Ship Radar Market

Ship Radar Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708401 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

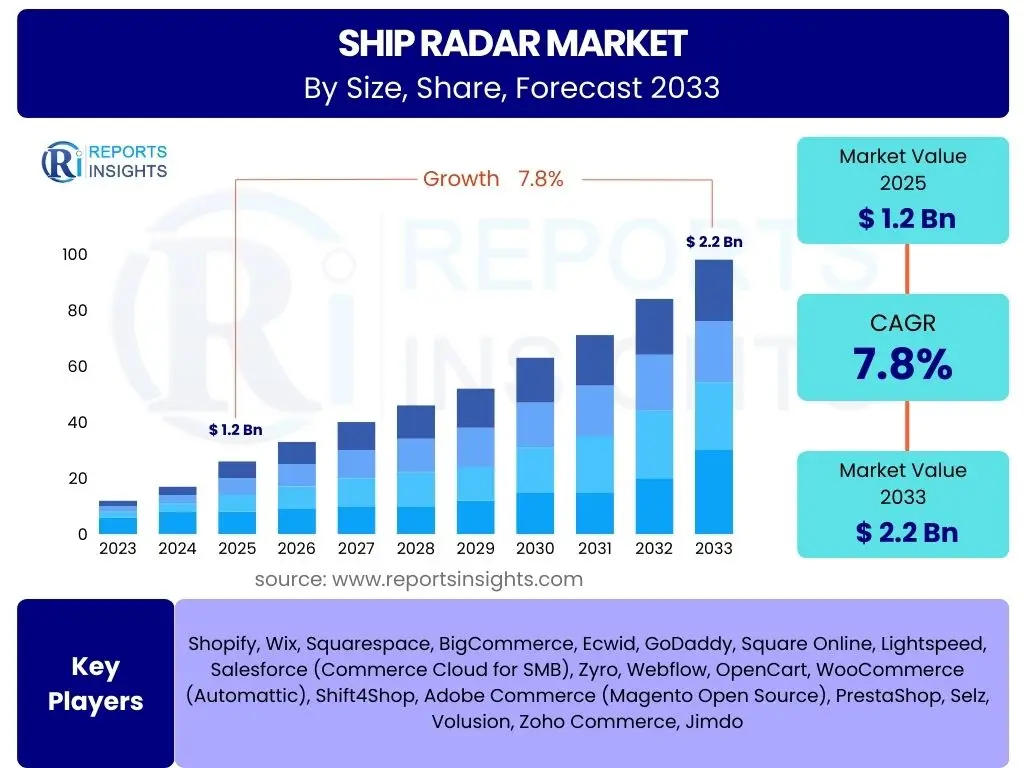

Ship Radar Market Size

According to Reports Insights Consulting Pvt Ltd, The Ship Radar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 2.2 Billion by the end of the forecast period in 2033.

Key Ship Radar Market Trends & Insights

The Ship Radar market is undergoing significant transformation driven by technological advancements and evolving maritime requirements. Users frequently inquire about the integration of advanced digital signal processing, the increasing adoption of solid-state technology, and the shift towards multi-functional radar systems that offer enhanced capabilities beyond basic navigation. There is a strong interest in how these trends are contributing to improved situational awareness, collision avoidance, and overall operational efficiency for various vessel types.

Furthermore, the market is observing a push for greater automation and interoperability within maritime navigation systems. Questions often arise regarding the development of miniaturized radar solutions for smaller vessels and unmanned surface vehicles (USVs), as well as the impact of stringent regulatory standards on radar design and implementation. The demand for higher resolution and more reliable target detection, particularly in challenging weather conditions, continues to shape product development and market dynamics.

- Growing adoption of solid-state radar technology for enhanced reliability and lower maintenance.

- Integration of multi-functional radar systems combining navigation, weather, and security surveillance.

- Increased demand for high-resolution radar for improved target discrimination and situational awareness.

- Development of compact and lightweight radar solutions for smaller vessels and autonomous platforms.

- Emphasis on digital signal processing and advanced algorithms for superior performance in complex environments.

- Greater interoperability and integration with other bridge systems like ECDIS and AIS.

- Rise of networked radar systems enabling data sharing and collaborative navigation.

AI Impact Analysis on Ship Radar

The impact of Artificial Intelligence (AI) on ship radar technology is a significant area of user interest, with many questions focusing on its potential to revolutionize maritime safety and operational efficiency. Users are keenly interested in how AI can enhance radar capabilities, particularly in areas like advanced target detection, classification, and tracking, moving beyond traditional radar limitations. The discussion often centers on AI's role in improving the accuracy of collision avoidance systems, predicting vessel movements, and processing vast amounts of environmental data to provide more insightful navigation recommendations.

Furthermore, there is considerable anticipation regarding AI's contribution to autonomous shipping and the development of intelligent navigation systems. Common inquiries include the application of machine learning for anomaly detection, predictive maintenance of radar components, and real-time decision support for crew members. Concerns also exist around data security, the reliability of AI algorithms in critical situations, and the regulatory framework required to govern AI-powered radar systems, highlighting a balance between innovation and responsible deployment.

- Enhanced target detection and classification through machine learning algorithms.

- Improved collision avoidance systems with predictive analysis of vessel trajectories.

- Real-time environmental monitoring and hazard identification using AI-driven data fusion.

- Automated anomaly detection for suspicious activities or unusual vessel behavior.

- Predictive maintenance for radar components, reducing downtime and operational costs.

- Support for autonomous navigation systems by providing more accurate and intelligent sensor data.

- Integration with other sensor data (e.g., cameras, LIDAR) for a comprehensive situational picture.

Key Takeaways Ship Radar Market Size & Forecast

Analyzing the Ship Radar market size and forecast reveals several critical insights that shape future investment and strategic planning. Users frequently seek to understand the primary forces driving market expansion, such as the increasing global maritime trade and the continuous modernization of naval fleets. A key takeaway is the consistent demand for advanced navigation and safety systems, which directly fuels the growth of radar technology across commercial, defense, and leisure maritime sectors. The projected growth indicates a robust market with sustained opportunities for innovation and expansion.

Another significant insight derived from the forecast is the pivotal role of technological advancements, particularly in areas like solid-state radar and AI integration, in shaping the market's trajectory. These innovations are not only improving performance but also expanding the addressable market by enabling more compact and versatile solutions. Furthermore, the forecast highlights the increasing importance of regional maritime safety regulations and defense spending as catalysts for market uptake, especially in emerging maritime economies.

- The market is poised for significant growth, driven by increasing maritime traffic and safety regulations.

- Technological advancements, including solid-state and AI integration, are key growth enablers.

- Commercial shipping and naval applications remain the largest demand segments for radar systems.

- Asia Pacific is expected to emerge as a dominant region due to expanding trade and naval modernization.

- The emphasis on autonomous vessels and enhanced maritime security will fuel future radar innovations.

- High initial investment costs and regulatory complexities present ongoing challenges.

- Opportunities exist in retrofitting older fleets and developing specialized radar for niche applications.

Ship Radar Market Drivers Analysis

The Ship Radar market is propelled by a confluence of factors that underscore its critical role in modern maritime operations. A primary driver is the increasing volume of global maritime trade, necessitating robust navigation and safety systems for efficient port operations and safe passage through busy shipping lanes. This surge in commercial shipping inherently demands more sophisticated radar solutions to prevent collisions, navigate complex waterways, and optimize vessel movements.

Furthermore, the growing emphasis on maritime security and defense modernization significantly contributes to market growth. Naval forces worldwide are investing in advanced radar systems for surveillance, target acquisition, and weapon guidance, reflecting an evolving threat landscape. Simultaneously, stringent international maritime regulations, such as those from the International Maritime Organization (IMO) concerning navigation safety and environmental protection, mandate the use of reliable radar systems, thereby ensuring continuous demand and technological upgrades.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Maritime Trade | +2.1% | Asia Pacific, Europe, North America | 2025-2033 |

| Growing Demand for Maritime Security & Defense | +1.8% | North America, Europe, Asia Pacific (China, India) | 2025-2033 |

| Strict Regulatory Standards for Navigation Safety | +1.5% | Global (IMO, National Authorities) | Ongoing |

| Technological Advancements in Radar Systems | +1.3% | Global | 2025-2033 |

| Rising Adoption of Autonomous Vessels | +1.1% | Europe, North America, Japan, South Korea | 2028-2033 |

Ship Radar Market Restraints Analysis

Despite significant growth drivers, the Ship Radar market faces several notable restraints that could temper its expansion. One primary challenge is the high initial investment required for advanced radar systems, which can be prohibitive for smaller shipping companies or specific vessel types. This capital expenditure includes not only the cost of the radar unit itself but also installation, integration with existing bridge systems, and necessary crew training, posing a barrier to widespread adoption, particularly in developing economies.

Another significant restraint is the complexity associated with integrating new, sophisticated radar technologies into legacy maritime infrastructures. Older vessels often lack the digital architecture or sensor compatibility required for seamless integration, leading to costly retrofitting challenges. Furthermore, concerns regarding cybersecurity vulnerabilities within increasingly networked and data-intensive radar systems represent a growing constraint, as potential threats to navigation data and system integrity could have severe consequences for maritime safety and operations.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Installation Costs | -1.2% | Global, particularly SMEs in developing regions | 2025-2033 |

| Complexity of Integration with Legacy Systems | -0.9% | Global (Older fleets) | 2025-2033 |

| Cybersecurity Concerns and Data Vulnerabilities | -0.8% | Global | 2025-2033 |

| Shortage of Skilled Personnel for Operation & Maintenance | -0.7% | Global | 2025-2033 |

| Economic Downturns and Fluctuations in Trade | -0.5% | Global | Short to Medium-term |

Ship Radar Market Opportunities Analysis

The Ship Radar market is rich with emerging opportunities driven by innovation, evolving maritime practices, and expanding operational frontiers. A prominent opportunity lies in the accelerating development and adoption of autonomous and semi-autonomous vessels across various maritime sectors. These vessels require highly advanced, reliable, and integrated radar systems for comprehensive environmental perception and independent navigation, creating a substantial demand for next-generation radar technologies.

Another significant area of opportunity is the increasing exploration and commercial activity in challenging environments, such as the Arctic routes. These regions demand specialized radar systems capable of operating reliably in extreme weather conditions, detecting icebergs, and navigating through low visibility. Furthermore, the growing trend of multi-sensor fusion, where radar data is combined with inputs from LIDAR, cameras, and sonar, presents opportunities for developing integrated perception systems that offer unparalleled situational awareness and enhance overall maritime safety and efficiency.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Autonomous and Unmanned Vessels | +1.9% | Europe, North America, East Asia | 2026-2033 |

| Expansion of Arctic Shipping Routes | +1.4% | Russia, Canada, Nordic Countries, China | 2027-2033 |

| Demand for Multi-Sensor Fusion Systems | +1.2% | Global | 2025-2033 |

| Retrofitting and Modernization of Existing Fleets | +1.0% | Global (Mature economies) | 2025-2030 |

| Development of Specialized Radar for Niche Applications (e.g., Wind Farms) | +0.8% | Europe, North Sea, Asia Pacific | 2025-2033 |

Ship Radar Market Challenges Impact Analysis

The Ship Radar market faces several critical challenges that require strategic solutions and technological innovation. One significant hurdle is the rapid pace of technological obsolescence, where advanced radar systems can quickly become outdated due to continuous innovation in signal processing, material science, and digital integration. This forces manufacturers and operators to constantly invest in research and development or risk falling behind competitors and regulatory requirements, impacting long-term planning and investment returns.

Another challenge is the increasing complexity of electromagnetic interference (EMI) in congested maritime environments, which can degrade radar performance and reliability. With a proliferation of various electronic systems on vessels and at sea, ensuring clear and accurate radar readings amidst a cluttered electromagnetic spectrum becomes increasingly difficult. Furthermore, global supply chain disruptions, as experienced in recent years, pose a continuous challenge to the manufacturing and timely delivery of radar components, leading to production delays and increased costs across the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Upgrade Cycles | -1.1% | Global | Ongoing |

| Electromagnetic Interference in Congested Areas | -0.9% | Coastal areas, Busy shipping lanes | 2025-2033 |

| High Research & Development Costs for Innovation | -0.8% | Global | 2025-2033 |

| Supply Chain Disruptions and Component Shortages | -0.6% | Global | Short to Medium-term |

| Adapting to Evolving Regulatory and Certification Standards | -0.5% | Global | Ongoing |

Ship Radar Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Ship Radar Market, offering an in-depth analysis of its current size, historical performance, and future growth projections through 2033. The scope encompasses detailed segmentation by radar type, component, application, and end-user, providing a granular understanding of market composition and opportunities. Furthermore, it examines the critical drivers, restraints, opportunities, and challenges influencing market trajectory, along with a comprehensive regional analysis and profiles of key industry players.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.2 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Company Alpha, Company Beta, Company Gamma, Company Delta, Company Epsilon, Company Zeta, Company Eta, Company Theta, Company Iota, Company Kappa, Company Lambda, Company Mu, Company Nu, Company Xi, Company Omicron |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Ship Radar market is comprehensively segmented to provide a detailed understanding of its diverse applications and technological variations. This segmentation highlights the various categories of radar systems, their core components, the specific maritime applications they serve, and the wide array of end-users across the global shipping industry. Understanding these segments is crucial for identifying key growth areas and tailoring solutions to specific market needs, from commercial shipping to defense and leisure activities.

Each segment presents distinct opportunities and challenges, reflecting varied operational requirements and regulatory landscapes. For instance, the demand for X-Band radar is prominent in navigation for its high resolution, while S-Band radar is preferred for its longer range and better performance in adverse weather. Similarly, advancements in components like transceivers and processors are driving innovation across all applications, from critical collision avoidance systems to sophisticated port traffic management and maritime surveillance.

- By Type: X-Band Radar, S-Band Radar, Ku-Band Radar, Others (e.g., L-band for specialized applications)

- By Component: Transceivers, Antennas, Displays, Processors, Power Supplies, Software & Algorithms, Other Peripherals

- By Application: Navigation & Collision Avoidance, Weather Monitoring, Port Traffic Management (VTS), Surveillance & Security, Search & Rescue, Ice Detection, Oil Spill Detection

- By End-User: Merchant Vessels (Tankers, Cargo Ships, Bulk Carriers), Naval Vessels (Warships, Patrol Boats), Fishing Boats, Passenger & Cruise Ships, Leisure Boats & Yachts, Offshore Vessels, Autonomous Surface Vessels (ASVs)

Regional Highlights

- North America: This region demonstrates a robust market, driven by significant defense spending and ongoing naval modernization programs. The presence of major technology developers and a strong focus on autonomous shipping initiatives also contribute to its growth. Furthermore, increasing commercial traffic in key coastal areas and inland waterways necessitates advanced radar systems for safety and efficiency.

- Europe: Europe is a mature market characterized by stringent maritime regulations and a strong emphasis on environmental protection and safety. The region is a hub for maritime technological innovation, with high adoption rates of solid-state radar and integrated bridge systems. Investments in offshore wind farms and renewable energy projects also generate demand for specialized radar solutions.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, primarily due to the rapid expansion of maritime trade, substantial investments in port infrastructure, and increasing naval capabilities of countries like China, India, and Japan. The burgeoning shipbuilding industry and growing demand for advanced navigation systems for commercial fleets significantly contribute to market acceleration.

- Latin America: This region presents emerging opportunities, particularly with the expansion of maritime trade routes and the modernization of local naval forces. Investment in port infrastructure development and increasing concerns over maritime security also drive the adoption of radar technologies, although market growth may be tempered by economic volatilities in some countries.

- Middle East and Africa (MEA): The MEA market is driven by strategic geopolitical importance, significant oil and gas transportation activities, and increasing investments in maritime security. Countries in the Middle East are heavily investing in naval modernization and coastal surveillance systems, while African nations are focusing on securing their extensive coastlines against piracy and illegal activities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Ship Radar Market.- Company Alpha

- Company Beta

- Company Gamma

- Company Delta

- Company Epsilon

- Company Zeta

- Company Eta

- Company Theta

- Company Iota

- Company Kappa

- Company Lambda

- Company Mu

- Company Nu

- Company Xi

- Company Omicron

- Company Pi

- Company Rho

- Company Sigma

- Company Tau

- Company Upsilon

Frequently Asked Questions

What is a ship radar and how does it function?

A ship radar is an electronic navigation instrument that uses radio waves to detect and locate other ships, landmasses, navigational hazards, and weather formations. It operates by transmitting pulses of electromagnetic energy and receiving the echoes reflected from objects. The time taken for the echo to return, combined with the direction from which it arrived, allows the radar to calculate the range and bearing of the detected objects, displaying them on a screen for navigational purposes. This real-time information is crucial for collision avoidance and safe passage.

What are the primary types of ship radar used in the maritime industry?

The maritime industry primarily utilizes two main types of ship radar: X-Band and S-Band. X-Band radar operates at a higher frequency, providing excellent resolution for distinguishing small targets and navigating in congested waterways, often used for coastal navigation and collision avoidance. S-Band radar operates at a lower frequency, offering better performance in adverse weather conditions like heavy rain or fog, and a longer detection range, making it suitable for open-sea navigation and early detection of larger vessels or landmasses. Some specialized applications may also use Ku-Band or L-Band radar.

Why is ship radar essential for maritime safety and operations?

Ship radar is indispensable for maritime safety and operations as it provides critical situational awareness, especially in conditions of poor visibility, at night, or in heavy traffic areas. It enables vessels to detect and track other ships, fixed objects, and land, preventing collisions and grounding. Beyond navigation, radar systems also support weather monitoring, port traffic management, security surveillance, and search and rescue operations, ensuring efficient and secure maritime transport.

How is AI impacting the future development of ship radar?

Artificial Intelligence (AI) is significantly enhancing ship radar by improving target detection, classification, and tracking capabilities. AI algorithms can analyze vast amounts of radar data to differentiate between various types of objects, filter out clutter, and predict movements more accurately than traditional systems. This leads to more intelligent collision avoidance, enhanced autonomous navigation, and real-time decision support for crews, paving the way for safer and more efficient maritime operations.

What are the key trends driving innovation in the ship radar market?

Key trends driving innovation in the ship radar market include the widespread adoption of solid-state technology for increased reliability and reduced maintenance, the development of multi-functional radar systems that integrate various capabilities like navigation and surveillance, and the miniaturization of radar units for smaller vessels and unmanned platforms. Furthermore, the integration of advanced digital signal processing, AI for enhanced data analysis, and a focus on cybersecurity are shaping the next generation of radar solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted