Semiconductor Package Substrate Market

Semiconductor Package Substrate Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706653 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

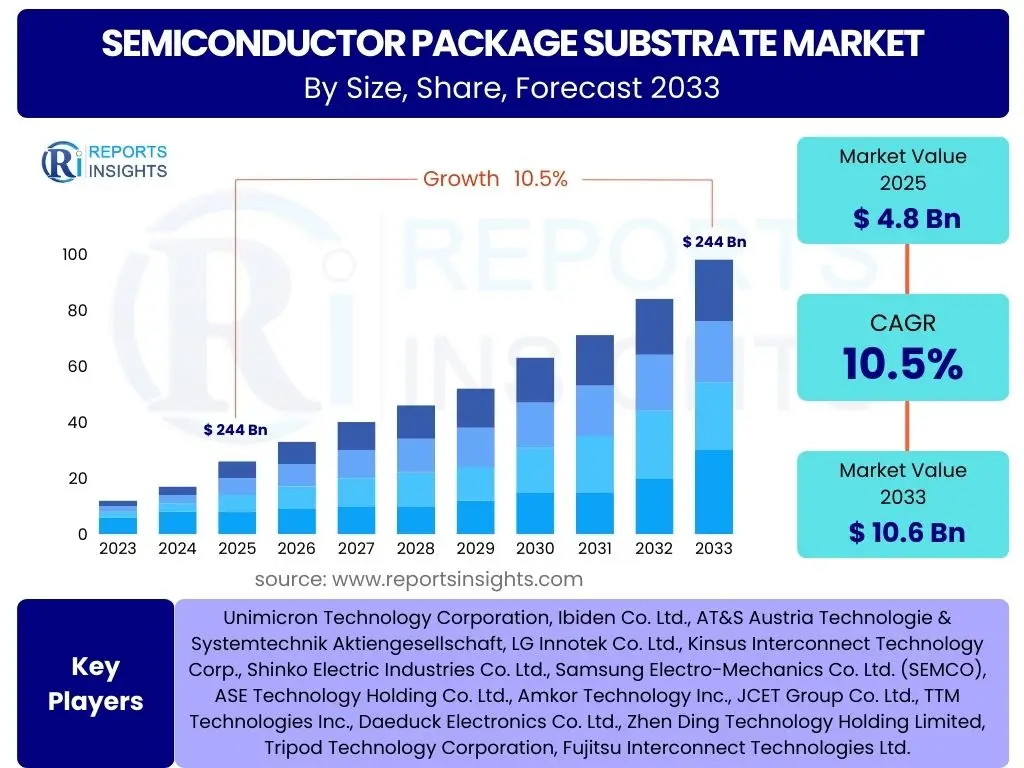

Semiconductor Package Substrate Market Size

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Package Substrate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033. The market is estimated at USD 4.8 Billion in 2025 and is projected to reach USD 10.6 Billion by the end of the forecast period in 2033.

Key Semiconductor Package Substrate Market Trends & Insights

The semiconductor package substrate market is undergoing significant transformation driven by the relentless demand for smaller, more powerful, and energy-efficient electronic devices. Key trends revolve around advancements in packaging technologies, such as advanced flip-chip and fan-out solutions, which enable higher integration density and improved electrical performance. Miniaturization continues to be a dominant force, pushing the boundaries of substrate design and material science to accommodate increasing transistor counts and complex chip architectures. Furthermore, the convergence of high-performance computing (HPC), artificial intelligence (AI), and 5G communication is creating a robust demand for substrates capable of handling high-speed data transfer and managing thermal dissipation effectively.

Environmental concerns and supply chain resilience are also shaping market trends. There is a growing emphasis on developing sustainable manufacturing processes and using eco-friendly materials to reduce the environmental footprint of semiconductor production. Geopolitical shifts and global events have highlighted the fragility of traditional supply chains, prompting a push towards regionalization and diversification of manufacturing bases to enhance robustness and reduce reliance on single points of failure. These combined factors are driving innovation in materials, design, and manufacturing processes within the semiconductor package substrate industry, focusing on performance, cost-efficiency, and sustainability.

- Advanced Packaging Technologies: Adoption of flip-chip, fan-out, and 3D stacking for higher integration and performance.

- Miniaturization and High-Density Interconnects: Demand for finer line widths and spaces to accommodate complex chip designs.

- High-Performance Computing (HPC) and AI Integration: Specialization of substrates for high-speed data, power delivery, and thermal management in data centers and AI accelerators.

- 5G and IoT Device Proliferation: Increased demand for compact, reliable, and energy-efficient substrates for connectivity devices.

- Sustainability and Green Manufacturing: Focus on eco-friendly materials, reduced waste, and energy-efficient production processes.

- Supply Chain Diversification: Efforts to regionalize manufacturing and secure resilient supply chains to mitigate geopolitical risks.

AI Impact Analysis on Semiconductor Package Substrate

The burgeoning field of artificial intelligence (AI) is profoundly impacting the semiconductor package substrate market, primarily by driving an unprecedented demand for high-performance computing (HPC) and specialized AI accelerators. AI workloads, characterized by massive parallel processing and high data throughput, necessitate advanced packaging solutions that can support greater integration of multiple dies (CPUs, GPUs, memory) within a single package. This drives innovation in areas like interposer technology, enabling ultra-fast communication between chips, and thermal management solutions, as AI processors generate significant heat. Users are increasingly concerned with substrates that offer superior electrical performance, low latency, and efficient power delivery to maximize AI chip capabilities.

Furthermore, AI is not just a consumer of advanced substrates but also a catalyst for their design and manufacturing. AI and machine learning algorithms are being employed in substrate design optimization, material discovery, and process control to improve yield, reduce defects, and accelerate time-to-market. The complexity of future AI chips will push the limits of traditional substrate manufacturing, making AI-driven automation and predictive maintenance crucial for maintaining efficiency and quality. Expectations are high for substrates that can facilitate chiplets and heterogeneous integration, creating modular and scalable AI systems, thereby further solidifying the symbiotic relationship between AI and advanced packaging.

- Increased Demand for High-Performance Substrates: AI processors require advanced substrates for high data rates and power delivery.

- Enhanced Thermal Management Requirements: AI chips generate substantial heat, necessitating improved substrate cooling solutions.

- Promotion of Heterogeneous Integration: Substrates must accommodate multiple chiplets (CPU, GPU, memory) for AI systems.

- Advanced Material Innovation: Driving research into novel materials for better electrical and thermal properties.

- AI-Driven Design and Manufacturing: Utilizing AI for substrate design optimization, yield improvement, and predictive maintenance in production.

Key Takeaways Semiconductor Package Substrate Market Size & Forecast

The semiconductor package substrate market is poised for robust growth, underpinned by fundamental shifts in the electronics industry. A critical takeaway is the escalating demand for advanced packaging technologies, which are essential for unlocking the full potential of next-generation semiconductors, particularly those designed for AI, HPC, and 5G applications. The market's expansion is not merely volume-driven but also driven by the increasing complexity and value of individual substrate units, reflecting the sophisticated requirements of modern electronic devices. This implies significant opportunities for companies that can innovate in materials science, manufacturing precision, and design capabilities.

Another significant insight is the strategic importance of supply chain resilience and regional manufacturing capabilities. Geopolitical factors and the lessons learned from recent global disruptions are compelling industry players to diversify their supply chains and invest in regional production hubs. This shift will likely lead to a more distributed manufacturing landscape, influencing investment patterns and fostering localized technological expertise. Ultimately, the market forecast underscores a dynamic sector characterized by rapid technological evolution, strong demand from high-growth end-use applications, and a strategic imperative for global supply chain optimization.

- Significant Growth Trajectory: The market is projected for substantial growth, driven by advanced technological demands.

- Pivotal Role of Advanced Packaging: Substrates are central to enabling high-performance computing, AI, and 5G functionalities.

- Innovation in Materials and Manufacturing: Continuous advancements are critical for meeting performance, miniaturization, and thermal management needs.

- Supply Chain Resilience: Growing emphasis on diversified and regionalized manufacturing bases for stability.

- Strategic Investment Opportunities: Attractive landscape for stakeholders focused on high-value, high-performance substrate solutions.

Semiconductor Package Substrate Market Drivers Analysis

The incessant drive for miniaturization in electronic devices remains a primary catalyst for the semiconductor package substrate market. As consumers and industries demand more compact and portable devices with enhanced functionalities, semiconductor manufacturers are compelled to integrate more components into smaller footprints. This pushes the boundaries of substrate technology, requiring finer line widths and spaces, higher layer counts, and advanced materials capable of supporting complex circuits within shrinking dimensions. The evolution of smartphones, wearables, and compact IoT devices critically depends on the advancements in high-density package substrates that can accommodate System-in-Package (SiP) and System-on-Chip (SoC) solutions efficiently.

The escalating demand for High-Performance Computing (HPC), Artificial Intelligence (AI), and 5G technologies is fundamentally reshaping the substrate market. These applications require massive data processing capabilities, ultra-low latency, and efficient power delivery, which cannot be achieved with conventional packaging methods. Advanced substrates, such as those used in flip-chip Ball Grid Arrays (FCBGAs) for GPUs and specialized interposers for AI accelerators, are crucial for managing the high-speed signals, dense interconnections, and significant thermal loads generated by these powerful chips. The transition to 5G connectivity also mandates smaller, higher-frequency-compatible substrates for base stations, network equipment, and end-user devices, further propelling market growth.

Moreover, the expansion of the Internet of Things (IoT) and the electrification of the automotive industry are creating diversified opportunities. IoT devices, ranging from smart home appliances to industrial sensors, demand low-cost, low-power, and often ruggedized substrates. In the automotive sector, the rise of electric vehicles (EVs) and autonomous driving systems necessitates highly reliable, durable, and thermally efficient substrates for power modules, infotainment systems, and advanced driver-assistance systems (ADAS). These varied application requirements collectively contribute to the sustained growth and innovation within the semiconductor package substrate market, emphasizing both performance and cost-effectiveness across different segments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization and Compact Device Demand | +2.1% | Global, particularly Asia Pacific (Consumer Electronics) | Short to Mid-term (2025-2030) |

| Growth in High-Performance Computing (HPC) & AI | +2.5% | North America, Asia Pacific (Data Centers, AI Research Hubs) | Long-term (2025-2033) |

| Proliferation of 5G Technology and IoT Devices | +1.8% | Global, especially China, South Korea, US, Europe | Mid-term (2026-2031) |

| Increasing Adoption of Electric Vehicles (EVs) and ADAS | +1.5% | Europe, North America, China (Automotive Manufacturing Hubs) | Long-term (2027-2033) |

| Advancements in Advanced Packaging Technologies (e.g., Fan-Out, 3D IC) | +1.9% | Global (Semiconductor Industry Leaders) | Short to Mid-term (2025-2030) |

Semiconductor Package Substrate Market Restraints Analysis

The semiconductor package substrate market faces significant restraints, primarily stemming from the substantial research and development (R&D) costs associated with developing advanced substrate technologies. As chip designs become more intricate and demands for miniaturization and higher performance intensify, the complexity of substrate materials and manufacturing processes increases exponentially. This necessitates heavy investment in cutting-edge equipment, novel material science, and sophisticated design tools, which can be a barrier for new entrants and can strain the profit margins of existing players, especially smaller ones. The continuous need for innovation means R&D cycles are short, requiring constant expenditure to remain competitive.

Another critical restraint is the inherent volatility and vulnerability of the global supply chain for raw materials and specialized components. The production of semiconductor package substrates relies on a complex web of global suppliers for critical materials such as BT resin, ABF (Ajinomoto Build-up Film), copper foils, and various chemicals. Geopolitical tensions, trade disputes, natural disasters, and pandemics can severely disrupt the availability and pricing of these materials, leading to production delays, increased costs, and ultimately impacting market stability. The concentrated nature of certain material suppliers also poses a significant risk, as reliance on a few key sources can exacerbate supply chain shocks.

Furthermore, the high capital expenditure required for establishing and upgrading manufacturing facilities acts as a significant impediment to market expansion and agility. Building a state-of-the-art substrate manufacturing plant involves investments of hundreds of millions to billions of dollars, making it a capital-intensive industry. This high barrier to entry limits the number of new players and can slow down the adoption of new technologies if existing players are hesitant to commit such large sums for uncertain returns. Additionally, the industry is highly susceptible to economic downturns, which can lead to reduced investment in new capacity and R&D, thereby slowing down overall market growth. Managing these high costs and supply chain risks remains a persistent challenge for the market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development (R&D) Costs | -1.2% | Global (Industry-wide) | Long-term (2025-2033) |

| Volatility of Global Supply Chains and Raw Material Prices | -1.5% | Global, particularly regions dependent on specific material imports | Short to Mid-term (2025-2029) |

| Significant Capital Expenditure for Manufacturing Facilities | -0.8% | Global (Especially for new entrants) | Long-term (2025-2033) |

| Intense Competition and Pricing Pressure | -0.7% | Asia Pacific (High concentration of manufacturers) | Mid-term (2026-2031) |

| Technological Complexity and Yield Management Challenges | -0.9% | Global (Advanced technology nodes) | Short to Mid-term (2025-2028) |

Semiconductor Package Substrate Market Opportunities Analysis

The advent of advanced packaging technologies presents a significant growth opportunity for the semiconductor package substrate market. As Moore's Law faces increasing physical limitations, the industry is shifting focus from simply shrinking transistors to integrating multiple components in sophisticated ways. Technologies like fan-out wafer-level packaging (FOWLP), system-in-package (SiP), and 3D stacking allow for greater functionality, performance, and miniaturization without relying solely on transistor scaling. This trend necessitates highly specialized and complex substrates capable of supporting these multi-chip architectures, offering a premium segment for innovation in materials and design, such as glass substrates and multi-layer organic substrates with finer pitches. The adoption of these advanced methods is critical for future high-performance applications.

Emerging markets, particularly in Southeast Asia, India, and parts of Latin America, offer substantial untapped potential. As these regions experience rapid economic development and increasing disposable incomes, the demand for consumer electronics, automotive components, and IT infrastructure is surging. This translates into a growing need for semiconductor package substrates to power a wide array of devices. Companies that can establish local manufacturing capabilities, tailor products to regional cost sensitivities, and build robust distribution networks within these emerging economies stand to gain significant market share. These regions often provide favorable investment environments and a growing talent pool, making them attractive for strategic expansion.

Furthermore, the increasing focus on sustainability and eco-friendly manufacturing provides an opportunity for market differentiation and innovation. Growing global awareness of environmental impact is pushing industries to adopt greener practices. For semiconductor package substrates, this translates to opportunities in developing recyclable or biodegradable materials, implementing energy-efficient manufacturing processes, and reducing waste generation. Companies that invest in and promote sustainable solutions can not only meet regulatory requirements but also appeal to environmentally conscious consumers and businesses, potentially unlocking new market segments and enhancing brand reputation. This shift towards green technologies can also foster collaboration between material science companies and substrate manufacturers to develop next-generation sustainable products.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Advanced Packaging Technologies (e.g., FOWLP, SiP, 3D IC) | +2.3% | Global (Key semiconductor manufacturing hubs) | Short to Mid-term (2025-2030) |

| Growth in Emerging Markets (e.g., India, Southeast Asia) | +1.7% | Asia Pacific, Latin America | Mid to Long-term (2027-2033) |

| Focus on Sustainable and Eco-friendly Manufacturing Practices | +1.0% | Europe, North America, Japan (Environmentally conscious regions) | Long-term (2028-2033) |

| Development of Novel Materials (e.g., glass substrates, advanced polymers) | +1.4% | Global (R&D focused regions) | Mid to Long-term (2027-2033) |

| Increased Demand for Custom and Application-Specific Substrates | +0.9% | Global (Specialized industries) | Short to Mid-term (2025-2030) |

Semiconductor Package Substrate Market Challenges Impact Analysis

One of the primary challenges for the semiconductor package substrate market is the rapid pace of technological obsolescence. The semiconductor industry is characterized by extremely short product life cycles and continuous innovation, driven by Moore's Law and the escalating demands for higher performance and smaller form factors. This means that current substrate technologies can quickly become outdated as new materials, designs, and manufacturing processes emerge. Manufacturers must constantly invest in R&D and upgrade their facilities, which is both capital-intensive and risky. Failure to keep pace with these advancements can lead to a loss of competitiveness and market share, requiring significant strategic agility and foresight.

Another significant challenge is the ongoing talent shortage, particularly for skilled engineers and technicians specializing in advanced materials science, microelectronics, and high-precision manufacturing. The complexity of designing and producing modern semiconductor package substrates demands highly specialized expertise, which is in limited supply globally. This shortage can lead to increased labor costs, delays in R&D and production, and hinder the adoption of advanced manufacturing techniques. Companies are increasingly competing for a small pool of qualified professionals, making recruitment and retention a critical concern that impacts innovation cycles and operational efficiency across the industry.

Furthermore, stringent quality control and yield management pose continuous operational challenges. The manufacturing of semiconductor package substrates involves highly intricate processes with extremely tight tolerances, where even microscopic defects can render a product unusable. Maintaining consistently high yields is crucial for profitability, given the high cost of raw materials and manufacturing. As design rules shrink and packaging becomes more complex, achieving acceptable yields becomes increasingly difficult, requiring sophisticated inspection systems, process optimization, and robust statistical process control. Any deviation can lead to significant material waste and production losses, impacting overall market supply and profitability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Innovation Pace | -1.0% | Global (High-tech regions) | Continuous (2025-2033) |

| Shortage of Skilled Workforce and Talent Acquisition | -0.8% | North America, Europe, Japan, Taiwan, South Korea | Long-term (2025-2033) |

| Stringent Quality Control and Yield Management | -0.9% | Global (Advanced manufacturing regions) | Short to Mid-term (2025-2030) |

| Increasing Environmental Regulations and Compliance Costs | -0.6% | Europe, North America, Japan (Stricter regulations) | Mid to Long-term (2027-2033) |

| Geopolitical Tensions and Trade Barriers | -1.1% | Global (Impacts cross-border trade and investment) | Short to Mid-term (2025-2029) |

Semiconductor Package Substrate Market - Updated Report Scope

This report provides an in-depth analysis of the Semiconductor Package Substrate Market, offering a comprehensive overview of its current state, historical performance, and future growth projections. It delves into the market size, key trends, drivers, restraints, opportunities, and challenges influencing its trajectory from 2025 to 2033. The report meticulously segments the market by various types, packaging technologies, and end-use applications, providing detailed insights into each segment's dynamics and regional contributions. Furthermore, it profiles key market players, offering competitive intelligence and strategic recommendations for stakeholders navigating this evolving landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 10.6 Billion |

| Growth Rate | 10.5% |

| Number of Pages | 257 |

| Key Trends | >|

| Segments Covered | >|

| Key Companies Covered | Unimicron Technology Corporation, Ibiden Co. Ltd., AT&S Austria Technologie & Systemtechnik Aktiengesellschaft, LG Innotek Co. Ltd., Kinsus Interconnect Technology Corp., Shinko Electric Industries Co. Ltd., Samsung Electro-Mechanics Co. Ltd. (SEMCO), ASE Technology Holding Co. Ltd., Amkor Technology Inc., JCET Group Co. Ltd., TTM Technologies Inc., Daeduck Electronics Co. Ltd., Zhen Ding Technology Holding Limited, Tripod Technology Corporation, Fujitsu Interconnect Technologies Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor package substrate market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segmentations allow for a detailed analysis of market dynamics across different technologies, applications, and material types, revealing specific growth pockets and competitive landscapes. Understanding these divisions is crucial for stakeholders to identify lucrative opportunities and tailor their product strategies effectively within a complex and rapidly evolving industry. Each segment exhibits unique characteristics influenced by technological advancements and end-user demands, shaping the overall market trajectory.

The market is primarily segmented by Type, differentiating between organic and inorganic substrates based on their material composition and performance characteristics. Organic substrates, predominantly made from BT resin and Ajinomoto Build-up Film (ABF), are widely used due to their cost-effectiveness and flexibility, particularly in consumer electronics. Inorganic substrates, such as ceramic and glass, offer superior thermal and electrical performance, making them suitable for high-frequency and high-power applications. Further segmentation by Packaging Type, including Flip Chip BGA (FCBGA), Wire Bond BGA (WBBGA), and advanced solutions like Fan-Out Wafer Level Packages (FOWLP) and System-in-Package (SiP), highlights the technological evolution aimed at achieving higher integration density and improved signal integrity. These packaging types directly influence the design and material requirements of the corresponding substrates.

The market's application-based segmentation provides insights into the diverse end-use industries driving demand. Consumer Electronics, encompassing smartphones, laptops, and wearables, remains a significant segment due to the sheer volume of devices and the continuous pursuit of miniaturization and enhanced features. The Automotive sector is rapidly growing, driven by the increasing adoption of electric vehicles, autonomous driving systems, and advanced infotainment. IT & Telecommunication, fueled by 5G infrastructure, data centers, and cloud computing, demands high-speed, high-reliability substrates. Industrial applications, healthcare devices, and aerospace & defense also contribute to market growth, each requiring specialized substrates tailored to their unique performance and reliability specifications. This multi-faceted segmentation helps to delineate the market's structure and identify key areas of growth and innovation.

- By Type:

- Organic Substrates (BT Resin, ABF)

- Inorganic Substrates (Ceramic, Glass)

- By Packaging Type:

- Flip Chip BGA (FCBGA)

- Wire Bond BGA (WBBGA)

- Chip Scale Package (CSP)

- System-in-Package (SiP)

- Fan-Out Wafer Level Package (FOWLP)

- Fan-In Wafer Level Package (FIWLP)

- By Application:

- Consumer Electronics

- Automotive

- Industrial

- IT & Telecommunication

- Healthcare

- Aerospace & Defense

Regional Highlights

- Asia Pacific (APAC): The Asia Pacific region dominates the semiconductor package substrate market due to the concentration of major semiconductor manufacturing hubs, including Taiwan, South Korea, Japan, and China. This region benefits from a robust ecosystem of foundries, outsourced semiconductor assembly and test (OSAT) companies, and leading electronics manufacturers. The strong demand from consumer electronics, coupled with significant investments in 5G infrastructure and AI development, fuels consistent growth. China, in particular, is a major growth engine driven by its large domestic electronics market and aggressive government support for semiconductor self-sufficiency.

- North America: North America is a significant market, propelled by strong demand from high-performance computing (HPC), artificial intelligence (AI), and advanced automotive electronics sectors. The region is home to leading fabless semiconductor companies and data center operators that drive innovation in chip design and advanced packaging. While less focused on high-volume manufacturing compared to APAC, North America leads in R&D for next-generation substrate technologies and specialized, high-value applications. Investments in domestic manufacturing capabilities are also increasing to enhance supply chain resilience.

- Europe: Europe represents a strong market for semiconductor package substrates, especially driven by its robust automotive, industrial, and telecommunications sectors. The region has a focus on high-reliability and specialized applications, with a growing emphasis on electric vehicles, industrial automation, and advanced connectivity solutions. European initiatives for semiconductor independence and the push towards sustainable manufacturing practices also influence the market dynamics, fostering innovation in eco-friendly materials and processes.

- Latin America: The Latin American market for semiconductor package substrates is emerging, driven by increasing industrialization, expanding consumer electronics markets, and growing penetration of IoT devices. While currently a smaller share, the region offers long-term growth potential as economic development progresses and local manufacturing capabilities expand. Brazil and Mexico are key countries, benefiting from investments in automotive and electronics assembly plants.

- Middle East and Africa (MEA): The Middle East and Africa region is an nascent but growing market, primarily influenced by investments in digital infrastructure, smart city initiatives, and the increasing adoption of consumer electronics. Countries in the Gulf Cooperation Council (GCC) are investing heavily in diversifying their economies, including the development of local technology sectors, which is expected to drive future demand for semiconductor components, including package substrates.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Package Substrate Market.- Unimicron Technology Corporation

- Ibiden Co. Ltd.

- AT&S Austria Technologie & Systemtechnik Aktiengesellschaft

- LG Innotek Co. Ltd.

- Kinsus Interconnect Technology Corp.

- Shinko Electric Industries Co. Ltd.

- Samsung Electro-Mechanics Co. Ltd. (SEMCO)

- ASE Technology Holding Co. Ltd.

- Amkor Technology Inc.

- JCET Group Co. Ltd.

- TTM Technologies Inc.

- Daeduck Electronics Co. Ltd.

- Zhen Ding Technology Holding Limited

- Tripod Technology Corporation

- Fujitsu Interconnect Technologies Ltd.

Frequently Asked Questions

What is a semiconductor package substrate?

A semiconductor package substrate is a critical component that serves as an electrical and mechanical interface between the silicon chip (die) and the printed circuit board (PCB). It provides electrical interconnections, distributes power, dissipates heat, and protects the chip from external damage, enabling the entire electronic device to function.

What factors are driving the growth of the semiconductor package substrate market?

The market's growth is primarily driven by the increasing demand for miniaturization in electronic devices, the rapid proliferation of 5G technology, the surge in High-Performance Computing (HPC) and Artificial Intelligence (AI) applications, and the robust expansion of the electric vehicle and Internet of Things (IoT) markets.

How does AI impact the semiconductor package substrate industry?

AI significantly impacts the industry by demanding high-performance substrates capable of managing high data rates and thermal loads from AI processors. It also influences substrate design and manufacturing through AI-driven optimization, improving efficiency, yield, and accelerating new material discovery.

What are the key challenges faced by the semiconductor package substrate market?

Key challenges include high research and development costs, the volatility and vulnerability of global supply chains for raw materials, the significant capital expenditure required for manufacturing facilities, the rapid pace of technological obsolescence, and a shortage of skilled labor.

Which regions are key contributors to the semiconductor package substrate market?

Asia Pacific is the dominant region due to its concentration of manufacturing hubs and high demand from consumer electronics. North America and Europe are also significant contributors, driven by HPC, AI, automotive, and industrial applications, while emerging markets in Latin America and MEA show promising growth potential.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted