Sheet Metal Fabrication Service Market

Sheet Metal Fabrication Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709150 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Sheet Metal Fabrication Service Market Size

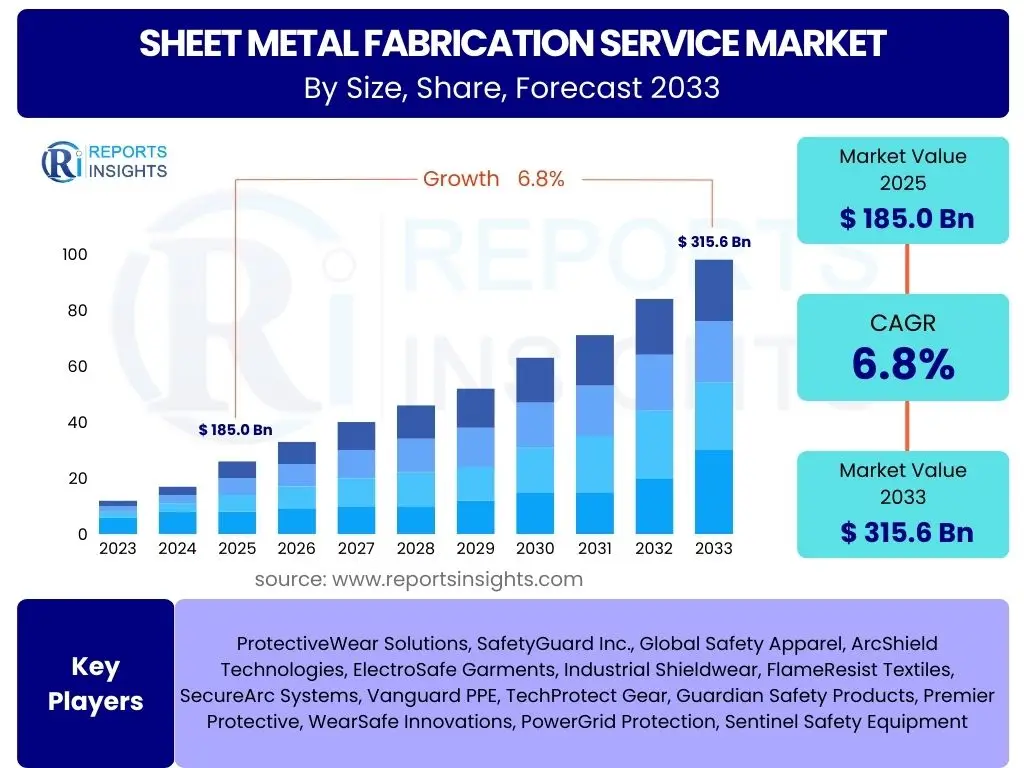

According to Reports Insights Consulting Pvt Ltd, The Sheet Metal Fabrication Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 185.0 Billion in 2025 and is projected to reach USD 315.6 Billion by the end of the forecast period in 2033.

Key Sheet Metal Fabrication Service Market Trends & Insights

The sheet metal fabrication service market is currently experiencing significant transformative trends driven by technological advancements and evolving industry demands. One prominent trend is the increasing adoption of automation and robotics, which enhances precision, efficiency, and safety in manufacturing processes. This shift is crucial for companies aiming to reduce labor costs and improve production throughput, addressing the growing need for high-volume, consistent output in various end-use sectors.

Another key insight is the accelerating demand for customized and on-demand fabrication solutions. Industries are moving away from mass production of standardized components towards tailored parts that meet specific design requirements and functional specifications. This trend is supported by advancements in CAD/CAM software and flexible manufacturing systems, enabling rapid prototyping and short-run production with minimal setup times. Furthermore, sustainability and material efficiency are becoming critical considerations, driving the adoption of practices that minimize waste and optimize material usage, reflecting a broader industry commitment to environmental responsibility.

The integration of advanced materials, such as high-strength steel alloys and lightweight aluminum composites, is also shaping the market. These materials offer superior performance characteristics, including improved strength-to-weight ratios and enhanced corrosion resistance, which are particularly valued in industries like aerospace, automotive, and defense. Additionally, the globalization of supply chains continues to influence market dynamics, with companies seeking to establish resilient and localized production networks to mitigate risks associated with international trade disruptions and geopolitical instabilities, emphasizing regional manufacturing capabilities.

- Increased automation and robotic integration in manufacturing.

- Growing demand for customized and on-demand fabrication.

- Emphasis on sustainable and eco-friendly manufacturing processes.

- Adoption of advanced materials like high-strength alloys and composites.

- Digitalization of design and production workflows (Industry 4.0 integration).

- Shift towards localized and resilient supply chain strategies.

- Focus on precision and quality control through advanced inspection systems.

AI Impact Analysis on Sheet Metal Fabrication Service

Artificial intelligence (AI) is poised to revolutionize the sheet metal fabrication service sector by introducing unprecedented levels of efficiency, precision, and operational intelligence. Users are keenly interested in how AI can optimize production processes, with common questions revolving around its application in predictive maintenance, quality control, and automated design. AI algorithms can analyze real-time data from machinery to predict potential failures, allowing for proactive maintenance and significantly reducing downtime, which is a critical concern for high-volume fabrication operations. This predictive capability translates directly into improved equipment utilization and reduced operational costs.

Furthermore, AI plays a pivotal role in enhancing quality control and design optimization. AI-powered vision systems can detect minute defects in fabricated parts with higher accuracy and speed than human inspectors, ensuring consistent product quality across large batches. In the design phase, generative AI tools can explore vast solution spaces, suggesting optimal designs for specific functional requirements, material properties, and manufacturing constraints, thereby accelerating the product development cycle and improving material efficiency. This capability is particularly valuable for complex geometries and performance-critical components.

The influence of AI also extends to supply chain management and process automation. AI-driven analytics can optimize material procurement, inventory management, and logistics, ensuring timely delivery of raw materials and finished products while minimizing holding costs. Integrating AI with robotic systems enables more sophisticated automation of tasks such as cutting, bending, and welding, with robots adapting to variations in material and design. This synergy between AI and automation addresses the challenges of labor shortages and the need for scalable production capabilities, fostering a more agile and responsive fabrication environment that can adapt to fluctuating market demands.

- Predictive maintenance for fabrication machinery, reducing downtime.

- Enhanced quality control through AI-powered vision systems for defect detection.

- Generative design and optimization of sheet metal components.

- AI-driven process optimization for cutting, bending, and welding.

- Intelligent automation of material handling and robotic assembly.

- Improved supply chain planning and inventory management.

- Real-time data analytics for process monitoring and performance improvement.

Key Takeaways Sheet Metal Fabrication Service Market Size & Forecast

The sheet metal fabrication service market is projected for substantial growth, indicating a robust future driven by ongoing industrial expansion and technological integration. A primary takeaway is the consistent demand stemming from diverse end-use industries such as automotive, aerospace, construction, and electronics, which are continually seeking high-precision metal components. This broad application base ensures sustained market momentum, making it an attractive sector for investment and strategic development. The forecast highlights that despite potential economic fluctuations, the fundamental need for fabricated metal parts will continue to fuel market expansion.

Another crucial insight is the increasing emphasis on advanced manufacturing techniques and smart factory initiatives. Companies are investing heavily in automation, robotics, and digital technologies to enhance efficiency, reduce production costs, and meet stringent quality standards. This shift is not merely about adopting new tools but about fundamentally transforming operational paradigms to achieve greater agility and responsiveness to market changes. The ability to integrate Industry 4.0 principles, such as IoT and real-time data analytics, will be a significant differentiator for market participants looking to capitalize on future growth opportunities.

Finally, the market is characterized by a strong push towards sustainability and custom solutions. Demand for eco-friendly manufacturing processes and materials is gaining traction, influencing procurement decisions and production strategies. Concurrently, the proliferation of bespoke product requirements across various sectors necessitates flexible fabrication services capable of rapid prototyping and personalized mass production. These trends underscore a market that is not only growing in size but also evolving in complexity, requiring players to be adaptable, innovative, and environmentally conscious to secure long-term success and capitalize on the projected market expansion.

- Market demonstrates robust growth potential, driven by diverse industrial demand.

- Significant investment in automation and advanced manufacturing technologies is observed.

- Increasing importance of customization and on-demand production capabilities.

- Sustainability and material efficiency are critical drivers for future development.

- Technological integration (Industry 4.0, AI) is key to competitive advantage.

- Emerging economies present substantial growth opportunities.

- Resilience in supply chains is becoming a strategic imperative for market players.

Sheet Metal Fabrication Service Market Drivers Analysis

The sheet metal fabrication service market is propelled by a confluence of powerful drivers that are fostering its expansion and evolution. Industrialization and urbanization across developing economies significantly fuel demand for fabricated metal components in construction, infrastructure development, and manufacturing sectors. As cities expand and industrial bases grow, the need for structural elements, machinery parts, and consumer goods made from sheet metal increases exponentially. This demographic and economic shift creates a steady and substantial order pipeline for fabrication service providers globally.

Technological advancements, particularly in automation, robotics, and precision manufacturing, serve as another critical driver. The integration of advanced CNC machines, laser cutting, and robotic welding systems enhances production efficiency, accuracy, and reduces turnaround times, making fabrication services more attractive and cost-effective for a wider range of applications. These innovations enable the production of complex geometries with tighter tolerances, meeting the increasingly sophisticated requirements of modern industries like aerospace and medical devices. Furthermore, the push towards Industry 4.0 principles, including IoT and AI, further optimizes manufacturing processes, driving down operational costs and improving overall output quality.

Moreover, the continuous demand from key end-use industries like automotive, aerospace & defense, and electronics acts as a foundational market driver. The automotive sector, for instance, relies heavily on sheet metal for vehicle bodies, chassis, and various internal components, driven by ongoing innovation in vehicle design and electric vehicle manufacturing. Similarly, the aerospace industry requires lightweight, high-strength metal components for aircraft, while the electronics sector utilizes precision-fabricated enclosures and components. These industries’ consistent need for high-quality, durable, and precisely engineered metal parts ensures a perpetual demand for specialized fabrication services.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Industrialization & Urbanization | +2.1% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

| Technological Advancements in Automation & Robotics | +1.8% | North America, Europe, Asia Pacific | Medium to Long-term (2025-2033) |

| Growing Demand from Automotive & Aerospace Sectors | +1.5% | Global | Long-term (2025-2033) |

| Expansion of Construction and Infrastructure Projects | +1.4% | Asia Pacific, North America, Europe | Medium to Long-term (2025-2033) |

Sheet Metal Fabrication Service Market Restraints Analysis

Despite its robust growth trajectory, the sheet metal fabrication service market faces several significant restraints that could impede its full potential. One major challenge is the volatility of raw material prices, particularly for steel, aluminum, and copper. Fluctuations in global commodity markets, often influenced by geopolitical events, supply chain disruptions, or trade policies, directly impact the cost of production for fabricators. This unpredictability makes it difficult for companies to provide stable pricing to clients, manage profit margins, and undertake long-term planning, potentially leading to project delays or cancellations when material costs surge unexpectedly.

Another critical restraint is the persistent shortage of skilled labor. Modern sheet metal fabrication requires highly trained professionals capable of operating advanced CNC machines, robotic welding systems, and sophisticated design software. The aging workforce, coupled with a lack of new entrants into vocational trades, creates a widening skills gap that affects production capacity and quality. This scarcity can lead to increased labor costs, slower adoption of new technologies, and a general bottleneck in meeting growing market demand, particularly in regions with strong manufacturing bases but insufficient training pipelines.

Furthermore, the high initial capital investment required for advanced fabrication equipment and technology can act as a barrier to entry for new players and a restraint for smaller or medium-sized enterprises seeking to upgrade their capabilities. State-of-the-art laser cutters, press brakes, and robotic cells are expensive, and their implementation often involves additional costs for training, software integration, and facility modifications. This significant financial outlay can limit competitive agility and innovation, especially for companies that may not have immediate access to substantial capital, thus concentrating market power among larger, more established firms.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material Prices | -1.3% | Global | Short to Medium-term (2025-2028) |

| Shortage of Skilled Labor | -1.1% | North America, Europe, parts of Asia Pacific | Long-term (2025-2033) |

| High Capital Investment for Advanced Machinery | -0.9% | Global | Medium to Long-term (2025-2033) |

| Intensifying Global Competition | -0.7% | Global | Long-term (2025-2033) |

Sheet Metal Fabrication Service Market Opportunities Analysis

The sheet metal fabrication service market is replete with significant opportunities for growth and innovation, driven by evolving industrial demands and technological advancements. One prominent opportunity lies in the increasing adoption of additive manufacturing and hybrid manufacturing processes. While traditional sheet metal fabrication remains essential, the integration of technologies like 3D printing for specialized components or tooling can complement conventional methods, offering new avenues for complex geometries, rapid prototyping, and customized parts. This hybrid approach enables fabricators to offer more comprehensive and versatile solutions, attracting a broader client base seeking cutting-edge manufacturing capabilities.

Another substantial opportunity is the expanding demand for bespoke and on-demand fabrication services across various industries. As product lifecycles shorten and consumer preferences become more diversified, manufacturers require flexible fabrication partners capable of producing low-volume, highly customized components quickly and cost-effectively. This trend is particularly evident in sectors like medical devices, consumer electronics, and specialized industrial machinery. Fabricators who can leverage digital design tools, automated processes, and agile production methodologies to meet these tailored requirements will secure a competitive edge and tap into a growing niche market.

Furthermore, the push towards sustainable and green manufacturing practices presents a lucrative opportunity for innovation and market differentiation. Companies are increasingly seeking fabrication partners who can demonstrate a commitment to environmental responsibility through optimized material usage, reduced waste generation, and energy-efficient processes. Investing in technologies that minimize scrap, recycle materials, and utilize renewable energy sources not only aligns with corporate sustainability goals but also enhances brand reputation and can lead to cost savings in the long run. Offering eco-friendly fabrication solutions allows companies to cater to environmentally conscious clients and secure contracts with organizations prioritizing sustainable supply chains.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of Additive & Hybrid Manufacturing | +1.6% | North America, Europe, Asia Pacific | Medium to Long-term (2026-2033) |

| Expanding Demand for Custom & On-demand Fabrication | +1.9% | Global | Long-term (2025-2033) |

| Adoption of Green Manufacturing Practices | +1.2% | Europe, North America, Japan | Long-term (2025-2033) |

| Expansion into Emerging Market Geographies | +1.5% | Asia Pacific, Latin America, MEA | Long-term (2025-2033) |

Sheet Metal Fabrication Service Market Challenges Impact Analysis

The sheet metal fabrication service market faces several distinct challenges that can impact its growth trajectory and operational efficiency. One significant challenge is the intense competition within the industry, driven by the presence of numerous small, medium, and large-scale fabricators. This crowded landscape often leads to price wars, reduced profit margins, and the constant pressure to differentiate services. Companies must continuously invest in new technologies, improve operational efficiencies, and offer specialized services to maintain their competitive edge, which can be particularly burdensome for smaller players.

Another considerable challenge is the susceptibility to supply chain disruptions. The fabrication process relies heavily on a steady and predictable supply of raw materials, components, and energy. Global events such as geopolitical conflicts, natural disasters, pandemics, or trade restrictions can severely disrupt these supply chains, leading to material shortages, increased lead times, and escalated costs. Such disruptions not only affect production schedules and delivery commitments but also undermine customer trust and can force companies to seek more expensive, less efficient alternative sourcing options.

Moreover, the complexity of integrating new technologies, particularly those associated with Industry 4.0 and AI, poses a significant challenge. While these technologies offer immense potential for efficiency and innovation, their successful implementation requires substantial upfront investment, specialized technical expertise, and a robust digital infrastructure. Fabricators often struggle with the compatibility of legacy systems with new digital solutions, the cybersecurity risks associated with connected factories, and the need to retrain or hire personnel with advanced IT and data analytics skills. Overcoming these integration hurdles is critical for capitalizing on technological advancements but demands considerable strategic planning and resource allocation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition & Price Pressure | -1.2% | Global | Long-term (2025-2033) |

| Supply Chain Vulnerabilities & Disruptions | -1.0% | Global | Short to Medium-term (2025-2028) |

| Complexity of New Technology Integration | -0.8% | Global | Medium to Long-term (2025-2033) |

| Adherence to Evolving Regulatory Standards | -0.6% | Europe, North America | Long-term (2025-2033) |

Sheet Metal Fabrication Service Market - Updated Report Scope

This updated report provides a comprehensive analysis of the Sheet Metal Fabrication Service Market, offering detailed insights into its current state, historical performance, and future growth projections. It covers an extensive range of market attributes, including size, growth rate, key trends, and a thorough segmentation across various processes, materials, end-use industries, and types. The report aims to equip stakeholders with critical data for strategic decision-making, highlighting opportunities, challenges, drivers, and restraints influencing market dynamics globally and regionally. It also profiles leading companies and addresses frequently asked questions to provide a holistic market view.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 185.0 Billion |

| Market Forecast in 2033 | USD 315.6 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Precision Metalworks, Global Fabrication Solutions, Advanced Sheet Metal, Integrated Manufacturing Group, Zenith Precision Engineering, Apex Metal Fabrication, Stellar Industrial Services, Elite Metalcraft, Dynamic Fabricators, Unified Metal Solutions, Core Fabrication Services, OptiForm Manufacturing, Summit Sheet Metal, Genesis Industrial Fabrications, Prime Metals Inc., NexGen Fabrication, Delta Metal Forming, Quantum Fabricators, Orion Engineering Solutions, Keystone Fabrication |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The sheet metal fabrication service market is broadly segmented to provide a granular understanding of its diverse landscape and cater to various industrial requirements. These segmentations are critical for analyzing market dynamics, identifying niche opportunities, and tailoring strategies to specific client needs. The market is primarily categorized by the fabrication process employed, the type of material utilized, the end-use industry served, and the nature of the fabrication service provided, each representing distinct operational characteristics and demand drivers.

By dissecting the market along these dimensions, it becomes possible to observe how different technological advancements or material innovations impact specific sub-segments. For instance, the demand for laser cutting services might surge in the electronics industry due to its precision, while heavy structural steel fabrication could see robust growth in the construction sector. Understanding these interdependencies and specific segment growth patterns is essential for market participants to allocate resources effectively and develop targeted offerings that resonate with their client base, ensuring sustained market relevance and profitability.

- By Process:

- Cutting (Laser Cutting, Plasma Cutting, Waterjet Cutting, Shearing)

- Bending (Press Brake Bending, Roll Forming)

- Punching

- Stamping

- Welding (MIG Welding, TIG Welding, Spot Welding, Resistance Welding)

- Finishing (Grinding, Polishing, Deburring, Coating)

- By Material:

- Steel (Carbon Steel, Stainless Steel, Galvanized Steel)

- Aluminum

- Copper

- Brass

- Others (Titanium, Nickel Alloys)

- By End-Use Industry:

- Automotive

- Aerospace & Defense

- Construction

- Electronics

- Industrial Machinery

- HVAC (Heating, Ventilation, and Air Conditioning)

- Medical Devices

- Telecommunications

- Energy (Renewable Energy, Oil & Gas)

- Others (Consumer Goods, Agriculture)

- By Type:

- Custom Fabrication

- Standard Fabrication

Regional Highlights

- North America: A mature market characterized by high adoption of advanced automation technologies and strong demand from the automotive, aerospace, and industrial machinery sectors. The region benefits from significant R&D investments and a focus on high-precision, low-volume production.

- Europe: Driven by stringent quality standards, emphasis on sustainability, and robust automotive and industrial sectors, particularly in Germany and Italy. There is a growing trend towards smart manufacturing and customized solutions.

- Asia Pacific (APAC): The largest and fastest-growing market due to rapid industrialization, urbanization, and significant manufacturing activities in China, India, Japan, and South Korea. Increased infrastructure development and electronics production fuel demand, alongside growing adoption of automation.

- Latin America: An emerging market experiencing steady growth, propelled by expanding automotive and construction industries, especially in Brazil and Mexico. Foreign investments and regional trade agreements contribute to market development.

- Middle East & Africa (MEA): Shows promising growth fueled by investments in infrastructure, energy projects (including renewables), and defense. Diversification efforts away from oil economies are driving manufacturing expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Sheet Metal Fabrication Service Market.- Precision Metalworks

- Global Fabrication Solutions

- Advanced Sheet Metal

- Integrated Manufacturing Group

- Zenith Precision Engineering

- Apex Metal Fabrication

- Stellar Industrial Services

- Elite Metalcraft

- Dynamic Fabricators

- Unified Metal Solutions

- Core Fabrication Services

- OptiForm Manufacturing

- Summit Sheet Metal

- Genesis Industrial Fabrications

- Prime Metals Inc.

- NexGen Fabrication

- Delta Metal Forming

- Quantum Fabricators

- Orion Engineering Solutions

- Keystone Fabrication

Frequently Asked Questions

What is sheet metal fabrication?

Sheet metal fabrication is the process of forming thin, flat metal sheets into desired shapes and components. It involves various techniques such as cutting, bending, punching, welding, and assembling to produce a wide range of products for diverse industries.

Which industries primarily utilize sheet metal fabrication services?

Sheet metal fabrication services are crucial for industries including automotive, aerospace & defense, construction, electronics, industrial machinery, HVAC, and medical devices. These sectors rely on precisely formed metal components for their products and infrastructure.

What are the key technologies driving innovation in sheet metal fabrication?

Key technologies include advanced CNC (Computer Numerical Control) machines, laser cutting, robotic welding, automated bending systems, and integrated CAD/CAM software. The adoption of Industry 4.0 principles, AI, and IoT further enhances efficiency and precision.

How is the Sheet Metal Fabrication Service Market expected to grow?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing industrialization, technological advancements, and rising demand from various end-use sectors globally.

What are the main challenges faced by sheet metal fabricators?

Major challenges include the volatility of raw material prices, a persistent shortage of skilled labor, intense market competition, high initial capital investment for advanced machinery, and the complexity of integrating new digital technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted