Scandium Oxide Market

Scandium Oxide Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707249 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

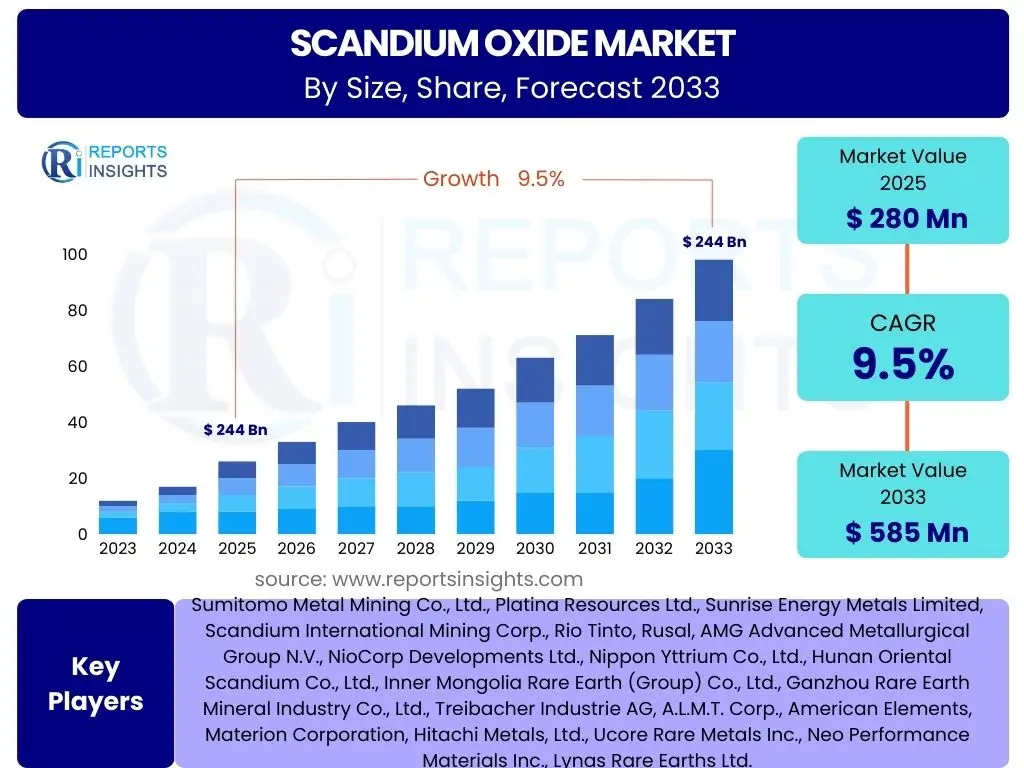

Scandium Oxide Market Size

According to Reports Insights Consulting Pvt Ltd, The Scandium Oxide Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 280 Million in 2025 and is projected to reach USD 585 Million by the end of the forecast period in 2033.

Key Scandium Oxide Market Trends & Insights

Analysis of common user queries regarding Scandium Oxide market trends reveals a strong interest in its burgeoning applications, particularly in high-performance alloys and energy technologies. Users are keen to understand how supply chain developments and technological advancements are shaping the market's trajectory, along with the increasing emphasis on sustainable sourcing and recycling initiatives. The market's growth is inherently linked to innovations in materials science and the expansion of industries requiring advanced, lightweight, and durable components.

A notable trend involves the growing demand for scandium-aluminum (Sc-Al) alloys, driven by the aerospace and automotive sectors' relentless pursuit of weight reduction without compromising strength. Another significant insight is the critical role of Scandium Oxide in Solid Oxide Fuel Cells (SOFCs), where its unique properties enhance efficiency and longevity, positioning it as a key material in the future of energy generation. Furthermore, the market is observing increased exploration into secondary sources and recycling methods to mitigate supply volatility and address environmental concerns, indicating a shift towards a more circular economy for rare earth elements.

- Surging demand for scandium-aluminum alloys in aerospace and automotive for lightweighting.

- Growing adoption in Solid Oxide Fuel Cells (SOFCs) for improved efficiency and durability.

- Increased research and development in advanced materials, including 3D printing applications.

- Emphasis on diversifying supply sources and developing sustainable extraction and recycling methods.

- Technological advancements in production processes to reduce costs and enhance purity.

AI Impact Analysis on Scandium Oxide

Common user questions regarding the impact of Artificial Intelligence (AI) on the Scandium Oxide market predominantly revolve around optimizing material discovery, enhancing production efficiency, and improving supply chain resilience. Users are interested in how AI can accelerate the identification of new scandium applications and alloys, predict market demand fluctuations, and streamline complex extraction and refining processes to reduce overall costs and environmental footprints.

AI's influence extends to predictive analytics for supply chain management, enabling better forecasting of raw material availability and demand, thereby mitigating price volatility and supply disruptions. Furthermore, AI-driven simulations and machine learning algorithms are increasingly being employed in materials science research to design novel scandium-containing compounds with tailored properties, significantly reducing the time and cost associated with traditional R&D. This integration of AI is set to revolutionize how Scandium Oxide is produced, processed, and utilized across various industries, fostering innovation and operational excellence.

- AI-driven material discovery and optimization for new scandium alloys and applications.

- Predictive analytics for enhanced supply chain management and demand forecasting.

- Process optimization in extraction and refining, leading to increased efficiency and reduced costs.

- Quality control and defect detection improvement in scandium-containing components manufacturing.

- Accelerated research and development through AI-powered simulations and data analysis.

Key Takeaways Scandium Oxide Market Size & Forecast

User queries about the Scandium Oxide market forecast frequently highlight the desire to understand the most significant growth enablers and potential challenges over the coming decade. A primary takeaway is the market's robust growth trajectory, fundamentally driven by its unique properties—lightweight, high strength-to-weight ratio, and excellent thermal stability—making it indispensable in high-value applications across aerospace, defense, and clean energy sectors. The projected increase in market size underscores a widening acceptance and integration of scandium-based solutions in critical industries.

Another key insight is the pivotal role of ongoing research and development in unlocking new commercial applications for Scandium Oxide, which is crucial for sustained market expansion beyond established uses. Despite potential supply constraints and high production costs, the increasing strategic importance of scandium in next-generation technologies, combined with efforts to diversify sourcing and improve extraction efficiencies, positions the market for significant long-term expansion. The forecast reflects a strong commitment from various industries to leverage scandium's advanced material properties for performance enhancement and technological innovation.

- Strong market growth anticipated, driven by high-performance applications in aerospace and energy.

- The critical role of Scandium Oxide in enabling advanced lightweight and high-efficiency technologies.

- Increasing strategic importance due to its unique material properties and versatility.

- Potential for new application discovery through continuous R&D and material science advancements.

- Efforts to secure and diversify supply chains are crucial for sustained market development.

Scandium Oxide Market Drivers Analysis

The Scandium Oxide market is significantly propelled by the escalating demand from industries prioritizing weight reduction, enhanced strength, and improved energy efficiency. The aerospace and defense sectors are particularly influential, with their constant need for advanced lightweight alloys that can offer superior performance and fuel efficiency in aircraft and missile components. Scandium-aluminum alloys, known for their exceptional strength-to-weight ratio and resistance to fatigue, are becoming increasingly attractive alternatives to traditional materials, driving substantial demand for Scandium Oxide. This fundamental shift towards high-performance materials is a core accelerator for market expansion.

Beyond aerospace, the burgeoning Solid Oxide Fuel Cells (SOFCs) market represents another crucial driver. Scandium-stabilized zirconia (ScSZ) electrolytes are instrumental in SOFCs, offering higher ionic conductivity and lower operating temperatures compared to other alternatives, leading to increased energy conversion efficiency and durability. As global efforts intensify to transition towards cleaner energy sources, the adoption of SOFCs for stationary power generation and auxiliary power units (APUs) is growing, directly translating into higher demand for Scandium Oxide. Furthermore, the expansion of 3D printing technologies and the exploration of scandium in medical implants and sports equipment are opening new application avenues, reinforcing the market's growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Lightweight Sc-Al Alloys (Aerospace & Automotive) | +1.8% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increasing Adoption in Solid Oxide Fuel Cells (SOFCs) | +1.5% | Asia Pacific, Europe, North America | Mid-to-Long term (2027-2033) |

| Advancements in 3D Printing and Additive Manufacturing | +0.9% | Global | Mid-to-Long term (2028-2033) |

| Rising Investments in Renewable Energy and Clean Technologies | +1.2% | Global | Long-term (2025-2033) |

| Increased Research & Development for New Scandium Applications | +0.7% | Global | Long-term (2025-2033) |

Scandium Oxide Market Restraints Analysis

Despite its promising applications, the Scandium Oxide market faces significant restraints, primarily stemming from its high production cost and limited primary supply sources. Scandium is predominantly obtained as a by-product of mining operations for other metals like aluminum, titanium, or rare earths, which makes its supply inherently dependent on the economics and output of these larger-scale operations. This by-product nature leads to a fragmented and often inconsistent supply, creating bottlenecks that can hinder large-scale adoption and lead to price volatility. The complex and energy-intensive extraction and refining processes further contribute to the high per-unit cost of Scandium Oxide, making it economically unfeasible for some potential applications and limiting its widespread commercialization.

Another major restraint is the relatively low awareness and limited commercial-scale production outside niche applications. While its properties are well-known in specialized scientific and engineering communities, the broader industrial market has not fully integrated scandium into its material strategies due to its scarcity and cost. This lack of widespread adoption means that industries often opt for more readily available and cheaper alternatives, even if they offer inferior performance. Overcoming these fundamental supply and cost barriers, along with educating potential end-users about its long-term value proposition, remains critical for unlocking the market's full potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Cost and Price Volatility | -1.1% | Global | Long-term (2025-2033) |

| Limited Primary Supply Sources and By-Product Nature | -0.9% | Global | Long-term (2025-2033) |

| Complex and Energy-Intensive Extraction Processes | -0.6% | Global | Long-term (2025-2033) |

| Lack of Widespread Industrial Awareness and Adoption | -0.4% | Global | Mid-to-Long term (2026-2033) |

| Availability of Alternative Materials with Lower Cost | -0.3% | Global | Short-to-Mid term (2025-2029) |

Scandium Oxide Market Opportunities Analysis

The Scandium Oxide market presents several compelling opportunities for growth and innovation, largely driven by advancements in extraction technologies and the increasing focus on resource efficiency. The development of more cost-effective and environmentally friendly methods for extracting scandium from abundant secondary sources, such as red mud (bauxite residue) from aluminum production, holds immense promise. These new extraction techniques could significantly lower production costs and diversify the global supply, thereby making scandium more accessible and attractive for a wider range of industrial applications. Investing in these innovative extraction and processing technologies is a key pathway to unlocking substantial market expansion.

Furthermore, the burgeoning electric vehicle (EV) industry and the broader push towards sustainable transportation offer substantial opportunities. Scandium-enhanced materials could play a role in lightweight EV components, improving battery efficiency and vehicle range, and potentially in next-generation battery technologies. The circular economy principles, particularly recycling initiatives for scandium-containing products, also represent a significant opportunity to establish a more sustainable and secure supply chain, reducing reliance on virgin material extraction. Strategic partnerships between miners, refiners, and end-users, along with supportive government policies for critical materials, can further accelerate market development and capitalize on these emerging opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Cost-Effective Extraction from Secondary Sources (e.g., Red Mud) | +1.5% | Asia Pacific, Europe, Global | Long-term (2028-2033) |

| Expansion into Electric Vehicle (EV) Lightweighting and Battery Applications | +1.3% | Global | Mid-to-Long term (2027-2033) |

| Growth in Aerospace Modernization and Next-Generation Aircraft Programs | +1.0% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increased Investment in Scandium Recycling and Circular Economy Initiatives | +0.8% | Global | Mid-to-Long term (2028-2033) |

| Strategic Partnerships and Joint Ventures Across the Value Chain | +0.7% | Global | Short-to-Mid term (2025-2030) |

Scandium Oxide Market Challenges Impact Analysis

The Scandium Oxide market faces several significant challenges that could impede its growth, primarily revolving around supply chain vulnerability and the high capital intensity required for new production ventures. Given that scandium is predominantly a by-product, its supply is often at the mercy of the operational stability and economic viability of larger mining projects. This inherent reliance creates a vulnerable supply chain susceptible to geopolitical tensions, trade disputes, and operational disruptions at primary mining sites, leading to supply uncertainty and price fluctuations. Establishing stable and diversified supply routes for Scandium Oxide remains a critical hurdle for widespread industrial adoption.

Furthermore, the development of new scandium extraction and refining facilities demands substantial capital investment, posing a significant barrier to entry for new players and limiting rapid scaling of production. Environmental regulations pertaining to mining and chemical processing also present a complex challenge, requiring adherence to stringent standards that add to operational costs and project timelines. Overcoming these challenges necessitates significant governmental support, sustained private investment, and continuous innovation in sustainable processing technologies to ensure a robust, environmentally compliant, and economically viable supply of Scandium Oxide to meet anticipated demand.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Vulnerability and Geopolitical Risks | -0.8% | Global | Long-term (2025-2033) |

| High Capital Investment Required for New Production Projects | -0.7% | Global | Long-term (2025-2033) |

| Stringent Environmental Regulations for Mining and Processing | -0.5% | Global | Long-term (2025-2033) |

| Market Acceptance and Industrial Scale-Up for New Applications | -0.4% | Global | Mid-to-Long term (2026-2033) |

| Technological Barriers in Purity Enhancement and Cost Reduction | -0.3% | Global | Long-term (2025-2033) |

Scandium Oxide Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Scandium Oxide market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers historical data from 2019 to 2023, provides current market estimates for 2025, and presents a robust forecast up to 2033, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 280 Million |

| Market Forecast in 2033 | USD 585 Million |

| Growth Rate | 9.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sumitomo Metal Mining Co., Ltd., Platina Resources Ltd., Sunrise Energy Metals Limited, Scandium International Mining Corp., Rio Tinto, Rusal, AMG Advanced Metallurgical Group N.V., NioCorp Developments Ltd., Nippon Yttrium Co., Ltd., Hunan Oriental Scandium Co., Ltd., Inner Mongolia Rare Earth (Group) Co., Ltd., Ganzhou Rare Earth Mineral Industry Co., Ltd., Treibacher Industrie AG, A.L.M.T. Corp., American Elements, Materion Corporation, Hitachi Metals, Ltd., Ucore Rare Metals Inc., Neo Performance Materials Inc., Lynas Rare Earths Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Scandium Oxide market is meticulously segmented to provide a granular understanding of its diverse applications, forms, purities, and sources, reflecting the varied requirements of end-use industries. This comprehensive segmentation allows for precise market analysis, identifying key growth areas and niche opportunities within the broader market landscape. Understanding these segments is crucial for stakeholders to tailor product offerings and marketing strategies effectively, addressing specific industrial demands and technological trends across the value chain.

- By Application:

- Aerospace & Defense: Dominant segment due to demand for lightweight, high-strength alloys in aircraft and missile components.

- Solid Oxide Fuel Cells (SOFCs): Rapidly growing segment driven by clean energy initiatives and advancements in energy conversion.

- Lighting (High-Intensity Discharge Lamps): Traditional application, experiencing steady demand.

- Sports Equipment: Niche application utilizing lightweight properties in bicycles, bats, etc.

- 3D Printing: Emerging application for advanced additive manufacturing materials.

- Automotive: Increasing interest for lightweight vehicle components to improve fuel efficiency and EV range.

- Others: Includes medical implants, advanced ceramics, and research applications.

- By Purity:

- 99.9% (3N): Standard purity for industrial applications.

- 99.99% (4N): Higher purity for specialized electronic and advanced material uses.

- 99.999% (5N): Ultra-high purity required for sensitive applications like semiconductors and advanced optics.

- Others: Including lower or custom purity levels.

- By Form:

- Powder: Most common form, used as a raw material for alloys and ceramics.

- Sputtering Target: Used in thin-film deposition for electronics and optics.

- Other Forms: Includes pellets, ingots, or custom shapes for specific processes.

- By Source:

- Primary Production (mining by-product): Scandium extracted as a by-product from ores of other metals like bauxite, titanium, or rare earths.

- Secondary Production (red mud, waste streams): Scandium recovered from industrial waste, offering a sustainable alternative.

- Recycling: Recovery of scandium from end-of-life products or manufacturing scrap.

Regional Highlights

- North America: This region demonstrates strong demand, primarily driven by its robust aerospace and defense industries. Significant investments in advanced materials research and a growing emphasis on high-performance alloys contribute to the region's market share. The United States and Canada are key players, with continuous innovation in lightweighting technologies and a focus on critical material supply chain security. The adoption of SOFC technology for commercial and industrial applications is also gaining traction, further bolstering demand.

- Europe: Europe is a vital market for Scandium Oxide, characterized by a well-established automotive sector that increasingly seeks lightweight solutions for fuel efficiency and electric vehicle performance. Furthermore, the region's strong commitment to renewable energy and the development of fuel cell technologies significantly drives the demand for Scandium Oxide in SOFC applications. Countries like Germany and France are at the forefront of advanced materials research and development, contributing to the market's expansion.

- Asia Pacific (APAC): The Asia Pacific region is anticipated to exhibit the highest growth rate, fueled by rapid industrialization, expanding manufacturing capabilities, and significant investments in electronics, automotive, and clean energy sectors. China, as a major producer and consumer of rare earth elements, plays a pivotal role in the scandium supply chain. Japan and South Korea are key innovators in SOFC technology and advanced materials, contributing substantially to regional demand and technological advancements. The region's increasing aerospace and defense spending also adds to market growth.

- Latin America: This region presents emerging opportunities for Scandium Oxide, particularly through its developing industrial base and potential for new mining projects that could yield scandium as a by-product. While currently a smaller market, growing industrialization and increasing awareness of advanced material benefits are expected to drive gradual adoption in various applications over the forecast period.

- Middle East and Africa (MEA): The MEA region is at an nascent stage in the Scandium Oxide market, but holds future potential. Investments in industrial diversification, infrastructure development, and nascent aerospace and defense capabilities could lead to increased demand. Exploration for mineral resources and potential partnerships for raw material processing could also contribute to market evolution in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Scandium Oxide Market.- Sumitomo Metal Mining Co., Ltd.

- Platina Resources Ltd.

- Sunrise Energy Metals Limited

- Scandium International Mining Corp.

- Rio Tinto

- Rusal

- AMG Advanced Metallurgical Group N.V.

- NioCorp Developments Ltd.

- Nippon Yttrium Co., Ltd.

- Hunan Oriental Scandium Co., Ltd.

- Inner Mongolia Rare Earth (Group) Co., Ltd.

- Ganzhou Rare Earth Mineral Industry Co., Ltd.

- Treibacher Industrie AG

- A.L.M.T. Corp.

- American Elements

- Materion Corporation

- Hitachi Metals, Ltd.

- Ucore Rare Metals Inc.

- Neo Performance Materials Inc.

- Lynas Rare Earths Ltd.

Frequently Asked Questions

Analyze common user questions about the Scandium Oxide market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Scandium Oxide used for primarily?

Scandium Oxide is primarily used in the production of high-strength, lightweight scandium-aluminum alloys for aerospace and defense applications. It is also a critical component in Solid Oxide Fuel Cells (SOFCs) for clean energy generation and in high-intensity discharge lamps.

What are the key drivers for the Scandium Oxide market growth?

Key drivers include the surging demand for lightweight materials in aerospace and automotive, increasing adoption in Solid Oxide Fuel Cells (SOFCs) for energy efficiency, and growing applications in advanced manufacturing processes like 3D printing.

What are the main challenges facing the Scandium Oxide market?

The primary challenges include the high production cost, limited primary supply sources due to its by-product nature, complex extraction processes, and supply chain vulnerabilities susceptible to geopolitical risks.

How is Scandium Oxide typically sourced or produced?

Scandium Oxide is predominantly sourced as a by-product from the mining of other metals like aluminum, titanium, or rare earths. Efforts are increasing to extract it from secondary sources such as red mud (bauxite residue) and through recycling initiatives.

Which region is expected to show the most significant growth in the Scandium Oxide market?

The Asia Pacific (APAC) region is projected to exhibit the most significant growth, driven by rapid industrialization, expanding manufacturing sectors, and substantial investments in clean energy, electronics, and advanced materials across countries like China, Japan, and South Korea.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted