Shared Mobility Market

Shared Mobility Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709410 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Shared Mobility Market Size

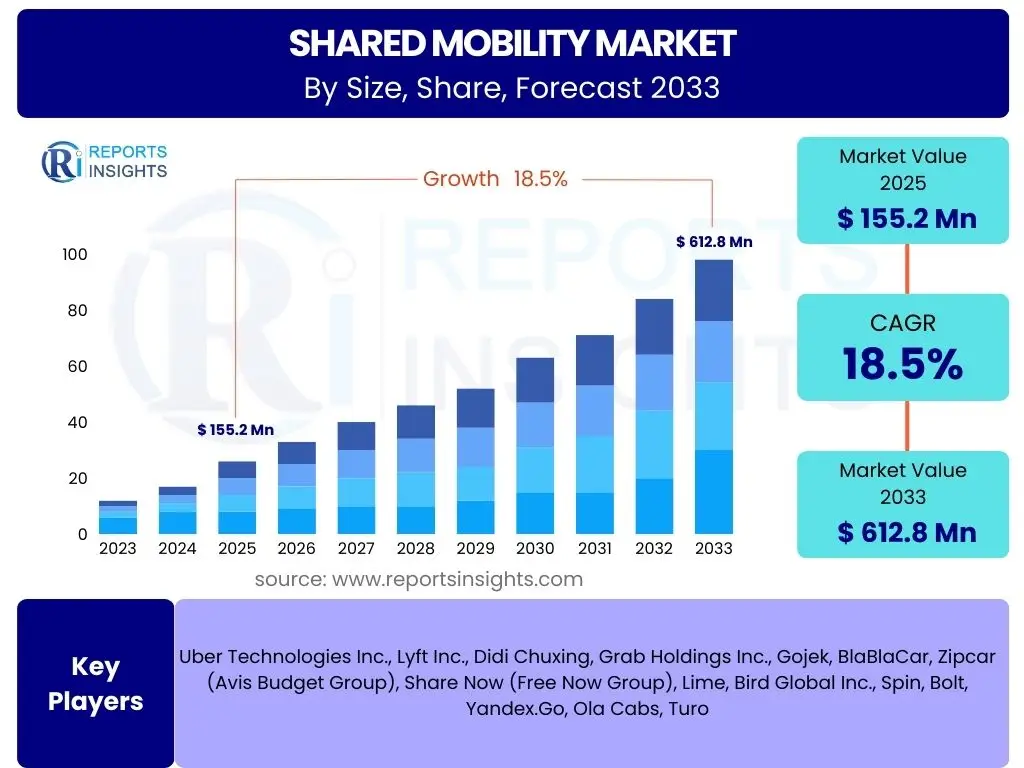

According to Reports Insights Consulting Pvt Ltd, The Shared Mobility Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 155.2 billion in 2025 and is projected to reach USD 612.8 billion by the end of the forecast period in 2033.

Key Shared Mobility Market Trends & Insights

The shared mobility landscape is undergoing rapid evolution, driven by shifting consumer preferences towards sustainable and cost-effective transportation options. A primary trend involves the diversification of service offerings, moving beyond traditional ride-hailing to include micro-mobility solutions like electric scooters and bikes, as well as peer-to-peer car sharing and on-demand transit. This expansion caters to a wider array of travel needs and distances, particularly in urban environments where traffic congestion and parking challenges are prevalent. Moreover, there is a strong inclination towards integrated multi-modal platforms that allow users to plan, book, and pay for various shared transportation services through a single application, enhancing convenience and efficiency.

Another significant insight points to the increasing collaboration between shared mobility providers, public transport authorities, and city governments. These partnerships are crucial for developing comprehensive urban mobility ecosystems that reduce private car dependency and support smart city initiatives. Data-driven insights from shared mobility platforms are being leveraged to optimize traffic flow, identify mobility gaps, and inform urban planning decisions. Furthermore, the industry is witnessing a surge in subscription-based models and flexible ownership options, reflecting a broader consumer shift from asset ownership to access-based services, particularly among younger demographics and in densely populated areas where vehicle ownership costs are prohibitive.

- Shift towards multi-modal integration platforms for seamless travel.

- Rapid expansion of micro-mobility options, including electric bikes and scooters.

- Increasing partnerships between private operators and public transport agencies.

- Growing adoption of subscription and flexible access models over vehicle ownership.

- Leveraging data analytics for urban planning and traffic optimization.

- Emphasis on sustainable and electric vehicle fleets within shared services.

- Development of autonomous vehicle integration pilot programs.

AI Impact Analysis on Shared Mobility

Artificial intelligence is fundamentally reshaping the shared mobility sector by enhancing operational efficiency, optimizing user experience, and enabling predictive capabilities. AI algorithms are crucial for dynamic pricing, real-time demand forecasting, and intelligent vehicle dispatch systems, allowing providers to match supply with demand more effectively and reduce idle times. This leads to improved resource utilization and increased profitability. Furthermore, AI-powered predictive maintenance helps in identifying potential issues with vehicles before they become critical, ensuring fleet reliability and safety, which is paramount for consumer trust and operational continuity in a high-utilization environment.

The application of AI extends to personalized user experiences, where algorithms analyze individual travel patterns and preferences to offer tailored recommendations for routes, vehicle types, and even multi-modal combinations. This personalization significantly boosts user satisfaction and encourages repeat usage. In the context of autonomous vehicles, AI is the backbone, enabling self-driving capabilities, navigation, and obstacle detection, paving the way for fully autonomous shared fleets that promise lower operational costs and enhanced safety. However, the integration of AI also raises concerns regarding data privacy, algorithmic bias in pricing or dispatching, and the potential displacement of human drivers, requiring careful ethical considerations and regulatory frameworks.

- Optimized vehicle routing and dispatching through AI algorithms.

- Dynamic pricing models based on real-time demand and supply.

- Enhanced predictive maintenance for fleet reliability and longevity.

- Personalized user experiences and travel recommendations.

- Foundation for autonomous shared vehicle operations, improving safety and efficiency.

- Advanced fraud detection and security measures.

- Improved customer service through AI-powered chatbots and virtual assistants.

Key Takeaways Shared Mobility Market Size & Forecast

The Shared Mobility market is poised for substantial growth over the next decade, with projections indicating a robust Compound Annual Growth Rate (CAGR) and a significant increase in market valuation. This expansion is largely attributed to the increasing global urbanization, rising environmental consciousness, and the digital transformation enabling sophisticated service delivery. Consumers are increasingly valuing convenience, cost-effectiveness, and sustainability, driving the adoption of shared transportation models as viable alternatives to private vehicle ownership. The forecast highlights a strong market trajectory, suggesting sustained investment and innovation in the sector to meet evolving urban mobility needs.

A crucial takeaway is the anticipated shift in mobility paradigms, moving from a vehicle-centric approach to a user-centric, service-oriented model. The market's growth will be fueled by technological advancements, including AI integration for operational efficiencies and improved user experiences, alongside policy support from governments promoting sustainable urban development. This indicates that successful market players will be those that can adapt to diverse regional needs, integrate with existing public transport infrastructure, and continuously innovate their service offerings to remain competitive and relevant in a dynamic urban landscape. The significant forecast figures underscore shared mobility's role as a cornerstone of future smart cities and sustainable transportation systems.

- Market projected for significant expansion with an 18.5% CAGR to 2033.

- Estimated market value to exceed USD 600 billion by 2033.

- Growth driven by urbanization, sustainability goals, and digital adoption.

- Emphasis on diverse service offerings and multi-modal integration for user convenience.

- Technological innovation, particularly AI, is critical for operational efficiency and user experience.

- Strong potential for integration with smart city initiatives and public transport networks.

- Shift from vehicle ownership to access-based mobility services.

Shared Mobility Market Drivers Analysis

Several pivotal factors are propelling the growth of the shared mobility market globally. Foremost among these is the escalating rate of urbanization, particularly in emerging economies, which exacerbates traffic congestion, parking scarcity, and air pollution, making private vehicle ownership less practical and more expensive. Shared mobility services offer a compelling solution to these urban challenges by optimizing vehicle utilization and reducing the total number of vehicles on the road. The increasing preference for cost-effective transportation alternatives also plays a significant role, as shared services often eliminate the financial burden of vehicle purchase, maintenance, insurance, and fuel, appealing to budget-conscious consumers.

Furthermore, heightened environmental awareness and the global push towards sustainable development goals are fueling demand for shared electric and low-emission vehicles. Governments and regulatory bodies are actively promoting shared mobility through favorable policies, incentives, and investment in infrastructure, recognizing its potential to reduce carbon footprints and improve urban air quality. The widespread adoption of smartphones and advancements in mobile application technology have also significantly lowered barriers to entry for users, making booking and managing shared rides or vehicles incredibly convenient and accessible, thereby broadening the market's reach and accelerating its expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization & Congestion | +4.8% | Global (Asia Pacific, Africa, Latin America particularly) | Long-term (2025-2033) |

| Growing Environmental Concerns & Sustainability Initiatives | +3.5% | Europe, North America, Select APAC Countries | Mid-to-Long-term (2026-2033) |

| Rising Cost of Vehicle Ownership | +4.2% | Global (Developed Economies & Major Cities) | Short-to-Mid-term (2025-2029) |

| Technological Advancements (e.g., AI, IoT, Mobile Apps) | +3.9% | Global | Ongoing (2025-2033) |

| Favorable Government Policies & Regulations | +2.1% | Europe, North America, China, India | Mid-term (2027-2031) |

| Changing Consumer Preferences (Access over Ownership) | +3.0% | Global (Youth Demographics) | Long-term (2025-2033) |

| Expansion of Electric Vehicle (EV) Fleets | +2.5% | Europe, China, North America | Mid-to-Long-term (2026-2033) |

Shared Mobility Market Restraints Analysis

Despite the optimistic growth trajectory, the shared mobility market faces several significant restraints that could impede its full potential. A primary concern is the varying and often inconsistent regulatory landscape across different cities and countries. Local governments may impose strict licensing requirements, operational restrictions, or caps on vehicle numbers, which can create significant barriers to entry and expansion for shared mobility providers. This fragmented regulatory environment necessitates continuous adaptation and negotiation, adding complexity and cost to operations. Furthermore, issues related to public safety and security, particularly concerning driver background checks, vehicle maintenance standards, and user privacy, can deter potential users and lead to increased regulatory scrutiny.

Another major restraint is the intense competition within the market, not only among shared mobility providers themselves but also from traditional public transport and private vehicle ownership. This competitive pressure often leads to price wars, eroding profit margins for operators. Additionally, infrastructure limitations, such as a lack of dedicated lanes for micro-mobility, insufficient charging stations for electric fleets, and inadequate parking solutions, can hinder the seamless integration and widespread adoption of shared services. User adoption rates can also be impacted by concerns regarding vehicle cleanliness, availability during peak hours, and reliability, particularly in regions with less mature shared mobility ecosystems or where public trust in such services is still developing.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inconsistent & Evolving Regulatory Frameworks | -3.7% | Global (Highly Fragmented) | Ongoing (2025-2033) |

| Public Safety & Security Concerns | -2.8% | Global | Long-term (2025-2033) |

| Intense Competition & Price Wars | -2.1% | Global (Highly Saturated Markets) | Short-to-Mid-term (2025-2029) |

| Infrastructure Limitations (e.g., Charging, Parking) | -3.2% | Emerging Markets, Densely Populated Cities | Mid-to-Long-term (2026-2033) |

| User Adoption Barriers (e.g., Trust, Habits) | -1.9% | Rural Areas, Less Digitally Literate Populations | Long-term (2025-2033) |

| Data Privacy & Cybersecurity Risks | -2.4% | Global | Ongoing (2025-2033) |

| High Operational Costs & Maintenance of Fleets | -1.5% | Global | Short-to-Mid-term (2025-2030) |

Shared Mobility Market Opportunities Analysis

The shared mobility market is replete with significant opportunities for innovation and expansion. A key area for growth lies in the further integration of shared services with existing public transportation networks. Developing seamless multi-modal platforms that allow users to combine public transit with first-mile/last-mile shared mobility options can enhance convenience, reduce reliance on private cars, and provide holistic urban travel solutions. There is also substantial untapped potential in underserved rural and suburban areas, where traditional public transport may be limited, and the cost of private vehicle ownership remains high. Tailoring shared mobility solutions to these specific demographic and geographic needs represents a considerable market opening.

The transition to electric vehicles (EVs) and autonomous vehicles (AVs) presents another immense opportunity. Shared EV fleets can significantly reduce operating costs due to lower fuel and maintenance expenses, while also aligning with sustainability objectives. As AV technology matures, fully autonomous shared fleets could revolutionize the industry by eliminating driver labor costs, enhancing safety, and providing highly efficient, on-demand services round the clock. Furthermore, strategic partnerships with corporations, universities, and tourism sectors to provide tailored shared mobility solutions, such as employee commuting programs or tourist transit packages, can unlock new revenue streams and expand market penetration. Developing advanced data analytics and predictive modeling capabilities can also create opportunities for optimized service delivery and personalized user experiences.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Public Transit & Multi-modal Platforms | +4.1% | Global (Major Cities) | Long-term (2026-2033) |

| Expansion into Underserved Rural & Suburban Areas | +3.6% | North America, Europe, Select APAC Regions | Mid-to-Long-term (2027-2033) |

| Adoption of Electric & Autonomous Vehicles in Fleets | +5.5% | Global (Technologically Advanced Regions) | Long-term (2028-2033) |

| Strategic Partnerships (Corporate, Tourism, Universities) | +3.0% | Global | Mid-term (2025-2030) |

| Data-driven Optimization & Personalized Services | +2.8% | Global | Ongoing (2025-2033) |

| Development of Micro-mobility as a Standalone Solution | +2.0% | Dense Urban Centers | Short-to-Mid-term (2025-2028) |

| Implementation of Mobility-as-a-Service (MaaS) Ecosystems | +3.3% | Europe, North America, Advanced APAC Cities | Long-term (2027-2033) |

Shared Mobility Market Challenges Impact Analysis

The shared mobility market faces several critical challenges that demand strategic responses from industry players and policymakers. One significant hurdle is establishing a sustainable and profitable business model amidst intense competition and high operational costs. The need for constant fleet maintenance, technological upgrades, and robust customer support, coupled with dynamic pricing pressures, often impacts profitability. Furthermore, managing the public perception and ensuring user trust is an ongoing challenge, particularly concerning safety incidents, data privacy breaches, or issues related to vehicle availability and cleanliness, which can quickly erode consumer confidence and hinder adoption.

Another substantial challenge involves navigating the complex and often conflicting interests of various stakeholders, including local governments, public transit operators, taxi associations, and the general public. Striking a balance between innovation, regulation, and public welfare requires continuous dialogue and adaptive policy-making. Moreover, addressing infrastructure gaps, such as the lack of dedicated parking for shared vehicles or sufficient charging infrastructure for electric fleets, poses a significant logistical and financial challenge, particularly in rapidly urbanizing areas. The rapid technological shifts, including the advent of autonomous vehicles, also present a challenge in terms of integration, public acceptance, and the need for new regulatory frameworks to ensure safe and ethical deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Sustainable Profitability & Business Models | -3.9% | Global | Ongoing (2025-2033) |

| Ensuring Public Trust, Safety & Security | -3.0% | Global | Long-term (2025-2033) |

| Regulatory Ambiguity & Stakeholder Conflicts | -3.5% | Global (Particularly in New Markets) | Mid-term (2025-2030) |

| Infrastructure Deficiencies (Charging, Parking, Lanes) | -2.7% | Emerging Markets, Densely Populated Cities | Mid-to-Long-term (2026-2033) |

| Adapting to Rapid Technological Evolution (e.g., AVs) | -2.0% | Global (Technologically Advanced Regions) | Long-term (2028-2033) |

| Managing Peak Demand & Vehicle Redistribution | -1.8% | Dense Urban Centers | Short-to-Mid-term (2025-2029) |

| High Initial Capital Expenditure for Fleet Expansion | -2.2% | Global (New Entrants) | Short-term (2025-2027) |

Shared Mobility Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Shared Mobility Market, offering a detailed analysis of its current size, historical trends, and future growth projections from 2025 to 2033. It examines the market through various lenses, including service types, vehicle categories, business models, and regional landscapes, to provide a holistic view of the industry. The report highlights key growth drivers, significant restraints, emerging opportunities, and critical challenges that are shaping the market, alongside the profound impact of artificial intelligence and sustainable practices on its evolution. Designed for stakeholders seeking strategic insights, it encapsulates market segmentation, competitive intelligence, and regional analyses to inform decision-making in a rapidly transforming mobility sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 155.2 Billion |

| Market Forecast in 2033 | USD 612.8 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Uber Technologies Inc., Lyft Inc., Didi Chuxing, Grab Holdings Inc., Gojek, BlaBlaCar, Zipcar (Avis Budget Group), Share Now (Free Now Group), Lime, Bird Global Inc., Spin, Bolt, Yandex.Go, Ola Cabs, Turo |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The shared mobility market is broadly segmented to capture the diverse nature of services and operational models, providing a granular view of its various components and growth areas. This segmentation helps in understanding specific market dynamics, consumer preferences, and technological adoption patterns across different verticals. It allows for a detailed analysis of which segments are driving growth, identifying niche opportunities, and pinpointing areas requiring further innovation or regulatory attention. Each segment reflects unique operational challenges and market potential, contributing to the overall complexity and dynamism of the shared mobility ecosystem.

- By Service Type: This segment includes a wide range of offerings such as car sharing (round-trip, one-way, free-floating), ride hailing (on-demand car services), bike sharing (docked, dockless, electric), scooter sharing (electric, traditional), peer-to-peer (P2P) ride sharing, and shuttle services, along with public transit integration. Each service type caters to different urban travel needs and distances.

- By Vehicle Type: Categorization by vehicle type encompasses passenger cars (including electric, hybrid, and internal combustion engine models), various types of bicycles (electric and non-electric), scooters (electric and non-electric), mopeds, and larger vehicles like buses and vans used for shared transport solutions. The rise of micro-mobility has significantly diversified this segment.

- By Business Model: The market is primarily divided into Peer-to-Peer (P2P) models, where individuals share their private vehicles or assets, and Business-to-Consumer (B2C) models, where companies own and operate the shared fleet. Each model presents distinct operational challenges, scalability, and market penetration strategies.

- By End User: Segmentation by end user typically distinguishes between Business and Consumer applications. Business users include corporate fleets, logistics companies utilizing shared delivery services, and employee commuting programs. Consumer users represent the general public utilizing shared mobility for commuting, leisure, tourism, and other personal travel needs.

Regional Highlights

- North America: This region is characterized by a mature shared mobility market, especially in ride-hailing and car-sharing segments, driven by early adoption of technology, significant venture capital investment, and a culture of convenience. Major cities have robust shared mobility infrastructure, and there's a growing emphasis on electric and autonomous shared vehicle deployment. Regulatory frameworks are evolving, with cities exploring ways to integrate shared mobility into broader urban planning.

- Europe: Europe is a leader in sustainable shared mobility, with strong government support for electric vehicles, cycling infrastructure, and integrated multi-modal transport solutions. Car-sharing and bike-sharing are well-established, with a rising trend in micro-mobility. Strict environmental regulations and a focus on reducing urban emissions are key drivers. The region is actively developing Mobility-as-a-Service (MaaS) platforms that combine various transport options seamlessly.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid urbanization, a large and digitally-savvy population, and increasing disposable incomes. Countries like China and India are experiencing explosive growth in ride-hailing and micro-mobility due to dense populations and persistent traffic congestion. Government initiatives promoting smart cities and sustainable transport are also contributing to market expansion.

- Latin America: This region presents significant potential due to high urbanization rates, infrastructure challenges, and a growing middle class seeking affordable and convenient transportation. Ride-hailing is particularly dominant, addressing gaps in public transport. Challenges include regulatory inconsistencies and varying levels of digital infrastructure, but robust demand continues to attract investment.

- Middle East and Africa (MEA): The MEA region is an emerging market for shared mobility, with growth concentrated in major urban centers. Economic diversification efforts, increasing tourism, and smart city initiatives are driving the adoption of ride-hailing and car-sharing services. However, market penetration varies widely, and infrastructure development, alongside evolving regulatory landscapes, remains key to unlocking the region's full potential.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Shared Mobility Market.- Uber Technologies Inc.

- Lyft Inc.

- Didi Chuxing

- Grab Holdings Inc.

- Gojek

- BlaBlaCar

- Zipcar (Avis Budget Group)

- Share Now (Free Now Group)

- Lime

- Bird Global Inc.

- Spin

- Bolt

- Yandex.Go

- Ola Cabs

- Turo

- Moovit (Intel Corporation)

- Via Transportation Inc.

- Getaround Inc.

- Motional Inc. (Hyundai-Aptiv JV)

- Argo AI (Ford-VW JV)

Frequently Asked Questions

What is shared mobility?

Shared mobility refers to transportation services where users have temporary access to a vehicle or means of transport, such as cars, bikes, or scooters, on an as-needed basis. It includes various models like ride-hailing, car-sharing, bike-sharing, and scooter-sharing, offering alternatives to private vehicle ownership.

What factors are driving the growth of the shared mobility market?

The market's growth is primarily driven by rapid urbanization, increasing traffic congestion and parking issues, rising costs of vehicle ownership, growing environmental consciousness, and advancements in digital technology (e.g., mobile apps, AI) that enhance convenience and efficiency for users.

How does AI impact shared mobility services?

AI significantly impacts shared mobility by enabling dynamic pricing, optimizing vehicle routing and dispatching, predicting demand, enhancing fleet maintenance, and personalizing user experiences. AI is also foundational for the development and deployment of autonomous shared vehicles.

What are the main challenges facing the shared mobility industry?

Key challenges include navigating inconsistent regulatory environments, ensuring public safety and trust, managing intense competition, addressing infrastructure limitations (like charging and parking), and achieving sustainable profitability in a dynamic market.

What are the future opportunities in the shared mobility market?

Future opportunities lie in greater integration with public transit to create multi-modal solutions, expansion into underserved rural and suburban areas, widespread adoption of electric and autonomous vehicle fleets, and leveraging data analytics for highly personalized and efficient services.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted