Semiconductor Bare Die Market

Semiconductor Bare Die Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709373 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

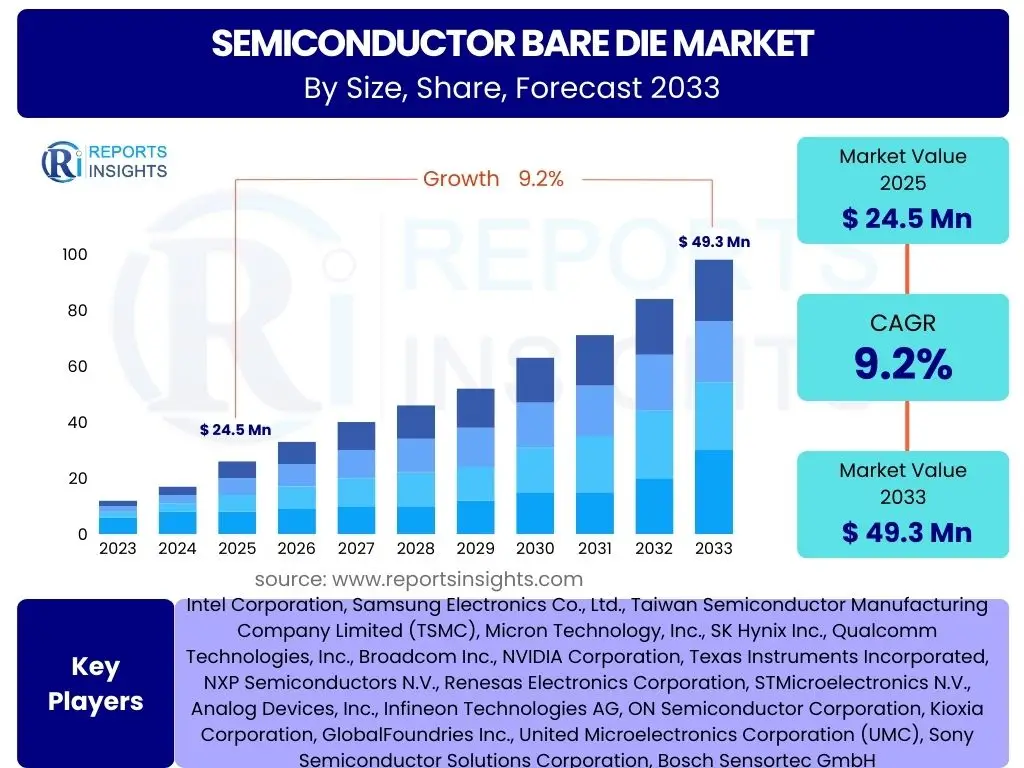

Semiconductor Bare Die Market Size

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Bare Die Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033. The market is estimated at USD 24.5 Billion in 2025 and is projected to reach USD 49.3 Billion by the end of the forecast period in 2033.

Key Semiconductor Bare Die Market Trends & Insights

User queries regarding the semiconductor bare die market frequently center on evolving technological landscapes, the impact of global supply chain dynamics, and shifts in application demand. A primary area of interest involves the push towards miniaturization and higher performance, which inherently favors bare die solutions for compact, high-density electronic systems. Furthermore, the increasing complexity of advanced packaging technologies is driving demand for bare die to enable heterogeneous integration and system-in-package (SiP) solutions, moving beyond traditional chip-on-board assemblies.

Another significant trend revolves around the expanding adoption of bare die in critical growth sectors such as automotive electronics, artificial intelligence (AI) hardware, and 5G infrastructure. These applications demand high levels of reliability, power efficiency, and thermal management, which bare die configurations can effectively address by minimizing parasitic effects and improving overall system performance. The market is also witnessing a trend towards greater customization and specialized bare die designs, moving away from commoditized components to tailored solutions that meet specific application requirements for diverse industries.

- Escalating demand for miniaturized and high-performance electronic devices across consumer and industrial sectors.

- Proliferation of advanced packaging technologies like 3D ICs, SiP, and chiplets, necessitating bare die for heterogeneous integration.

- Rapid growth in automotive electronics, including ADAS and in-vehicle infotainment, boosting bare die adoption.

- Expansion of Artificial Intelligence (AI) and Machine Learning (ML) applications, driving demand for specialized bare die for accelerators and processors.

- Deployment of 5G infrastructure and related communication equipment requiring high-frequency, low-power bare die components.

- Focus on supply chain resilience and regional manufacturing capabilities influencing sourcing strategies for bare die.

- Increased investment in IoT devices and edge computing, where compact bare die solutions are critical for form factor and power efficiency.

- Emergence of specialized bare die for high-reliability applications in aerospace and defense.

AI Impact Analysis on Semiconductor Bare Die

Common user questions regarding AI's impact on semiconductor bare die highlight its role as both a demand driver and a technological enabler. Users are keen to understand how the proliferation of AI and machine learning workloads, from data centers to edge devices, is directly influencing the design, production, and demand for specific bare die types. The immense computational power required for AI training and inference necessitates highly optimized processors, memory, and specialized accelerators, all of which are increasingly implemented using bare die configurations to achieve desired performance, power efficiency, and compact footprints.

Beyond demand, there's significant interest in how AI technologies themselves are being utilized within the bare die manufacturing process. This includes AI-driven process optimization, predictive maintenance for semiconductor equipment, and AI-enhanced quality control and inspection systems for bare die. The ability of AI to analyze vast datasets can lead to improved yield rates, reduced defects, and faster development cycles for new bare die designs. Furthermore, AI is fostering innovation in advanced packaging, enabling more complex and efficient integration of multiple bare die into sophisticated modules.

- Demand Driver: AI's computational requirements fuel significant demand for high-performance processor, memory, and accelerator bare die (e.g., GPUs, NPUs, HBM).

- Advanced Packaging Enabler: AI workloads drive the adoption of 2.5D and 3D bare die stacking, chiplets, and heterogeneous integration for optimized performance and power.

- Edge AI Growth: Miniaturization requirements for edge AI devices (IoT, wearables, automotive) heavily rely on compact bare die solutions.

- Design & Manufacturing Optimization: AI-powered tools assist in bare die design, simulation, and manufacturing process optimization, improving yields and efficiency.

- Data Center Expansion: AI applications in data centers necessitate large volumes of high-density bare die for servers and networking equipment.

- Increased Complexity: AI models demand more complex and specialized bare die architectures, pushing innovation in material science and interconnect technology.

- Market Segmentation: AI's varied applications lead to specialized bare die development for specific use cases (e.g., inference chips, training chips, vision processing units).

Key Takeaways Semiconductor Bare Die Market Size & Forecast

User inquiries about key takeaways from the semiconductor bare die market size and forecast often focus on understanding the primary growth catalysts, the sustainability of current expansion rates, and the strategic implications for industry stakeholders. A central insight is the market's robust growth trajectory, driven by an insatiable demand for advanced electronics across diverse sectors. This expansion is not merely incremental but represents a fundamental shift towards higher integration and specialized functionalities that bare die inherently enable, particularly for high-performance computing, AI, and next-generation communication technologies.

Another crucial takeaway is the intertwined relationship between bare die market growth and broader technological advancements, specifically in advanced packaging and heterogeneous integration. The forecast indicates that as electronic systems become more complex and miniaturized, the reliance on bare die will intensify, making it a cornerstone for future innovation. Furthermore, the market's resilience despite geopolitical and supply chain fluctuations underscores its strategic importance, compelling manufacturers to invest in expanding capacity, diversifying supply chains, and innovating in bare die technology to meet the escalating global demand.

- The Semiconductor Bare Die Market exhibits strong growth potential, projected to nearly double in value by 2033.

- Technological advancements in AI, 5G, and automotive electronics are primary accelerators for market expansion.

- Advanced packaging solutions are increasingly reliant on bare die, driving integration and performance improvements.

- The market's resilience is supported by increasing investments in manufacturing capacity and diversified supply chains.

- Miniaturization and higher power efficiency requirements across end-use industries bolster demand for bare die.

- Strategic partnerships and collaborations within the semiconductor ecosystem are crucial for innovation and market penetration.

- The APAC region is anticipated to remain a dominant force in both production and consumption of bare die.

Semiconductor Bare Die Market Drivers Analysis

The semiconductor bare die market is propelled by a confluence of technological advancements and expanding application landscapes. The relentless pursuit of miniaturization in electronic devices, coupled with the demand for higher performance and lower power consumption, makes bare die an indispensable component. As conventional silicon die face physical limits, bare die enables more efficient space utilization and facilitates advanced packaging techniques, such as 3D stacking and chiplets, which are crucial for next-generation products. This drive is particularly evident in consumer electronics, where devices are becoming smaller yet more powerful.

Furthermore, the burgeoning demand from key growth sectors like automotive, artificial intelligence, and 5G telecommunications acts as a significant market driver. Automotive electronics, including advanced driver-assistance systems (ADAS) and electric vehicles (EVs), require highly reliable, high-performance semiconductors in compact form factors, often best achieved with bare die. Similarly, the computational intensity of AI and the high-frequency requirements of 5G infrastructure necessitate specialized bare die for processors, memory, and RF components. These sectors demand robust and efficient solutions, creating a sustained upward trajectory for bare die adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Miniaturization & High Performance | +2.5% | Global, particularly APAC, North America | 2025-2033 (Long-term) |

| Expansion of Advanced Packaging Technologies | +2.0% | Global, especially East Asia (Taiwan, South Korea) | 2025-2033 (Long-term) |

| Rising Adoption in Automotive Electronics | +1.8% | Europe, North America, Japan, China | 2025-2033 (Mid to Long-term) |

| Proliferation of Artificial Intelligence (AI) and 5G | +2.2% | Global, particularly North America, China, Europe | 2025-2033 (Mid to Long-term) |

| Increasing IoT and Edge Computing Device Production | +1.5% | Global, with strong growth in emerging markets | 2025-2033 (Mid to Long-term) |

Semiconductor Bare Die Market Restraints Analysis

Despite robust growth, the semiconductor bare die market faces several significant restraints that could temper its expansion. One primary challenge is the escalating complexity and cost associated with advanced bare die manufacturing processes. Producing bare die with shrinking geometries and increasing functionality requires substantial capital investment in highly sophisticated fabrication equipment, cleanroom facilities, and advanced materials. This high barrier to entry limits the number of players and increases the overall cost, which can impact profitability and the accessibility of bare die for certain applications, especially for smaller market participants.

Furthermore, the inherent challenges in handling, testing, and integrating bare die present a considerable restraint. Bare die are delicate and require specialized handling equipment and expertise to prevent physical damage or contamination. The absence of traditional packaging makes testing more intricate and time-consuming, as bare die must often be integrated into an interposer or temporary carrier for functional verification. These complexities contribute to higher manufacturing overheads and longer development cycles, posing a challenge for widespread adoption, particularly for companies without extensive experience in bare die integration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing & R&D Costs | -1.2% | Global, affects all regions | 2025-2033 (Long-term) |

| Complexity in Handling & Testing Bare Die | -0.8% | Global, particularly new entrants | 2025-2033 (Long-term) |

| Supply Chain Vulnerabilities & Geopolitical Tensions | -1.5% | Global, especially East Asia, North America, Europe | 2025-2028 (Short to Mid-term) |

| Intellectual Property and Design Security Concerns | -0.5% | Global, with emphasis on IP-heavy regions | 2025-2033 (Long-term) |

| Skilled Workforce Shortage | -0.7% | Global, particularly North America, Europe | 2025-2033 (Long-term) |

Semiconductor Bare Die Market Opportunities Analysis

The semiconductor bare die market is ripe with opportunities driven by emerging technologies and expanding applications. One significant area of opportunity lies in the continued innovation within advanced packaging techniques. As chip designers push for higher integration densities and specialized functionalities, the demand for bare die that can be seamlessly incorporated into 2.5D and 3D stacking, chiplets, and fan-out wafer-level packaging (FOWLP) will intensify. This trend allows for the creation of heterogeneous systems that combine different types of bare die, such as logic, memory, and analog, into a single, high-performance module, opening new avenues for product development and differentiation.

Furthermore, the rapid growth of niche and specialized markets presents substantial opportunities. Areas like quantum computing, medical implants, and high-reliability aerospace components require custom bare die solutions with stringent performance and form factor requirements. The shift towards edge computing and pervasive IoT devices, which demand ultra-compact and power-efficient designs, also creates a fertile ground for bare die innovation. Companies that can develop tailored bare die solutions for these high-value, low-volume applications, or offer flexible integration services, stand to gain significant market share and establish strong competitive positions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Further Advancements in Advanced Packaging Technologies | +1.5% | Global, particularly APAC (Taiwan, South Korea) | 2025-2033 (Long-term) |

| Emerging Applications in Quantum Computing & Medical Devices | +1.0% | North America, Europe, Japan | 2027-2033 (Mid to Long-term) |

| Growth in High-Performance Computing (HPC) & Data Centers | +1.2% | North America, Europe, China | 2025-2033 (Long-term) |

| Expansion into New Geographic Markets | +0.8% | Southeast Asia, India, Latin America | 2026-2033 (Mid to Long-term) |

| Customization & Niche Bare Die Solutions for Specialized Industries | +0.9% | Global, driven by specific industrial needs | 2025-2033 (Long-term) |

Semiconductor Bare Die Market Challenges Impact Analysis

The semiconductor bare die market faces several formidable challenges that could impede its growth and stability. A significant hurdle is the persistent geopolitical instability and trade tensions that can disrupt global supply chains. The highly globalized nature of semiconductor manufacturing means that political conflicts, trade disputes, or even natural disasters in key regions can severely impact the availability of raw materials, manufacturing capacity, and distribution channels for bare die. This volatility necessitates strategic diversification and localization efforts, which can be costly and time-consuming for manufacturers.

Another critical challenge is the escalating cost of developing and maintaining cutting-edge fabrication facilities. As semiconductor technology progresses to smaller nodes and more complex designs, the capital expenditure required for new fabs, research and development, and advanced tooling reaches unprecedented levels. This high investment barrier, coupled with the rapid pace of technological obsolescence, puts immense pressure on manufacturers to achieve high utilization rates and quick returns on investment. Furthermore, the semiconductor industry faces a severe shortage of skilled talent, from design engineers to process technicians, which threatens to slow innovation and production capabilities across the bare die ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Instability & Supply Chain Disruptions | -1.0% | Global, particularly East Asia, North America | 2025-2030 (Short to Mid-term) |

| High Capital Expenditure for Advanced Fabs | -0.9% | Global, impacts major semiconductor manufacturing regions | 2025-2033 (Long-term) |

| Technological Obsolescence & Rapid Innovation Cycles | -0.6% | Global, especially leading technology hubs | 2025-2033 (Long-term) |

| Environmental Regulations & Sustainability Pressures | -0.4% | Europe, North America, Japan | 2026-2033 (Mid to Long-term) |

| Talent Shortage & Retention | -0.7% | Global, particularly in advanced research and manufacturing | 2025-2033 (Long-term) |

Semiconductor Bare Die Market - Updated Report Scope

This comprehensive market report provides a detailed analysis of the global semiconductor bare die market, offering in-depth insights into its size, growth trends, and future projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges influencing the industry landscape. It segments the market by various parameters, including product type, application, end-use industry, and geography, to provide a granular understanding of market dynamics and competitive positioning.

The report also features a competitive analysis of key players, highlighting their strategies, product portfolios, and market presence. Utilizing a robust research methodology, it delivers actionable intelligence crucial for strategic decision-making, investment planning, and market entry strategies for stakeholders across the semiconductor value chain. The forecast period extends to 2033, offering a long-term perspective on market evolution and potential growth avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 24.5 Billion |

| Market Forecast in 2033 | USD 49.3 Billion |

| Growth Rate | 9.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, Samsung Electronics Co., Ltd., Taiwan Semiconductor Manufacturing Company Limited (TSMC), Micron Technology, Inc., SK Hynix Inc., Qualcomm Technologies, Inc., Broadcom Inc., NVIDIA Corporation, Texas Instruments Incorporated, NXP Semiconductors N.V., Renesas Electronics Corporation, STMicroelectronics N.V., Analog Devices, Inc., Infineon Technologies AG, ON Semiconductor Corporation, Kioxia Corporation, GlobalFoundries Inc., United Microelectronics Corporation (UMC), Sony Semiconductor Solutions Corporation, Bosch Sensortec GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The semiconductor bare die market is meticulously segmented to provide a comprehensive view of its intricate dynamics and diverse applications. This granular analysis allows for a clearer understanding of how different product types, technologies, and end-use industries contribute to the overall market growth and evolution. By dissecting the market into distinct categories, stakeholders can identify high-growth areas, emerging technological preferences, and specific market niches that offer significant investment and development opportunities.

The segmentation by type, for instance, distinguishes between logic, memory, analog, and power management bare die, each driven by unique demand characteristics. Furthermore, technology-based segmentation highlights the adoption rates of various material compositions and fabrication processes. The application and end-use industry breakdowns illustrate how bare die are integral to sectors ranging from consumer electronics to highly specialized defense systems, underscoring the pervasive nature and critical importance of bare die in modern electronic systems. This detailed segmentation is crucial for strategic planning and targeted market approaches.

- By Type: Logic Bare Die, Memory Bare Die (DRAM, NAND, SRAM), Analog Bare Die, Mixed-Signal Bare Die, Optoelectronics Bare Die, Power Management Bare Die, Microcontroller Bare Die, Sensor Bare Die

- By Technology: CMOS, BiCMOS, SiGe, GaN, SiC, Others

- By Wafer Size: 8-inch, 12-inch, 6-inch and below, 18-inch and above

- By Application: Consumer Electronics (Smartphones, Tablets, Wearables, Laptops, IoT Devices), Automotive (ADAS, Infotainment, Powertrain, Body Electronics), Industrial (Automation, Robotics, Smart Factories), Healthcare (Medical Implants, Diagnostic Equipment), Telecommunications (5G Infrastructure, Base Stations), Data Centers (Servers, Storage, Networking), Defense & Aerospace

- By End-Use Industry: Information & Communication Technology (ICT), Automotive, Industrial Automation, Healthcare, Consumer Electronics, Others

Regional Highlights

- Asia Pacific (APAC): Dominates the global bare die market due to the presence of major semiconductor foundries, packaging facilities, and a robust electronics manufacturing ecosystem, particularly in countries like Taiwan, South Korea, China, and Japan. Strong demand from consumer electronics, automotive, and telecommunications sectors further fuels growth.

- North America: A significant market driven by innovation in AI, high-performance computing, data centers, and advanced defense technologies. The region benefits from substantial R&D investments and the presence of leading fabless design companies and technology giants.

- Europe: Characterized by strong growth in automotive electronics, industrial automation, and specialized healthcare applications. Germany, France, and the Netherlands are key contributors, focusing on high-value, niche bare die solutions and advanced manufacturing.

- Latin America: An emerging market with growing potential, driven by increasing adoption of consumer electronics and expanding manufacturing bases, though still smaller in scale compared to other regions.

- Middle East & Africa (MEA): Showing nascent growth, primarily in telecommunications infrastructure and defense sectors, with increasing government investments in technology and industrialization efforts.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Bare Die Market.- Intel Corporation

- Samsung Electronics Co., Ltd.

- Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- Micron Technology, Inc.

- SK Hynix Inc.

- Qualcomm Technologies, Inc.

- Broadcom Inc.

- NVIDIA Corporation

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- Analog Devices, Inc.

- Infineon Technologies AG

- ON Semiconductor Corporation

- Kioxia Corporation

- GlobalFoundries Inc.

- United Microelectronics Corporation (UMC)

- Sony Semiconductor Solutions Corporation

- Bosch Sensortec GmbH

Frequently Asked Questions

What is a semiconductor bare die?

A semiconductor bare die is an unpackaged, individual integrated circuit (IC) or chip that has been cut from a semiconductor wafer. It consists of the functional circuitry without the protective casing, leads, or other packaging components, making it smaller and lighter for direct integration into advanced electronic systems.

Why is the demand for bare die increasing?

Demand for bare die is increasing primarily due to the ongoing trend towards miniaturization, the need for higher performance and power efficiency in electronic devices, and the proliferation of advanced packaging technologies like 3D stacking and chiplets, which require unpackaged chips for optimal integration and reduced form factor.

Which industries are the major consumers of semiconductor bare die?

Major consumers of semiconductor bare die include consumer electronics (smartphones, wearables), automotive (ADAS, EVs), industrial automation, telecommunications (5G infrastructure), data centers, and specialized applications in healthcare and defense, all requiring compact, high-performance integrated solutions.

How does AI impact the bare die market?

AI significantly impacts the bare die market by driving demand for high-performance bare die (e.g., GPUs, NPUs, HBM) to handle intensive computational workloads. Additionally, AI technologies are being integrated into manufacturing processes to optimize bare die design, testing, and yield rates, fostering efficiency and innovation.

What are the key challenges in the bare die market?

Key challenges in the bare die market include high manufacturing and R&D costs, the complexity of handling and testing delicate unpackaged chips, geopolitical instability and supply chain vulnerabilities, the rapid pace of technological obsolescence, and a shortage of skilled labor in the semiconductor industry.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted