Specialty Sugar Market

Specialty Sugar Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706839 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Specialty Sugar Market Size

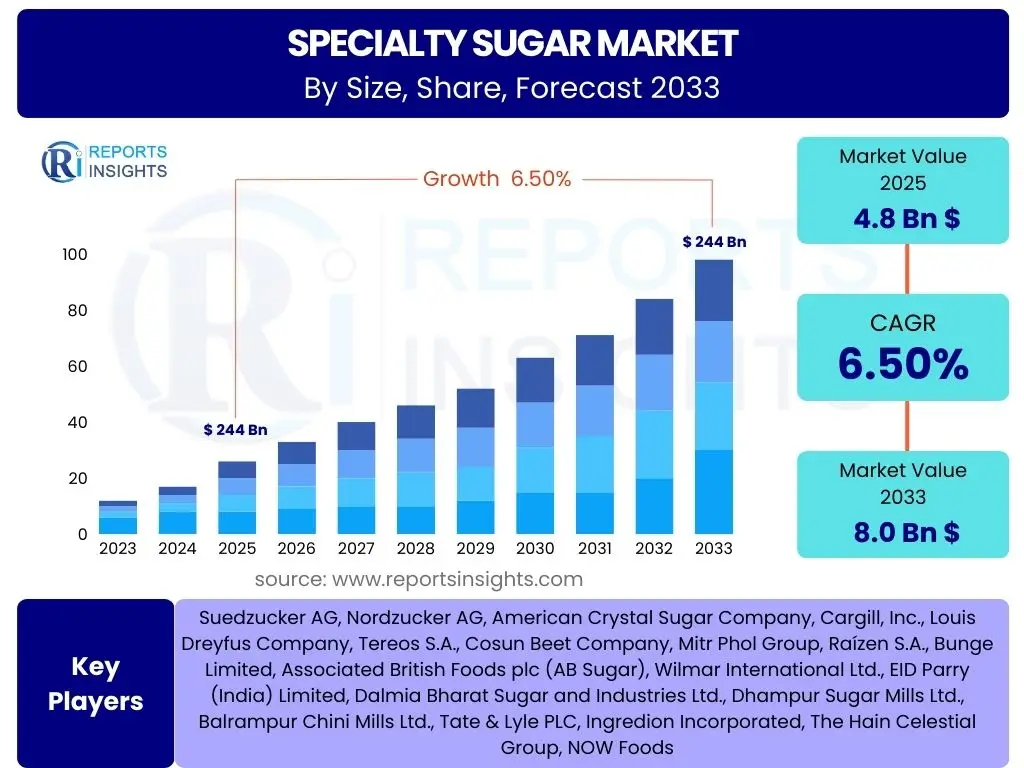

According to Reports Insights Consulting Pvt Ltd, The Specialty Sugar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at 4.8 Billion USD in 2025 and is projected to reach 8.0 Billion USD by the end of the forecast period in 2033.

Key Specialty Sugar Market Trends & Insights

The Specialty Sugar Market is undergoing significant transformation, primarily driven by evolving consumer preferences and a heightened focus on health and wellness. Consumers are increasingly seeking natural, minimally processed, and clean-label ingredients, which directly fuels the demand for specialty sugars over conventional refined options. This shift is observed across various demographic segments, influencing product development and marketing strategies within the food and beverage industry.

Furthermore, diversification in the application of specialty sugars is a notable trend. Beyond traditional confectionery and bakery, these sugars are finding expanding roles in functional foods, nutraceuticals, pharmaceuticals, and even personal care products, owing to their unique flavor profiles, textures, and perceived health benefits. Innovations in processing technologies also contribute to this trend, enabling the production of new specialty sugar variants with enhanced functional properties or improved sustainability footprints. The industry is also witnessing an emphasis on sustainable sourcing and ethical production practices, responding to growing environmental and social concerns among consumers and stakeholders.

- Rising consumer demand for natural and minimally processed food ingredients.

- Increased preference for specialty sugars due to perceived health benefits and unique flavor profiles.

- Expansion of specialty sugar applications beyond traditional food and beverage sectors.

- Growing focus on clean label and transparent ingredient sourcing.

- Technological advancements in sugar production enhancing quality and diversity.

- Emphasis on sustainable and ethical sourcing practices across the supply chain.

AI Impact Analysis on Specialty Sugar

The integration of Artificial Intelligence (AI) holds transformative potential for the Specialty Sugar Market, addressing several critical areas from raw material sourcing to final product distribution. AI-powered analytics can optimize agricultural yields for sugarcane and sugar beet cultivation by predicting optimal planting and harvesting times, monitoring soil health, and managing irrigation more efficiently. This precision agriculture approach can lead to higher quality raw materials, reduced waste, and more consistent supply chains, directly impacting the availability and cost-effectiveness of specialty sugars.

Within processing and manufacturing, AI can revolutionize quality control and product development. Machine learning algorithms can analyze vast datasets from production lines to detect impurities, optimize crystallization processes, and ensure consistent product specifications, thereby enhancing the purity and quality of specialty sugars. Furthermore, AI can accelerate the research and development of novel sugar types or functional sugar blends by simulating molecular interactions and predicting sensory attributes, leading to quicker market introduction of innovative products tailored to specific consumer demands. Supply chain logistics and demand forecasting also stand to benefit significantly, with AI optimizing routes, predicting market fluctuations, and minimizing storage costs, ultimately improving the efficiency and responsiveness of the entire specialty sugar ecosystem.

- Enhanced precision agriculture for sugarcane and sugar beet, optimizing yield and quality.

- Improved quality control and process optimization in manufacturing through AI-driven analytics.

- Accelerated research and development of novel specialty sugar products and formulations.

- Optimized supply chain management and demand forecasting, reducing waste and increasing efficiency.

- Predictive maintenance for machinery, minimizing downtime in processing facilities.

- Personalized product development based on consumer data analysis.

Key Takeaways Specialty Sugar Market Size & Forecast

The Specialty Sugar Market is poised for robust and sustained growth throughout the forecast period, driven by a confluence of evolving consumer demands, expanding application areas, and continuous innovation. A primary takeaway is the increasing consumer discernment towards healthier and more natural ingredients, positioning specialty sugars as attractive alternatives to traditional refined sugars and artificial sweeteners. This trend underscores a broader shift in dietary preferences and a growing willingness among consumers to pay a premium for products that align with their wellness goals.

Another significant insight is the diversification of revenue streams for specialty sugar producers. Beyond their traditional strongholds in confectionery and beverages, these sugars are increasingly being incorporated into nutraceuticals, functional foods, and even non-food applications like personal care, indicating a broad and untapped market potential. The market's resilience is also highlighted by its ability to navigate regulatory challenges and raw material price volatility, largely due to its value proposition tied to naturalness and specific functional attributes. The forecast indicates that key regions, particularly North America, Europe, and Asia Pacific, will continue to be pivotal drivers, with emerging economies contributing significantly to future expansion due to rising disposable incomes and changing consumption patterns.

- The market is projected to experience strong and consistent growth, surpassing previous estimates.

- Consumer-driven demand for natural, healthy, and clean-label ingredients is a primary growth catalyst.

- Application diversification into pharmaceuticals, nutraceuticals, and personal care segments is crucial.

- Asia Pacific and North America are expected to remain dominant, with significant growth potential in emerging markets.

- Innovation in product offerings and sustainable sourcing are key competitive differentiators.

- The market exhibits resilience against various restraints, driven by strong underlying demand trends.

Specialty Sugar Market Drivers Analysis

The Specialty Sugar Market's expansion is fundamentally propelled by the global shift towards health-conscious dietary choices and a preference for natural ingredients. Consumers are becoming increasingly aware of the health implications associated with excessive consumption of highly processed sugars and artificial sweeteners, leading them to seek out alternatives that are perceived as healthier, less refined, and derived from natural sources. This trend is amplified by the growing prevalence of lifestyle diseases and a greater emphasis on preventive healthcare, encouraging individuals to opt for ingredients that offer some nutritional benefits or are less detrimental to health.

Furthermore, the versatility and unique characteristics of specialty sugars, such as distinct flavors, colors, and textures, make them highly desirable in various food and beverage applications. From gourmet bakery products to craft beverages and health-focused snacks, specialty sugars provide functional benefits and enhance the sensory experience, driving their adoption across a wider range of product categories. The increasing disposable income in developing economies, coupled with a rising interest in international cuisines and premium food products, further stimulates the demand for these unique sugar varieties, contributing significantly to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Consumer Health Consciousness | +1.8% | Global, particularly North America, Europe | Short-to-Mid-term (2025-2029) |

| Growing Demand for Natural & Clean Label Ingredients | +1.5% | North America, Europe, Asia Pacific | Short-to-Mid-term (2025-2030) |

| Expansion of Food & Beverage Applications | +1.2% | Asia Pacific, Latin America, Europe | Mid-term (2026-2033) |

| Rising Demand in Pharmaceuticals and Nutraceuticals | +1.0% | North America, Europe, China | Long-term (2028-2033) |

| Technological Advancements in Sugar Production | +0.7% | Global | Mid-to-Long-term (2027-2033) |

Specialty Sugar Market Restraints Analysis

Despite robust growth drivers, the Specialty Sugar Market faces several restraining factors that could impede its full potential. One significant challenge is the increasing regulatory scrutiny and public health campaigns aimed at reducing overall sugar consumption. Governments and health organizations worldwide are implementing policies such as sugar taxes, stricter labeling requirements, and educational initiatives to combat rising rates of obesity and diabetes. These measures can diminish consumer demand for all types of sugar, including specialty varieties, by fostering a general perception that all sugars are detrimental to health, regardless of their processing or origin.

Another major restraint is the inherent volatility in raw material prices, primarily sugarcane and sugar beet. Factors such as adverse weather conditions, geopolitical tensions, and global supply-demand imbalances can lead to unpredictable fluctuations in the cost of these agricultural commodities. Such price instability directly impacts the production costs of specialty sugars, potentially narrowing profit margins for manufacturers and leading to higher retail prices, which could deter price-sensitive consumers. Additionally, the increasing competition from a wide array of alternative sweeteners, including high-intensity artificial sweeteners, natural low-calorie sweeteners (like stevia and erythritol), and sugar alcohols, poses a significant threat. These alternatives often offer lower calorie counts or functional benefits that some consumers prioritize, presenting a compelling substitute for specialty sugars in various applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Sugar Consumption Regulations & Health Campaigns | -1.0% | North America, Europe, Australia | Short-to-Mid-term (2025-2030) |

| Volatility in Raw Material Prices (Sugarcane, Sugar Beet) | -0.7% | Global | Short-term (2025-2027) |

| Competition from Low-Calorie & Artificial Sweeteners | -0.9% | Global | Mid-to-Long-term (2026-2033) |

| High Production Costs of Specialty Sugars | -0.4% | Global | Short-to-Mid-term (2025-2029) |

Specialty Sugar Market Opportunities Analysis

The Specialty Sugar Market is ripe with numerous opportunities for growth and innovation, driven by evolving consumer demands and technological advancements. One significant area of opportunity lies in the continuous innovation and development of novel functional sugars. As consumers increasingly seek ingredients that offer specific health benefits beyond basic nutrition, there is a strong demand for specialty sugars that can provide attributes like prebiotic effects, lower glycemic index, or enhanced mineral content. Research and development efforts focused on creating these advanced sugar varieties can unlock new market segments and applications, particularly in the health and wellness, and pharmaceutical sectors.

Emerging economies present vast untapped potential for market expansion. Countries in Asia Pacific, Latin America, and Africa are experiencing rapid urbanization, rising disposable incomes, and a growing middle class, leading to increased consumption of processed foods, premium beverages, and diverse culinary products. As these regions adopt more sophisticated consumer tastes and become more exposed to global food trends, the demand for specialty sugars is expected to surge. Strategic market entry and localized product offerings tailored to regional preferences can capitalize on this burgeoning demand. Furthermore, the increasing global emphasis on sustainability and ethical sourcing provides a unique opportunity for producers to differentiate their products. Implementing sustainable agricultural practices, fair trade initiatives, and transparent supply chains can resonate strongly with environmentally conscious consumers and command premium pricing, establishing a competitive advantage in the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Functional Sugars | +1.5% | North America, Europe, Japan | Mid-to-Long-term (2027-2033) |

| Untapped Potential in Emerging Economies | +1.3% | Asia Pacific (China, India), Latin America | Long-term (2028-2033) |

| Focus on Sustainable and Ethical Sourcing | +0.9% | Global, particularly Europe, North America | Mid-to-Long-term (2026-2033) |

| Increasing Applications in Non-Food Industries | +0.6% | Global | Mid-term (2026-2030) |

Specialty Sugar Market Challenges Impact Analysis

The Specialty Sugar Market faces several significant challenges that could affect its growth trajectory and operational efficiency. One of the primary concerns is the potential for supply chain disruptions, which can arise from various factors including extreme weather events, pest outbreaks, geopolitical conflicts, or global health crises. Such disruptions can severely impact the availability of raw materials like sugarcane and sugar beet, leading to production delays, increased costs, and ultimately, higher prices for end-consumers. The complex global nature of supply chains for agricultural commodities makes them particularly vulnerable to these external shocks, requiring robust risk management strategies from market participants.

Another persistent challenge is consumer perception, particularly the broad association of all sugars with negative health outcomes. Despite specialty sugars often being less processed or offering unique nutritional attributes, they still fall under the general 'sugar' umbrella, which is frequently targeted by public health campaigns. Educating consumers about the distinct benefits, origins, and processing methods of specialty sugars versus highly refined options is crucial but difficult and resource-intensive. Overcoming this generalized negative perception requires continuous marketing and public relations efforts to highlight the unique value proposition of specialty varieties. Furthermore, navigating the diverse and often complex international regulatory landscape poses a significant hurdle for companies operating globally. Varying standards for food labeling, ingredient definitions, import/export duties, and health claims across different countries necessitate substantial compliance efforts and can limit market access or increase operational complexities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions & Geopolitical Instability | -0.8% | Global | Short-term (2025-2026) |

| Educating Consumers on Specialty Sugar Benefits | -0.5% | Global | Mid-term (2026-2030) |

| Navigating Diverse International Regulations | -0.4% | Global | Long-term (2028-2033) |

| Maintaining Cost-Effectiveness in Production | -0.3% | Global | Short-to-Mid-term (2025-2029) |

Specialty Sugar Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Specialty Sugar Market, covering its current size, historical trends, and future growth projections from 2025 to 2033. The report meticulously examines market dynamics, including key drivers, restraints, opportunities, and challenges, offering strategic insights for stakeholders. It also includes a detailed segmentation analysis by type, application, form, and source, along with a regional outlook highlighting key growth hotspots and market opportunities across major geographical areas. Furthermore, the report profiles leading market players, assessing their strategies, product portfolios, and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | 4.8 Billion USD |

| Market Forecast in 2033 | 8.0 Billion USD |

| Growth Rate | 6.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Suedzucker AG, Nordzucker AG, American Crystal Sugar Company, Cargill, Inc., Louis Dreyfus Company, Tereos S.A., Cosun Beet Company, Mitr Phol Group, Raízen S.A., Bunge Limited, Associated British Foods plc (AB Sugar), Wilmar International Ltd., EID Parry (India) Limited, Dalmia Bharat Sugar and Industries Ltd., Dhampur Sugar Mills Ltd., Balrampur Chini Mills Ltd., Tate & Lyle PLC, Ingredion Incorporated, The Hain Celestial Group, NOW Foods |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Specialty Sugar Market is comprehensively segmented to provide a granular understanding of its diverse components and their respective contributions to overall market growth. These segments highlight distinct product categories, end-use industries, physical forms, and raw material origins, each exhibiting unique market dynamics and growth potentials. The segmentation allows for a detailed analysis of specific consumer preferences and industrial requirements, informing targeted marketing strategies and product development efforts within the market.

Analyzing the market across these dimensions reveals key areas of innovation and demand. For instance, the 'By Type' segment differentiates between various processing levels and forms of specialty sugars, from liquid syrups to highly refined granulated options, each serving specific functional roles in food manufacturing. The 'By Application' segment underscores the versatility of specialty sugars, showcasing their crucial roles not only in traditional food and beverage formulations but also in expanding non-food industries like pharmaceuticals and personal care, driven by their purity and functional attributes. This multi-dimensional segmentation is critical for stakeholders to identify high-growth niches and tailor their offerings to precise market needs, facilitating strategic decision-making and optimizing resource allocation across the value chain.

- By Type:

- Liquid Sugar (Invert Sugar, Molasses, Syrups, etc.)

- Powdered Sugar (Icing Sugar, Confectioners' Sugar, etc.)

- Granulated Sugar (Turbinado, Demerara, Muscovado, Brown Sugar, etc.)

- Others (Coconut Sugar, Date Sugar, Maple Sugar, etc.)

- By Application:

- Food & Beverages (Bakery & Confectionery, Dairy & Frozen Desserts, Beverages, Snacks, Processed Foods, etc.)

- Pharmaceuticals & Nutraceuticals

- Personal Care & Cosmetics

- Others (Animal Feed, Industrial Applications)

- By Form:

- Crystalline

- Liquid

- Syrup

- By Source:

- Sugarcane

- Sugar Beet

- Fruits

- Palm

- Others

Regional Highlights

- North America: This region is a significant market for specialty sugars, driven by a strong consumer focus on health and wellness, clean label ingredients, and the growing demand for natural and organic food products. The robust food and beverage industry, coupled with increasing awareness of diversified sugar options, fuels market expansion.

- Europe: Europe represents another key market, characterized by stringent food safety regulations and a high demand for sustainable and ethically sourced ingredients. Innovation in functional foods and a preference for authentic, artisanal products contribute to the uptake of specialty sugars.

- Asia Pacific (APAC): Expected to exhibit the fastest growth, the APAC region is propelled by rapid urbanization, rising disposable incomes, and changing dietary patterns. The expanding food processing sector, coupled with a growing consumer base seeking premium and diverse food ingredients, makes this region a crucial growth hub. Countries like China and India are major contributors.

- Latin America: This region is witnessing steady growth, largely due to the increasing adoption of Western dietary trends and the expansion of the processed food and beverage industry. Traditional sugar-producing countries are exploring new avenues for specialty sugar production and export.

- Middle East and Africa (MEA): The MEA market is an emerging growth area for specialty sugars, driven by improving economic conditions, a growing young population, and increasing awareness of healthier food alternatives. Investment in food processing infrastructure is also contributing to market development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Specialty Sugar Market.- Suedzucker AG

- Nordzucker AG

- American Crystal Sugar Company

- Cargill, Inc.

- Louis Dreyfus Company

- Tereos S.A.

- Cosun Beet Company

- Mitr Phol Group

- Raízen S.A.

- Bunge Limited

- Associated British Foods plc (AB Sugar)

- Wilmar International Ltd.

- EID Parry (India) Limited

- Dalmia Bharat Sugar and Industries Ltd.

- Dhampur Sugar Mills Ltd.

- Balrampur Chini Mills Ltd.

- Tate & Lyle PLC

- Ingredion Incorporated

- The Hain Celestial Group

- NOW Foods

Frequently Asked Questions

What are the primary growth drivers for the Specialty Sugar Market?

The primary growth drivers include increasing consumer health consciousness, a rising demand for natural and clean label ingredients, and the expanding application of specialty sugars across various food, beverage, pharmaceutical, and personal care industries. Unique functional properties and diverse flavor profiles also contribute significantly.

How does consumer preference impact the Specialty Sugar Market?

Consumer preference profoundly impacts the market by shifting demand towards less processed, natural, and healthier sugar alternatives. This drives innovation in specialty sugar production and encourages manufacturers to focus on transparency in sourcing and processing to meet evolving consumer expectations for clean label products.

What role do natural and clean label trends play in Specialty Sugar?

Natural and clean label trends are central to the Specialty Sugar Market, as consumers increasingly seek products with simple, recognizable ingredients. This preference positions specialty sugars, often perceived as more natural and less refined, as desirable alternatives to conventional or artificial sweeteners, driving their adoption and market growth.

Which regions are expected to exhibit significant growth in Specialty Sugar?

Asia Pacific is projected to show the most significant growth due to rapid urbanization, rising disposable incomes, and a burgeoning food processing industry. North America and Europe will also maintain strong positions, driven by established health and wellness trends and an emphasis on premium, natural ingredients.

What challenges does the Specialty Sugar Market face?

Key challenges include stringent global regulations and health campaigns discouraging overall sugar consumption, volatility in raw material prices, and intense competition from a growing array of low-calorie and artificial sweeteners. Educating consumers about the distinct benefits of specialty sugars also remains a significant hurdle.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted