Smart Meter Market

Smart Meter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702447 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

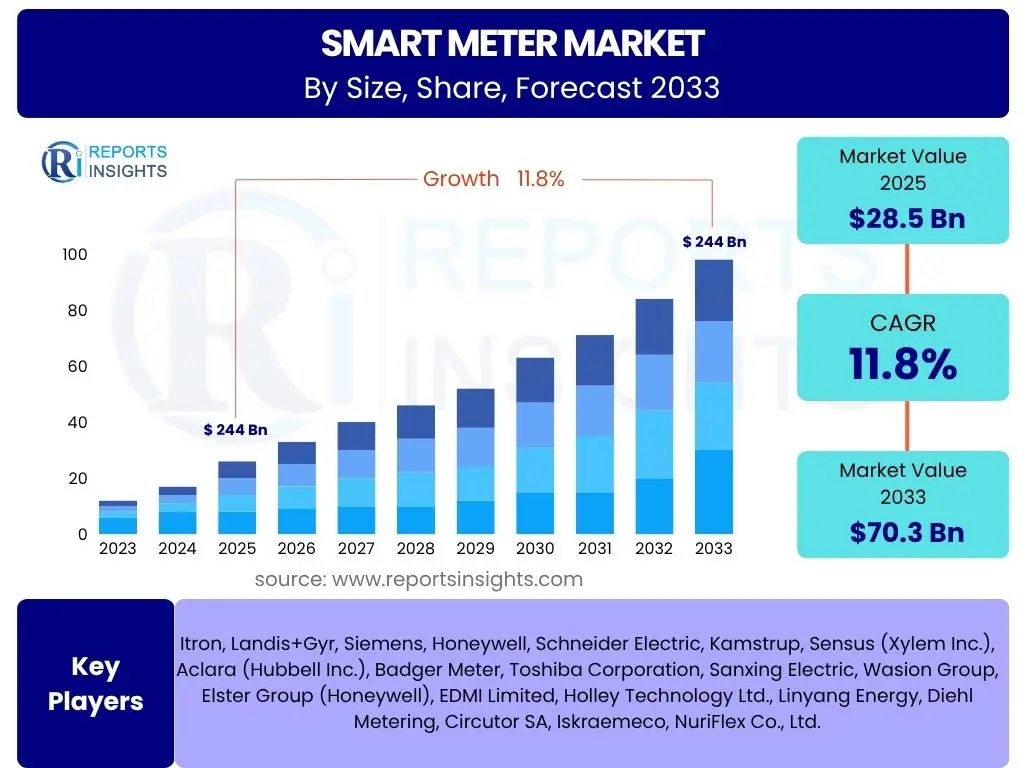

Smart Meter Market Size

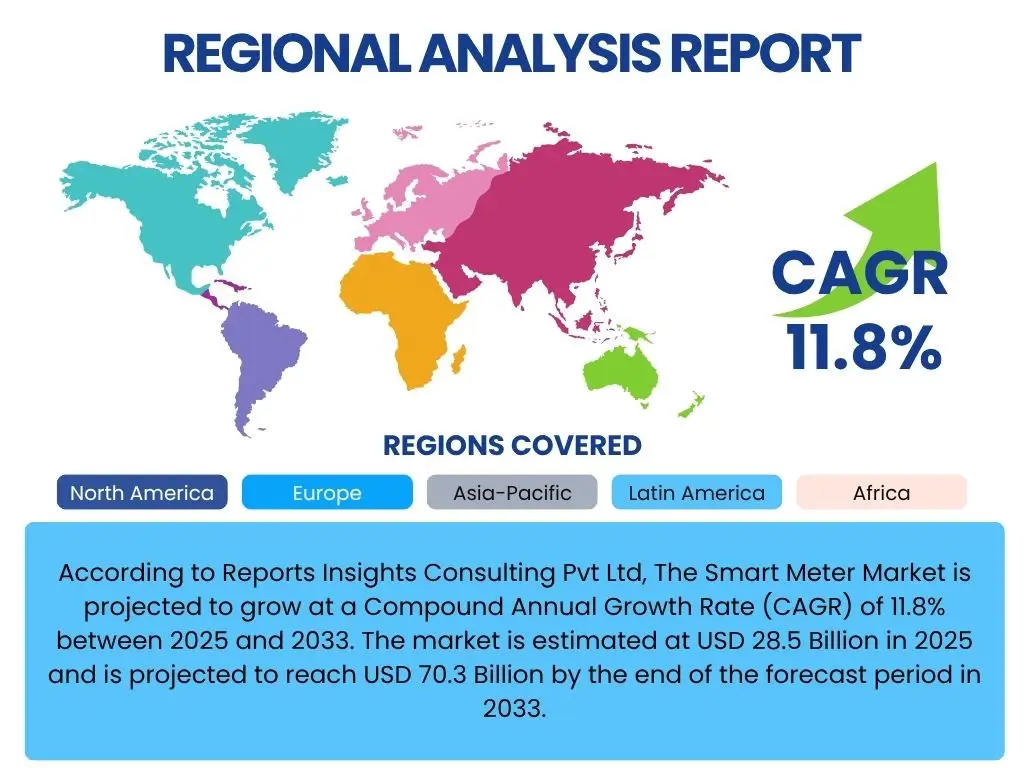

According to Reports Insights Consulting Pvt Ltd, The Smart Meter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8% between 2025 and 2033. The market is estimated at USD 28.5 Billion in 2025 and is projected to reach USD 70.3 Billion by the end of the forecast period in 2033.

Key Smart Meter Market Trends & Insights

Common user inquiries about the Smart Meter market frequently revolve around the evolving technological landscape, the influence of regulatory mandates, and the increasing integration of digital infrastructure. Users seek to understand how these elements collectively shape market growth and impact consumer and utility interactions. A predominant theme is the shift towards advanced metering infrastructure (AMI) over traditional automatic meter reading (AMR) systems, driven by the demand for real-time data and enhanced grid management capabilities. Furthermore, the convergence of smart meters with broader smart grid initiatives and the Internet of Things (IoT) ecosystems is a significant area of interest, reflecting a move towards more interconnected and intelligent energy systems.

Another critical area of user concern and analytical focus is the growing emphasis on energy efficiency and sustainability. As global efforts to combat climate change intensify, smart meters are viewed as foundational tools for demand-side management, enabling consumers and utilities to monitor and optimize energy consumption. This trend is complemented by the rising consumer awareness regarding energy costs and the desire for greater control over household utility usage. Consequently, the market is witnessing innovations in user interfaces, data analytics platforms, and value-added services that empower end-users with actionable insights into their energy consumption patterns.

Moreover, the market is characterized by a strong regulatory push from governments worldwide, particularly in developed economies, to modernize aging grid infrastructure and promote sustainable energy practices. These mandates often include targets for smart meter deployment, incentivizing utilities to invest in new technologies. This regulatory environment, coupled with ongoing technological advancements in communication protocols and data processing capabilities, defines the current trajectory of the Smart Meter market, highlighting a transition towards more resilient, efficient, and interactive energy distribution networks.

- Growing adoption of Advanced Metering Infrastructure (AMI) systems for real-time data and remote management.

- Increasing integration of smart meters with IoT devices and smart home ecosystems.

- Strong emphasis on energy efficiency and demand-side management by utilities and consumers.

- Supportive government policies and regulatory mandates for smart grid modernization and smart meter deployment.

- Development of sophisticated data analytics platforms for deriving actionable insights from meter data.

- Rising focus on cybersecurity measures to protect smart meter data and infrastructure.

- Expansion into new applications, including water and gas metering, beyond electricity.

AI Impact Analysis on Smart Meter

User queries regarding the impact of Artificial Intelligence (AI) on Smart Meters frequently center on AI's potential to revolutionize data processing, enhance predictive capabilities, and bolster the security of smart grid systems. There is considerable interest in how AI can move beyond basic data collection to provide deeper insights into consumption patterns, identify anomalies, and optimize energy distribution in real-time. Users are keen to understand AI's role in improving grid reliability, reducing operational costs, and personalizing energy management for end-users, reflecting a desire for more intelligent and responsive utility services.

A key theme in user concerns is the practical implementation and challenges associated with integrating AI into existing smart meter infrastructure. Questions often arise concerning the computational power required, the ethical implications of data privacy when AI analyzes granular consumption data, and the need for skilled personnel to develop and manage AI-driven systems. Users also explore the potential for AI to enhance preventive maintenance of grid components by predicting failures and optimizing resource allocation, thereby reducing downtime and improving service quality.

Furthermore, users are interested in the long-term transformative effects of AI on the utility sector, envisioning a future where AI-powered smart meters facilitate dynamic pricing, enable peer-to-peer energy trading, and support the seamless integration of distributed renewable energy sources. The general expectation is that AI will unlock new levels of efficiency, intelligence, and resilience within the energy grid, moving it closer to a fully autonomous and self-optimizing system while also addressing the complexities of modern energy demands and environmental goals.

- Enhanced predictive analytics for demand forecasting and grid optimization.

- Real-time anomaly detection and fraud prevention through AI-driven pattern recognition.

- Automated fault detection and predictive maintenance reducing operational costs and downtime.

- Optimized energy distribution and load balancing in smart grids, improving efficiency.

- Personalized energy consumption insights and recommendations for consumers.

- Improved cybersecurity by identifying and responding to abnormal network behaviors.

- Facilitation of dynamic pricing models and peer-to-peer energy trading.

- Better integration and management of distributed renewable energy sources.

Key Takeaways Smart Meter Market Size & Forecast

User inquiries about the key takeaways from the Smart Meter market size and forecast consistently point towards a desire for a concise understanding of the market's growth trajectory, primary drivers, and significant regional contributions. There is a strong interest in grasping the overall investment potential and strategic implications for stakeholders, including utilities, technology providers, and policymakers. Users seek clarity on whether the market's expansion is sustainable and what underlying factors will continue to fuel its projected growth over the forecast period, emphasizing the need for robust data-backed conclusions.

Another crucial area of interest concerns the long-term impact of regulatory frameworks and technological advancements on market dynamics. Users want to know how global initiatives for grid modernization and energy efficiency translate into tangible market opportunities and what role smart meters play in achieving broader sustainability goals. The implications of this growth for both developed and emerging economies are also a recurring theme, highlighting the global interconnectedness of energy infrastructure development.

Ultimately, the core insight users seek is a clear picture of the smart meter market's inevitability and its foundational role in the future of energy management. The takeaways must succinctly convey that this market is not merely growing but transforming the utility landscape, driven by a confluence of regulatory push, technological pull, and an increasing global imperative for efficient and sustainable energy use. The forecast indicates a robust and consistent expansion, making smart meters a pivotal component of modern energy infrastructure.

- The Smart Meter market is poised for substantial and sustained growth, driven by global energy modernization efforts.

- Significant investment opportunities exist across the value chain, from hardware manufacturing to data analytics services.

- Regulatory support and government mandates are critical accelerators for market expansion, especially in established economies.

- Technological advancements, particularly in communication and data processing, are enhancing smart meter capabilities and driving adoption.

- Asia Pacific is projected to lead in market share due to rapid urbanization and infrastructure development, while Europe and North America maintain high adoption rates.

- The transition towards Advanced Metering Infrastructure (AMI) is a key factor underpinning the market's projected value increase.

Smart Meter Market Drivers Analysis

The Smart Meter market is propelled by a confluence of factors, primarily driven by the global imperative for energy efficiency, grid modernization, and the integration of renewable energy sources. Government regulations and policies worldwide are playing a pivotal role, mandating or incentivizing the deployment of smart meters to enhance energy conservation, reduce carbon emissions, and improve grid reliability. These legislative efforts create a stable demand foundation for manufacturers and solution providers, ensuring a continuous push towards widespread adoption across residential, commercial, and industrial sectors.

Furthermore, the escalating global energy demand coupled with volatile energy prices is compelling utilities to seek more efficient and intelligent energy management solutions. Smart meters offer the ability to monitor consumption in real-time, facilitate demand-response programs, and enable dynamic pricing, all of which contribute to better energy management and cost reduction for both utilities and consumers. The increasing consumer awareness regarding energy consumption and the desire for greater control over their utility bills also serve as significant drivers, fostering a demand for transparency and actionable data that smart meters readily provide.

Technological advancements, particularly in communication protocols (such as cellular, RF, and PLC), data analytics, and the Internet of Things (IoT), are continuously enhancing the capabilities and cost-effectiveness of smart meter deployments. The integration of smart meters with broader smart grid initiatives allows for improved outage management, enhanced grid stability, and the seamless incorporation of distributed energy resources like rooftop solar. This technological evolution not only makes smart meters more robust and versatile but also lowers the barriers to adoption by offering more reliable and feature-rich solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Government Mandates & Regulations for Grid Modernization | +2.5% | Europe, North America, APAC (China, India) | Long-term (2025-2033) |

| Rising Energy Costs & Focus on Energy Efficiency | +1.8% | Global, particularly Europe and Asia Pacific | Mid-term (2025-2029) |

| Increasing Adoption of Smart Grid Infrastructure | +2.0% | North America, Europe, parts of Asia Pacific | Long-term (2025-2033) |

| Integration of Renewable Energy Sources | +1.5% | Global, particularly developed economies | Long-term (2028-2033) |

| Technological Advancements in Communication & Analytics | +1.2% | Global | Ongoing (2025-2033) |

Smart Meter Market Restraints Analysis

Despite the strong growth trajectory, the Smart Meter market faces several significant restraints that can impede its full potential. One of the primary challenges is the high initial investment required for deployment. Utilities often need to overhaul existing infrastructure, which can be a substantial capital expenditure, particularly for large-scale rollouts across an entire service area. This financial burden can be a deterrent, especially for smaller utilities or those operating in regions with limited government subsidies or funding mechanisms, leading to slower adoption rates.

Another major concern revolves around data privacy and cybersecurity. Smart meters collect granular consumption data, which, if compromised, could reveal sensitive information about a household's activities or industrial operations. The potential for data breaches, hacking attempts, or unauthorized access raises significant privacy concerns among consumers and regulatory bodies. Utilities must invest heavily in robust cybersecurity measures and ensure compliance with stringent data protection regulations, which adds to the cost and complexity of smart meter deployment and can erode consumer trust if not adequately addressed.

Furthermore, consumer resistance and a lack of awareness or understanding about the benefits of smart meters can act as a restraint. Some consumers harbor skepticism about the technology, fearing potential health impacts from electromagnetic fields, or distrusting the accuracy of billing based on new metering systems. Overcoming this resistance requires comprehensive public awareness campaigns, transparent communication from utilities, and demonstrated benefits that clearly outweigh perceived risks. The absence of standardized protocols for smart meter interoperability across different manufacturers and regions also presents a challenge, potentially leading to vendor lock-in and complicating large-scale, integrated smart grid deployments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Deployment Costs | -1.5% | Global, particularly developing economies | Mid-term (2025-2029) |

| Data Privacy and Cybersecurity Concerns | -1.0% | North America, Europe | Ongoing (2025-2033) |

| Lack of Standardization & Interoperability Issues | -0.8% | Global | Long-term (2025-2033) |

| Consumer Resistance and Acceptance Challenges | -0.7% | Select regions globally | Short-term (2025-2027) |

Smart Meter Market Opportunities Analysis

The Smart Meter market is brimming with opportunities driven by emerging technologies and evolving energy landscapes. One significant area of growth lies in the integration of smart meters with advanced analytics and Artificial Intelligence (AI). This integration moves beyond mere data collection, enabling utilities to derive actionable insights for predictive maintenance, optimized grid operations, and personalized energy management for consumers. As AI capabilities mature, the potential for dynamic pricing, real-time load balancing, and enhanced fraud detection expands, creating new value propositions for both service providers and end-users.

Another prominent opportunity is the expansion into developing and emerging economies. While developed regions have initiated or completed significant smart meter rollouts, vast populations in countries across Asia Pacific, Latin America, and Africa still rely on traditional metering systems. Rapid urbanization, increasing energy demand, and government initiatives to modernize infrastructure in these regions present enormous untapped markets. Utilities in these areas can leapfrog older technologies and directly implement advanced smart meter solutions, often benefiting from lower deployment costs and supportive policies aimed at energy access and efficiency.

Furthermore, the diversification of smart meter applications beyond electricity to include water and gas metering offers substantial growth potential. As utilities aim for holistic resource management, integrating smart water and gas meters into a unified smart utility network allows for comprehensive monitoring, leak detection, and consumption optimization across all utility services. The convergence of these metering types, coupled with the increasing focus on smart city initiatives, creates a broader ecosystem where smart meters serve as foundational elements for integrated urban infrastructure, opening up new revenue streams and fostering cross-sector collaborations for market players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Advanced Analytics & AI for Enhanced Insights | +1.7% | Global, particularly North America & Europe | Long-term (2028-2033) |

| Expansion into Developing & Emerging Economies | +2.0% | Asia Pacific (India, Southeast Asia), Latin America, MEA | Mid-term (2025-2030) |

| Diversification into Smart Water and Gas Metering | +1.3% | Global | Mid-term (2025-2029) |

| Growth in Smart City Initiatives and Integrated Utility Management | +1.0% | Global, urban centers | Long-term (2028-2033) |

Smart Meter Market Challenges Impact Analysis

The Smart Meter market, while promising, contends with several impactful challenges that can influence its growth trajectory. One significant hurdle is the persistent issue of interoperability and a lack of universal standardization across various smart meter technologies and communication protocols. Different manufacturers often employ proprietary systems, making it difficult for utilities to integrate diverse smart meter types into a single, cohesive smart grid network. This fragmentation can lead to higher deployment costs, increased complexity in system management, and limits the scalability and flexibility of smart grid initiatives, potentially slowing down wider adoption.

Another critical challenge is managing the sheer volume and velocity of data generated by smart meters. The transition from manual meter reading to real-time data collection results in an unprecedented deluge of data points, requiring robust data storage, processing, and analytical capabilities. Utilities often face challenges in building the necessary IT infrastructure and developing the expertise to effectively manage, analyze, and secure this big data. Without adequate data governance and analytical tools, the full benefits of smart meter deployments – such as predictive maintenance, demand forecasting, and personalized energy insights – cannot be realized, potentially undermining the value proposition.

Furthermore, securing the smart meter infrastructure against cyber threats remains a paramount and evolving challenge. As smart meters become integral to critical national infrastructure, they present an attractive target for cyberattacks, ranging from data breaches and privacy violations to more severe disruptions like grid manipulation or blackouts. Ensuring end-to-end security from the meter device to the data center, including secure communication channels and robust encryption, requires continuous investment in advanced cybersecurity solutions and skilled personnel. The constantly evolving nature of cyber threats means utilities must remain vigilant and continuously update their security protocols, adding significant operational costs and risks to smart meter deployments.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability & Lack of Standardization | -1.2% | Global | Ongoing (2025-2033) |

| Management of Big Data & Analytics Infrastructure | -0.9% | Global | Mid-term (2025-2029) |

| Cybersecurity Threats & Data Protection Compliance | -1.1% | Global, particularly North America & Europe | Ongoing (2025-2033) |

| Integration with Legacy Systems | -0.8% | Global, established grids | Long-term (2025-2033) |

Smart Meter Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Smart Meter market, offering a detailed understanding of its current size, historical performance, and future growth projections. It meticulously examines the driving forces, existing restraints, emerging opportunities, and significant challenges that shape the market landscape. The scope extends to a detailed segmentation analysis, encompassing various types, technologies, and end-use applications, alongside a thorough regional assessment to highlight key market dynamics across different geographies, providing actionable insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 Billion |

| Market Forecast in 2033 | USD 70.3 Billion |

| Growth Rate | 11.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Itron, Landis+Gyr, Siemens, Honeywell, Schneider Electric, Kamstrup, Sensus (Xylem Inc.), Aclara (Hubbell Inc.), Badger Meter, Toshiba Corporation, Sanxing Electric, Wasion Group, Elster Group (Honeywell), EDMI Limited, Holley Technology Ltd., Linyang Energy, Diehl Metering, Circutor SA, Iskraemeco, NuriFlex Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Smart Meter market is extensively segmented to provide a granular view of its diverse applications and technological nuances. This comprehensive segmentation allows for a detailed analysis of market dynamics, growth drivers, and opportunities within specific sub-sectors, enabling stakeholders to identify lucrative niches and tailor strategies effectively. The market is primarily bifurcated by Type into Advanced Metering Infrastructure (AMI) and Automatic Meter Reading (AMR), reflecting the ongoing technological transition in data collection and communication capabilities.

Further segmentation by Phase (Single Phase and Three Phase) addresses the distinct requirements of different consumer types, from residential households to large industrial and commercial complexes. The Technology segment differentiates meters based on their communication methods, including Power Line Communication (PLC), Radio Frequency (RF), and Cellular technologies (GPRS/3G/4G/5G), along with others like satellite and fiber optic, highlighting the varied connectivity solutions deployed globally. This technical breakdown is crucial for understanding network infrastructure dependencies and deployment costs.

Additionally, the market is segmented by End-Use, distinguishing between Residential, Commercial, and Industrial applications, each with unique consumption patterns and regulatory frameworks. The Application segment further refines this by categorizing smart meters for Electricity, Gas, and Water, emphasizing the increasing trend towards holistic smart utility management beyond just power grids. This multi-dimensional segmentation ensures a precise understanding of market size, growth rates, and competitive landscapes across all key functional areas of smart metering.

- By Type:

- Advanced Metering Infrastructure (AMI): Represents the most sophisticated form, enabling two-way communication between the meter and the utility, supporting real-time data, remote control, and advanced grid functionalities.

- Automatic Meter Reading (AMR): Involves one-way communication, typically from the meter to the utility, primarily for automated billing purposes, with less real-time capability.

- By Phase:

- Single Phase: Predominantly used in residential settings for smaller loads.

- Three Phase: Utilized for larger loads, common in commercial, industrial, and some larger residential applications requiring higher power capacities.

- By Technology:

- Power Line Communication (PLC): Utilizes existing electrical power lines for data transmission.

- Radio Frequency (RF): Employs radio waves for wireless communication between meters and collection points.

- Cellular (GPRS/3G/4G/5G): Leverages cellular networks for data transmission, offering wide coverage.

- Others (e.g., Satellite, Fiber Optic): Niche technologies used in specific geographic or infrastructure contexts.

- By End-Use:

- Residential: Meters installed in homes and apartments for individual consumer billing and energy management.

- Commercial: Meters for small to medium-sized businesses, retail establishments, and offices.

- Industrial: Meters for large manufacturing plants, factories, and heavy industries with significant energy consumption.

- By Application:

- Electricity Meters: The most widely adopted segment, for monitoring and managing electricity consumption.

- Gas Meters: For tracking natural gas usage in residential, commercial, and industrial sectors.

- Water Meters: For monitoring water consumption, enabling leak detection and efficient water resource management.

Regional Highlights

- North America: This region is a mature market for smart meters, characterized by early adoption driven by favorable regulatory mandates and significant investments in smart grid infrastructure. The focus here is increasingly on enhancing grid resilience, integrating distributed energy resources, and leveraging advanced analytics for improved operational efficiency and customer engagement. Strong governmental support and ongoing modernization efforts ensure sustained growth.

- Europe: Europe is another leading market, propelled by stringent EU directives aimed at energy efficiency, decarbonization, and consumer empowerment. Countries like the UK, France, Spain, and Italy have implemented large-scale smart meter rollouts, with a strong emphasis on cybersecurity and data privacy. The region is witnessing robust growth in AMI deployments and the integration of smart meters with renewable energy projects.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing and largest market for smart meters, primarily due to rapid urbanization, expanding energy demand, and massive infrastructure development in countries like China and India. Government initiatives to address power deficits, reduce AT&C losses, and promote clean energy are driving extensive smart meter deployments across residential and commercial sectors. The region presents significant untapped potential for vendors.

- Latin America: This region is an emerging market for smart meters, with increasing awareness and adoption driven by the need to combat energy theft, improve billing accuracy, and modernize aging grid infrastructure. Countries like Brazil and Mexico are leading the charge, with pilot projects and gradual rollouts gaining momentum. Investment in smart grid technologies is anticipated to accelerate in the coming years.

- Middle East and Africa (MEA): The MEA region is witnessing growing interest and investment in smart meter technologies, spurred by rapid economic development, diversification away from fossil fuels, and smart city initiatives. Countries in the GCC region (e.g., UAE, Saudi Arabia) are making substantial investments in advanced utility infrastructure, while parts of Africa are focusing on improving energy access and reducing technical and commercial losses.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Smart Meter Market.- Itron

- Landis+Gyr

- Siemens

- Honeywell

- Schneider Electric

- Kamstrup

- Sensus (Xylem Inc.)

- Aclara (Hubbell Inc.)

- Badger Meter

- Toshiba Corporation

- Sanxing Electric

- Wasion Group

- Elster Group (Honeywell)

- EDMI Limited

- Holley Technology Ltd.

- Linyang Energy

- Diehl Metering

- Circutor SA

- Iskraemeco

- NuriFlex Co., Ltd.

Frequently Asked Questions

What is a Smart Meter?

A Smart Meter is an electronic device that records consumption of electric energy, gas, or water in intervals of an hour or less and communicates that information back to the utility for monitoring and billing. Unlike traditional meters, smart meters facilitate two-way communication between the meter and the central system, enabling real-time data collection, remote meter reading, and advanced grid management functionalities.

How do Smart Meters benefit consumers?

Smart meters offer consumers several benefits, including more accurate billing due to real-time data, insights into their energy consumption patterns which can help them manage and reduce usage, and the ability to participate in demand-response programs. They also enable faster outage detection and restoration, improve overall service reliability, and support the integration of smart home devices.

What are the primary drivers of the Smart Meter market?

The Smart Meter market is primarily driven by government mandates for grid modernization and energy efficiency, rising energy costs, increasing adoption of smart grid infrastructure, and technological advancements in communication and data analytics. The global push for sustainable energy solutions and the integration of renewable sources also significantly contribute to market growth.

What are the main challenges facing Smart Meter adoption?

Key challenges include the high initial investment costs for utilities, persistent data privacy and cybersecurity concerns among consumers and regulators, and a lack of universal standardization leading to interoperability issues between different systems. Consumer resistance due to misinformation or lack of understanding also presents a hurdle.

How does AI impact Smart Meter technology?

AI significantly enhances smart meter capabilities by enabling advanced predictive analytics for demand forecasting and grid optimization, real-time anomaly detection for fraud prevention and fault identification, and automated asset management. AI-driven insights empower utilities to manage energy distribution more efficiently, improve cybersecurity, and offer personalized energy services to consumers, moving towards a more intelligent and resilient grid.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted