Semiconductor Lithography Equipment Market

Semiconductor Lithography Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709645 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

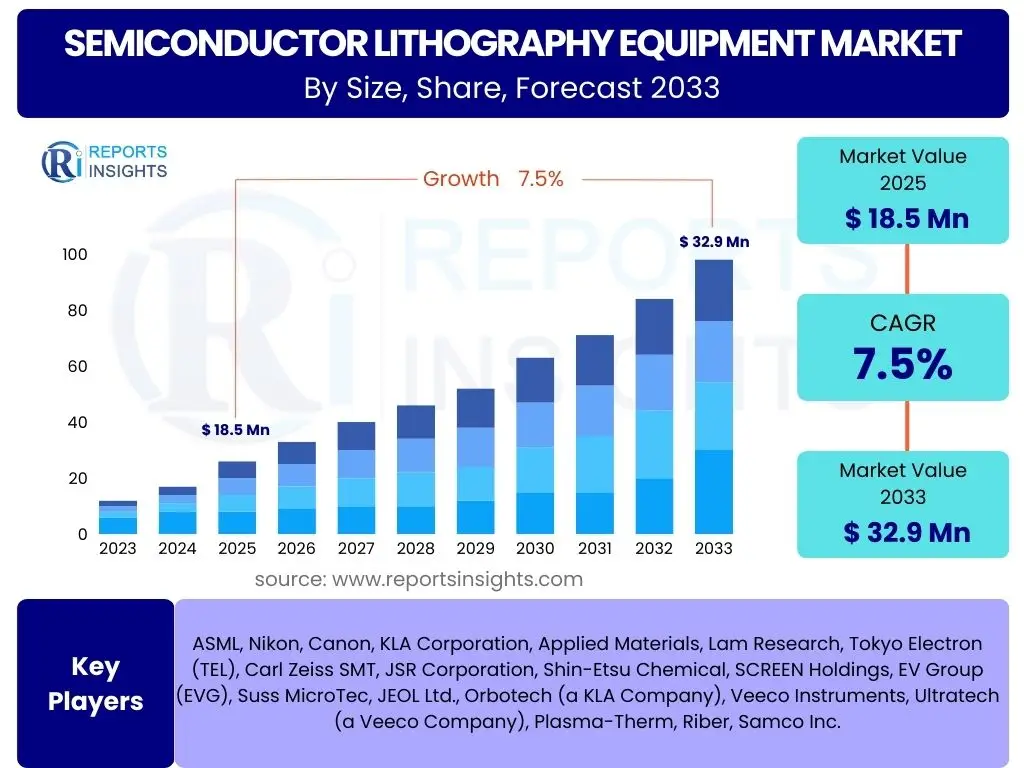

Semiconductor Lithography Equipment Market Size

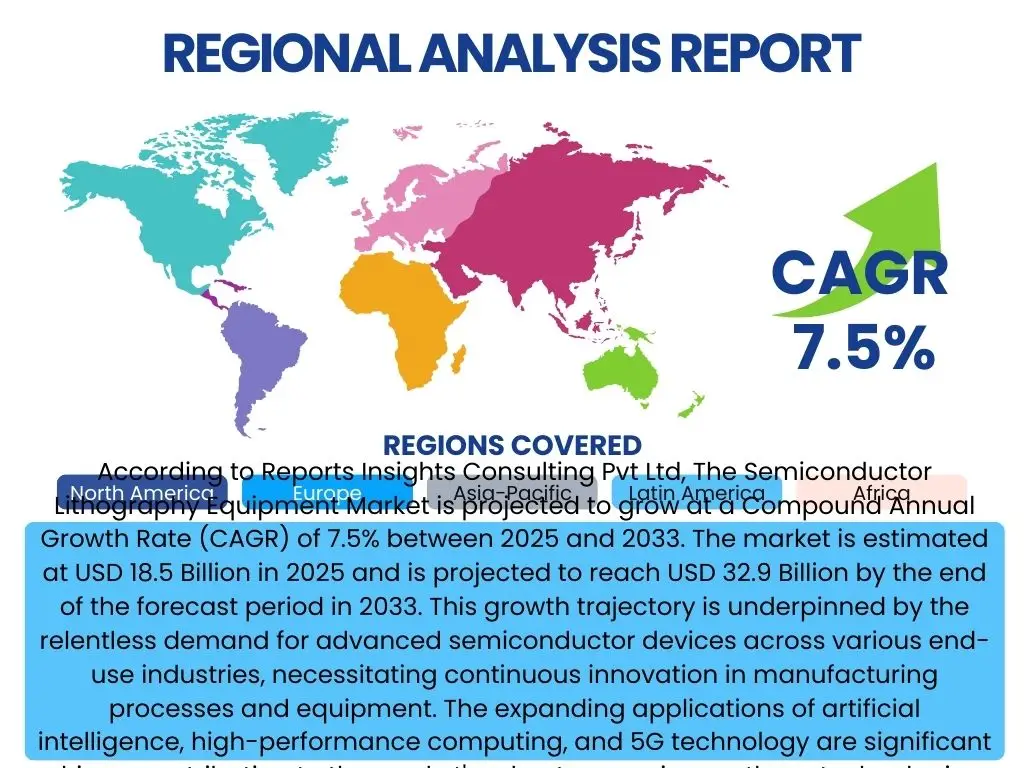

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Lithography Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 32.9 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by the relentless demand for advanced semiconductor devices across various end-use industries, necessitating continuous innovation in manufacturing processes and equipment. The expanding applications of artificial intelligence, high-performance computing, and 5G technology are significant drivers contributing to the market's robust expansion, as these technologies require increasingly sophisticated and miniaturized chips.

The market's valuation reflects substantial investments in research and development by key industry players, focusing on next-generation lithography technologies such as Extreme Ultraviolet (EUV) lithography. These investments are critical for achieving higher resolution patterns and increasing transistor density, which are essential for manufacturing smaller, faster, and more power-efficient semiconductors. The projected market size in 2033 also accounts for the anticipated ramp-up in fabrication plant capacities globally, particularly in regions striving for semiconductor manufacturing self-sufficiency. Geopolitical factors and strategic national initiatives to bolster domestic chip production further influence the long-term market outlook and capital expenditure plans within the industry.

Key Semiconductor Lithography Equipment Market Trends & Insights

User inquiries frequently highlight the escalating demand for higher precision and throughput in semiconductor manufacturing, driven by the pervasive need for smaller, more powerful, and energy-efficient electronic devices. This emphasis on advanced capabilities underscores a critical industry shift towards cutting-edge lithography technologies. Furthermore, there is considerable interest in how geopolitical considerations and the imperative for supply chain resilience are shaping market dynamics, particularly concerning regional investment and technological independence. The integration of smart manufacturing principles and advanced analytics into lithography processes also emerges as a key area of user focus, pointing towards a future where automation and data-driven insights optimize production efficiency and yield.

- Escalating adoption of Extreme Ultraviolet (EUV) lithography for manufacturing advanced nodes below 7nm, signifying a major technological shift.

- Increasing focus on double patterning and multi-patterning techniques for DUV lithography to extend its capabilities for finer feature sizes.

- Growing integration of Artificial Intelligence (AI) and Machine Learning (ML) for process optimization, predictive maintenance, and yield enhancement in lithography equipment.

- Strategic investments in regional semiconductor manufacturing hubs, driven by geopolitical considerations and the pursuit of supply chain resilience.

- Development of advanced resist materials and innovative mask technologies to complement next-generation lithography systems.

- Emphasis on eco-friendly and sustainable manufacturing practices, leading to equipment designs with lower energy consumption and reduced chemical waste.

- Expansion of the market into new application areas such as advanced packaging, MEMS, and photonics, leveraging lithography for diverse device fabrication.

AI Impact Analysis on Semiconductor Lithography Equipment

Common user questions regarding AI's impact on semiconductor lithography equipment frequently revolve around its potential to revolutionize operational efficiency, precision, and yield. Users are keen to understand how AI can address the complex challenges inherent in advanced lithography, such as defect detection, process variability, and equipment downtime. There is significant interest in AI's role in enabling predictive maintenance for highly sophisticated lithography tools, thereby minimizing unscheduled interruptions and maximizing equipment utilization. Furthermore, inquiries often touch upon AI's capabilities in optimizing exposure parameters, improving pattern fidelity, and accelerating the design-to-manufacturing cycle, all of which are critical for staying competitive in a rapidly evolving semiconductor landscape.

The integration of artificial intelligence into semiconductor lithography equipment is poised to bring about transformative changes, addressing some of the most pressing challenges in advanced chip manufacturing. AI algorithms can process vast amounts of sensor data from lithography tools in real-time, enabling predictive analytics for identifying potential equipment failures before they occur. This capability significantly reduces costly downtime and enhances overall equipment effectiveness (OEE). Moreover, AI-powered systems are being developed to optimize complex exposure parameters and alignment processes, leading to improved pattern fidelity and reduced defect rates, which are crucial for the yield of high-volume manufacturing of advanced nodes. Such advancements enable a higher degree of automation and precision that was previously unattainable through traditional control systems.

- Enhanced Predictive Maintenance: AI algorithms analyze sensor data to forecast equipment failures, reducing downtime and maintenance costs.

- Optimized Process Control: Machine learning models fine-tune exposure parameters and focus settings in real-time, improving pattern uniformity and critical dimension (CD) control.

- Accelerated Defect Detection and Classification: AI-driven image analysis rapidly identifies and categorizes lithography defects, enabling faster corrective actions.

- Improved Yield Management: AI correlates process data with wafer yield, providing insights to optimize manufacturing steps and reduce scrap.

- Automated Recipe Generation: AI assists in generating and adjusting complex lithography recipes, shortening development cycles for new processes.

- Advanced Metrology and Inspection: AI enhances the accuracy and speed of in-line metrology and inspection systems, providing better feedback for process control.

- Support for Design-Technology Co-Optimization (DTCO): AI facilitates better collaboration between design and manufacturing, optimizing mask designs for lithography constraints.

Key Takeaways Semiconductor Lithography Equipment Market Size & Forecast

User queries regarding key takeaways from the Semiconductor Lithography Equipment market size and forecast consistently point to the strategic importance of understanding long-term growth drivers, particularly the sustained demand for advanced computing and connectivity. Users are interested in discerning which technological advancements will command the most significant investment and market share, with a notable focus on the transition to EUV lithography. There is also a keen desire for insights into the resilience of the market against macroeconomic fluctuations and geopolitical tensions, alongside the critical role of innovation in sustaining competitive advantages. The market's overall health and future direction are often viewed through the lens of capacity expansion projects and the evolving landscape of global semiconductor supply chains.

The Semiconductor Lithography Equipment Market is characterized by robust growth driven primarily by the global demand for increasingly sophisticated semiconductor devices. The forecasted market expansion reflects significant ongoing investments in next-generation fabrication technologies, with Extreme Ultraviolet (EUV) lithography emerging as a pivotal factor for future manufacturing nodes. Stakeholders must recognize the critical interplay between technological advancements, geopolitical influences on supply chain localization, and the relentless pursuit of enhanced efficiency and yield. The market's resilience is tied to its ability to innovate and adapt to these complex dynamics, ensuring continued support for the broader electronics industry.

- Sustained Market Growth: The market is projected for significant growth, driven by escalating demand for advanced semiconductors in AI, 5G, IoT, and high-performance computing.

- EUV Lithography Dominance: EUV technology is a primary growth engine, critical for manufacturing chips at advanced nodes (7nm and below), necessitating substantial capital expenditure.

- Technological Innovation Imperative: Continuous R&D in areas like advanced optics, resist materials, and process control is essential for competitive advantage and market leadership.

- Geopolitical and Supply Chain Influence: National strategies to bolster domestic semiconductor production are shaping investment patterns and fostering regional market development.

- Focus on Automation and AI Integration: Increasing adoption of AI and machine learning for optimizing process control, predictive maintenance, and yield management is a key differentiator.

- High Capital Intensity: The market remains highly capital-intensive, with substantial barriers to entry and a focus on long-term strategic investments by key players.

- Emerging Application Expansion: Growth extends beyond traditional logic and memory into advanced packaging, MEMS, and power semiconductors, broadening the market scope.

Semiconductor Lithography Equipment Market Drivers Analysis

The semiconductor lithography equipment market is fundamentally propelled by the insatiable global demand for advanced electronic devices, which necessitates continuous innovation in chip manufacturing. As industries like artificial intelligence, 5G communication, and autonomous vehicles expand, the need for smaller, faster, and more power-efficient semiconductors intensifies, directly driving investments in state-of-the-art lithography tools. This demand is further amplified by the ongoing trend of digital transformation across various sectors, leading to increased data generation and processing requirements. The persistent push for miniaturization and higher integration density in integrated circuits demands increasingly precise and sophisticated patterning capabilities that only advanced lithography can provide.

Furthermore, significant geopolitical initiatives aimed at fostering domestic semiconductor manufacturing capabilities play a crucial role in stimulating market growth. Countries are investing heavily in establishing and expanding local foundries to reduce reliance on foreign supply chains, thereby creating new opportunities for lithography equipment suppliers. The rapid advancements in materials science and computational lithography also serve as key drivers, enabling the development of more effective photoresists and optical systems that push the boundaries of resolution. These factors collectively contribute to a robust growth environment, characterized by consistent capital expenditure from chip manufacturers striving to meet future technological requirements.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Advanced Semiconductors (AI, 5G, IoT, HPC) | +2.5-3.0% | Global (APAC, North America, Europe) | Short to Long-term (2025-2033) |

| Transition to Advanced Nodes (7nm, 5nm, 3nm) | +1.8-2.2% | Global (Taiwan, South Korea, USA, Europe) | Medium to Long-term (2026-2033) |

| Government Initiatives & Strategic Investments in Local Fabs | +1.5-2.0% | USA, Europe, China, Japan, India | Medium to Long-term (2026-2033) |

| Increased Adoption of EUV Lithography | +1.0-1.5% | Global (Leading-edge Foundries) | Medium to Long-term (2025-2033) |

| Growth in Advanced Packaging Technologies | +0.8-1.2% | APAC, North America | Short to Medium-term (2025-2030) |

Semiconductor Lithography Equipment Market Restraints Analysis

Despite robust growth, the semiconductor lithography equipment market faces significant restraints that can impede its expansion and increase operational complexities. The exceptionally high cost associated with acquiring and maintaining state-of-the-art lithography equipment, particularly EUV systems, represents a major barrier. These systems require substantial capital investment, which can be prohibitive for smaller companies and even strain the budgets of large semiconductor manufacturers, leading to delayed upgrades or limited adoption of advanced technologies. Furthermore, the immense complexity of these machines necessitates highly specialized infrastructure, including ultra-clean environments and advanced power management systems, adding to the overall cost of ownership and operational overhead.

Another crucial restraint is the inherent technological complexity and the extended research and development cycles required for new lithography generations. Developing next-generation tools involves overcoming fundamental physics challenges and requires close collaboration across a highly specialized ecosystem, from optical component manufacturers to photoresist developers. This long development timeline can make it difficult for equipment manufacturers to respond swiftly to rapidly evolving market demands and technological shifts. Additionally, the limited number of key suppliers for critical components and complete lithography systems creates potential bottlenecks in the supply chain, posing risks to timely equipment delivery and global market stability, especially in the face of geopolitical tensions or unforeseen disruptions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Equipment & R&D (EUV systems) | -1.5% to -2.0% | Global | Long-term (2025-2033) |

| Technological Complexity & Long Development Cycles | -1.0% to -1.5% | Global | Medium to Long-term (2026-2033) |

| Stringent Environmental & Safety Regulations | -0.5% to -0.8% | Europe, North America, Japan | Short to Long-term (2025-2033) |

| Skilled Labor Shortage for Operation & Maintenance | -0.4% to -0.7% | Global | Short to Medium-term (2025-2030) |

| Geopolitical Tensions & Export Controls | -0.8% to -1.2% | China, USA, Europe | Short to Medium-term (2025-2030) |

Semiconductor Lithography Equipment Market Opportunities Analysis

The semiconductor lithography equipment market is ripe with opportunities driven by several emerging technological advancements and evolving market demands. The increasing adoption of EUV lithography, though currently expensive, presents a significant long-term opportunity for manufacturers who can successfully scale and refine this technology. As the industry pushes towards sub-3nm nodes, the indispensable nature of EUV ensures sustained demand and continuous investment in its ecosystem, including next-generation sources, optics, and resist materials. Furthermore, the expansion of advanced packaging techniques, such as 3D stacking and chiplets, opens up new avenues for lithography equipment tailored to these specific requirements, moving beyond traditional wafer processing.

Beyond core technological advancements, the global push for digitalization and the growth of new application areas represent substantial opportunities. The proliferation of IoT devices, the rollout of 5G networks, and the burgeoning demand for edge AI capabilities all require a vast array of new semiconductor components, many of which necessitate high-precision lithography. Additionally, the development of computational lithography solutions, coupled with AI and machine learning, offers opportunities for optimizing existing DUV and EUV systems, extending their lifespan, and improving their performance. The market also stands to benefit from strategic partnerships and collaborations that facilitate joint research and development, accelerating the pace of innovation and fostering a more robust, integrated supply chain capable of addressing future challenges.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Continued Investment in Next-Gen EUV (High-NA EUV) | +2.0-2.5% | Global (Leading-edge Foundries) | Medium to Long-term (2027-2033) |

| Expansion into Advanced Packaging & Heterogeneous Integration | +1.5-1.8% | APAC, North America | Short to Long-term (2025-2033) |

| Growth in Specialty Devices (MEMS, Photonics, Power Semiconductors) | +1.0-1.3% | Europe, Japan, North America | Medium-term (2026-2031) |

| Emergence of New Market Verticals (Quantum Computing, Neuromorphic Chips) | +0.7-1.0% | Global | Long-term (2029-2033) |

| Development of Advanced Materials and Processes (Resists, Masks) | +0.6-0.9% | Global (Material Science Hubs) | Short to Medium-term (2025-2030) |

Semiconductor Lithography Equipment Market Challenges Impact Analysis

The semiconductor lithography equipment market faces multifaceted challenges that demand sophisticated solutions and strategic foresight. The relentless pursuit of Moore's Law, pushing feature sizes ever smaller, introduces significant technical hurdles related to pattern fidelity, overlay control, and defectivity. Achieving these advanced parameters requires extraordinary precision and control at every step of the lithography process, pushing the limits of current technological capabilities. Furthermore, the escalating costs associated with R&D, manufacturing, and operating next-generation lithography tools pose a substantial financial challenge, potentially limiting the adoption rates for some manufacturers and increasing the overall capital expenditure required for chip production. These financial pressures are compounded by the need for continuous investment in a highly specialized and expensive infrastructure.

Beyond the technical and economic complexities, the market is also vulnerable to supply chain disruptions and geopolitical instabilities. The highly concentrated nature of the lithography equipment supply chain, with a few dominant players, means that any disruption, whether from natural disasters, trade disputes, or component shortages, can have widespread repercussions across the global semiconductor industry. Maintaining a skilled workforce capable of designing, manufacturing, and servicing these highly advanced machines is another critical challenge, as the specific expertise required is scarce and in high demand. Addressing these challenges effectively will be crucial for sustaining market growth and ensuring the continuous advancement of semiconductor technology.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Extreme Technical Complexity of Sub-3nm Nodes (Patterning, Defectivity) | -1.2% to -1.8% | Global (Leading-edge Foundries) | Long-term (2027-2033) |

| High Operating Costs & Infrastructure Requirements | -0.8% to -1.2% | Global | Long-term (2025-2033) |

| Concentrated Supply Chain & Geopolitical Risks | -0.7% to -1.0% | Global | Short to Medium-term (2025-2030) |

| Talent Shortage in Highly Specialized Fields | -0.5% to -0.8% | Global | Short to Medium-term (2025-2030) |

| Rapid Technological Obsolescence | -0.6% to -0.9% | Global | Short to Medium-term (2025-2030) |

Semiconductor Lithography Equipment Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Semiconductor Lithography Equipment Market, covering historical data, current market dynamics, and future projections. It delivers critical insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The scope encompasses detailed segmentation by equipment type, technology, application, end-user, and wafer size, offering a granular view of market trends and competitive landscapes. The report is designed to assist stakeholders in making informed strategic decisions, identifying lucrative investment avenues, and understanding the technological shifts shaping the industry's future. It also features a comprehensive profile of leading market players, alongside an examination of the impact of emerging technologies like AI on market evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 32.9 Billion |

| Growth Rate | 7.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASML, Nikon, Canon, KLA Corporation, Applied Materials, Lam Research, Tokyo Electron (TEL), Carl Zeiss SMT, JSR Corporation, Shin-Etsu Chemical, SCREEN Holdings, EV Group (EVG), Suss MicroTec, JEOL Ltd., Orbotech (a KLA Company), Veeco Instruments, Ultratech (a Veeco Company), Plasma-Therm, Riber, Samco Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Lithography Equipment Market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates a detailed analysis of market trends, technological adoption rates, and investment patterns across different product categories, end-user applications, and geographical regions. By breaking down the market into these specific segments, stakeholders can identify niche opportunities, assess competitive landscapes more effectively, and tailor their strategies to target specific growth areas. The interplay between these segments is crucial for comprehending the overall market structure and predicting future shifts in demand and supply.

The segmentation strategy takes into account critical factors such as the type of lithography equipment used, the underlying technology, the specific applications in semiconductor manufacturing, the primary end-users, and the prevailing wafer sizes. This comprehensive approach ensures that all significant facets of the market are covered, from cutting-edge EUV systems driving advanced node fabrication to more established DUV and I-line technologies still essential for various device types. Understanding these segments is vital for anyone seeking to navigate the complexities of this highly technical and capital-intensive industry, offering clarity on where current and future growth resides.

- By Equipment Type: EUV Lithography Systems, DUV Lithography Systems (ArF Immersion, ArF Dry, KrF), I-line Lithography Systems, G-line Lithography Systems.

- By Technology: Steppers, Scanners, Mask Aligners.

- By Application: Memory Manufacturing (DRAM, NAND), Foundry Services, Logic & Microprocessors, MEMS & NEMS, Advanced Packaging, Power Devices.

- By End-User: Integrated Device Manufacturers (IDMs), Foundries, OSATs (Outsourced Semiconductor Assembly and Test), Research & Development Institutions.

- By Wafer Size: 200mm Wafer, 300mm Wafer, 450mm Wafer.

Regional Highlights

- Asia Pacific (APAC): Dominates the global semiconductor lithography equipment market, primarily driven by the presence of major foundries and IDMs in countries like Taiwan, South Korea, China, and Japan. Massive investments in new fabrication plants and the expansion of existing facilities to meet the rising global demand for semiconductors significantly bolster market growth in this region. Government support for domestic chip production, especially in China, further accelerates market development.

- North America: Represents a significant market share due to substantial R&D investments, the presence of leading semiconductor device manufacturers, and a strong focus on advanced technology nodes. Initiatives to reshore semiconductor manufacturing and bolster supply chain resilience contribute to increased capital expenditure on lithography equipment. The region is a hub for innovation in AI, high-performance computing, and aerospace, driving demand for cutting-edge chips.

- Europe: Exhibits steady growth, fueled by strong government and private sector initiatives aimed at strengthening the regional semiconductor ecosystem. Countries like the Netherlands (home to a major lithography equipment vendor) and Germany are key players in research and manufacturing. Investments in automotive electronics, industrial IoT, and specialized semiconductor applications are significant drivers.

- Latin America: While a smaller market, it shows nascent growth potential, particularly in areas like advanced packaging and assembly operations. Increasing government focus on developing local tech infrastructure and attracting foreign investment could stimulate future demand.

- Middle East and Africa (MEA): Currently a niche market, but with growing interest in digital transformation and technological infrastructure development. Emerging economies in the region are exploring opportunities in semiconductor manufacturing and design, which could lead to gradual investments in lithography equipment in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Lithography Equipment Market.- ASML

- Nikon

- Canon

- KLA Corporation

- Applied Materials

- Lam Research

- Tokyo Electron (TEL)

- Carl Zeiss SMT

- JSR Corporation

- Shin-Etsu Chemical

- SCREEN Holdings

- EV Group (EVG)

- Suss MicroTec

- JEOL Ltd.

- Orbotech (a KLA Company)

- Veeco Instruments

- Ultratech (a Veeco Company)

- Plasma-Therm

- Riber

- Samco Inc.

Frequently Asked Questions

Analyze common user questions about the Semiconductor Lithography Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is semiconductor lithography equipment?

Semiconductor lithography equipment refers to advanced tools used in the manufacturing of integrated circuits (ICs) to create intricate patterns on semiconductor wafers. These patterns define the electrical circuits and components of a chip, utilizing light to transfer a design from a photomask onto a photoresist-coated wafer, a critical step in miniaturization.

What drives the growth of the semiconductor lithography equipment market?

The market's growth is primarily driven by the increasing global demand for advanced semiconductors in applications like AI, 5G, IoT, and high-performance computing, coupled with the continuous pursuit of smaller, more powerful, and energy-efficient electronic devices. Government initiatives to establish regional semiconductor manufacturing hubs also significantly contribute to market expansion.

What role does EUV lithography play in the market?

Extreme Ultraviolet (EUV) lithography is a pivotal technology in the market, enabling the manufacturing of advanced semiconductor nodes (7nm and below). Its ability to create finer patterns with higher precision makes it indispensable for next-generation chips, driving substantial investments and defining the future trajectory of high-volume, leading-edge chip production.

What are the main challenges faced by the semiconductor lithography equipment market?

Key challenges include the extremely high cost of advanced equipment and R&D, the inherent technological complexity of sub-3nm patterning, the highly concentrated global supply chain with associated geopolitical risks, and a persistent shortage of highly specialized talent required for operation and maintenance.

How is AI impacting semiconductor lithography equipment?

AI is transforming lithography by enabling enhanced predictive maintenance for equipment, optimizing complex process controls for improved pattern fidelity and yield, accelerating defect detection and classification, and assisting in automated recipe generation. This integration leads to greater efficiency, precision, and cost reduction in semiconductor manufacturing.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted