Smartphone Cover Glass Market

Smartphone Cover Glass Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703124 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

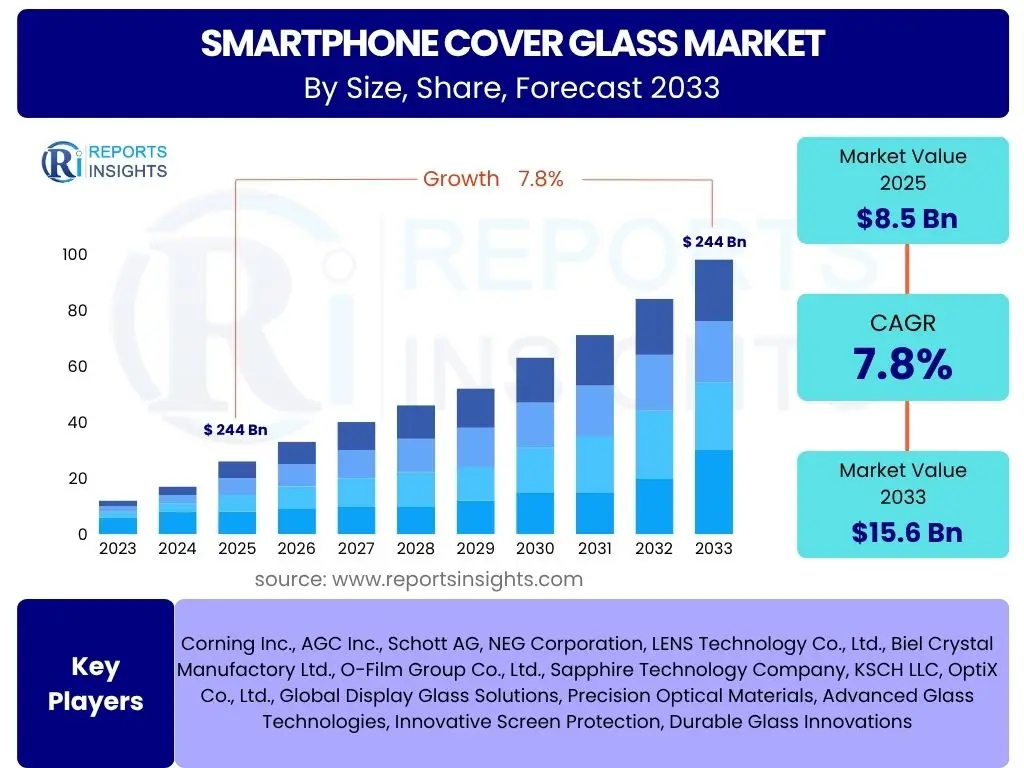

Smartphone Cover Glass Market Size

According to Reports Insights Consulting Pvt Ltd, The Smartphone Cover Glass Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 8.5 billion in 2025 and is projected to reach USD 15.6 billion by the end of the forecast period in 2033.

Key Smartphone Cover Glass Market Trends & Insights

The smartphone cover glass market is experiencing significant evolution, driven by advancements in material science and consumer demand for enhanced durability and aesthetics. Current trends indicate a strong shift towards ultra-thin, lightweight, and highly durable glass solutions that can withstand greater impact and scratches. Furthermore, the integration of advanced functionalities such as haptic feedback layers and integrated sensor technology directly into the cover glass is emerging as a critical differentiator, moving beyond mere protection to become an integral part of the user interface. The increasing adoption of foldable and flexible display technologies also necessitates innovative cover glass materials that can bend and flex without compromising structural integrity or optical clarity, pushing manufacturers to explore novel compositions and manufacturing processes.

Another prominent trend involves the growing emphasis on sustainable manufacturing practices and the development of eco-friendly glass materials. Consumers and regulatory bodies are increasingly demanding products with a reduced environmental footprint, leading to research and development into recycled content, lower energy consumption during production, and the elimination of hazardous substances. Anti-glare and anti-fingerprint coatings continue to be refined, improving user experience, while aesthetic trends like frosted glass and customizable finishes are gaining traction, allowing for greater device personalization. These multifaceted trends collectively shape the market, requiring constant innovation from material suppliers and smartphone manufacturers to meet evolving consumer expectations and technological demands.

- Increased demand for ultra-durable and scratch-resistant glass.

- Rising adoption of flexible and foldable cover glass for new form factors.

- Integration of advanced haptic and sensor technologies within the glass.

- Growing focus on sustainable and eco-friendly manufacturing processes.

- Advancements in anti-glare, anti-fingerprint, and privacy screen coatings.

- Emergence of customizable aesthetic finishes such as frosted and colored glass.

- Development of thinner and lighter glass designs for enhanced device ergonomics.

AI Impact Analysis on Smartphone Cover Glass

Artificial intelligence is poised to significantly transform various facets of the smartphone cover glass industry, primarily by enhancing manufacturing efficiency, quality control, and the potential for personalized user experiences. AI-driven vision systems can meticulously inspect glass surfaces for microscopic defects with unprecedented speed and accuracy, far surpassing human capabilities and reducing scrap rates. Predictive maintenance algorithms, powered by AI, can analyze equipment performance data to anticipate potential failures in the highly complex glass manufacturing machinery, minimizing downtime and optimizing production flows. This leads to higher yields, lower operational costs, and consistent product quality, which are critical competitive advantages in a volume-driven market.

Beyond manufacturing, AI holds promise for material innovation and design optimization. Machine learning algorithms can analyze vast datasets of material properties and performance characteristics, accelerating the discovery and development of new glass compositions with superior strength, flexibility, or optical properties. AI could also facilitate the design of adaptive cover glass features that respond to user behavior or environmental conditions, though this is a more long-term prospect. Furthermore, in the realm of supply chain management, AI can optimize logistics, predict demand fluctuations more accurately, and ensure a stable supply of raw materials, contributing to greater market stability and efficiency across the entire value chain for smartphone cover glass.

- Enhanced quality control through AI-powered defect detection systems.

- Optimized manufacturing processes via predictive maintenance and AI-driven robotics.

- Accelerated material discovery and development using machine learning algorithms.

- Improved supply chain efficiency and demand forecasting through AI analytics.

- Potential for personalized and adaptive cover glass functionalities in the future.

- Reduced production waste and improved resource utilization.

Key Takeaways Smartphone Cover Glass Market Size & Forecast

The smartphone cover glass market is set for robust growth, driven by an increasing global smartphone penetration, continuous innovation in display technologies, and the rising consumer demand for premium, durable devices. The forecast period indicates a steady expansion, primarily fueled by the replacement cycle of existing smartphones and the introduction of new form factors that require specialized glass solutions. Market participants should focus on developing advanced material science capabilities to meet the evolving requirements for strength, flexibility, and optical clarity, which are becoming paramount for modern smartphone designs. Strategic partnerships across the value chain, from raw material suppliers to device manufacturers, will be crucial for capitalizing on emerging opportunities and mitigating potential supply chain disruptions.

A significant takeaway is the strong emphasis on balancing performance with cost-effectiveness, as manufacturers seek to differentiate their products in a highly competitive landscape. Companies that can innovate in manufacturing processes to reduce production costs while maintaining high quality will gain a substantial edge. Furthermore, the sustainability aspect is gaining increasing importance, making eco-friendly material development and responsible manufacturing practices a key competitive differentiator. Overall, the market's trajectory points towards a future where cover glass is not merely a protective layer but an integral, technologically advanced component that enhances user experience and device functionality, demanding continuous investment in research and development to maintain market relevance.

- Consistent market growth projected through 2033, driven by smartphone adoption and technological advancements.

- Emphasis on high durability, thinness, and flexible solutions for new device designs.

- Strategic importance of material science innovation and sustainable manufacturing.

- Necessity for cost-effective production methods to remain competitive.

- Collaboration across the supply chain is vital for resilience and innovation.

- Cover glass transitioning from a protective layer to an active, integrated component.

Smartphone Cover Glass Market Drivers Analysis

The global smartphone cover glass market is primarily propelled by the unrelenting expansion of the smartphone industry itself, coupled with an increasing consumer expectation for premium device aesthetics and durability. As smartphones become indispensable tools for daily life, the demand for robust, scratch-resistant, and aesthetically pleasing cover glass solutions intensifies. Advancements in display technologies, such as higher resolution screens and edge-to-edge designs, necessitate increasingly sophisticated and high-performance glass, directly driving innovation and adoption in this market segment. Moreover, the accelerating replacement cycles for smartphones, fueled by technological upgrades and evolving consumer preferences, ensure a consistent demand for new devices and, consequently, for advanced cover glass.

The emergence of new smartphone form factors, including foldable phones, bendable screens, and devices with multiple displays, is creating entirely new avenues for cover glass innovation. These form factors require ultra-thin, highly flexible, and durable glass that can withstand repeated bending without compromising optical integrity or physical strength. This pushes manufacturers to invest heavily in research and development, leading to breakthrough materials and processing techniques. Furthermore, the rising disposable incomes in emerging economies are expanding the consumer base for smartphones, particularly for mid-range and high-end models, which typically feature advanced cover glass, thereby contributing significantly to overall market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Smartphone Penetration | +2.5% | Asia Pacific, Africa, Latin America | 2025-2033 |

| Rising Demand for Premium & Durable Smartphones | +1.8% | North America, Europe, Asia Pacific | 2025-2033 |

| Advancements in Display Technologies (e.g., Foldable, Edge-to-Edge) | +1.5% | Global | 2026-2033 |

| Frequent Smartphone Replacement Cycles | +1.0% | North America, Europe, Asia Pacific | 2025-2030 |

| Growth in Disposable Income in Emerging Markets | +0.8% | China, India, Southeast Asia | 2025-2033 |

Smartphone Cover Glass Market Restraints Analysis

Despite robust growth prospects, the smartphone cover glass market faces several significant restraints that could impede its expansion. One primary concern is the relatively high cost of advanced glass materials and the complex manufacturing processes involved, which can contribute to higher overall smartphone production costs. This cost factor can be particularly impactful in price-sensitive markets, limiting the adoption of premium glass solutions in budget-friendly smartphone segments. Intense competition among glass manufacturers further pressures pricing, potentially compressing profit margins for market players and discouraging investment in highly speculative or expensive R&D. The demand for increasingly thinner and lighter glass also introduces manufacturing complexities and potentially higher defect rates, adding to production challenges and costs.

Another key restraint is the inherent fragility of glass, despite advancements in strengthening technologies. While modern cover glass is significantly more durable, it remains susceptible to breakage under severe impact, leading to consumer dissatisfaction and the need for replacements. This fragility can slow down the adoption of novel designs that might expose more glass surface area, such as all-glass bodies. Furthermore, geopolitical tensions and trade disputes can disrupt global supply chains for essential raw materials used in glass production, leading to material shortages or price volatility. Regulatory complexities and environmental concerns related to glass manufacturing and disposal also present ongoing challenges, necessitating continuous compliance and adaptation by industry participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Advanced Glass | -1.2% | Global, particularly emerging markets | 2025-2033 |

| Intense Price Competition Among Manufacturers | -0.9% | Global | 2025-2030 |

| Inherent Fragility & Breakage Susceptibility | -0.7% | Global | 2025-2033 |

| Supply Chain Disruptions & Raw Material Volatility | -0.6% | Asia Pacific, Europe (dependent on origin) | 2025-2028 |

| Complexities of Ultra-Thin Glass Production | -0.5% | Global | 2025-2033 |

Smartphone Cover Glass Market Opportunities Analysis

Significant opportunities are emerging in the smartphone cover glass market, primarily driven by the continuous evolution of smartphone design and functionality. The proliferation of innovative form factors, such as foldable, rollable, and extendable smartphones, presents a substantial growth avenue for companies capable of developing ultra-thin, flexible, and highly durable cover glass. These next-generation devices require entirely new material properties and manufacturing techniques, offering a competitive advantage to early innovators. Furthermore, the increasing integration of advanced features directly into the cover glass, such as in-display fingerprint sensors, under-display cameras, and sophisticated haptic feedback layers, expands the functional role of cover glass beyond simple protection, creating new value propositions and revenue streams for manufacturers.

Beyond traditional smartphone applications, the development of augmented reality (AR) and virtual reality (VR) technologies, often reliant on smartphone connectivity, offers a synergistic growth opportunity. AR/VR headsets and smart glasses could utilize specialized cover glass with enhanced optical properties and protective layers, potentially opening up new market segments. Additionally, the growing consumer awareness and demand for sustainable products are creating opportunities for manufacturers to develop and market eco-friendly cover glass solutions, including those made from recycled materials or produced with reduced environmental impact. Investment in R&D for self-healing coatings and improved anti-reflective properties also represents a fertile ground for innovation, promising enhanced user experience and product longevity, thereby stimulating consumer upgrades and new market demand.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Foldable and Flexible Smartphone Designs | +1.8% | Global, particularly North America, Asia Pacific | 2026-2033 |

| Integration of Advanced In-Display Technologies | +1.5% | Global | 2025-2033 |

| Development of Sustainable & Recyclable Glass Solutions | +1.0% | Europe, North America, East Asia | 2027-2033 |

| Expansion into AR/VR Devices & Smart Wearables | +0.8% | North America, Europe, Asia Pacific | 2028-2033 |

| Advancements in Self-Healing & Anti-Reflective Coatings | +0.7% | Global | 2025-2033 |

Smartphone Cover Glass Market Challenges Impact Analysis

The smartphone cover glass market faces several inherent challenges that demand continuous innovation and strategic adaptation from industry players. One significant challenge is the ongoing quest to balance extreme durability with increasing thinness and lightness, as consumer demand for slim, elegant devices often conflicts with the need for robust protection. Achieving this balance requires significant material science breakthroughs and highly precise manufacturing techniques, which can be capital-intensive and time-consuming. Furthermore, the rapid pace of technological obsolescence in the smartphone industry means that cover glass manufacturers must constantly innovate to keep up with evolving design trends and functional requirements, leading to short product development cycles and high R&D expenditures.

Another major challenge revolves around managing the complexities of global supply chains. Raw materials for specialized glass often originate from specific regions, making the supply chain vulnerable to geopolitical tensions, trade restrictions, natural disasters, or logistical disruptions. This can lead to price volatility, material shortages, and delays in production. Intense competition, particularly from lower-cost manufacturers, also poses a challenge to established players, pressuring profit margins and requiring continuous efforts in process optimization and cost reduction. Environmental regulations regarding manufacturing emissions and waste disposal, coupled with the energy-intensive nature of glass production, present additional hurdles, pushing companies to invest in more sustainable and compliant operational practices, adding to overall operational costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing Durability with Thinness & Lightness | -1.0% | Global | 2025-2033 |

| Rapid Technological Obsolescence & Short Product Cycles | -0.8% | Global | 2025-2033 |

| Vulnerability of Global Supply Chains | -0.7% | Asia Pacific, Europe (manufacturing hubs) | 2025-2029 |

| Intense Price Pressure from Competition | -0.6% | Global | 2025-2033 |

| Meeting Stringent Environmental Regulations | -0.5% | Europe, North America, East Asia | 2025-2033 |

Smartphone Cover Glass Market - Updated Report Scope

This report provides an in-depth analysis of the global smartphone cover glass market, offering a comprehensive overview of its current landscape, historical performance, and future growth trajectories. The scope encompasses detailed market sizing, segmentation analysis by material, application, and end-use, and a thorough examination of key market dynamics including drivers, restraints, opportunities, and challenges. It also includes regional insights, competitive landscape analysis of leading industry players, and a forecast spanning from 2025 to 2033, providing actionable intelligence for stakeholders. The report aims to furnish businesses with strategic insights to navigate market complexities, identify lucrative growth avenues, and make informed investment decisions in this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 billion |

| Market Forecast in 2033 | USD 15.6 billion |

| Growth Rate | 7.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Corning Inc., AGC Inc., Schott AG, NEG Corporation, LENS Technology Co., Ltd., Biel Crystal Manufactory Ltd., O-Film Group Co., Ltd., Sapphire Technology Company, KSCH LLC, OptiX Co., Ltd., Global Display Glass Solutions, Precision Optical Materials, Advanced Glass Technologies, Innovative Screen Protection, Durable Glass Innovations |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The smartphone cover glass market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segmentations allow for a detailed analysis of market dynamics based on the specific material compositions, the various applications within a smartphone, the end-use categories of devices, and the underlying strengthening technologies employed. This structured approach helps in identifying high-growth areas, understanding consumer preferences for different types of glass, and recognizing the technological advancements driving innovation in each sub-segment. Such comprehensive segmentation is critical for stakeholders to tailor strategies, optimize product portfolios, and target specific market niches effectively.

By dissecting the market across these dimensions, the report offers valuable insights into how material science innovations, design trends, and manufacturing capabilities contribute to the overall market landscape. For instance, the transition from traditional aluminosilicate to lithium-aluminosilicate glass is a key trend in the material segment, driven by enhanced durability requirements. Similarly, the growing adoption of foldable phones is significantly impacting the end-use segment, necessitating flexible glass solutions. Understanding these intricate interdependencies across segments is essential for anticipating market shifts and maintaining a competitive edge in the highly dynamic smartphone cover glass industry.

- By Material:

- Alkali-Aluminosilicate Glass: Widely used for its balance of strength and cost-effectiveness.

- Lithium-Aluminosilicate Glass: Known for superior drop performance and flexibility, crucial for premium and foldable devices.

- Borosilicate Glass: Valued for thermal shock resistance and optical clarity, often used in specific components.

- Others: Includes specialized glass types and composites for niche applications.

- By Application:

- Front Cover: The primary protective layer for the main display, demanding high durability and clarity.

- Back Cover: Increasingly adopted for aesthetic appeal, wireless charging compatibility, and improved grip.

- Camera Lens Cover: Specialized glass offering high optical transparency and scratch resistance for camera protection.

- By End-Use:

- Standard Smartphones: Traditional rigid devices forming the largest segment.

- Foldable Smartphones: Emerging segment requiring ultra-thin and highly flexible glass.

- Rugged Smartphones: Devices designed for extreme conditions, needing enhanced impact resistance.

- Others: Includes smartwatches, tablets, and other portable devices using similar cover glass.

- By Technology:

- Chemically Strengthened Glass: Predominantly used due to its superior scratch and drop resistance achieved through ion exchange.

- Heat Strengthened Glass: Offers improved mechanical strength compared to untreated glass, used in specific applications.

- Untreated Glass: Basic glass used where cost is a primary consideration or less stringent durability is required.

Regional Highlights

The global smartphone cover glass market exhibits distinct regional dynamics, influenced by varying levels of smartphone penetration, manufacturing capabilities, and consumer purchasing power. Asia Pacific stands as the largest and fastest-growing market, primarily driven by the massive production capacities of smartphone manufacturers in countries like China, South Korea, and Taiwan, coupled with the immense consumer base in China and India. This region is a hub for innovation in display and glass technology, with significant investments in research and development for next-generation materials and production processes, especially for foldable and premium devices. The rapid urbanization and increasing disposable incomes further fuel the demand for advanced smartphones and, consequently, high-quality cover glass.

North America and Europe represent mature markets characterized by high adoption rates of premium and flagship smartphones, driving demand for advanced, durable, and aesthetically pleasing cover glass solutions. These regions are also at the forefront of adopting new technologies such as foldable phones and devices with integrated smart functionalities. Latin America and the Middle East & Africa (MEA) are emerging markets with significant growth potential, driven by increasing smartphone penetration and improving economic conditions. While these regions may still prioritize cost-effectiveness, the gradual shift towards higher-end devices is creating a growing demand for robust and visually appealing cover glass, leading to new opportunities for market expansion and strategic investments.

- Asia Pacific: Dominant market due to high smartphone manufacturing volume, large consumer base in China and India, and a hub for R&D in display technologies. Expected to maintain the highest growth rate.

- North America: Mature market with high demand for premium and flagship smartphones, driving innovation in durable and aesthetically advanced cover glass. Early adopter of new form factors.

- Europe: Similar to North America, characterized by high disposable income and strong consumer preference for quality and design, leading to consistent demand for advanced cover glass. Emphasis on sustainability also growing.

- Latin America: Emerging market with increasing smartphone penetration and a growing middle class, leading to expanding demand for mid-range to high-end devices and associated cover glass.

- Middle East & Africa (MEA): Rapidly expanding smartphone market, particularly in urban centers, presenting new opportunities for cover glass manufacturers as device adoption increases and consumer preferences shift towards more durable and feature-rich phones.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Smartphone Cover Glass Market.- Corning Inc.

- AGC Inc.

- Schott AG

- NEG Corporation

- LENS Technology Co., Ltd.

- Biel Crystal Manufactory Ltd.

- O-Film Group Co., Ltd.

- Sapphire Technology Company

- KSCH LLC

- OptiX Co., Ltd.

- Global Display Glass Solutions

- Precision Optical Materials

- Advanced Glass Technologies

- Innovative Screen Protection

- Durable Glass Innovations

Frequently Asked Questions

What is smartphone cover glass and why is it important?

Smartphone cover glass is the protective layer, typically made of specially engineered glass, that covers a smartphone's display and sometimes its back. It is crucial for protecting the delicate internal components from scratches, cracks, and impacts, while also enabling touch functionality and maintaining optical clarity for display viewing. Its importance has grown with the advent of larger, more immersive displays and the increasing aesthetic value of smartphone design.

How is smartphone cover glass made durable?

Smartphone cover glass achieves its durability primarily through chemical strengthening, a process where glass is immersed in a hot potassium salt solution. This causes smaller sodium ions in the glass surface to be replaced by larger potassium ions, creating a layer of compressive stress. This compressive layer makes the glass significantly more resistant to scratches and impacts compared to untreated glass.

What are the latest innovations in smartphone cover glass?

Recent innovations include the development of ultra-thin, flexible glass for foldable smartphones, highly durable lithium-aluminosilicate compositions offering superior drop performance, and integrated functionalities like under-display fingerprint sensors and haptic feedback layers. Research also focuses on self-healing coatings, enhanced anti-glare properties, and sustainable manufacturing processes.

How do foldable phones impact the cover glass market?

Foldable phones profoundly impact the market by driving demand for entirely new types of cover glass: ultra-thin, highly flexible glass that can bend repeatedly without breaking or showing crease marks. This necessitates significant advancements in material science and manufacturing processes, opening new growth opportunities for specialized glass manufacturers and differentiating their offerings from traditional rigid glass.

What are the key factors driving the growth of the smartphone cover glass market?

Key growth drivers include the continuous increase in global smartphone adoption, particularly in emerging markets, rising consumer demand for premium, durable, and aesthetically appealing devices, and ongoing technological advancements in display technologies such as foldable screens and edge-to-edge designs. Additionally, the regular smartphone replacement cycle contributes significantly to sustained demand for new cover glass.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted