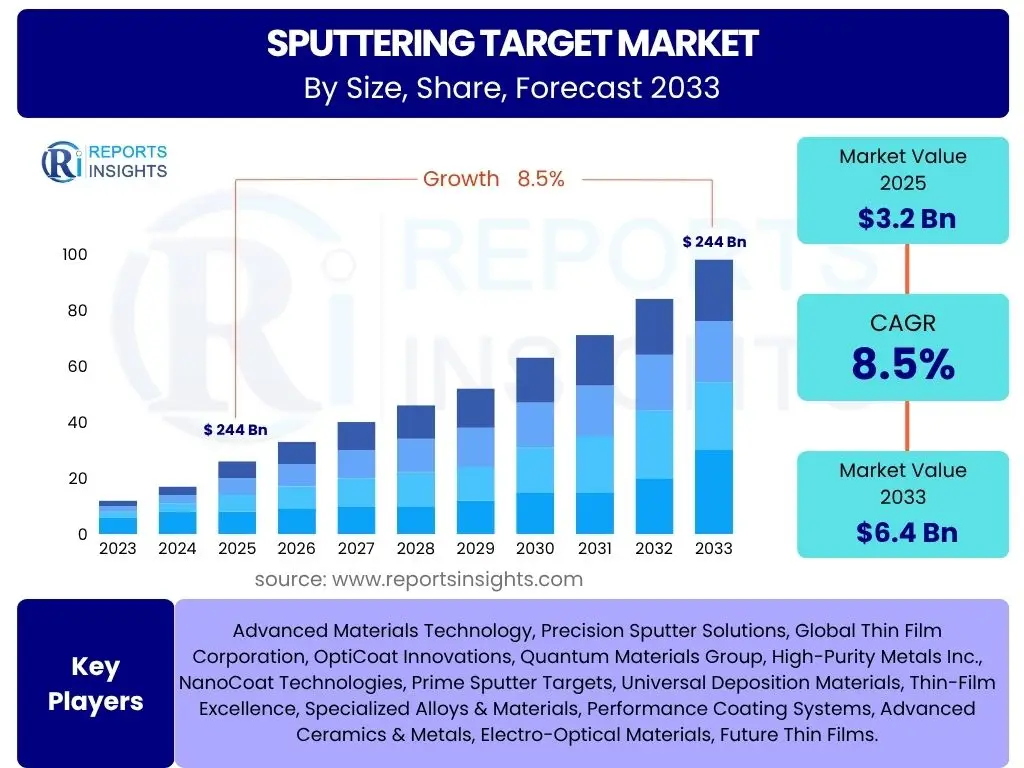

According to Reports Insights Consulting Pvt Ltd, The Sputtering Target Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 3.2 Billion in 2025 and is projected to reach USD 6.4 Billion by the end of the forecast period in 2033.

Key Sputtering Target Market Trends & Insights

The sputtering target market is currently undergoing significant transformation, primarily driven by rapid advancements in the electronics and display sectors. User inquiries consistently highlight the increasing demand for high-purity and specialized targets as miniaturization and performance requirements in semiconductors and sophisticated display technologies become more stringent. This trend is further amplified by the expansion of innovative applications beyond traditional electronics, pushing the boundaries of material science and deposition techniques.

Another prominent trend attracting considerable attention is the growing integration of sputtering technology into emerging fields such as renewable energy, particularly thin-film solar cells, and advanced automotive electronics, including sensors and infotainment systems. The push towards sustainable manufacturing practices and the development of new functional coatings for enhanced durability and efficiency are also key areas of interest, influencing research and development efforts across the industry.

- Miniaturization in Semiconductor Manufacturing: Driving demand for ultra-high purity and advanced material targets for smaller, more powerful chips.

- Evolution of Flat Panel Displays: Increased adoption of OLED, QLED, and micro-LED technologies requiring specialized targets for superior optical properties.

- Growth in Automotive Electronics: Expansion of advanced driver-assistance systems (ADAS), in-car entertainment, and electric vehicle components necessitating durable and high-performance coatings.

- Renewable Energy Sector Expansion: Rising demand for sputtering targets in thin-film solar cells, fuel cells, and energy storage devices.

- Advancements in Medical Devices and Biomedical Coatings: Increasing use of biocompatible and anti-bacterial coatings for implants and surgical instruments.

- Development of Wear-Resistant and Decorative Coatings: Growing applications in industrial tools, consumer goods, and architectural glass for enhanced durability and aesthetic appeal.

AI Impact Analysis on Sputtering Target

The integration of Artificial Intelligence (AI) and machine learning (ML) is anticipated to profoundly impact the sputtering target market, addressing common user concerns regarding manufacturing efficiency, material innovation, and quality control. AI can optimize sputtering parameters, leading to improved film uniformity, adhesion, and purity, thereby reducing material waste and enhancing production yields. This capability is particularly crucial for complex multi-layered structures and novel material compositions, which are becoming increasingly prevalent in advanced electronics and specialized coatings.

Furthermore, AI-driven analytics can significantly accelerate the discovery and development of new sputtering target materials and alloys. By analyzing vast datasets from experimental results, simulations, and material properties, AI algorithms can predict optimal compositions and processing routes, drastically shortening research and development cycles. Users expect AI to streamline quality assurance processes through real-time monitoring and anomaly detection, ensuring consistent product quality and mitigating potential defects, thereby fostering greater reliability and cost-effectiveness in manufacturing operations.

- Optimized Sputtering Process Parameters: AI algorithms can analyze real-time data to fine-tune power, pressure, temperature, and gas flow for superior film properties and reduced material consumption.

- Accelerated Material Discovery and Design: AI can predict novel material compositions with desired properties, reducing trial-and-error in developing new sputtering targets and thin films.

- Enhanced Quality Control and Defect Detection: Machine vision and AI analytics can identify microscopic defects in targets and deposited films, ensuring higher product quality and reliability.

- Predictive Maintenance for Sputtering Systems: AI can forecast equipment failures, enabling proactive maintenance and minimizing downtime in manufacturing facilities.

- Automated Data Analysis and Reporting: AI tools can process large volumes of manufacturing data, providing actionable insights for process improvement and strategic decision-making.

- Improved Supply Chain Management: AI can optimize inventory levels and logistics for raw materials and finished targets, enhancing efficiency and resilience against disruptions.

Key Takeaways Sputtering Target Market Size & Forecast

The sputtering target market is poised for robust growth through 2033, a trajectory largely influenced by the escalating demand for high-performance materials across diverse industrial applications. A significant takeaway is the pivotal role of the semiconductor and flat panel display industries, which continue to be primary consumers, driving innovation in target purity and composition. The forecast indicates sustained expansion, underpinned by ongoing technological advancements that necessitate increasingly sophisticated thin-film deposition capabilities.

Another crucial insight is the emergence of new growth vectors in automotive electronics, renewable energy, and medical devices, diversifying the market's revenue streams and reducing its sole reliance on traditional electronics. Geographically, Asia Pacific is expected to maintain its dominance, propelled by substantial investments in manufacturing infrastructure and a burgeoning consumer electronics market. The market's future success is also dependent on overcoming challenges related to high production costs and raw material price volatility, requiring strategic partnerships and continuous innovation in material science.

- Significant Growth Projection: The market is set for substantial expansion, reaching USD 6.4 Billion by 2033, driven by broad industrial applications.

- Semiconductor and Display Dominance: These sectors remain the core drivers, dictating the demand for advanced and specialized sputtering targets.

- Emerging Application Expansion: New opportunities in automotive, renewable energy, and medical devices are diversifying market demand.

- Asia Pacific Leads Regional Growth: The region's robust electronics manufacturing base positions it as the primary market for sputtering targets.

- Material Innovation Focus: Continued research into new alloys and high-purity materials is critical for meeting evolving performance requirements.

- Operational Efficiency Imperative: Addressing production costs and supply chain stability will be key to sustainable market expansion.

Sputtering Target Market Drivers Analysis

The sputtering target market's expansion is fundamentally propelled by several critical factors, predominantly the relentless growth and evolution of the global semiconductor industry. As electronic devices become more powerful, compact, and energy-efficient, there is a continuous demand for higher purity and more complex material targets to achieve advanced chip functionalities. This technological imperative drives innovation in sputtering target compositions and manufacturing processes, ensuring the availability of materials capable of meeting stringent performance criteria.

Beyond semiconductors, the burgeoning demand for sophisticated flat panel displays across various consumer electronics, including smartphones, televisions, and wearable devices, significantly contributes to market growth. The increasing adoption of OLED and QLED technologies, alongside advancements in automotive electronics for in-vehicle infotainment and safety systems, further fuels the need for specialized sputtering targets that enable the creation of high-definition, durable, and functional thin films. These drivers collectively create a robust and expanding market for sputtering targets across multiple high-tech industries.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Semiconductor Industry | +2.5% | Global, particularly APAC (China, South Korea, Taiwan) | Long-term (2025-2033) |

| Expanding Flat Panel Display Market | +1.8% | APAC (China, Japan, South Korea), North America | Medium-term (2025-2030) |

| Increasing Automotive Electronics Adoption | +1.5% | North America, Europe, APAC (Japan, South Korea) | Long-term (2025-2033) |

| Advancements in Thin-Film Technologies | +1.2% | Global | Long-term (2025-2033) |

| Rising Demand for High-Performance Coatings | +1.0% | Global, across industrial and consumer sectors | Medium-term (2025-2030) |

Sputtering Target Market Restraints Analysis

Despite the positive growth outlook, the sputtering target market faces several inherent restraints that could temper its expansion. One significant challenge is the substantial capital investment required for establishing and maintaining high-purity sputtering target manufacturing facilities. The specialized equipment, stringent cleanroom environments, and complex processing techniques involved in producing high-quality targets contribute to high operational costs, which can act as a barrier to entry for new players and limit expansion for existing ones, particularly for niche materials.

Moreover, the market is susceptible to volatility in raw material prices, as many sputtering targets rely on rare metals and specialized alloys, whose supply chains can be subject to geopolitical factors, mining limitations, or sudden demand surges. Stringent environmental regulations related to the disposal and recycling of hazardous materials used in target manufacturing and the byproducts of the sputtering process also pose operational and financial challenges. Additionally, competition from alternative thin-film deposition techniques, such as chemical vapor deposition (CVD) and atomic layer deposition (ALD), which may offer cost or performance advantages in specific applications, can also act as a market restraint, compelling manufacturers to continuously innovate and differentiate their offerings.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment for Manufacturing | -1.0% | Global | Long-term (2025-2033) |

| Stringent Environmental Regulations | -0.8% | Europe, North America, parts of Asia | Medium-term (2025-2030) |

| Raw Material Price Volatility | -0.7% | Global | Short-term (2025-2027) |

| Competition from Alternative Deposition Technologies | -0.5% | Global | Long-term (2025-2033) |

Sputtering Target Market Opportunities Analysis

The sputtering target market is characterized by several promising opportunities that are anticipated to drive future growth and innovation. A key area of growth lies in the burgeoning field of flexible electronics, where sputtering targets are crucial for depositing conductive and insulating layers on flexible substrates, enabling the development of bendable displays, wearable devices, and smart textiles. This segment offers significant potential as consumer demand shifts towards more versatile and integrated electronic solutions.

Furthermore, the escalating global emphasis on renewable energy presents a substantial opportunity for sputtering target manufacturers, particularly in the production of high-efficiency thin-film solar cells and advanced battery technologies. The ongoing research and development in next-generation materials, such as those for quantum computing and advanced sensors, also create new avenues for specialized sputtering targets. Strategic partnerships and collaborations between target manufacturers, equipment suppliers, and end-use industries can unlock further opportunities by facilitating the development of tailored solutions and accelerating market penetration in these high-growth sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in Flexible Electronics | +1.5% | APAC, North America, Europe | Long-term (2025-2033) |

| Growth in Renewable Energy Sector (Solar, Fuel Cells) | +1.3% | Global, particularly China, EU, US | Long-term (2025-2033) |

| Research & Development in Advanced Materials | +1.0% | North America, Europe, Japan | Long-term (2025-2033) |

| Demand for Smart Packaging & IoT Devices | +0.8% | Global | Medium-term (2025-2030) |

Sputtering Target Market Challenges Impact Analysis

The sputtering target market faces distinct challenges that require strategic responses from manufacturers and stakeholders. One primary challenge is the continuous demand for achieving ultra-high purity levels in targets, especially for advanced semiconductor and optical applications. Impurities, even at trace levels, can severely degrade the performance and reliability of thin films, necessitating sophisticated and costly purification processes that are difficult to scale while maintaining cost-effectiveness.

Furthermore, managing the waste generated during target manufacturing and the recycling of spent targets poses a significant environmental and economic challenge. Many target materials are rare or toxic, requiring specialized handling and disposal protocols. The rapid pace of technological obsolescence in end-use industries, particularly electronics, means that sputtering target manufacturers must constantly innovate and adapt their product lines, which demands substantial R&D investment and can lead to shorter product lifecycles. Lastly, a shortage of skilled labor proficient in advanced material science, thin-film deposition, and precision manufacturing techniques can hinder production capabilities and innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Ultra-High Purity Levels | -1.2% | Global | Long-term (2025-2033) |

| Waste Management and Recycling of Targets | -0.9% | Europe, North America, Japan | Medium-term (2025-2030) |

| Rapid Technological Obsolescence | -0.7% | Global | Short-term (2025-2028) |

| Skilled Workforce Shortage | -0.6% | Global | Long-term (2025-2033) |

Sputtering Target Market - Updated Report Scope

This report provides a comprehensive analysis of the global sputtering target market, encompassing historical data, current market dynamics, and future projections. It delves into the key drivers, restraints, opportunities, and challenges influencing market growth, offering a detailed segmentation across various material types, applications, end-use industries, and forms. The report also highlights regional market trends and profiles leading companies to provide a holistic understanding of the competitive landscape and strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.2 Billion |

| Market Forecast in 2033 | USD 6.4 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Materials Technology, Precision Sputter Solutions, Global Thin Film Corporation, OptiCoat Innovations, Quantum Materials Group, High-Purity Metals Inc., NanoCoat Technologies, Prime Sputter Targets, Universal Deposition Materials, Thin-Film Excellence, Specialized Alloys & Materials, Performance Coating Systems, Advanced Ceramics & Metals, Electro-Optical Materials, Future Thin Films. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The sputtering target market is comprehensively segmented to provide granular insights into its diverse components, reflecting the varied applications and material requirements across industries. This segmentation aids in understanding the specific drivers and opportunities within each category, from the types of materials used to their end-use applications and physical forms. Such detailed analysis is crucial for stakeholders to identify high-growth areas and tailor their product development and market strategies effectively.

The segmentation by material type highlights the critical role of specific metals, alloys, and ceramics, each offering unique properties essential for different thin-film characteristics. Application-based segmentation reveals the market's reliance on high-tech sectors like semiconductors and displays, while also pointing to emerging areas such as medical devices and renewable energy. Furthermore, delineating by end-use industry and target form provides a clearer picture of market demands and technological preferences across the global landscape.

- By Material Type:

- Metals: Aluminum, Copper, Titanium, Tungsten, Chromium, Niobium

- Alloys: Al-Si, Ti-Al, Ni-Cr, Co-Fe

- Ceramics: ITO (Indium Tin Oxide), IGZO (Indium Gallium Zinc Oxide), SiO2 (Silicon Dioxide), Al2O3 (Aluminum Oxide), TiN (Titanium Nitride), SiC (Silicon Carbide)

- Pure Elements: Silicon, Germanium, Gold, Silver, Platinum

- By Application:

- Semiconductor: Logic & Memory Devices, Power Devices, MEMS

- Displays: LCD, OLED, QLED, Micro-LED

- Solar Cells: CIGS (Copper Indium Gallium Selenide), Amorphous Silicon, CdTe (Cadmium Telluride)

- Decorative Coatings

- Wear-Resistant Coatings

- Optical Coatings

- Data Storage: HDD, SSD

- Medical Devices: Implants, Surgical Tools

- Sensors

- By End-Use Industry:

- Electronics: Consumer Electronics, Industrial Electronics

- Automotive

- Aerospace & Defense

- Energy: Solar, Fuel Cells

- Medical

- Industrial Tools

- Architectural Glass

- By Form:

- Planar Target

- Rotary Target

Regional Highlights

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for sputtering targets, primarily driven by the colossal manufacturing bases for semiconductors, flat panel displays, and consumer electronics in countries like China, South Korea, Japan, and Taiwan. Significant government investments in advanced manufacturing and a rapidly expanding middle class with increasing disposable income further fuel demand for electronic devices and, consequently, sputtering targets. The region is also a hub for innovation in thin-film solar technology and flexible electronics, consolidating its market leadership.

- North America: The North American market is characterized by robust demand from the advanced electronics, aerospace & defense, and automotive sectors. The United States, in particular, is a leader in semiconductor research and development, high-performance computing, and specialized medical device manufacturing, all of which require sophisticated sputtering targets. Emphasis on high-purity materials and stringent quality standards drives premium product demand in this region.

- Europe: Europe's sputtering target market is propelled by strong automotive, industrial tooling, and optical coating industries. Countries such as Germany, the UK, and France are significant contributors, focusing on innovative coatings for wear resistance, decorative finishes, and precision optics. The region also demonstrates a growing interest in renewable energy applications and environmental sustainability, influencing the demand for eco-friendly sputtering solutions.

- Latin America: While a smaller market, Latin America is experiencing gradual growth, primarily due to expanding automotive production and increasing demand for consumer electronics. Brazil and Mexico are key countries, focusing on establishing domestic manufacturing capabilities and adopting advanced coating technologies. The region offers opportunities for targeted expansion as industrialization progresses.

- Middle East and Africa (MEA): The MEA region is an emerging market for sputtering targets, driven by infrastructure development, diversification of economies, and growing investments in industrial and automotive sectors. The demand for architectural glass coatings for energy efficiency and decorative purposes, alongside nascent electronics manufacturing, presents long-term growth prospects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Sputtering Target Market.- Advanced Materials Technology

- Precision Sputter Solutions

- Global Thin Film Corporation

- OptiCoat Innovations

- Quantum Materials Group

- High-Purity Metals Inc.

- NanoCoat Technologies

- Prime Sputter Targets

- Universal Deposition Materials

- Thin-Film Excellence

- Specialized Alloys & Materials

- Performance Coating Systems

- Advanced Ceramics & Metals

- Electro-Optical Materials

- Future Thin Films

- PVD Products Inc.

- Sputtertech Solutions

- Vapor Deposition Systems

- Applied Materials Group

- Material Science Innovators

Frequently Asked Questions

Analyze common user questions about the Sputtering Target market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a sputtering target and how does it work?

A sputtering target is a source material used in physical vapor deposition (PVD) processes, specifically sputtering, to deposit thin films onto a substrate. An energized plasma bombards the target, dislodging atoms that then condense as a thin film on the desired surface. This process is crucial for creating precise and uniform coatings across various industries.

What are the primary applications of sputtering targets?

Sputtering targets are predominantly used in the manufacturing of semiconductors, flat panel displays (LCD, OLED), solar cells, and data storage devices. They also find extensive use in creating decorative, wear-resistant, and optical coatings for industrial tools, automotive components, architectural glass, and medical devices.

Which material types are commonly used for sputtering targets?

Common sputtering target materials include various metals like aluminum, copper, and titanium; alloys such as Al-Si and Ti-Al; and ceramics like ITO, IGZO, and silicon dioxide. Pure elements like silicon, gold, and silver are also frequently utilized depending on the specific thin-film properties required for the application.

What are the key factors driving the growth of the sputtering target market?

Key growth drivers include the continuous demand for advanced semiconductors, the expansion of the flat panel display market, increasing adoption of automotive electronics, and the rising demand for high-performance coatings in industries such as renewable energy and medical devices. Technological advancements requiring ultra-thin and precise films also contribute significantly.

Which region dominates the sputtering target market?

Asia Pacific (APAC) currently dominates the sputtering target market. This is attributed to the region's large-scale manufacturing capabilities in semiconductors, consumer electronics, and displays, particularly in countries like China, South Korea, Japan, and Taiwan, which are major consumers of sputtering targets.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted