SDN Orchestration Market

SDN Orchestration Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708686 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

SDN Orchestration Market Size

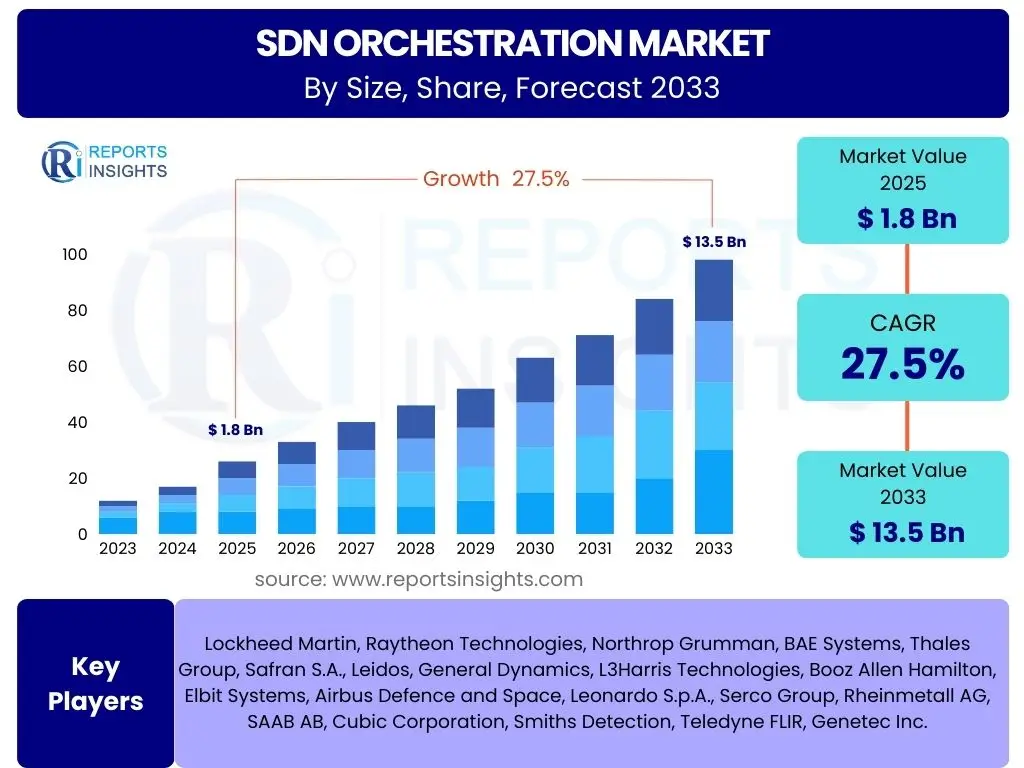

According to Reports Insights Consulting Pvt Ltd, The SDN Orchestration Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 27.5% between 2025 and 2033. The market is estimated at USD 1.8 Billion in 2025 and is projected to reach USD 13.5 Billion by the end of the forecast period in 2033.

Key SDN Orchestration Market Trends & Insights

Users frequently inquire about the evolving landscape of SDN orchestration, particularly regarding its integration with emerging technologies and its role in enterprise digital transformation. The market is witnessing a significant shift towards more automated, AI-driven solutions that provide enhanced network visibility, proactive management, and reduced operational complexities. There is a growing demand for multi-domain orchestration capabilities that can seamlessly manage hybrid and multi-cloud environments, addressing the complexities introduced by diverse infrastructure components. Furthermore, the emphasis on security and compliance within orchestrated networks is becoming a paramount concern, driving innovations in secure-by-design orchestration frameworks.

Another prominent trend observed is the increasing adoption of open-source SDN orchestration platforms, which offer flexibility and cost-effectiveness, fostering a collaborative ecosystem for development and innovation. This trend is complemented by the rising need for robust analytics and real-time telemetry to optimize network performance and resource utilization effectively. Enterprises are actively seeking solutions that can not only automate routine tasks but also intelligently predict and prevent network issues, thereby improving overall service delivery and end-user experience. The convergence of network functions virtualization (NFV) with SDN orchestration continues to drive the demand for comprehensive, end-to-end service automation across telecommunication and data center infrastructures.

- Shift towards AI-driven automation for network management.

- Increased demand for multi-domain and hybrid cloud orchestration.

- Growing adoption of open-source SDN orchestration platforms.

- Emphasis on enhanced security and compliance in orchestrated environments.

- Rising importance of real-time network analytics and telemetry.

- Convergence of SDN orchestration with NFV for end-to-end service automation.

- Focus on proactive network issue prediction and prevention.

AI Impact Analysis on SDN Orchestration

User inquiries concerning AI's influence on SDN Orchestration predominantly revolve around its potential to enhance automation, predictive capabilities, and operational efficiency, alongside concerns regarding data privacy and the complexity of integration. AI is poised to revolutionize SDN orchestration by enabling intelligent decision-making, optimizing resource allocation, and automating complex network configurations that would otherwise require extensive manual intervention. Its application in areas such as anomaly detection, predictive maintenance, and dynamic traffic management promises significant improvements in network performance, reliability, and security. However, questions persist regarding the ethical implications of AI-driven network control and the need for robust governance frameworks to ensure transparent and responsible deployment.

The integration of AI into SDN orchestration frameworks is expected to foster a new generation of self-healing and self-optimizing networks, capable of adapting to changing demands and mitigating threats autonomously. This includes leveraging machine learning algorithms for traffic engineering, identifying security vulnerabilities in real-time, and automating root cause analysis for faster problem resolution. While the benefits in terms of cost reduction and service agility are substantial, organizations are also keen to understand the practical challenges associated with data collection, model training, and the skilled workforce required to manage these advanced systems. Overcoming these hurdles will be critical for widespread AI adoption in the SDN orchestration domain.

- Enables intelligent automation for network configuration and management.

- Enhances predictive analytics for anomaly detection and proactive issue resolution.

- Optimizes dynamic resource allocation and traffic engineering.

- Facilitates the development of self-healing and self-optimizing networks.

- Improves real-time security threat detection and mitigation.

- Automates complex root cause analysis, reducing mean time to repair (MTTR).

- Raises concerns regarding data privacy, ethical considerations, and integration complexity.

Key Takeaways SDN Orchestration Market Size & Forecast

Common user questions regarding market size and forecast highlight a strong interest in understanding the long-term growth trajectory and the underlying factors driving this expansion. The SDN Orchestration market is poised for robust growth throughout the forecast period, driven primarily by the escalating demand for network automation and the widespread adoption of cloud-based services. Enterprises and service providers are increasingly investing in SDN orchestration solutions to manage the increasing complexity of modern networks, optimize operational expenditures, and enhance agility in service delivery. The projected substantial increase in market valuation signifies a critical transition towards software-defined and automated network infrastructures across various industries.

Furthermore, the significant Compound Annual Growth Rate (CAGR) projected reflects the accelerating pace of digital transformation and the imperative for organizations to build more resilient, scalable, and intelligent networks. The forecast indicates that SDN orchestration will play a pivotal role in enabling flexible network architectures that can seamlessly integrate with hybrid IT environments and support emerging technologies such as 5G, IoT, and edge computing. This robust growth underscores the market's maturity and its crucial function in future-proofing network infrastructures against evolving demands and technological advancements.

- Significant market growth expected, driven by network automation and cloud adoption.

- Substantial increase in market valuation from 2025 to 2033.

- SDN orchestration is crucial for managing modern network complexity.

- Key enabler for digital transformation and service agility across enterprises.

- Essential for supporting emerging technologies like 5G, IoT, and edge computing.

- Indicates a strong industry shift towards software-defined and automated networks.

SDN Orchestration Market Drivers Analysis

The SDN Orchestration market is propelled by several compelling factors that underscore the imperative for modernizing network infrastructures. A primary driver is the exponential growth in network complexity, stemming from the proliferation of cloud services, diverse applications, and an increasing number of connected devices. Organizations are seeking sophisticated tools to manage this complexity, automate routine tasks, and ensure optimal performance and security across distributed environments. SDN orchestration offers a unified approach to policy enforcement, resource allocation, and service chain management, significantly simplifying operations.

Another critical driver is the continuous demand for operational efficiency and cost reduction within IT departments. By automating network provisioning, configuration, and maintenance, SDN orchestration minimizes human error, reduces manual effort, and allows IT teams to focus on strategic initiatives rather than repetitive tasks. This efficiency gain, coupled with the ability to dynamically scale network resources, translates into tangible cost savings and improved resource utilization, making it an attractive investment for enterprises and service providers alike. The shift towards agile and DevOps methodologies in software development further necessitates flexible and programmable network infrastructures that SDN orchestration inherently provides.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Network Complexity and Data Traffic | +5.0% | Global, particularly North America, APAC | 2025-2033 |

| Rising Adoption of Cloud Computing and Virtualization | +4.5% | Global | 2025-2033 |

| Demand for Network Automation and Operational Efficiency | +4.0% | Global, strong in developed economies | 2025-2033 |

| Growth of 5G, IoT, and Edge Computing | +3.5% | APAC, North America, Europe | 2026-2033 |

SDN Orchestration Market Restraints Analysis

Despite its significant growth potential, the SDN Orchestration market faces several restraints that could impede its widespread adoption. One major challenge is the substantial initial investment required for deploying and integrating SDN orchestration solutions. This includes costs associated with new hardware, software licenses, and the necessary infrastructure upgrades, which can be prohibitive for smaller organizations or those with legacy systems. The perceived high capital expenditure often deters potential adopters, especially when the long-term return on investment is not immediately clear or quantified.

Another significant restraint is the complexity involved in migrating from traditional network architectures to software-defined environments. This transition requires extensive planning, skilled personnel, and careful management to avoid service disruptions. The interoperability challenges between different vendor solutions and existing legacy systems also add to this complexity, demanding significant customization and integration efforts. Furthermore, a shortage of skilled professionals with expertise in SDN orchestration, network programming, and automation technologies poses a critical hurdle, limiting the effective implementation and management of these advanced systems across various regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Migration Costs | -3.0% | Global, more pronounced in emerging economies | 2025-2029 |

| Interoperability and Integration Challenges with Legacy Systems | -2.5% | Global | 2025-2030 |

| Lack of Skilled Workforce and Expertise | -2.0% | Global | 2025-2033 |

| Security Concerns in Software-Defined Networks | -1.5% | Global | 2025-2033 |

SDN Orchestration Market Opportunities Analysis

The SDN Orchestration market presents numerous opportunities for growth, driven by evolving technological landscapes and increasing enterprise demands. The expansion of 5G networks and the proliferation of IoT devices globally represent a significant opportunity. These technologies necessitate highly agile, scalable, and automated network infrastructures to manage massive data volumes and diverse connectivity requirements. SDN orchestration is uniquely positioned to provide the dynamic provisioning and management capabilities essential for optimizing resource utilization and ensuring seamless service delivery in these next-generation environments, particularly for use cases in smart cities, industrial automation, and connected vehicles.

Furthermore, the growing adoption of hybrid cloud and multi-cloud strategies by enterprises creates a substantial demand for unified network orchestration solutions. Organizations seek to seamlessly extend their network policies and services across on-premises data centers and various public cloud environments, requiring robust orchestration platforms that can bridge these disparate domains. This trend opens avenues for vendors offering integrated, multi-cloud management capabilities, enabling consistent network connectivity, security, and performance regardless of the underlying infrastructure. The continuous innovation in AI and machine learning also provides opportunities for developing more intelligent, self-optimizing SDN orchestration solutions that can proactively address network challenges and enhance operational efficiency.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of 5G Networks and IoT Ecosystems | +4.0% | APAC, North America, Europe | 2026-2033 |

| Increasing Adoption of Hybrid and Multi-Cloud Architectures | +3.5% | Global | 2025-2033 |

| Demand for Network Slicing in 5G for Diverse Services | +3.0% | APAC, Europe | 2027-2033 |

| Integration of AI/ML for Predictive Network Management | +2.5% | Global | 2025-2033 |

SDN Orchestration Market Challenges Impact Analysis

The SDN Orchestration market faces several inherent challenges that demand strategic solutions from vendors and adopters alike. One significant challenge is the ongoing concern regarding network security within software-defined environments. While SDN offers greater control and visibility, the centralization of control planes introduces new potential attack vectors. Ensuring robust security policies, granular access controls, and effective threat detection mechanisms across a dynamically changing network infrastructure remains a complex task, requiring continuous innovation in security features and integration with existing security frameworks.

Another major challenge lies in achieving true interoperability and standardization across the diverse ecosystem of SDN components and vendor offerings. The lack of a universally accepted set of open standards can lead to vendor lock-in and complicate the integration of different SDN solutions, especially in multi-vendor environments. This fragmentation can hinder seamless communication and policy enforcement across different network domains, thereby limiting the full potential of SDN orchestration. Additionally, the rapid pace of technological evolution necessitates constant updates and training, which can be challenging for organizations to keep up with, further impacting adoption rates and successful deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Robust Security in Software-Defined Networks | -2.0% | Global | 2025-2033 |

| Lack of Standardization and Interoperability | -1.5% | Global | 2025-2030 |

| Complexities in Managing Multi-Vendor Environments | -1.0% | Global | 2025-2033 |

| Rapid Technological Evolution and Need for Continuous Training | -0.8% | Global | 2025-2033 |

SDN Orchestration Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the SDN Orchestration market, providing an in-depth analysis of its current landscape and future trajectory. It covers critical aspects such as market size, growth drivers, restraints, opportunities, and challenges across various segments and geographical regions. The report offers stakeholders actionable insights to navigate the evolving market, identify strategic growth avenues, and make informed business decisions by examining key trends, competitive landscapes, and the impact of emerging technologies like AI on market development.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 13.5 Billion |

| Growth Rate | 27.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Cisco Systems Inc., VMware Inc., Ericsson AB, Nokia Corporation, Juniper Networks Inc., Huawei Technologies Co. Ltd., IBM Corporation, Hewlett Packard Enterprise (HPE), Fujitsu Limited, NEC Corporation, Ciena Corporation, Dell Technologies Inc., Arista Networks Inc., Versa Networks Inc., Zscaler Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The SDN Orchestration market is meticulously segmented to provide a granular understanding of its diverse components, deployment methods, target end-users, and functional applications. This segmentation allows for a detailed analysis of specific market niches, identifying areas of high growth and emerging opportunities. The market's structure reflects the evolving needs of various industries seeking enhanced network agility, automation, and cost-efficiency through software-defined networking principles.

Each segment and sub-segment is influenced by distinct drivers and faces unique challenges, contributing differently to the overall market dynamics. For instance, the 'Software' component segment, particularly orchestrators and analytics, is expected to exhibit robust growth due to the increasing demand for intelligent, automated network management. Similarly, the 'Cloud-Based' deployment model is gaining traction among service providers and enterprises aiming for greater flexibility and scalability, while the 'Service Providers' end-user segment remains a dominant force due to their extensive network infrastructures and the imperative to deliver innovative, agile services.

- By Component

- Software

- Controller

- Orchestrator

- Analytics & Virtual Network Functions

- Services

- Professional Services

- Managed Services

- Software

- By Deployment Model

- On-Premises

- Cloud-Based

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By End-User

- Service Providers

- Telecommunication Service Providers

- Cloud Service Providers

- Managed Service Providers

- Enterprises

- BFSI

- IT & Telecom

- Healthcare

- Government

- Manufacturing

- Retail

- Media & Entertainment

- Others

- Service Providers

- By Application

- Network Virtualization

- Data Center Automation

- Cloud Bursting

- Service Chaining

- Bandwidth on Demand

- Others

Regional Highlights

The global SDN Orchestration market exhibits diverse growth patterns and adoption rates across different geographical regions, influenced by varying levels of digital infrastructure development, regulatory frameworks, and enterprise IT spending. North America currently holds a significant share of the market, driven by the early adoption of advanced networking technologies, a robust presence of key market players, and high investment in cloud computing and data centers. The region's mature IT infrastructure and the continuous drive for network modernization by large enterprises and telecommunication service providers contribute significantly to its market dominance. Furthermore, the rapid expansion of 5G networks and the increasing demand for software-defined security solutions are fueling further growth in this region.

Europe is also a substantial market for SDN orchestration, characterized by strong regulatory support for digital transformation and a growing emphasis on industrial automation and smart infrastructure. Countries such as Germany, the UK, and France are leading the adoption, primarily due to initiatives aimed at enhancing network efficiency, supporting distributed cloud architectures, and improving cybersecurity postures. The region's focus on data privacy and the General Data Protection Regulation (GDPR) further drives the need for sophisticated network control and orchestration capabilities to ensure compliance and data integrity across complex network environments. Investment in smart city projects and next-generation mobile networks continues to bolster market expansion in Europe.

The Asia Pacific (APAC) region is projected to experience the highest growth rate during the forecast period, primarily due to rapid economic development, increasing digitalization across industries, and massive investments in telecommunications infrastructure. Countries like China, India, Japan, and South Korea are at the forefront of 5G deployment, IoT adoption, and data center expansion, creating immense demand for advanced SDN orchestration solutions. The region's large population, growing internet penetration, and the rise of digital-native businesses necessitate scalable and flexible network architectures, making SDN orchestration a critical component of their IT strategies. Government initiatives supporting digital transformation further accelerate market growth in APAC.

Latin America and the Middle East & Africa (MEA) regions are emerging markets for SDN orchestration, with significant growth potential over the forecast period. In Latin America, the increasing demand for enhanced connectivity, cloud services, and digital transformation initiatives in countries like Brazil and Mexico are driving the adoption of SDN solutions. The MEA region is witnessing substantial investments in smart city projects, data centers, and telecommunication infrastructure, particularly in the Gulf Cooperation Council (GCC) countries and South Africa. As these regions continue to develop their digital economies, the need for efficient, automated network management will become paramount, fostering greater adoption of SDN orchestration technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the SDN Orchestration Market.- Cisco Systems Inc.

- VMware Inc.

- Ericsson AB

- Nokia Corporation

- Juniper Networks Inc.

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Fujitsu Limited

- NEC Corporation

- Ciena Corporation

- Dell Technologies Inc.

- Arista Networks Inc.

- Versa Networks Inc.

- Zscaler Inc.

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- ServiceNow Inc.

- NTT Communications Corporation

Frequently Asked Questions

Analyze common user questions about the SDN Orchestration market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is SDN Orchestration and why is it important?

SDN Orchestration refers to the automated coordination and management of network resources and services in a software-defined networking (SDN) environment. It is crucial because it automates complex network tasks, enhances agility, optimizes resource utilization, and ensures consistent policy enforcement across diverse network infrastructures, significantly reducing operational costs and human error.

How does SDN Orchestration differ from traditional network management?

SDN Orchestration differs from traditional network management by providing a centralized, programmable control plane that abstracts the underlying hardware. This enables automated, policy-driven network configuration and dynamic resource allocation, contrasting with traditional methods that rely heavily on manual, device-by-device configuration and lack holistic, real-time visibility.

What are the primary benefits of implementing SDN Orchestration?

Key benefits include enhanced network agility and flexibility, significant reduction in operational expenses through automation, improved network performance and reliability, simplified management of complex and hybrid IT environments, faster service delivery, and stronger security posture through centralized policy enforcement.

What challenges might organizations face when adopting SDN Orchestration?

Organizations may encounter challenges such as high initial investment costs, complexities in integrating with existing legacy infrastructure, a shortage of skilled personnel with SDN expertise, and concerns regarding network security in a centralized control plane environment. Achieving vendor interoperability can also be a significant hurdle.

How will AI and Machine Learning impact the future of SDN Orchestration?

AI and Machine Learning will profoundly impact SDN Orchestration by enabling more intelligent automation, predictive analytics for network issues, dynamic traffic optimization, and self-healing capabilities. This will lead to highly autonomous networks that can adapt to changing conditions, proactively mitigate threats, and significantly enhance operational efficiency and network resilience.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted