Solar Photovoltaic Glass Market

Solar Photovoltaic Glass Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709849 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

Solar Photovoltaic Glass Market Size

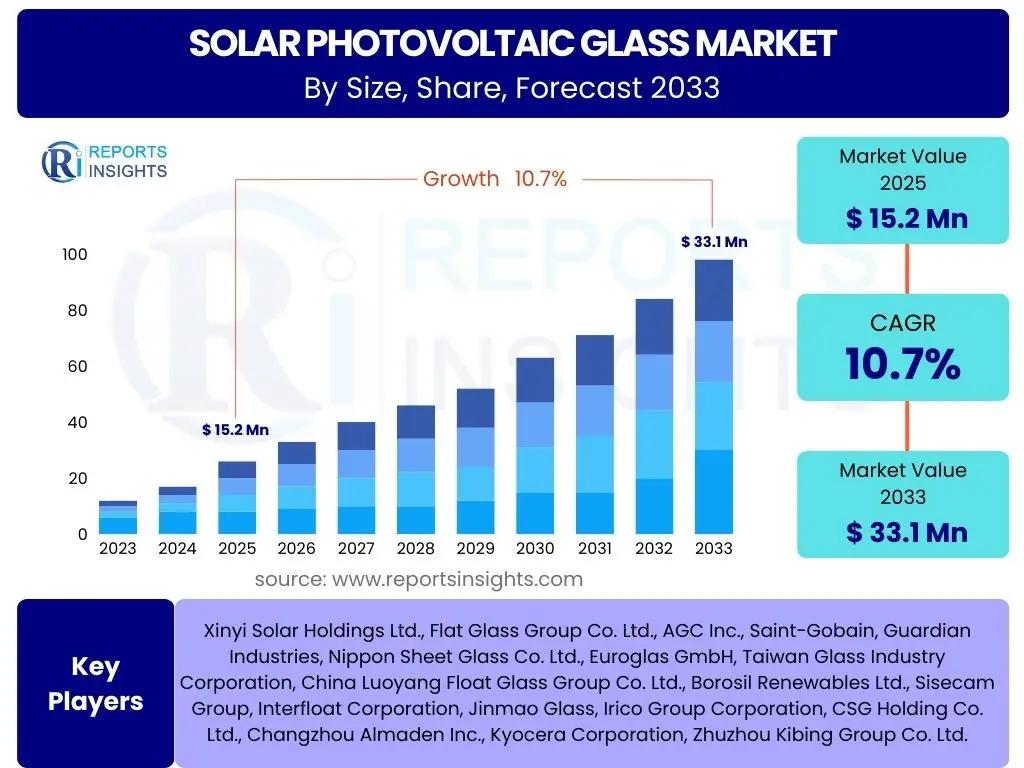

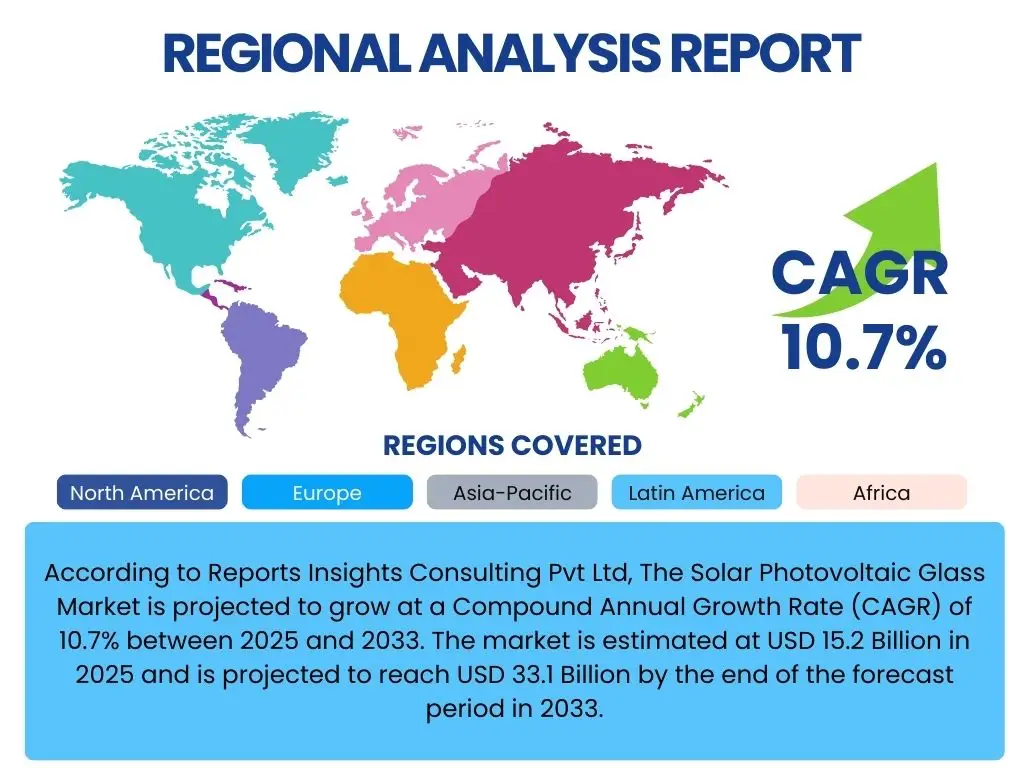

According to Reports Insights Consulting Pvt Ltd, The Solar Photovoltaic Glass Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.7% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 33.1 Billion by the end of the forecast period in 2033.

Key Solar Photovoltaic Glass Market Trends & Insights

The Solar Photovoltaic Glass market is witnessing significant evolution driven by technological advancements and increasing global demand for renewable energy. User inquiries frequently highlight the rising adoption of advanced glass types, such as anti-reflective and bifacial glass, which enhance module efficiency and overall power output. There is also a keen interest in integrated solar solutions, where PV glass blends seamlessly into architectural designs and automotive applications, moving beyond traditional rooftop installations.

Furthermore, the market is influenced by the push for sustainable manufacturing practices, with a focus on reducing the carbon footprint of glass production and improving recyclability. Innovations in material science are leading to lighter, more durable, and more aesthetically pleasing PV glass options. The convergence of these trends suggests a market poised for continued expansion, characterized by efficiency improvements, integration versatility, and environmental consciousness, catering to a broader range of applications and consumer preferences.

- Increasing demand for high-efficiency bifacial solar modules, driving demand for specialized glass.

- Growing adoption of Building-Integrated Photovoltaics (BIPV) and transparent solar glass for architectural aesthetics and energy generation.

- Technological advancements in anti-reflective and anti-soiling coatings to enhance light transmission and reduce maintenance.

- Emphasis on lightweight and flexible PV glass solutions for diverse applications, including automotive and portable devices.

- Development of sustainable and recyclable glass materials to reduce environmental impact.

AI Impact Analysis on Solar Photovoltaic Glass

The integration of Artificial Intelligence (AI) in the Solar Photovoltaic Glass sector is a growing area of interest, with user questions frequently addressing its potential to revolutionize manufacturing, quality control, and product innovation. AI is expected to optimize production processes by predicting equipment failures, fine-tuning material mixtures for desired properties, and automating complex inspection tasks, thereby reducing waste and improving output consistency. This includes sophisticated analytics for raw material sourcing and inventory management, ensuring a more resilient supply chain.

Beyond manufacturing, AI holds promise in accelerating the research and development of new glass formulations, such as those with improved light absorption or enhanced durability, through advanced material design simulations. Furthermore, AI-driven solutions can analyze performance data from installed PV modules, identifying patterns of degradation in glass or coatings and recommending proactive maintenance strategies. This comprehensive application of AI is anticipated to drive down costs, shorten innovation cycles, and significantly enhance the reliability and performance of solar photovoltaic glass products.

- AI-driven optimization of manufacturing processes for increased efficiency and reduced material waste.

- Enhanced quality control through AI-powered visual inspection systems, identifying microscopic flaws in glass.

- Predictive maintenance for glass manufacturing equipment, minimizing downtime and operational costs.

- Accelerated material research and development using AI for new PV glass compositions and coatings.

- Supply chain optimization and demand forecasting for raw materials through AI analytics.

Key Takeaways Solar Photovoltaic Glass Market Size & Forecast

User inquiries into the Solar Photovoltaic Glass market size and forecast consistently seek clarity on the primary drivers of growth and the long-term sustainability of the industry. A central takeaway is the robust growth trajectory, fueled by global renewable energy targets and declining solar power generation costs, making solar an increasingly attractive investment. The market's expansion is not merely quantitative but also qualitative, with a clear shift towards advanced glass technologies that offer superior performance and integration capabilities, which will be crucial for meeting future energy demands efficiently.

Another significant takeaway is the increasing diversification of applications for PV glass, moving beyond conventional utility-scale projects to encompass Building-Integrated Photovoltaics (BIPV), transparent solar windows, and even automotive sectors. This broadening scope, coupled with ongoing innovations in glass properties like anti-reflectivity and bifacial functionality, underscores the market's resilience and adaptability. The forecast indicates sustained expansion, positioning solar photovoltaic glass as a critical component in the global energy transition, underpinned by technological advancements and supportive policy frameworks.

- The market is poised for substantial growth, driven by global renewable energy initiatives and policy support.

- Technological innovations in glass coatings and structures are key to enhancing PV module efficiency and market penetration.

- BIPV and transparent PV glass represent significant growth avenues, integrating solar technology into diverse urban and architectural landscapes.

- Asia Pacific will remain a dominant region, driven by large-scale solar installations and manufacturing capabilities.

- Sustainable manufacturing practices and recyclability are becoming increasingly critical for market competitiveness and environmental compliance.

Solar Photovoltaic Glass Market Drivers Analysis

The Solar Photovoltaic Glass market is primarily propelled by the global shift towards renewable energy sources and supportive governmental policies aimed at reducing carbon emissions. Increasing awareness regarding climate change, coupled with the decreasing cost of solar power generation, has made photovoltaic systems a highly attractive alternative to traditional fossil fuels. This surge in demand for solar energy directly translates into a heightened need for high-quality, efficient PV glass, which is a fundamental component of solar panels.

Furthermore, advancements in solar cell technology, such as the rise of bifacial modules and thin-film technologies, necessitate specialized glass that can optimize performance and durability. Innovations in glass coatings, such as anti-reflective and anti-soiling layers, further enhance light transmission and reduce maintenance, thereby increasing the overall efficiency and lifespan of solar panels. These technological improvements, combined with substantial investments in solar infrastructure across residential, commercial, and utility-scale projects, continue to drive market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Renewable Energy Targets & Government Incentives | +3.5% | Europe, North America, Asia Pacific (China, India) | Long-term (2025-2033) |

| Declining Cost of Solar Power Generation | +2.8% | Global | Mid to Long-term (2025-2033) |

| Technological Advancements in PV Modules (e.g., Bifacial) | +2.2% | Asia Pacific, Europe, North America | Mid-term (2025-2030) |

| Growing Demand for Building-Integrated Photovoltaics (BIPV) | +1.5% | Europe, North America, Japan | Long-term (2027-2033) |

Solar Photovoltaic Glass Market Restraints Analysis

Despite the robust growth of the solar energy sector, the Solar Photovoltaic Glass market faces several significant restraints that could impede its trajectory. One primary concern is the volatility in raw material prices, particularly for silica and soda ash, which are essential components of glass manufacturing. Fluctuations in these costs can directly impact the production expenses of PV glass, thereby affecting pricing strategies and overall market competitiveness, potentially slowing adoption rates, especially in cost-sensitive markets.

Furthermore, the high capital expenditure required for establishing and upgrading advanced glass manufacturing facilities acts as a barrier to entry for new players and limits the expansion capabilities of existing ones. This substantial initial investment, coupled with the energy-intensive nature of glass production, contributes to higher operational costs. Additionally, trade protectionism and tariffs on imported solar components in various regions can disrupt supply chains, increase costs for manufacturers, and reduce the affordability of solar installations, collectively posing a challenge to the market's consistent growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Silica, Soda Ash) | -1.8% | Global | Short to Mid-term (2025-2028) |

| High Initial Investment & Production Costs | -1.5% | Emerging Economies, Europe | Long-term (2025-2033) |

| Trade Protectionism & Tariffs on Solar Components | -1.2% | North America, Europe, India | Mid-term (2025-2030) |

| Supply Chain Disruptions & Geopolitical Tensions | -1.0% | Global | Short-term (2025-2026) |

Solar Photovoltaic Glass Market Opportunities Analysis

The Solar Photovoltaic Glass market is presented with numerous opportunities for expansion, largely driven by the continuous innovation in product development and the broadening scope of solar applications. The emergence of transparent PV glass and flexible substrates offers significant potential, enabling solar energy generation in previously unfeasible areas such as windows, facades, and curved surfaces. This creates new markets in the construction and automotive industries, moving beyond traditional rooftop installations and integrating solar technology seamlessly into everyday environments.

Furthermore, the increasing global focus on energy storage solutions, coupled with the drive for energy independence, provides an indirect but powerful opportunity for the PV glass sector. As solar power generation becomes more ubiquitous, the demand for efficient and durable solar modules, and by extension, the specialized glass they require, will intensify. Emerging economies, particularly in Asia Pacific and Africa, with their rapidly growing energy needs and abundant solar resources, represent untapped markets with substantial potential for large-scale solar installations and the associated demand for PV glass components.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Transparent & Flexible PV Glass | +2.5% | Global, particularly developed markets | Mid to Long-term (2026-2033) |

| Growing Demand for Building-Integrated Photovoltaics (BIPV) | +2.0% | Europe, North America, Japan | Long-term (2027-2033) |

| Expansion in Emerging Economies (Asia Pacific, Africa) | +1.8% | China, India, Southeast Asia, Sub-Saharan Africa | Long-term (2025-2033) |

| Synergy with Energy Storage Solutions & Smart Grids | +1.0% | Global | Mid to Long-term (2026-2033) |

Solar Photovoltaic Glass Market Challenges Impact Analysis

The Solar Photovoltaic Glass market confronts several operational and environmental challenges that demand innovative solutions. One significant challenge pertains to the recycling and disposal of end-of-life solar panels, which contain specialized glass. As the volume of installed solar capacity grows, managing the waste stream effectively and developing cost-efficient recycling technologies for PV glass becomes paramount to maintaining the industry's sustainability credentials and reducing environmental impact. Inadequate infrastructure for recycling can lead to environmental concerns and missed opportunities for resource recovery.

Another key challenge involves the intense global competition among PV glass manufacturers, which often leads to price wars and puts pressure on profit margins. This competitive environment necessitates continuous innovation and cost reduction strategies, which can be difficult to sustain while maintaining high product quality and performance standards. Furthermore, regulatory hurdles, complex permitting processes for solar projects, and rapidly evolving trade policies can create uncertainty for manufacturers and project developers, impacting investment decisions and market stability. Overcoming these challenges will be crucial for the sustained growth and long-term viability of the solar photovoltaic glass sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Recycling and Disposal of End-of-Life PV Modules | -1.5% | Europe, North America, Japan | Mid to Long-term (2028-2033) |

| Intense Global Competition & Price Erosion | -1.3% | Asia Pacific (China), Global | Short to Mid-term (2025-2030) |

| Maintaining Quality & Performance with Cost Pressures | -1.0% | Global | Long-term (2025-2033) |

| Regulatory Hurdles & Evolving Trade Policies | -0.8% | North America, Europe, India | Short to Mid-term (2025-2028) |

Solar Photovoltaic Glass Market - Updated Report Scope

This report offers a comprehensive analysis of the Solar Photovoltaic Glass Market, providing in-depth insights into market size, growth trends, key drivers, restraints, opportunities, and competitive landscape. It segments the market based on glass type, application, and end-use, further dissecting regional dynamics. The report incorporates an impact analysis of Artificial Intelligence and addresses the latest technological advancements influencing market evolution and future outlook.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 33.1 Billion |

| Growth Rate | 10.7% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Xinyi Solar Holdings Ltd., Flat Glass Group Co. Ltd., AGC Inc., Saint-Gobain, Guardian Industries, Nippon Sheet Glass Co. Ltd., Euroglas GmbH, Taiwan Glass Industry Corporation, China Luoyang Float Glass Group Co. Ltd., Borosil Renewables Ltd., Sisecam Group, Interfloat Corporation, Jinmao Glass, Irico Group Corporation, CSG Holding Co. Ltd., Changzhou Almaden Inc., Kyocera Corporation, Zhuzhou Kibing Group Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Solar Photovoltaic Glass market is meticulously segmented to provide a detailed understanding of its diverse components and their respective growth trajectories. These segments help in identifying specific market niches, understanding technological preferences, and analyzing end-user adoption patterns. The segmentation by type, application, and end-use allows for a granular assessment of market dynamics, revealing key areas of innovation and investment across the global landscape.

- By Type:

- Tempered Glass: Standard robust glass for solar panels.

- Anti-Reflective Glass: Coated glass to maximize light transmission and efficiency.

- Transparent Conductive Oxide (TCO) Glass: Essential for thin-film solar cells.

- Bifacial Glass: Used in modules that capture sunlight from both sides, enhancing energy yield.

- Others: Includes specialized ultra-clear glass for specific applications.

- By Application:

- Crystalline Silicon PV Modules: Dominant technology, including monocrystalline for high efficiency and polycrystalline for cost-effectiveness.

- Thin-Film PV Modules: Emerging technologies like Cadmium Telluride (CdTe), Copper Indium Gallium Selenide (CIGS), and Amorphous Silicon (a-Si) requiring specific glass properties.

- By End-Use:

- Residential: Rooftop installations for homes.

- Commercial: Solar panels on businesses and public buildings.

- Industrial: Large-scale installations for industrial power needs.

- Utility-Scale: Massive solar farms for grid power generation.

- Automotive: Integration of PV glass into vehicles for range extension or auxiliary power.

- Others: Includes portable solar chargers and specialized off-grid applications.

Regional Highlights

- Asia Pacific: The largest and fastest-growing market, driven by massive solar capacity installations in China and India, extensive manufacturing capabilities, and government support for renewable energy projects. Countries like Vietnam, Australia, and Japan are also making significant contributions.

- Europe: A mature market with strong emphasis on BIPV, sustainable energy policies, and technological innovation. Germany, Spain, and Italy are leading the adoption of advanced PV glass and solar solutions, pushing for energy independence and decarbonization targets.

- North America: Experiencing robust growth due to favorable government incentives, increasing demand for residential and commercial solar, and investments in large-scale utility projects in the United States and Canada. Focus on domestic manufacturing and advanced PV technologies.

- Latin America: An emerging market with significant solar potential, particularly in countries like Brazil, Chile, and Mexico, driven by energy demand and abundant solar resources. Investments in utility-scale projects are increasing, though regulatory frameworks can pose challenges.

- Middle East and Africa (MEA): Demonstrating strong growth potential, especially in countries like UAE, Saudi Arabia, and South Africa, fueled by ambitious renewable energy targets, large desert areas suitable for solar farms, and initiatives to diversify energy sources away from fossil fuels.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Solar Photovoltaic Glass Market.- Xinyi Solar Holdings Ltd.

- Flat Glass Group Co. Ltd.

- AGC Inc.

- Saint-Gobain

- Guardian Industries

- Nippon Sheet Glass Co. Ltd.

- Euroglas GmbH

- Taiwan Glass Industry Corporation

- China Luoyang Float Glass Group Co. Ltd.

- Borosil Renewables Ltd.

- Sisecam Group

- Interfloat Corporation

- Jinmao Glass

- Irico Group Corporation

- CSG Holding Co. Ltd.

- Changzhou Almaden Inc.

- Kyocera Corporation

- Zhuzhou Kibing Group Co. Ltd.

Frequently Asked Questions

What types of glass are used in solar panels?

Solar panels primarily use tempered glass for durability and protection. Specialized types include anti-reflective glass to increase light absorption, Transparent Conductive Oxide (TCO) glass for thin-film modules, and bifacial glass for modules that capture light from both sides.

How do anti-reflective coatings improve solar panel efficiency?

Anti-reflective (AR) coatings reduce light reflection from the glass surface, allowing more sunlight to penetrate the solar cells. This increased light transmission directly translates to higher energy conversion efficiency and greater power output from the solar panel.

What is Building-Integrated Photovoltaics (BIPV) and its relevance to PV glass?

BIPV involves integrating solar photovoltaic materials directly into building architectural elements like facades, roofs, or windows. PV glass is crucial for BIPV, enabling solar panels to serve as structural or aesthetic components, generating electricity while blending seamlessly with building design.

Which region dominates the Solar Photovoltaic Glass market?

The Asia Pacific region currently dominates the Solar Photovoltaic Glass market, primarily due to large-scale solar project installations, extensive manufacturing capacities in countries like China and India, and strong governmental support for renewable energy initiatives.

What are the key drivers for the growth of the Solar Photovoltaic Glass market?

Key drivers include global renewable energy targets, declining costs of solar power generation, supportive government incentives, and technological advancements in PV modules such as bifacial and thin-film technologies that require high-performance glass.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted