Service Provider Router Market

Service Provider Router Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708534 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Service Provider Router Market Size

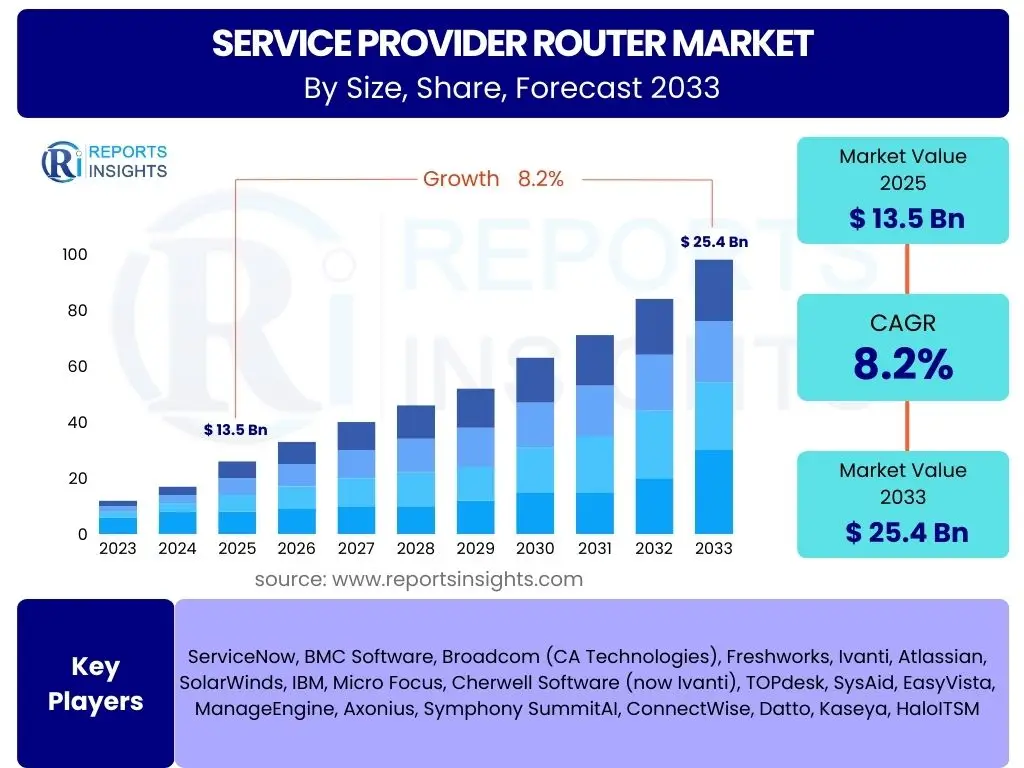

According to Reports Insights Consulting Pvt Ltd, The Service Provider Router Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 13.5 Billion in 2025 and is projected to reach USD 25.4 Billion by the end of the forecast period in 2033.

Key Service Provider Router Market Trends & Insights

The Service Provider Router market is currently undergoing a significant transformation driven by the escalating demand for high-bandwidth connectivity and advanced network services. Key trends include the widespread adoption of 5G technology, which necessitates robust and high-capacity routing infrastructure to support increased data traffic, lower latency, and massive device connectivity. Furthermore, the push towards network virtualization through Software-Defined Networking (SDN) and Network Function Virtualization (NFV) is reshaping router architectures, enabling greater agility, scalability, and cost efficiency for service providers. These trends collectively underscore a shift towards more intelligent, flexible, and resilient network core and edge solutions.

Another prominent insight is the growing emphasis on edge computing, which requires distributed routing capabilities closer to data sources to minimize latency and optimize performance for emerging applications like IoT and augmented reality. The integration of advanced security features directly into router hardware and software is also becoming critical, as cyber threats grow in sophistication and frequency. Service providers are increasingly seeking routers that can support comprehensive security protocols, deep packet inspection, and threat intelligence to protect their vast network infrastructures and customer data. These developments reflect a dynamic market focused on meeting future connectivity demands with innovative and secure routing solutions.

- Rapid deployment of 5G networks globally.

- Increased adoption of Software-Defined Networking (SDN) and Network Function Virtualization (NFV).

- Growing demand for higher bandwidth and lower latency.

- Proliferation of edge computing architectures.

- Integration of advanced cybersecurity features into router platforms.

- Focus on energy-efficient and sustainable routing solutions.

- Expansion of cloud-native network infrastructures.

AI Impact Analysis on Service Provider Router

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is profoundly transforming the Service Provider Router market by enhancing network operational efficiency, predictive capabilities, and security posture. Users are keenly interested in how AI can automate complex network management tasks, optimize traffic routing in real-time, and proactively identify potential network failures. AI-driven analytics allow service providers to gain deeper insights into network performance, predict congestion patterns, and dynamically adjust network resources to maintain optimal service quality, especially critical in the era of 5G and increasing data volumes. This intelligence translates into reduced operational costs and improved customer experience, directly addressing key concerns of service providers.

Expectations for AI's influence also extend to advanced threat detection and anomaly identification. AI algorithms can analyze vast amounts of network data to detect sophisticated cyber threats and unusual network behavior that might bypass traditional security measures, thereby strengthening the resilience of service provider networks. Furthermore, AI is crucial for the continuous optimization of energy consumption in large-scale routing infrastructures, aligning with sustainability goals. The ability of AI to learn from network behavior and adapt configurations autonomously is viewed as a game-changer, promising more self-optimizing and self-healing networks, which is a significant area of focus for future router development and deployment strategies.

- Enhanced network automation and orchestration through AI/ML.

- Predictive analytics for network performance and fault detection.

- Real-time traffic optimization and dynamic routing path selection.

- AI-driven cybersecurity for advanced threat detection and anomaly identification.

- Improved resource management and energy efficiency in network operations.

- Automated configuration and self-healing network capabilities.

- Data-driven insights for capacity planning and network evolution.

Key Takeaways Service Provider Router Market Size & Forecast

Analysis of common user questions concerning the Service Provider Router market size and forecast reveals a strong interest in understanding the primary growth catalysts and the sustainability of the projected expansion. Users frequently inquire about the specific technologies driving this growth, such as 5G, and the long-term implications of increasing data consumption. The insights highlight that the market's robust CAGR is fundamentally underpinned by the global digital transformation, which necessitates ever more capable and resilient network infrastructure to support a myriad of connected devices and advanced services. The forecast emphasizes a sustained demand for routing solutions that can handle escalating traffic, provide ultra-low latency, and integrate sophisticated security features, making router upgrades and deployments a continuous investment area for service providers.

Another key takeaway is the geographic diversity of market growth, with significant opportunities emerging across both developed and developing regions as they embark on widespread 5G rollouts and digital infrastructure modernization. The substantial market valuation projected by 2033 underscores the critical role routers play in the foundational architecture of modern communication networks. It also signals a competitive landscape where innovation in router design, software capabilities, and energy efficiency will be pivotal for market leadership. The market's future will be characterized by ongoing technological advancements, strategic partnerships, and a focus on delivering scalable, secure, and highly performant routing solutions to meet the evolving demands of a hyper-connected world.

- Strong market growth driven by global 5G expansion and digital transformation.

- Significant investment in network upgrades and capacity enhancements anticipated.

- Technological advancements in SDN, NFV, and AI integration are key drivers.

- Demand for high-performance, low-latency, and secure routing solutions is paramount.

- Asia Pacific and North America expected to lead market expansion.

- Market size projected to nearly double by 2033, indicating sustained demand.

Service Provider Router Market Drivers Analysis

The Service Provider Router market is profoundly influenced by several key drivers that are compelling telecommunication companies and internet service providers to continuously upgrade and expand their network infrastructure. A primary driver is the accelerating global rollout of 5G networks, which demands high-capacity, low-latency, and highly flexible routing solutions to manage the massive influx of data traffic and myriad connected devices. This technological shift necessitates significant investments in new-generation routers capable of handling higher speeds and more complex network slicing requirements. Additionally, the exponential growth in internet traffic, fueled by video streaming, cloud computing, and online gaming, places immense pressure on existing networks, mandating robust routing solutions that can scale efficiently and reliably.

Furthermore, the increasing adoption of cloud services and the expansion of the Internet of Things (IoT) ecosystem are creating unprecedented demands for network bandwidth and connectivity at the edge. Service provider routers are critical in facilitating seamless and secure data flow between edge devices, cloud data centers, and end-users. The imperative for network virtualization, through technologies like Software-Defined Networking (SDN) and Network Function Virtualization (NFV), also acts as a significant driver. These technologies enable greater network agility, automation, and cost-effectiveness, pushing service providers to deploy routers that are compatible with virtualized environments and support dynamic resource allocation. These combined factors are collectively propelling the market forward, ensuring sustained investment in advanced routing technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Global 5G Network Rollout | +2.5% | Global, particularly North America, APAC, Europe | Short to Mid-term (2025-2030) |

| Exponential Growth in Internet Data Traffic | +1.8% | Global | Long-term (2025-2033) |

| Increasing Adoption of Cloud Services and IoT | +1.5% | North America, Europe, APAC | Mid-term (2026-2031) |

| Demand for Network Virtualization (SDN/NFV) | +1.2% | Global, focused on advanced economies | Mid to Long-term (2027-2033) |

| Rise of Edge Computing Architectures | +1.0% | Global | Mid to Long-term (2027-2033) |

Service Provider Router Market Restraints Analysis

Despite the robust growth drivers, the Service Provider Router market faces several significant restraints that could impede its expansion. One major challenge is the high initial capital expenditure required for deploying and upgrading advanced router infrastructure. Service providers often operate on tight budgets and the significant cost associated with acquiring cutting-edge hardware, software licenses, and integration services can be a substantial barrier, especially for smaller providers or those in developing regions. This high CapEx requirement can delay or scale back network modernization initiatives, slowing down overall market growth. Additionally, the complexity involved in managing and integrating these sophisticated routing solutions into existing legacy networks poses a significant operational hurdle, requiring specialized technical expertise and extensive planning.

Another restraint pertains to escalating cybersecurity threats and the continuous need for robust security features, which adds to the cost and complexity of router development and deployment. As networks become more interconnected and data flows more sensitive, routers must incorporate advanced threat detection and prevention mechanisms, increasing their price point and maintenance overhead. Furthermore, intense price competition among vendors, coupled with the long lifecycle of networking equipment, can suppress profit margins and limit investment in rapid innovation. Regulatory hurdles and compliance standards, particularly concerning data privacy and network neutrality in various regions, also introduce complexity and potential delays in market expansion. These factors collectively present challenges that service providers and vendors must navigate to sustain market momentum.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -1.5% | Global, particularly emerging markets | Long-term (2025-2033) |

| Complexity of Network Integration and Management | -1.2% | Global | Mid to Long-term (2026-2033) |

| Intense Price Competition Among Vendors | -0.8% | Global | Long-term (2025-2033) |

| Evolving Cybersecurity Threats and Regulatory Compliance | -0.7% | North America, Europe | Long-term (2025-2033) |

Service Provider Router Market Opportunities Analysis

The Service Provider Router market is rich with opportunities driven by technological advancements and evolving connectivity demands. A significant opportunity lies in the expansion of private 5G networks for enterprises across various industries, including manufacturing, logistics, and healthcare. These dedicated networks require specialized routing solutions that offer enhanced security, ultra-low latency, and guaranteed quality of service, creating a lucrative niche for router vendors. Furthermore, the increasing focus on smart cities initiatives and rural broadband expansion in underserved areas globally presents a substantial demand for robust and scalable routing infrastructure to support widespread connectivity and public services. These initiatives often involve government funding and partnerships, fostering a stable market for long-term deployments.

Another compelling opportunity emerges from the growing demand for advanced managed services offered by service providers. This includes network-as-a-service (NaaS) models, where routing infrastructure is delivered and managed as a service, allowing enterprises to consume network resources flexibly without significant upfront investment. This shift towards OpEx models for network infrastructure can accelerate adoption and open new revenue streams for service providers, subsequently boosting demand for compatible routers. The integration of Artificial Intelligence and Machine Learning into router operations for predictive maintenance, automated optimization, and enhanced security also represents a significant growth avenue. Routers equipped with AI capabilities can offer superior performance and operational efficiency, differentiating offerings in a competitive market and driving innovation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Private 5G Networks for Enterprises | +1.7% | North America, Europe, APAC | Mid to Long-term (2026-2033) |

| Growth in Smart City and Rural Broadband Initiatives | +1.5% | APAC, Latin America, Africa, Europe | Long-term (2025-2033) |

| Development of Network-as-a-Service (NaaS) Models | +1.3% | North America, Europe | Mid to Long-term (2027-2033) |

| Integration of AI/ML for Network Automation and Security | +1.0% | Global | Long-term (2028-2033) |

Service Provider Router Market Challenges Impact Analysis

The Service Provider Router market, while dynamic, faces several significant challenges that necessitate strategic responses from vendors and service providers alike. One prominent challenge is the increasing complexity of network architectures, driven by the convergence of various technologies such as 5G, IoT, and cloud computing. This complexity makes it harder to design, deploy, and manage routing infrastructure, requiring advanced skill sets and robust orchestration tools. The rapid pace of technological innovation further exacerbates this, as service providers constantly need to adapt their networks to new standards and functionalities, leading to shorter refresh cycles and higher operational overheads. Maintaining interoperability between diverse vendor equipment and ensuring seamless integration across various network domains remains a persistent hurdle.

Another critical challenge is the persistent supply chain disruptions, which can impact the availability of critical components, leading to delays in product delivery and network deployment. Geopolitical tensions, trade disputes, and global events have highlighted the vulnerability of the technology supply chain, forcing manufacturers to diversify sources and build resilience. Furthermore, the industry faces a shortage of skilled personnel with expertise in advanced networking technologies, including SDN, NFV, and AI-driven network management. This talent gap can hinder the efficient deployment, operation, and optimization of modern routing solutions, affecting overall market growth and the ability of service providers to fully leverage new technologies. Addressing these challenges requires collaborative efforts across the ecosystem, including investments in training, supply chain diversification, and open standards development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Network Complexity and Integration Issues | -1.0% | Global | Long-term (2025-2033) |

| Persistent Supply Chain Disruptions | -0.9% | Global | Short to Mid-term (2025-2027) |

| Shortage of Skilled Networking Personnel | -0.8% | Global | Long-term (2025-2033) |

| High Energy Consumption of Advanced Routing Hardware | -0.6% | Global | Long-term (2025-2033) |

Service Provider Router Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Service Provider Router market, covering key market dynamics, technological advancements, competitive landscape, and future growth trajectories. It delves into the segmentation by product type, application, and end-user, offering granular insights into market opportunities and challenges across different regions. The scope extends to a detailed assessment of the impact of emerging technologies such as 5G, SDN, NFV, and AI on router deployment and evolution. This report aims to equip stakeholders with actionable intelligence for strategic decision-making in a rapidly evolving telecommunications infrastructure landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 13.5 Billion |

| Market Forecast in 2033 | USD 25.4 Billion |

| Growth Rate | 8.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Cisco Systems Inc., Huawei Technologies Co. Ltd., Juniper Networks Inc., Nokia Corporation, Ericsson AB, Ciena Corporation, Hewlett Packard Enterprise (HPE), ZTE Corporation, NEC Corporation, D-Link Corporation, ADTRAN, Ekinops, Fujitsu, Infinera Corporation, Extreme Networks, Coriant, Telco Systems, Allied Telesis, Arista Networks, Mellanox Technologies (now NVIDIA) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Service Provider Router market is extensively segmented to provide a granular understanding of its diverse components and evolving landscape. These segmentations are critical for identifying specific growth areas, competitive dynamics, and technological shifts across different product types, underlying technologies, varied applications, and distinct end-user categories. The detailed breakdown allows for a comprehensive analysis of where demand is originating and how different router solutions are being deployed to address specific network requirements and service offerings within the global telecommunications infrastructure.

- By Type: This segment categorizes routers based on their functional placement within a service provider's network architecture.

- Core Routers: High-capacity routers forming the backbone of the network, handling aggregate traffic.

- Edge Routers: Connect core networks to external networks or customer premises, optimizing traffic flow at the network's periphery.

- Aggregation Routers: Collect traffic from multiple access points and funnel it to edge or core routers, often used in metro networks.

- By Technology: This segmentation focuses on the underlying technological principles and capabilities of the routers.

- Traditional Routers: Hardware-centric routers with fixed functions.

- Virtual Routers (vRouters): Software-based routers running on general-purpose hardware, offering flexibility and scalability.

- SDN/NFV-enabled Routers: Routers designed to integrate seamlessly with Software-Defined Networking and Network Function Virtualization architectures, enabling programmability and automation.

- By Application: This segment classifies routers based on their primary use cases within a service provider's operations.

- Fixed Line Broadband: Routers supporting internet access over wired connections (DSL, Fiber, Cable).

- Mobile Backhaul: Routers connecting cellular base stations to the core network, crucial for 4G and 5G.

- Data Center Interconnect (DCI): High-speed routers facilitating communication between geographically dispersed data centers.

- Cloud Networking: Routers optimized for connecting to and within cloud environments, ensuring efficient data exchange.

- Enterprise Connectivity: Routers used by service providers to offer managed network services to business customers.

- By End User: This segmentation defines the primary entities deploying and utilizing service provider routers.

- Telecom Operators: Traditional telecommunication companies providing voice and data services.

- Internet Service Providers (ISPs): Companies offering internet access to residential and business customers.

- Cloud Service Providers: Entities offering cloud computing resources and services, requiring robust routing for their infrastructure.

- Managed Service Providers (MSPs): Companies that manage IT services for other businesses, including network infrastructure.

Regional Highlights

- North America: This region maintains a significant market share due to early adoption of advanced networking technologies, extensive 5G deployments, and a strong presence of major telecom operators and cloud service providers. High data consumption, coupled with continuous infrastructure modernization, drives sustained demand for high-performance service provider routers. The presence of key industry innovators also fosters a dynamic competitive environment and rapid technological advancement.

- Europe: The European market is characterized by substantial investments in 5G infrastructure, particularly in countries like Germany, the UK, and France. Regulatory mandates for improved digital connectivity and a strong focus on network virtualization and energy efficiency are key drivers. The region exhibits a growing demand for edge computing solutions and secure routing capabilities to support diverse industry applications.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, primarily fueled by rapid economic growth, massive subscriber bases in countries like China and India, and extensive 5G rollouts. Government initiatives to expand digital infrastructure, increasing internet penetration in rural areas, and a burgeoning smart cities movement are propelling significant investments in service provider routers across the region.

- Latin America: This region is experiencing steady growth, driven by increasing internet penetration, expanding mobile broadband services, and ongoing efforts to upgrade existing network infrastructure. Investments in fiber optic networks and preparations for future 5G deployments are creating new opportunities for router vendors, particularly in major economies like Brazil and Mexico.

- Middle East and Africa (MEA): The MEA region is witnessing considerable growth, largely due to ambitious national digital transformation agendas, significant investments in 5G networks, and efforts to bridge the digital divide. Countries in the GCC region are leading in advanced network deployments, while growing mobile connectivity in Africa presents substantial long-term market potential for scalable routing solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Service Provider Router Market.- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- Juniper Networks Inc.

- Nokia Corporation

- Ericsson AB

- Ciena Corporation

- Hewlett Packard Enterprise (HPE)

- ZTE Corporation

- NEC Corporation

- D-Link Corporation

- ADTRAN

- Ekinops

- Fujitsu

- Infinera Corporation

- Extreme Networks

- Coriant

- Telco Systems

- Allied Telesis

- Arista Networks

- Mellanox Technologies (now NVIDIA)

Frequently Asked Questions

Analyze common user questions about the Service Provider Router market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a Service Provider Router?

A Service Provider Router is a high-capacity, robust networking device designed to handle vast amounts of data traffic and complex routing decisions across large-scale communication networks, such as those operated by telecom companies, ISPs, and cloud providers. These routers form the backbone of the internet and telecommunications infrastructure, enabling connectivity for millions of users and devices.

How is 5G impacting the Service Provider Router Market?

5G is significantly impacting the market by driving demand for more powerful, low-latency, and high-bandwidth routers. It necessitates upgrades to core and edge routing infrastructure to support increased data volumes, network slicing, and new applications like IoT and edge computing, leading to substantial market growth and innovation.

What are the primary challenges in the Service Provider Router Market?

Key challenges include the high initial capital expenditure for advanced router deployment, the increasing complexity of network management, persistent global supply chain disruptions impacting component availability, and a shortage of skilled networking professionals to manage sophisticated systems.

What role does AI play in Service Provider Routers?

AI is increasingly used to enhance router functionality through automation of network operations, real-time traffic optimization, predictive maintenance, and advanced cybersecurity threat detection. AI-driven routers aim for greater efficiency, resilience, and self-healing capabilities.

What are the key growth opportunities for Service Provider Router vendors?

Significant opportunities include the expansion of private 5G networks for enterprises, government initiatives for smart cities and rural broadband, the adoption of Network-as-a-Service (NaaS) models, and the continuous integration of AI/ML for network intelligence and automation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted