Sheet Metal Market

Sheet Metal Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703460 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Sheet Metal Market Size

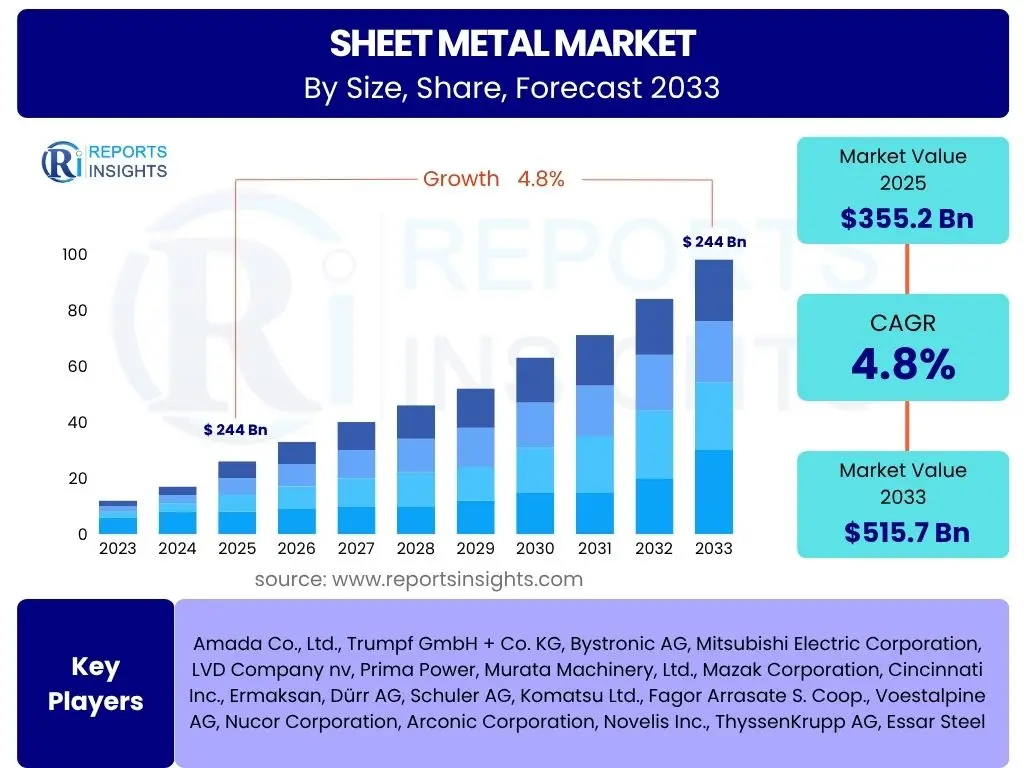

According to Reports Insights Consulting Pvt Ltd, The Sheet Metal Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 355.2 Billion in 2025 and is projected to reach USD 515.7 Billion by the end of the forecast period in 2033.

Key Sheet Metal Market Trends & Insights

The sheet metal market is currently experiencing significant transformative trends driven by technological advancements and evolving industrial demands. Key insights reveal a strong move towards enhanced automation and digitalization, enabling greater precision, efficiency, and reduced waste in manufacturing processes. This shift is particularly evident in the adoption of Industry 4.0 principles, integrating smart factories with interconnected systems. Furthermore, a growing emphasis on sustainable manufacturing practices, including the use of recyclable materials and energy-efficient production methods, is shaping market dynamics, responding to increasing environmental regulations and consumer preferences for eco-friendly products.

Another prominent trend is the increasing demand for customized and specialized sheet metal components across various end-use industries, such as automotive, aerospace, and electronics. This necessitates agile manufacturing processes capable of rapid prototyping and high-mix, low-volume production. The development and adoption of advanced alloys and materials, offering superior strength-to-weight ratios and corrosion resistance, are also contributing to the innovation landscape, enabling new applications and improving product performance. These trends collectively underscore a market moving towards greater technological sophistication, environmental responsibility, and responsiveness to intricate market needs.

- Digitalization and Industry 4.0 Integration: Increasing adoption of smart manufacturing, IoT, and data analytics in production.

- Automation and Robotics: Greater use of automated machinery and robotic systems for enhanced precision and efficiency.

- Sustainable Manufacturing Practices: Emphasis on recycling, waste reduction, and energy-efficient production methods.

- Demand for Lightweight Materials: Growing preference for materials like aluminum and advanced high-strength steel in automotive and aerospace.

- Customization and Personalization: Rising need for tailor-made sheet metal components for niche applications.

- Advanced Forming Technologies: Evolution of processes such as hydroforming, superplastic forming, and roll forming.

- Global Supply Chain Optimization: Efforts to enhance resilience and efficiency in the international supply of raw materials and finished goods.

- Emergence of Smart Buildings and Infrastructure: Driving demand for sheet metal in HVAC systems, roofing, and structural elements.

AI Impact Analysis on Sheet Metal

Artificial Intelligence (AI) is poised to revolutionize the sheet metal industry by optimizing design, production, and supply chain operations. User inquiries often center on how AI can enhance efficiency, reduce costs, and improve quality. AI algorithms can analyze vast datasets from manufacturing processes to predict material behavior, optimize cutting paths, and identify potential defects before they occur, leading to significant material waste reduction and increased yield. This predictive capability extends to machine maintenance, where AI-driven monitoring can anticipate equipment failures, enabling proactive interventions and minimizing costly downtime, thereby addressing common concerns regarding operational efficiency and throughput.

Furthermore, AI facilitates advanced automation and robotics in sheet metal fabrication, allowing for more complex and precise operations with less human intervention. Users are interested in AI's role in design optimization, where generative design tools can rapidly create multiple design iterations, considering material properties and manufacturing constraints to achieve optimal performance and manufacturability. The integration of AI in quality control, through machine vision and anomaly detection, ensures consistent product quality, while its application in supply chain management helps in demand forecasting, inventory optimization, and logistics planning. These applications collectively signify a shift towards more intelligent, adaptive, and autonomous sheet metal manufacturing environments, promising substantial improvements across the value chain.

- Design Optimization: AI-powered generative design for lightweighting and material efficiency.

- Predictive Maintenance: AI algorithms analyze machine data to anticipate equipment failures, reducing downtime.

- Quality Control: Machine learning for real-time defect detection and quality assurance in production.

- Automated Welding and Bending: AI integration in robotic systems for enhanced precision and adaptability.

- Supply Chain Optimization: AI for demand forecasting, inventory management, and logistics planning.

- Process Optimization: AI-driven analysis of manufacturing data to improve efficiency and reduce waste.

- Energy Management: AI tools to monitor and optimize energy consumption in sheet metal factories.

- Workforce Training and Augmentation: AI-powered simulations for training and augmented reality tools for workers.

Key Takeaways Sheet Metal Market Size & Forecast

The sheet metal market is set for robust expansion through 2033, driven by increasing industrialization and technological advancements across various sectors. The projected significant growth from USD 355.2 Billion in 2025 to USD 515.7 Billion by 2033, at a CAGR of 4.8%, underscores a healthy and dynamic industry. This growth is primarily fueled by consistent demand from vital end-use industries such as automotive, construction, and electronics, alongside emerging applications in renewable energy and electric vehicles. The market's resilience is evident in its ability to integrate new technologies, particularly automation and digitalization, to enhance production capabilities and meet evolving customer requirements for precision and customization.

Despite potential challenges related to raw material price volatility and environmental regulations, opportunities arising from sustainable practices and the development of advanced materials are expected to mitigate these pressures. The emphasis on lightweighting, driven by fuel efficiency and performance demands, especially in transportation, will continue to be a crucial growth vector. Geographically, Asia Pacific is anticipated to remain a dominant force due to rapid industrial development and urbanization, while mature markets in North America and Europe will focus on technological innovation and high-value applications. The overall outlook suggests a progressive market, characterized by innovation, efficiency improvements, and a strategic response to global sustainability imperatives.

- Significant Market Expansion: Expected to grow from USD 355.2 Billion in 2025 to USD 515.7 Billion by 2033.

- Consistent CAGR: Projected at 4.8%, indicating stable and sustained growth.

- Driving Sectors: Strong demand from automotive, construction, electronics, and industrial machinery.

- Technological Integration: Increasing adoption of automation, AI, and Industry 4.0 principles to boost efficiency.

- Focus on Lightweighting: Continuous demand for lighter and stronger materials, particularly in transportation.

- Sustainability Imperatives: Growing emphasis on eco-friendly production methods and recyclable materials.

- Regional Dynamics: Asia Pacific leads in growth, while North America and Europe focus on innovation.

- Emerging Opportunities: Growth in electric vehicles, renewable energy, and customized solutions.

Sheet Metal Market Drivers Analysis

The sheet metal market's expansion is fundamentally propelled by the robust and continuous demand from its key end-use industries. The automotive sector, for instance, heavily relies on sheet metal for vehicle bodies, chassis, and various structural components, with the global shift towards electric vehicles further stimulating demand for lightweight and high-strength materials. Similarly, the burgeoning construction industry utilizes sheet metal for roofing, cladding, HVAC systems, and architectural elements in both residential and commercial projects, driven by urbanization and infrastructure development worldwide. The industrial machinery and equipment sector, encompassing everything from agricultural machinery to heavy manufacturing tools, also represents a significant consumer, requiring durable and precisely fabricated sheet metal parts.

Beyond traditional industrial demand, technological advancements and the pursuit of efficiency are also acting as critical drivers. Innovations in manufacturing processes, such as high-speed laser cutting, advanced bending techniques, and automated welding, enable producers to deliver complex geometries with higher precision and faster turnaround times. Furthermore, the increasing global focus on energy efficiency and sustainability promotes the adoption of lightweight sheet metal alloys, reducing material consumption and improving operational performance in end products. The expansion of electronics manufacturing, particularly in consumer goods and telecommunications infrastructure, equally contributes to market growth by requiring intricate and high-quality sheet metal enclosures and components.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Automotive & Transportation Sector | +1.2% | Global, particularly Asia Pacific, North America, Europe | 2025-2033 |

| Increasing Construction & Infrastructure Development | +1.0% | Asia Pacific, Middle East & Africa, Latin America | 2025-2033 |

| Rise in Industrial Machinery & Equipment Manufacturing | +0.8% | North America, Europe, Asia Pacific | 2025-2033 |

| Technological Advancements in Fabrication Processes | +0.7% | Global | 2025-2033 |

| Demand for Lightweight & High-Strength Materials | +0.6% | Global | 2025-2033 |

Sheet Metal Market Restraints Analysis

The sheet metal market faces several significant restraints that can impede its growth trajectory. One of the primary concerns is the inherent volatility of raw material prices, particularly for steel, aluminum, and copper. Fluctuations in global commodity markets, geopolitical tensions, and supply chain disruptions can lead to unpredictable material costs, directly impacting manufacturing profitability and pricing strategies. Such unpredictability makes long-term planning challenging for manufacturers and can force them to absorb costs or pass them on to consumers, potentially affecting demand. This economic instability is a constant source of concern for market participants across all regions, necessitating robust risk management strategies.

Another considerable restraint is the increasing stringency of environmental regulations and sustainability mandates globally. While promoting responsible manufacturing, these regulations often necessitate substantial investments in new technologies, waste management systems, and compliance measures. This can increase operational costs, particularly for smaller and medium-sized enterprises (SMEs) that may struggle to meet the financial burden of upgrading their facilities and processes. Furthermore, the sheet metal industry, being capital-intensive, requires significant upfront investment in high-precision machinery, automation, and advanced software, which can be a barrier to entry for new players and limit expansion for existing ones, especially in regions with limited access to capital or credit. The shortage of skilled labor, particularly in specialized areas like precision welding and CNC programming, also acts as a bottleneck, affecting production capacity and efficiency across key manufacturing hubs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices | -0.9% | Global | 2025-2033 |

| Stringent Environmental Regulations | -0.7% | Europe, North America, specific Asian countries | 2025-2033 |

| High Capital Investment Requirements | -0.6% | Global, particularly developing regions | 2025-2033 |

| Shortage of Skilled Labor | -0.5% | North America, Europe, parts of Asia | 2025-2033 |

| Economic Slowdowns & Geopolitical Instability | -0.4% | Global, variable by region | 2025-2033 |

Sheet Metal Market Opportunities Analysis

Despite the challenges, the sheet metal market is ripe with opportunities driven by emerging technologies and evolving industry landscapes. One significant opportunity lies in the burgeoning electric vehicle (EV) market. EVs require substantial amounts of lightweight sheet metal for battery enclosures, body structures, and other components to maximize range and efficiency. This shift away from traditional internal combustion engines presents a sustained and growing demand for advanced aluminum and high-strength steel alloys. Similarly, the rapid expansion of the renewable energy sector, encompassing solar panels, wind turbines, and energy storage systems, offers new avenues for sheet metal applications, particularly in support structures, casings, and electrical enclosures. These sectors are global in nature, opening up substantial new market segments for sheet metal manufacturers capable of meeting specific material and design requirements.

Furthermore, the ongoing digitalization of manufacturing, often referred to as Industry 4.0, provides a wealth of opportunities for process optimization and new service offerings. The integration of advanced analytics, artificial intelligence, and machine learning into sheet metal fabrication processes can lead to unprecedented levels of precision, waste reduction, and predictive maintenance. This enables manufacturers to offer more customized and complex components with faster lead times, catering to niche market demands and high-value applications. The increasing adoption of smart building technologies also creates opportunities for sheet metal in HVAC systems, intelligent facades, and integrated architectural solutions. Lastly, the push for circular economy principles encourages innovation in recycling and material reuse, potentially reducing reliance on virgin materials and creating more sustainable and cost-effective production models.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicle (EV) Manufacturing | +1.1% | Global, especially China, Europe, North America | 2025-2033 |

| Expansion of Renewable Energy Sector | +0.9% | Europe, North America, Asia Pacific | 2025-2033 |

| Adoption of Industry 4.0 and Smart Manufacturing | +0.8% | Global, particularly developed economies | 2025-2033 |

| Increasing Demand for Custom Fabrication | +0.7% | Global | 2025-2033 |

| Development of Advanced & Hybrid Materials | +0.6% | Global | 2025-2033 |

Sheet Metal Market Challenges Impact Analysis

The sheet metal market confronts several significant challenges that demand strategic responses from manufacturers. One of the most persistent issues is the global supply chain vulnerability, which became acutely evident during recent geopolitical events and the pandemic. Disruptions in the availability and transportation of raw materials, such as steel and aluminum, lead to production delays, increased costs, and ultimately, impact delivery schedules for end products. This necessitates diversified sourcing strategies and greater regionalization of supply chains to build resilience against external shocks. Furthermore, the inherent intensity of competition within the sheet metal fabrication sector, especially for standard parts, puts constant downward pressure on pricing, making it challenging for companies to maintain healthy profit margins without continuous innovation and efficiency gains.

Another critical challenge stems from the rapid pace of technological advancements. While new technologies offer opportunities, they also require significant investment in upgrading machinery, software, and workforce skills. Companies that fail to adapt to innovations like advanced automation, AI integration, and new forming processes risk falling behind competitors. This is exacerbated by the ongoing shortage of skilled labor, particularly in roles requiring expertise in operating complex CNC machines, robotic welders, and precision measurement equipment. Attracting and retaining talent capable of navigating these advanced manufacturing environments remains a formidable hurdle across many regions. Lastly, the industry faces increasing pressure to minimize environmental impact, including managing waste effectively and reducing energy consumption. Compliance with evolving sustainability standards and the transition to more eco-friendly production methods add another layer of complexity and cost to operations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions | -0.8% | Global | 2025-2033 |

| Intense Competitive Landscape | -0.7% | Global | 2025-2033 |

| Rapid Technological Obsolescence | -0.6% | Global, particularly developed economies | 2025-2033 |

| Environmental Compliance & Waste Management | -0.5% | Europe, North America, specific Asian countries | 2025-2033 |

| Fluctuating Energy Costs | -0.4% | Global, variable by region | 2025-2033 |

Sheet Metal Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global Sheet Metal Market, offering an updated and detailed analysis of its size, trends, and future projections. The scope of the report encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, providing a holistic view of the forces shaping the industry. It also includes an in-depth segmentation analysis by material, end-use industry, process, and application, alongside a comprehensive regional outlook, to identify key growth areas and investment opportunities. Furthermore, the report assesses the impact of emerging technologies like Artificial Intelligence on market evolution, offering strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 355.2 Billion |

| Market Forecast in 2033 | USD 515.7 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 250 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Amada Co., Ltd., Trumpf GmbH + Co. KG, Bystronic AG, Mitsubishi Electric Corporation, LVD Company nv, Prima Power, Murata Machinery, Ltd., Mazak Corporation, Cincinnati Inc., Ermaksan, Dürr AG, Schuler AG, Komatsu Ltd., Fagor Arrasate S. Coop., Voestalpine AG, Nucor Corporation, Arconic Corporation, Novelis Inc., ThyssenKrupp AG, Essar Steel |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The sheet metal market is comprehensively segmented to provide a granular understanding of its diverse applications and material preferences. This detailed breakdown allows for a precise analysis of demand patterns and technological advancements across various sectors. The primary segmentation by material includes steel, aluminum, copper, brass, and titanium, each possessing unique properties that dictate their suitability for specific applications. Steel, particularly stainless and galvanized variants, dominates due to its strength and cost-effectiveness, while aluminum gains traction for its lightweight properties, crucial in automotive and aerospace industries. Copper and brass are valued for their conductivity and corrosion resistance, essential in electronics and plumbing, respectively.

Further segmentation by end-use industry highlights the critical role of sheet metal in sectors such as automotive, construction, electronics, and industrial machinery. The automotive sector, for instance, drives demand for advanced high-strength steels and aluminum for vehicle body-in-white structures and chassis. Construction utilizes sheet metal extensively for roofing, facades, and HVAC systems. Electronics and industrial machinery rely on precise sheet metal enclosures and components for protection and functionality. Segmentation by process, including stamping, bending, shearing, and laser cutting, reflects the varied manufacturing techniques employed, while application-based segmentation (e.g., structural components, enclosures) clarifies the end-use of fabricated sheet metal products. This multi-faceted segmentation provides a robust framework for understanding the market's complexities and identifying specific growth niches.

- By Material:

- Steel (Stainless Steel, Carbon Steel, Galvanized Steel)

- Aluminum

- Copper

- Brass

- Titanium

- Others (e.g., Nickel Alloys, Zinc)

- By End-Use Industry:

- Automotive

- Construction

- Electronics

- Industrial Machinery

- Aerospace & Defense

- HVAC (Heating, Ventilation, and Air Conditioning)

- Others (e.g., Medical Devices, Consumer Goods, Appliances)

- By Process:

- Stamping

- Bending

- Shearing

- Punching

- Welding

- Laser Cutting

- Plasma Cutting

- Waterjet Cutting

- Roll Forming

- Hydroforming

- Others (e.g., Deep Drawing, Spinning)

- By Application:

- Structural Components

- Enclosures & Casings

- Frames & Chassis

- Decorative Elements

- Piping & Ducting

- Panels & Roofing

- Components for Appliances

- Others

Regional Highlights

- North America: This region represents a mature yet innovative market for sheet metal, characterized by a strong emphasis on automation, advanced manufacturing techniques, and high-value applications. Demand is primarily driven by the robust automotive, aerospace & defense, and industrial machinery sectors. There is a growing focus on lightweighting materials and precision fabrication, with significant investments in Industry 4.0 technologies. The region also sees increased demand for custom fabrication services and environmentally compliant solutions.

- Europe: Europe is a hub for technological innovation in sheet metal processing, with stringent environmental regulations driving the adoption of sustainable practices and advanced material recycling. Key drivers include the automotive industry, particularly the transition to electric vehicles, and robust manufacturing in industrial machinery and construction. Germany, Italy, and France are significant contributors, known for their advanced machinery and high-quality production. The region shows strong interest in smart factory solutions and energy-efficient processes.

- Asia Pacific (APAC): APAC is the largest and fastest-growing market for sheet metal, fueled by rapid industrialization, urbanization, and a booming manufacturing sector, especially in China, India, Japan, and South Korea. The region benefits from increasing demand in automotive, electronics, and construction industries. It serves as a global manufacturing base, driving significant volumes of sheet metal production and consumption. Investments in advanced manufacturing technologies and automation are rapidly increasing to enhance competitive advantages and meet rising domestic and international demand.

- Latin America: This region presents emerging opportunities for the sheet metal market, driven by infrastructure development projects, growth in the automotive sector (particularly in Brazil and Mexico), and expanding industrial base. While still developing compared to other regions, there is a steady increase in demand for sheet metal in construction and manufacturing. Investments in modernizing manufacturing facilities are underway, aiming to improve efficiency and quality.

- Middle East & Africa (MEA): The MEA region is witnessing significant growth in the construction and infrastructure sectors, particularly in the GCC countries, which is a major driver for sheet metal demand. Diversification of economies away from oil dependence is leading to increased industrial activity and manufacturing investments. Sheet metal is extensively used in large-scale commercial and residential projects, as well as in the development of new industrial zones and smart cities. However, market growth can be influenced by regional geopolitical stability and fluctuating oil prices.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Sheet Metal Market.- Amada Co., Ltd.

- Trumpf GmbH + Co. KG

- Bystronic AG

- Mitsubishi Electric Corporation

- LVD Company nv

- Prima Power

- Murata Machinery, Ltd.

- Mazak Corporation

- Cincinnati Inc.

- Ermaksan

- Dürr AG

- Schuler AG

- Komatsu Ltd.

- Fagor Arrasate S. Coop.

- Voestalpine AG

- Nucor Corporation

- Arconic Corporation

- Novelis Inc.

- ThyssenKrupp AG

- Essar Steel

Frequently Asked Questions

What is sheet metal and what are its primary uses?

Sheet metal is metal formed into thin, flat pieces or coils, widely used in various industries. Its primary uses include manufacturing components for automotive bodies, aircraft parts, construction materials (e.g., roofing, HVAC ducts), industrial machinery casings, electronic enclosures, and consumer appliances. Its versatility allows for bending, cutting, and shaping into complex forms.

What are the key factors driving the growth of the sheet metal market?

Key drivers include robust demand from the automotive, construction, and electronics industries, rapid urbanization, increasing infrastructure development, and continuous technological advancements in manufacturing processes like automation and laser cutting. The growing adoption of lightweight materials for fuel efficiency also contributes significantly to market expansion.

What challenges does the sheet metal industry face?

The sheet metal industry faces challenges such as the volatility of raw material prices, stringent environmental regulations requiring costly compliance, high capital investment for advanced machinery, and a persistent shortage of skilled labor. Global supply chain disruptions and intense market competition also pose significant hurdles.

How is technology impacting the sheet metal market?

Technology is profoundly impacting the sheet metal market by enabling greater precision, efficiency, and customization. This includes the integration of Industry 4.0 principles, artificial intelligence (AI) for design optimization and predictive maintenance, advanced automation and robotics, and sophisticated software for simulation and production planning. These innovations lead to higher quality products and reduced waste.

Which regions are key contributors to the sheet metal market?

Asia Pacific (APAC) is the largest and fastest-growing market due to rapid industrialization and manufacturing activities in countries like China and India. North America and Europe are significant contributors, known for technological innovation, high-value production, and demand from mature industries. Latin America and the Middle East & Africa are emerging markets driven by infrastructure development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted