Smart Water Metering Market

Smart Water Metering Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703954 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

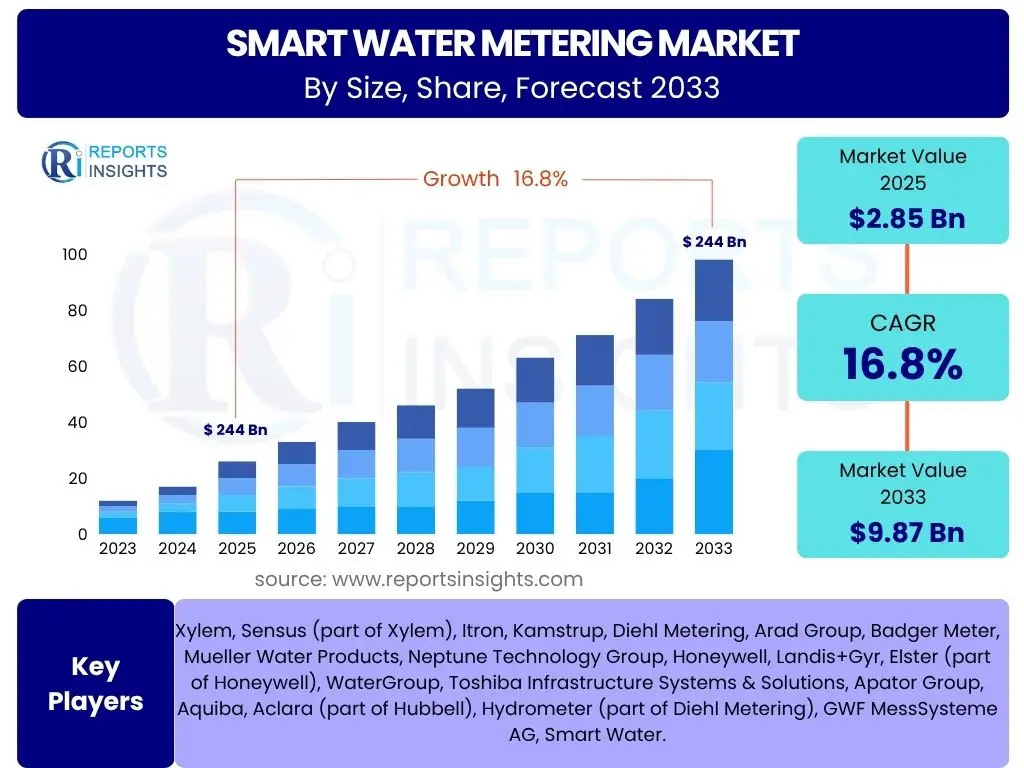

Smart Water Metering Market Size

According to Reports Insights Consulting Pvt Ltd, The Smart Water Metering Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 16.8% between 2025 and 2033. The market is estimated at USD 2.85 billion in 2025 and is projected to reach USD 9.87 billion by the end of the forecast period in 2033.

Key Smart Water Metering Market Trends & Insights

The Smart Water Metering market is undergoing a significant transformation, driven by an increasing global emphasis on water conservation, efficiency, and infrastructure modernization. Key trends revolve around the integration of advanced connectivity technologies, such as cellular IoT (NB-IoT, LoRaWAN) and 5G, enabling real-time data transmission and enhanced network control. This technological evolution facilitates not only accurate billing but also proactive leak detection, demand forecasting, and improved operational efficiency for utility providers worldwide.

Further insights indicate a growing adoption of cloud-based platforms and data analytics tools that transform raw meter data into actionable intelligence. This shift supports smart city initiatives, promoting sustainable urban development and resource management. The market is also seeing a convergence of smart metering with broader smart grid and smart home ecosystems, creating a more interconnected and optimized utility infrastructure. Regulatory mandates and government incentives for water resource management and digital transformation are significant drivers shaping these trends, pushing utilities towards more intelligent water networks.

- Increased adoption of Narrowband IoT (NB-IoT) and LoRaWAN for extended network coverage and low power consumption.

- Rising integration of Artificial Intelligence and Machine Learning for predictive analytics and anomaly detection.

- Growing focus on water conservation and sustainable water management practices globally.

- Expansion of smart city initiatives driving the deployment of advanced water infrastructure.

- Enhanced cybersecurity measures for protecting sensitive water consumption data.

- Shift towards software-as-a-service (SaaS) models for data management and analytics platforms.

- Greater emphasis on consumer engagement platforms to promote conscious water usage.

AI Impact Analysis on Smart Water Metering

Artificial Intelligence (AI) is poised to revolutionize the Smart Water Metering market by transforming raw data into actionable insights, significantly enhancing operational efficiency and resource management. Users are particularly interested in how AI can move beyond basic data collection to offer predictive capabilities, enabling utilities to anticipate infrastructure failures, optimize water distribution networks, and detect leaks with unprecedented accuracy. The integration of machine learning algorithms allows for continuous learning from consumption patterns and environmental data, leading to more precise forecasting and a reduction in non-revenue water (NRW) losses.

Common concerns include the computational resources required for AI implementation, the need for high-quality, continuous data streams, and the ethical implications surrounding data privacy and security. However, expectations are high for AI to automate complex processes, identify fraudulent activities, and personalize consumer engagement through tailored recommendations for water saving. The strategic deployment of AI is anticipated to drive substantial cost savings for utilities, improve service reliability for consumers, and contribute significantly to global water sustainability efforts by enabling smarter, more resilient water systems.

- Predictive Leak Detection: AI algorithms analyze flow data patterns to identify anomalies indicative of leaks, minimizing water loss.

- Optimized Water Distribution: Machine learning models predict demand fluctuations, optimizing pressure and flow across the network.

- Enhanced Customer Engagement: AI-driven insights provide personalized consumption reports and conservation tips to users.

- Automated Anomaly Detection: Real-time monitoring for unusual consumption, potential fraud, or meter tampering.

- Infrastructure Health Monitoring: AI assesses the condition of pipes and equipment, forecasting maintenance needs and preventing failures.

- Improved Billing Accuracy: AI can refine billing processes by identifying inconsistencies and validating meter readings.

- Resource Allocation Efficiency: Smarter allocation of water resources based on real-time data and predictive models.

Key Takeaways Smart Water Metering Market Size & Forecast

The Smart Water Metering market is experiencing robust expansion, driven by the imperative for efficient water resource management and the rapid digitalization of utility infrastructure globally. Key takeaways underscore a significant projected growth trajectory, reflecting increasing investments in advanced metering infrastructure (AMI) and associated software and services. This growth is largely fueled by escalating global water scarcity concerns, aging conventional water infrastructure, and supportive governmental regulations promoting sustainable practices and smart city developments. The market’s momentum is also strongly linked to the ongoing advancements in IoT, AI, and data analytics, which are enabling more precise monitoring, control, and optimization of water networks.

Furthermore, the forecast highlights a strategic shift towards integrated solutions that offer comprehensive data insights, enhanced operational efficiency, and improved customer engagement. The substantial increase in market valuation by 2033 indicates a broad acceptance and integration of smart water technologies across residential, commercial, and industrial sectors. This growth signals a global commitment to reducing non-revenue water, enhancing service reliability, and building resilient water systems capable of addressing future challenges. The market is evolving from simple meter reading to a complex ecosystem of intelligent water management solutions.

- The market is poised for significant growth, projected to nearly quadruple in value by 2033.

- Technological advancements in IoT, AI, and communication protocols are critical growth enablers.

- Increasing global water stress and regulatory support are primary demand drivers.

- Investments are shifting towards comprehensive AMI solutions encompassing hardware, software, and services.

- Focus on reducing non-revenue water (NRW) and improving operational efficiency is paramount.

- Integration with broader smart city frameworks is a key developmental trajectory.

Smart Water Metering Market Drivers Analysis

The global Smart Water Metering market is significantly propelled by a confluence of critical drivers, prominently including the escalating global water scarcity and the increasing need for efficient water resource management. As populations grow and climate change impacts water availability, governments and utilities are compelled to adopt smart solutions to monitor, conserve, and distribute water more effectively. This imperative drives investments in smart meters that provide real-time data, enabling leak detection, accurate billing, and improved demand-side management, thereby directly addressing the urgent need for water conservation.

Another major driver is the widespread aging water infrastructure in many developed and developing regions. Traditional water networks are prone to leaks and inefficiencies, leading to substantial non-revenue water losses. Smart metering offers a technological upgrade that helps pinpoint and mitigate these losses, extending the lifespan of existing infrastructure through proactive maintenance. Additionally, supportive government policies and regulatory mandates aimed at promoting water conservation, digitalization of utilities, and smart city development are accelerating the adoption of these technologies, providing incentives and frameworks for implementation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Water Scarcity and Conservation Needs | +4.5% | Global, particularly MEA, Asia Pacific | Long-term (2025-2033) |

| Aging Water Infrastructure and Non-Revenue Water (NRW) Reduction | +3.8% | North America, Europe, parts of Asia Pacific | Mid to Long-term (2025-2033) |

| Supportive Government Policies and Smart City Initiatives | +3.2% | Europe, Asia Pacific, North America | Mid-term (2025-2030) |

| Technological Advancements (IoT, AI, Data Analytics) | +2.5% | Global | Ongoing (2025-2033) |

| Operational Efficiency and Cost Savings for Utilities | +2.0% | Global | Short to Mid-term (2025-2028) |

Smart Water Metering Market Restraints Analysis

Despite the strong growth potential, the Smart Water Metering market faces several significant restraints that could impede its expansion. One of the primary barriers is the high upfront capital investment required for deploying smart metering infrastructure. This includes not only the cost of the meters themselves but also the communication networks, software platforms, and necessary upgrades to existing utility systems. For smaller municipalities or utilities with limited budgets, these initial costs can be prohibitive, slowing down adoption rates, particularly in developing regions where financial resources are scarce.

Another substantial restraint is the concern surrounding data privacy and cybersecurity. Smart meters collect and transmit sensitive consumption data, raising questions about how this data is stored, protected, and utilized. Breaches or misuse of this information can erode consumer trust and lead to regulatory scrutiny, requiring utilities to invest heavily in robust cybersecurity measures, which adds to the overall cost and complexity of deployment. Additionally, a lack of standardized communication protocols and interoperability issues between different smart metering solutions from various vendors can create integration challenges, leading to fragmented systems and hindering seamless data exchange.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Investment | -3.5% | Global, particularly developing economies | Long-term (2025-2033) |

| Data Privacy and Cybersecurity Concerns | -2.8% | North America, Europe | Ongoing (2025-2033) |

| Lack of Standardization and Interoperability Issues | -2.0% | Global | Mid-term (2025-2030) |

| Complexity of Integration with Legacy Systems | -1.5% | Global | Mid-term (2025-2030) |

Smart Water Metering Market Opportunities Analysis

The Smart Water Metering market is rich with significant opportunities for growth and innovation, driven by evolving technological landscapes and increasing demands for efficient resource management. A key opportunity lies in the expanding scope of smart city initiatives worldwide, which integrate various intelligent infrastructure components, including smart water systems. As urban areas aim for greater sustainability and efficiency, the demand for connected water networks that enable real-time monitoring, leak detection, and optimized distribution will continue to surge, creating broad deployment avenues for smart metering solutions.

Furthermore, the continuous advancements in IoT, AI, and data analytics present substantial opportunities for developing more sophisticated and value-added services beyond basic metering. This includes predictive maintenance services for water infrastructure, advanced analytics for consumption forecasting, and personalized consumer engagement platforms that empower users to manage their water usage more effectively. The growing focus on combating climate change and achieving Sustainable Development Goals (SDGs) also provides a strong impetus for adopting smart water technologies, particularly in developing economies where water infrastructure development and conservation are paramount concerns, offering untapped market potential.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Smart City Initiatives Globally | +3.0% | Asia Pacific, Europe, North America | Long-term (2025-2033) |

| Development of Advanced Analytics and AI-driven Solutions | +2.7% | Global | Ongoing (2025-2033) |

| Growing Demand in Developing Economies for New Infrastructure | +2.5% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Integration with Broader Utility Management Systems | +1.8% | Global | Mid-term (2025-2030) |

| Focus on Sustainable Development Goals and Water Conservation | +1.5% | Global | Long-term (2025-2033) |

Smart Water Metering Market Challenges Impact Analysis

The Smart Water Metering market faces several critical challenges that demand strategic responses from stakeholders to ensure sustainable growth. One significant challenge is the complex process of integrating new smart metering systems with existing legacy infrastructure. Many utilities operate with outdated, disparate systems that were not designed for the real-time data flow and interoperability required by smart technologies. This integration complexity often leads to prolonged deployment times, increased costs, and technical hurdles, requiring substantial IT investment and skilled personnel to manage the transition effectively.

Another major challenge revolves around the security of data and the prevention of cyber-attacks. As smart meters transmit sensitive consumption data over networks, they become potential targets for malicious activities, including data theft, manipulation, or disruption of service. Ensuring robust cybersecurity measures, including encryption, authentication, and continuous monitoring, is paramount but presents an ongoing technical and financial burden for utilities. Furthermore, achieving consumer acceptance and addressing public skepticism regarding the accuracy of smart meters and the privacy of their data remains a challenge, necessitating clear communication, transparent data policies, and visible benefits to build trust.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Integration with Legacy IT and OT Systems | -2.2% | Global | Mid-term (2025-2030) |

| Cybersecurity Threats and Data Privacy Concerns | -1.9% | North America, Europe | Ongoing (2025-2033) |

| Ensuring Consumer Acceptance and Addressing Public Skepticism | -1.5% | Global | Short to Mid-term (2025-2028) |

| Lack of Skilled Workforce for Deployment and Management | -1.0% | Global, particularly developing economies | Long-term (2025-2033) |

Smart Water Metering Market - Updated Report Scope

This report provides a comprehensive analysis of the global Smart Water Metering market, offering in-depth insights into its size, growth trends, drivers, restraints, opportunities, and challenges. The scope encompasses detailed segmentation analysis by component, type, application, and technology, providing a granular view of market dynamics across various sectors. Furthermore, the report delves into regional market trends and competitive landscapes, profiling key industry players to offer a holistic understanding of the market ecosystem. It aims to equip stakeholders with critical data for strategic decision-making and investment planning within the evolving smart water sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 9.87 Billion |

| Growth Rate | 16.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Xylem, Sensus (part of Xylem), Itron, Kamstrup, Diehl Metering, Arad Group, Badger Meter, Mueller Water Products, Neptune Technology Group, Honeywell, Landis+Gyr, Elster (part of Honeywell), WaterGroup, Toshiba Infrastructure Systems & Solutions, Apator Group, Aquiba, Aclara (part of Hubbell), Hydrometer (part of Diehl Metering), GWF MessSysteme AG, Smart Water. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Smart Water Metering market is comprehensively segmented across several key dimensions, providing a detailed understanding of its diverse applications and technological underpinnings. These segmentations allow for a granular analysis of market demand, technological preferences, and growth opportunities within specific categories. Understanding these segments is crucial for stakeholders to tailor their product offerings, marketing strategies, and investment decisions to target the most promising areas of the market.

- By Component: This segment includes the physical hardware necessary for metering, the software platforms for data management and analysis, and the services that support deployment and ongoing operations.

- Hardware: Encompasses smart water meters, communication modules that enable data transmission, and data concentrators that aggregate information from multiple meters.

- Software: Comprises Meter Data Management (MDM) systems for handling large volumes of meter data, Billing & Customer Information Systems (CIS) for revenue management, and advanced Analytics & Visualization Platforms for actionable insights.

- Services: Includes critical activities such as system installation, ongoing maintenance & technical support, and expert consulting for deployment strategies and system optimization.

- By Type: Differentiates between the two primary architectures for smart metering systems, reflecting different levels of automation and real-time capabilities.

- Advanced Metering Infrastructure (AMI): Provides two-way communication between the meter and the utility, enabling real-time data exchange, remote control, and advanced functionalities like demand response and outage management.

- Automated Meter Reading (AMR): Primarily involves one-way communication for automatic collection of meter readings, typically requiring a mobile or fixed network to collect data periodically, rather than continuously.

- By Application: Categorizes the market based on the end-use sector, highlighting the varying needs and adoption rates across different consumer groups.

- Residential: Focuses on smart meters deployed in individual homes, primarily for accurate billing, leak detection, and promoting water conservation among homeowners.

- Commercial: Pertains to meters installed in businesses, offices, and retail establishments, often with higher consumption and a need for detailed consumption analytics for operational efficiency.

- Industrial: Involves large-scale deployments in manufacturing plants, processing facilities, and other industrial sites where precise water usage monitoring is critical for process optimization, compliance, and waste reduction.

- By Technology: Examines the different communication technologies used to transmit data from smart meters to the utility, impacting range, power consumption, and data transfer rates.

- Cellular: Utilizes mobile network technologies like NB-IoT (Narrowband IoT), LoRaWAN (Long Range Wide Area Network), and increasingly 5G for wide-area coverage and reliable data transmission.

- RF (Radio Frequency): Includes short-range wireless technologies such as ZigBee and Wi-Fi, often used in dense urban environments or for specific local area network applications.

- Wired: Refers to traditional cable-based connections like Ethernet or fiber optic, typically deployed in specific industrial or commercial settings requiring high data reliability and security.

Regional Highlights

- North America: This region is a mature market for smart water metering, driven by aging infrastructure replacement, focus on reducing non-revenue water, and increasing adoption of advanced analytics. The United States and Canada are leading the way with significant investments in AMI deployments and integration with smart city initiatives. Regulatory support for water conservation and efficiency also plays a crucial role in market growth.

- Europe: Europe is experiencing robust growth due to stringent environmental regulations, government mandates for smart meter rollout, and a strong emphasis on sustainability and resource management. Countries like the UK, France, Germany, and Spain are actively implementing smart water projects to combat water stress and improve operational efficiencies. The region benefits from well-established utility infrastructure and a high level of technological readiness.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, primarily due to rapid urbanization, increasing industrialization, and significant infrastructure development in emerging economies like China, India, and Southeast Asian countries. The region faces severe water scarcity issues, driving the need for efficient water management solutions. Government investments in smart city projects and digitalization initiatives are key growth catalysts.

- Latin America: This region presents considerable growth potential, although adoption rates vary by country. Brazil, Mexico, and Argentina are emerging as key markets, driven by efforts to modernize outdated infrastructure, reduce water losses, and improve service delivery. Economic stability and governmental support for public utility upgrades are crucial for market expansion.

- Middle East and Africa (MEA): The MEA region is witnessing significant adoption of smart water metering, particularly in water-stressed countries in the Middle East, driven by acute water scarcity and large-scale infrastructure projects. Countries like UAE, Saudi Arabia, and South Africa are investing heavily in smart water technologies to ensure sustainable water supply and combat rapid population growth and climate change impacts.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Smart Water Metering Market.- Xylem

- Sensus (part of Xylem)

- Itron

- Kamstrup

- Diehl Metering

- Arad Group

- Badger Meter

- Mueller Water Products

- Neptune Technology Group

- Honeywell

- Landis+Gyr

- Elster (part of Honeywell)

- WaterGroup

- Toshiba Infrastructure Systems & Solutions

- Apator Group

- Aquiba

- Aclara (part of Hubbell)

- Hydrometer (part of Diehl Metering)

- GWF MessSysteme AG

- Smart Water

Frequently Asked Questions

Analyze common user questions about the Smart Water Metering market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Smart Water Metering?

Smart Water Metering refers to the use of advanced meters that automatically record water consumption and communicate data wirelessly to utility providers. This technology enables real-time monitoring, remote management, and provides consumers with detailed insights into their water usage for efficiency.

What are the primary benefits of Smart Water Metering for utilities?

For utilities, smart water metering offers numerous benefits including reduced non-revenue water through leak detection, improved billing accuracy, enhanced operational efficiency, optimized network management, and better customer service by providing transparent usage data.

How does AI impact the Smart Water Metering market?

AI significantly impacts the smart water metering market by enabling predictive analytics for leak detection, optimizing water distribution, identifying consumption anomalies, and enhancing overall system intelligence, leading to more efficient and sustainable water management.

What are the main challenges in adopting Smart Water Metering systems?

Key challenges include the high upfront capital investment required for deployment, concerns regarding data privacy and cybersecurity, complexity in integrating with legacy infrastructure, and the need for a skilled workforce to manage and maintain these advanced systems.

Which regions are leading in Smart Water Metering adoption?

North America and Europe are currently leading in smart water metering adoption due to aging infrastructure and strong regulatory support. However, Asia Pacific is projected to experience the fastest growth, driven by rapid urbanization and increasing water scarcity concerns in emerging economies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted