Semiconductor Advanced Packaging Market

Semiconductor Advanced Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700092 | Last Updated : July 22, 2025 |

Format : ![]()

![]()

![]()

![]()

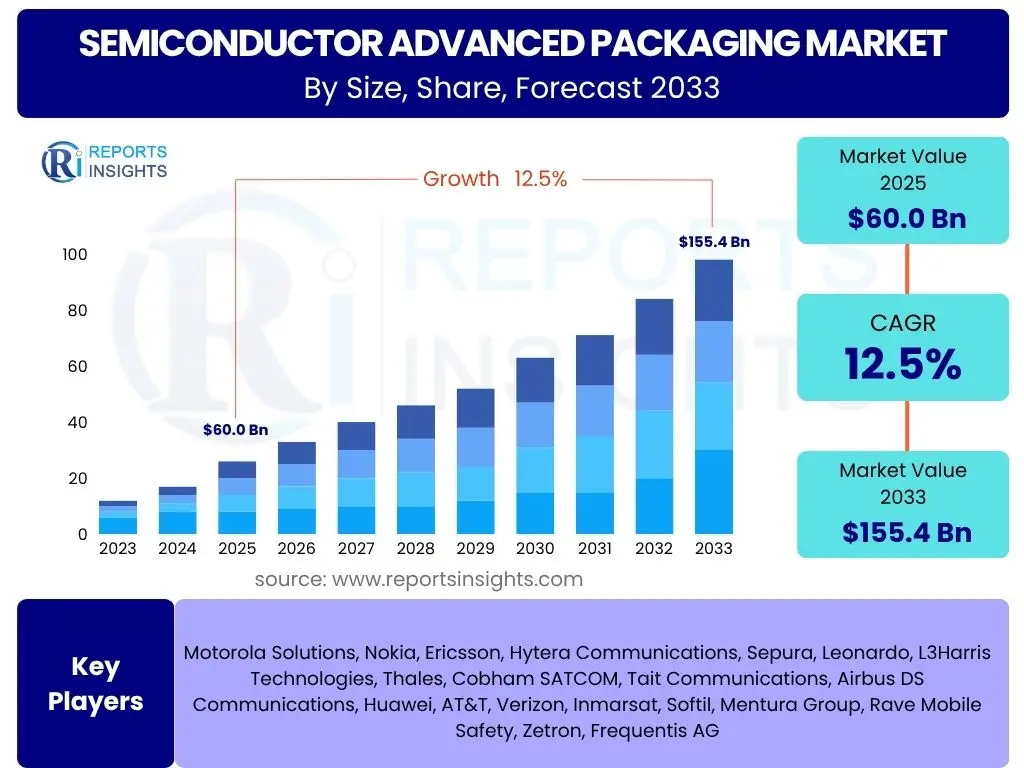

Semiconductor Advanced Packaging Market is projected to grow at a Compound annual growth rate (CAGR) of 12.5% between 2025 and 2033, reaching USD 60.0 billion in 2025 and is projected to grow to USD 155.4 billion by 2033, the end of the forecast period.

Key Semiconductor Advanced Packaging Market Trends & Insights

The semiconductor advanced packaging market is currently shaped by several transformative trends, driven by the escalating demand for high-performance, compact, and energy-efficient electronic devices. These trends highlight the industry's continuous evolution towards more sophisticated integration solutions. The increasing complexity of modern chip designs necessitates innovative packaging techniques that can facilitate greater functionality within smaller form factors, while also ensuring robust performance and thermal management.

Moreover, the strategic shift towards heterogeneous integration, where diverse functional blocks are combined into a single package, is fundamentally altering the landscape of semiconductor manufacturing. This approach enables the creation of highly specialized and optimized systems, moving beyond the traditional monolithic chip design. The widespread adoption of these advanced packaging methods is crucial for enabling the next generation of computing, communication, and automotive technologies, reflecting a broader industry push for enhanced capabilities and improved cost-efficiency.

- Miniaturization and higher integration density requirements are driving packaging innovations.

- Heterogeneous integration and chiplet architectures are gaining significant traction.

- Increasing demand for high-bandwidth memory (HBM) integration in HPC and AI.

- Development of advanced thermal management solutions for denser packages.

- Shift towards wafer-level packaging (WLP), especially Fan-Out Wafer-Level Packaging (FOWLP).

- Growing importance of co-design principles between chip and package.

AI Impact Analysis on Semiconductor Advanced Packaging

The advent and rapid proliferation of Artificial intelligence (AI) across various sectors have profoundly reshaped the demands placed on semiconductor advanced packaging. AI workloads, particularly in areas like deep learning, machine learning inference, and generative AI, require immense computational power, high-speed data transfer, and low latency. Traditional packaging methods often fall short in meeting these stringent requirements, making advanced packaging indispensable for optimizing AI hardware performance. This impact is evident in the push for novel interconnects and multi-die integration techniques that can support the high data throughput necessary for AI processing units (APUs) and graphics processing units (GPUs) designed for AI applications.

Furthermore, AI's influence extends beyond just the performance needs of the chips themselves. It also drives innovation in the packaging process, with AI and machine learning being leveraged for yield optimization, defect detection, and predictive maintenance in advanced packaging lines. This dual impact — driving the necessity for more capable packaging solutions and simultaneously enhancing the efficiency of their manufacturing — positions AI as a central catalyst for the future trajectory of the semiconductor advanced packaging market. The integration of high-bandwidth memory (HBM) within advanced packages, for instance, is a direct response to the memory bandwidth demands of large AI models, illustrating a clear symbiotic relationship between AI advancements and packaging technology evolution.

- Accelerated demand for high-bandwidth memory (HBM) integration for AI accelerators.

- Increased complexity and necessity for multi-die and heterogeneous integration for AI chips.

- Requirement for ultra-low latency and high-speed interconnections to support AI workloads.

- AI-driven optimization of packaging processes, including yield enhancement and quality control.

- Development of specialized packaging solutions for edge AI and quantum computing applications.

Key Takeaways Semiconductor Advanced Packaging Market Size & Forecast

- The global Semiconductor Advanced Packaging Market is projected to achieve significant growth, reaching USD 155.4 billion by 2033.

- The market is expected to expand at a robust Compound Annual Growth Rate (CAGR) of 12.5% during the forecast period from 2025 to 2033.

- Starting from an estimated market size of USD 60.0 billion in 2025, the market demonstrates strong upward trajectory.

- Key drivers for this growth include the escalating demand from high-performance computing, AI, automotive, and 5G sectors.

- Miniaturization and increased functional integration in consumer electronics are significant contributors to market expansion.

- Asia Pacific is anticipated to remain the dominant region in terms of both manufacturing and consumption.

- Innovations in 2.5D/3D packaging, fan-out wafer-level packaging, and hybrid bonding technologies will fuel future growth.

Semiconductor Advanced Packaging Market Drivers Analysis

The semiconductor advanced packaging market is propelled by a confluence of powerful drivers, each contributing significantly to its accelerated growth. The relentless pursuit of higher performance, greater energy efficiency, and smaller form factors across various electronic devices is at the core of this demand. As traditional scaling limits of silicon chips become more challenging, advanced packaging offers a critical pathway to continue enhancing semiconductor capabilities without relying solely on transistor density improvements. This shift underscores a fundamental evolution in semiconductor manufacturing strategy, where packaging is no longer just a protective enclosure but an integral part of chip design and system optimization.

Furthermore, the emergence of transformative technologies such as artificial intelligence, 5G connectivity, and autonomous driving is creating unprecedented demands for highly integrated and sophisticated semiconductor solutions. These applications require immense processing power, high bandwidth, and robust reliability, which can only be achieved through advanced packaging techniques like 2.5D/3D integration, chiplet architectures, and wafer-level packaging. The ability of advanced packaging to enable heterogeneous integration — combining different types of chips (e.g., logic, memory, sensors) into a single package — is also a key driver, allowing for the creation of customized, high-performance systems that are optimized for specific applications. These factors collectively highlight the indispensable role of advanced packaging in enabling the next generation of electronic innovation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Explosive Growth of AI/ML and High-Performance Computing (HPC) | +4.0% | North America, Asia Pacific (China, Taiwan, South Korea) | Short-term to Long-term |

| Miniaturization and Increasing Functionality in Consumer Electronics | +3.5% | Asia Pacific (China, South Korea, Japan), Europe, North America | Short-term to Mid-term |

| Rise of 5G and IoT Connectivity | +2.5% | Asia Pacific, North America, Europe | Mid-term to Long-term |

| Automotive Industry's Shift to Electrification and Autonomous Driving | +1.5% | Europe (Germany), North America, Asia Pacific (Japan, South Korea, China) | Mid-term to Long-term |

| Cost Efficiency and Yield Improvement through Chiplet Architectures | +1.0% | Global, particularly major semiconductor manufacturing hubs | Mid-term to Long-term |

Semiconductor Advanced Packaging Market Restraints Analysis

Despite the robust growth trajectory of the semiconductor advanced packaging market, several significant restraints pose challenges to its unbridled expansion. One of the primary barriers is the inherently high cost associated with the research, development, and manufacturing of advanced packaging technologies. The necessity for specialized equipment, high-precision processes, and often exotic materials escalates the overall capital expenditure, making it a considerable hurdle for smaller companies and potentially increasing the final product cost for consumers. This cost sensitivity can sometimes limit the widespread adoption of the most cutting-edge packaging solutions, especially in price-competitive market segments.

Furthermore, the complexity of design and manufacturing processes represents another critical restraint. Advanced packaging involves intricate multi-layer structures, precise alignment requirements, and novel integration techniques that demand highly specialized expertise and sophisticated fabrication capabilities. This complexity not only extends design cycles and time-to-market but also increases the potential for manufacturing defects, impacting yields and overall production efficiency. Additionally, the challenges related to effective thermal management in increasingly dense packages, coupled with a highly interdependent global supply chain susceptible to geopolitical instabilities and material shortages, further constrain the market. These factors collectively require continuous innovation and strategic mitigation efforts to sustain the market's growth momentum.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development and Manufacturing Costs | -2.0% | Global, particularly emerging economies | Short-term to Long-term |

| Complex Design and Manufacturing Processes | -1.5% | Global, impacting R&D and production hubs | Short-term to Mid-term |

| Thermal Management Challenges in Highly Integrated Packages | -1.0% | Global, especially for HPC and AI applications | Mid-term to Long-term |

| Supply Chain Dependencies and Geopolitical Tensions | -0.8% | Global, with emphasis on Asia Pacific and North America | Short-term to Mid-term |

| Lack of Industry-Wide Standardization for New Technologies | -0.7% | Global, affecting multi-vendor ecosystems | Mid-term to Long-term |

Semiconductor Advanced Packaging Market Opportunities Analysis

The semiconductor advanced packaging market is poised for significant expansion, driven by a myriad of emerging opportunities that promise to redefine its scope and impact. The relentless pursuit of innovative device architectures, such as quantum computing and advanced edge AI systems, presents entirely new avenues for highly specialized and complex packaging solutions. These nascent fields will demand unprecedented levels of integration, ultra-low latency, and extreme environmental resilience, pushing the boundaries of current packaging capabilities and spurring significant R&D investments. Such developments create a fertile ground for breakthroughs in material science, interconnection techniques, and overall package design.

Furthermore, technological advancements within the packaging industry itself, particularly the development and maturation of technologies like hybrid bonding, are opening doors to higher integration densities and improved performance. Hybrid bonding offers the potential for ultra-fine pitch interconnections and stronger mechanical bonds, enabling truly monolithic-like performance from stacked dies. Beyond core technology, the increasing focus on localized manufacturing and governmental incentives aimed at strengthening domestic semiconductor supply chains also represents a substantial opportunity. These initiatives are fostering investments in new fabrication facilities and R&D centers globally, creating a more diversified and resilient advanced packaging ecosystem. These combined factors underscore a vibrant future for innovation and growth in the semiconductor advanced packaging domain.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Quantum Computing and Advanced Edge AI | +2.5% | North America, Europe, Asia Pacific (Japan, South Korea) | Long-term |

| Development and Adoption of Hybrid Bonding Technologies | +2.0% | Asia Pacific (Taiwan, South Korea, Japan), North America | Mid-term to Long-term |

| Growth in Advanced Packaging Equipment and Material Market | +1.5% | Global, especially equipment manufacturing hubs | Short-term to Mid-term |

| Increased Focus on System-in-Package (SiP) Solutions for IoT and Wearables | +1.0% | Asia Pacific, North America, Europe | Short-term to Mid-term |

| Regionalization and Government Incentives for Domestic Manufacturing | +0.8% | North America, Europe, Southeast Asia | Mid-term to Long-term |

Semiconductor Advanced Packaging Market Challenges Impact Analysis

The semiconductor advanced packaging market, while experiencing robust growth, is not without its significant challenges that could impede its full potential. One of the most critical hurdles lies in the scalability of advanced packaging technologies from research and development phases to high-volume, cost-effective manufacturing. Translating innovative lab processes into repeatable, mass-producible solutions often faces issues related to yield, throughput consistency, and stringent process control requirements. This transition demands substantial investment in automation and quality assurance systems, which can be difficult to justify for specialized, low-volume applications.

Moreover, the highly specialized nature of advanced packaging creates a profound workforce skill gap. The integration of diverse disciplines, ranging from materials science and precision engineering to complex thermal and electrical design, requires a multidisciplinary talent pool that is currently in short supply. Attracting, training, and retaining such highly skilled professionals is a continuous challenge for the industry. Furthermore, as packaging becomes more intricate and components are densely integrated, ensuring long-term reliability and thermal stability under various operational conditions becomes increasingly complex. Addressing these challenges through collaborative efforts, strategic investments in talent development, and robust R&D will be crucial for the sustained growth and innovation within the semiconductor advanced packaging market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scalability Issues for High-Volume Manufacturing | -1.8% | Global, especially for new packaging types | Short-term to Mid-term |

| Workforce Skill Gap and Talent Shortage | -1.2% | Global, impacting R&D and manufacturing centers | Short-term to Long-term |

| Ensuring Reliability and Durability of Complex Packages | -1.0% | Global, particularly for mission-critical applications | Mid-term to Long-term |

| Intellectual Property (IP) Protection and Collaboration Complexities | -0.7% | Global, affecting cross-company R&D | Mid-term to Long-term |

| Environmental and Sustainability Concerns of Manufacturing | -0.5% | Global, driven by regulatory pressures | Long-term |

Semiconductor Advanced Packaging Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Semiconductor Advanced Packaging Market, offering valuable insights into its current landscape and future growth trajectories. The report meticulously covers key market attributes, historical data, and forward-looking forecasts, enabling stakeholders to make informed strategic decisions. It delves into the segmentation of the market by various parameters, providing a granular view of demand across different packaging types, applications, and regional landscapes. Furthermore, the report identifies and profiles key industry players, offering a competitive analysis that highlights market positioning and strategic initiatives. This detailed scope ensures a holistic understanding of market dynamics, emerging trends, and the opportunities and challenges shaping the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 60.0 Billion |

| Market Forecast in 2033 | USD 155.4 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASE Technology Holding, Amkor Technology, JCET Group, SPIL, Powertech Technology Inc, UTAC Group, STATS ChipPAC, Tongfu Microelectronics, United Microelectronics Corporation, Intel Corporation, Samsung Electronics Co Ltd, TSMC, Infineon Technologies AG, Texas Instruments Incorporated, STMicroelectronics, NXP Semiconductors, Broadcom Inc, Qualcomm Incorporated, Micron Technology Inc, SK Hynix Inc |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

:The Semiconductor Advanced Packaging Market is comprehensively analyzed across various segments to provide a detailed understanding of its dynamics and growth drivers. These segmentations allow for a granular view of market trends, enabling stakeholders to identify key growth areas and tailor their strategies effectively. Each segment contributes uniquely to the overall market landscape, driven by specific technological needs and application demands. The detailed breakdown covers the distinct packaging technologies, the diverse applications they enable, the industries that leverage them, and the critical materials involved in their manufacturing. This structured analysis highlights the multifaceted nature of the advanced packaging ecosystem and its intricate dependencies.

Understanding these segments is crucial for predicting market shifts, identifying investment opportunities, and optimizing product development. For instance, the rapid expansion of AI and high-performance computing heavily influences the demand for 2.5D/3D IC packaging, while the miniaturization trend in consumer electronics drives innovations in wafer-level packaging. Similarly, advancements in automotive electronics necessitate robust and reliable packaging solutions, pushing the boundaries of material science. The interdependencies between these segments underscore the complexity and dynamism of the semiconductor advanced packaging market, providing a roadmap for future strategic planning and innovation.

- By Packaging Type: This segment categorizes advanced packaging based on the foundational technology utilized.

- Flip Chip (FC): A direct chip attachment method enabling higher I/O density and better electrical performance.

- Wafer-Level Packaging (WLP): Packaging technologies performed at the wafer level before dicing, offering smaller form factors and lower cost.

- Fan-Out Wafer-Level Packaging (FOWLP): Packaging where the redistribution layer (RDL) extends beyond the original die area, allowing for more I/O connections.

- Fan-In Wafer-Level Packaging (FIWLP): Packaging where the RDL and contacts remain within the original die area.

- 2.5D/3D IC Packaging: Advanced stacking techniques using interposers (2.5D) or directly stacking dies with Through-Silicon Vias (TSVs) (3D) for high integration.

- System-in-Package (SiP): Integration of multiple active electronic components, as well as passive components and other devices, into a single package.

- Through-Silicon Via (TSV): Vertical electrical connections that pass completely through a silicon wafer or die, enabling 3D stacking.

- Others: Includes emerging technologies like Hybrid Bonding, Embedded Die, and other specialized packaging solutions.

- By Application: This segment groups advanced packaging based on its end-use in various electronic products and systems.

- Consumer Electronics: Devices such as smartphones, tablets, wearables, laptops, and smart home devices.

- Automotive: Applications in Advanced Driver-Assistance Systems (ADAS), infotainment systems, electric vehicle power electronics, and autonomous driving.

- High-Performance Computing (HPC) & Data Centers: Used in servers, supercomputers, AI accelerators, and networking infrastructure requiring extreme processing power and bandwidth.

- Industrial: Applications in industrial automation, robotics, smart manufacturing equipment, and industrial IoT.

- Healthcare: Utilized in medical devices, diagnostic equipment, and wearable health monitoring technologies.

- Aerospace & Defense: High-reliability and ruggedized packaging for avionics, military communication, and surveillance systems.

- Telecommunications: Critical for 5G base stations, networking equipment, and high-speed data transmission.

- Others: Includes emerging applications in quantum computing, specialized sensors, and niche markets.

- By End-Use Industry: This segment focuses on the primary industry verticals that adopt advanced packaging technologies.

- Electronics Manufacturing: Companies involved in the design and production of electronic devices.

- Semiconductor Foundries: Companies that fabricate semiconductor devices for other companies.

- IDM (Integrated Device Manufacturers): Companies that design, manufacture, and market their own semiconductor products.

- OSAT (Outsourced Semiconductor Assembly and Test): Companies specializing in outsourced assembly and testing of semiconductor devices.

- MEMS & Sensors: Industries focusing on Micro-Electro-Mechanical Systems and various types of sensors requiring specialized packaging.

- By Material: This segment delineates the market based on the critical materials used in advanced packaging processes.

- Substrates: Materials forming the base of the package, including Organic (e.g., BT resin), Ceramic, Glass, and Silicon substrates.

- Bonding Wires: Conductive wires used for electrical connections, primarily Copper, Gold, and Silver.

- Encapsulants: Materials used to protect the integrated circuit from environmental factors and mechanical damage.

- Dielectric Materials: Insulating materials used between conductive layers within the package.

- Others: Includes solder balls, underfill materials, thermal interface materials, and other specialized compounds.

Regional Highlights

The regional analysis of the Semiconductor Advanced Packaging Market reveals distinct patterns of growth, innovation, and manufacturing prowess across different geographies. Asia Pacific continues to dominate the global landscape, largely due to its established semiconductor manufacturing ecosystem, including leading foundries, OSAT (Outsourced Semiconductor Assembly and Test) providers, and a vast consumer electronics market. North America and Europe, while having strong R&D capabilities and demand from high-end applications like HPC and automotive, are increasingly focusing on strategic investments to bolster their domestic manufacturing capacities and supply chain resilience.- Asia Pacific (APAC): This region is the undisputed leader in the semiconductor advanced packaging market, driven by the presence of major semiconductor foundries, leading OSAT companies, and a robust electronics manufacturing base in countries like Taiwan, South Korea, China, and Japan. The high demand for consumer electronics, automotive components, and data center infrastructure in this region fuels continuous investment in advanced packaging technologies. Taiwan, in particular, stands out for its advanced foundry capabilities and expertise in 2.5D/3D packaging and Fan-Out WLP. South Korea is strong in memory packaging and SiP, while China is rapidly expanding its domestic packaging capabilities.

- North America: Characterized by strong innovation in high-performance computing, AI, and data center technologies, North America is a significant consumer and innovator in advanced packaging. The region focuses on cutting-edge packaging solutions for high-end processors, GPUs, and specialized AI accelerators. While much of the manufacturing is outsourced, there is a growing strategic push, backed by government initiatives, to bring more advanced packaging R&D and manufacturing back onshore to ensure supply chain security and technological leadership.

- Europe: Europe is a key player, especially in the automotive, industrial, and telecommunications sectors. Countries like Germany and France are driving demand for robust and reliable advanced packaging solutions for ADAS, industrial automation, and 5G infrastructure. The region excels in research and development, particularly in areas like MEMS packaging and sensor integration. Investments are also increasing to strengthen domestic manufacturing capabilities and foster collaboration across the semiconductor value chain within the EU.

- Latin America & Middle East and Africa (MEA): While currently smaller in market share compared to the leading regions, these areas present emerging opportunities. Growth in these regions is primarily driven by increasing digitalization, expanding consumer electronics markets, and developing IT infrastructure. Investments in new manufacturing facilities and increased adoption of advanced technologies are expected to contribute to future growth, albeit at a slower pace than the established semiconductor hubs.

Top Key Players:

The market research report covers the analysis of key stake holders of the Semiconductor Advanced Packaging Market. Some of the leading players profiled in the report include -:- ASE Technology Holding

- Amkor Technology

- JCET Group

- SPIL

- Powertech Technology Inc

- UTAC Group

- STATS ChipPAC

- Tongfu Microelectronics

- United Microelectronics Corporation

- Intel Corporation

- Samsung Electronics Co Ltd

- TSMC

- Infineon Technologies AG

- Texas Instruments Incorporated

- STMicroelectronics

- NXP Semiconductors

- Broadcom Inc

- Qualcomm Incorporated

- Micron Technology Inc

- SK Hynix Inc

Frequently Asked Questions:

What is semiconductor advanced packaging?

Semiconductor advanced packaging refers to a suite of innovative techniques and technologies that go beyond traditional chip encapsulation to enhance the performance, functionality, and form factor of integrated circuits. It involves sophisticated methods like 2.5D/3D integration, wafer-level packaging, and System-in-Package (SiP) solutions, enabling higher integration density, improved electrical performance, better thermal management, and smaller device footprints. These technologies are crucial for meeting the demands of modern electronic devices and high-performance computing.

Why is advanced packaging critical for future electronics?

Advanced packaging is critical for future electronics because it addresses the limitations of traditional chip scaling (Moore's Law) by enabling continued performance improvements, miniaturization, and heterogeneous integration. It allows different types of chips (e.g., logic, memory, sensors) to be combined into a single, high-performance package, reducing latency, improving power efficiency, and enabling new functionalities essential for emerging technologies like AI, 5G, autonomous vehicles, and IoT devices. It is a key enabler for the next generation of computing and communication.

How does AI impact the semiconductor advanced packaging market?

AI significantly impacts the semiconductor advanced packaging market by driving demand for solutions that offer ultra-high bandwidth, low latency, and efficient power delivery, which are essential for AI accelerators and high-performance computing. AI workloads necessitate advanced packaging techniques like 2.5D/3D integration with High-Bandwidth Memory (HBM) and complex multi-die configurations. Additionally, AI itself is increasingly being used to optimize advanced packaging manufacturing processes, improving yield, quality control, and overall efficiency in production.

What are the main types of advanced packaging technologies?

The main types of advanced packaging technologies include Flip Chip (FC), which provides higher I/O density and better electrical performance; Wafer-Level Packaging (WLP), encompassing Fan-In WLP (FIWLP) and Fan-Out WLP (FOWLP) for compact designs; 2.5D/3D IC packaging, which stacks dies vertically using interposers or Through-Silicon Vias (TSVs) for increased integration; and System-in-Package (SiP), which integrates multiple components into a single package for miniaturization and enhanced functionality. Emerging technologies like hybrid bonding are also gaining prominence.

Which regions are leading in semiconductor advanced packaging innovation and manufacturing?

Asia Pacific is the leading region in semiconductor advanced packaging innovation and manufacturing, particularly driven by countries like Taiwan, South Korea, China, and Japan. This dominance is due to the presence of major foundries, outsourced semiconductor assembly and test (OSAT) companies, and a robust electronics manufacturing ecosystem. North America and Europe also contribute significantly, particularly in advanced research and development for high-performance computing, AI, and automotive applications, with increasing strategic investments to bolster their domestic manufacturing capabilities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted