SCADA Market

SCADA Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703429 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

SCADA Market Size

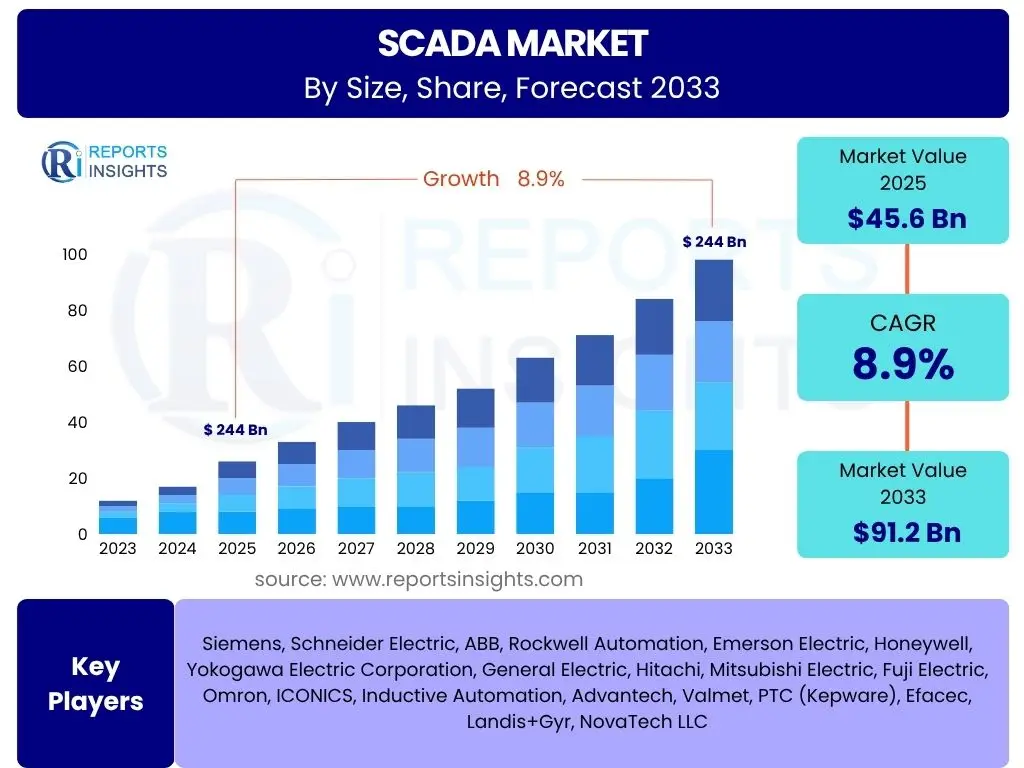

According to Reports Insights Consulting Pvt Ltd, The SCADA Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 45.6 Billion in 2025 and is projected to reach USD 91.2 Billion by the end of the forecast period in 2033.

Key SCADA Market Trends & Insights

The SCADA market is undergoing a significant transformation, driven by advancements in digital technologies and the increasing demand for operational efficiency across various industries. Common user questions often revolve around the shift towards more integrated, intelligent, and secure SCADA systems. Key trends indicate a strong move towards cloud-based deployments, allowing for greater scalability, remote accessibility, and reduced infrastructure costs. Furthermore, the convergence of SCADA with the Internet of Things (IoT) and Industrial Internet of Things (IIoT) is creating new paradigms for data collection, analysis, and control, enabling more granular monitoring and predictive capabilities.

Another prominent trend is the intensified focus on cybersecurity within SCADA environments. As operational technology (OT) networks become more interconnected, the vulnerability to cyber threats increases, prompting organizations to invest in robust security measures and real-time threat detection systems. Additionally, the adoption of edge computing is gaining traction, bringing computational power closer to the data source, which reduces latency and enhances the speed of critical decision-making. These evolving trends collectively define a market moving towards more resilient, agile, and intelligent automation solutions.

- Cloud-based SCADA adoption for enhanced scalability and remote access.

- Integration with IoT and IIoT for comprehensive data acquisition and predictive insights.

- Heightened emphasis on cybersecurity measures to protect critical infrastructure.

- Emergence of Edge Computing for real-time data processing and reduced latency.

- Increased demand for mobile and user-friendly SCADA interfaces.

- Application of Artificial Intelligence and Machine Learning for predictive maintenance and anomaly detection.

AI Impact Analysis on SCADA

User inquiries frequently address how Artificial Intelligence (AI) is transforming SCADA systems, focusing on its potential benefits and implementation challenges. AI’s impact on SCADA is profound, primarily enabling a shift from reactive to proactive operational management. Through machine learning algorithms, SCADA systems can now analyze vast amounts of operational data, identify subtle patterns, and predict equipment failures before they occur, significantly reducing downtime and maintenance costs. This predictive capability extends to optimizing energy consumption, enhancing process efficiency, and improving overall system reliability by learning from historical performance and adapting to dynamic conditions.

Beyond predictive maintenance, AI empowers SCADA with enhanced anomaly detection, distinguishing between normal operational fluctuations and genuine threats or malfunctions with greater accuracy than traditional rule-based systems. This capability is crucial for critical infrastructure protection and maintaining operational integrity. However, the integration of AI also introduces challenges such as the need for high-quality, labeled data for training models, the computational resources required for complex algorithms, and the expertise needed to deploy and manage AI-driven SCADA solutions. Despite these complexities, AI is poised to become an indispensable component of advanced SCADA architectures, offering intelligent automation and unprecedented levels of operational insight.

- Predictive maintenance and anomaly detection, minimizing downtime and operational disruptions.

- Operational optimization through real-time data analysis and intelligent resource allocation.

- Enhanced decision-making capabilities for operators based on AI-driven insights.

- Improved energy management and resource utilization in industrial processes.

- Strengthened cybersecurity by identifying unusual network behaviors and potential threats.

- Reduction in human error through automated responses and intelligent warnings.

Key Takeaways SCADA Market Size & Forecast

Common user questions regarding the SCADA market size and forecast often aim to understand the overarching growth drivers and the strategic implications for industry stakeholders. The market is poised for robust expansion, primarily fueled by the global push for industrial automation, the modernization of aging infrastructure, and the increasing adoption of Industry 4.0 principles. The forecast indicates sustained demand for SCADA solutions that offer enhanced connectivity, data analytics, and operational intelligence, driven by the imperative to improve efficiency, reduce operational costs, and ensure business continuity across diverse sectors.

A significant takeaway is the market's resilience and adaptability, particularly in response to evolving technological landscapes and heightened security concerns. The transition towards smarter, more interconnected operational environments emphasizes the value proposition of SCADA as a foundational technology for digital transformation. Companies that strategically invest in advanced SCADA capabilities, particularly those integrating cloud, AI, and robust cybersecurity, are well-positioned to capitalize on this growth trajectory. The market’s upward trend underscores its critical role in supporting efficient and secure operations worldwide.

- Robust and consistent growth trajectory projected through 2033.

- Market expansion driven by escalating demand for industrial automation and smart infrastructure.

- Digitalization initiatives and Industry 4.0 adoption are primary catalysts for growth.

- Significant opportunities in upgrading existing legacy SCADA systems.

- Cybersecurity and data analytics capabilities are becoming critical differentiators.

- Shift towards software-centric and cloud-enabled SCADA solutions for increased agility.

SCADA Market Drivers Analysis

The SCADA market is profoundly influenced by a confluence of drivers that underpin its expansion across various industries. The primary driver is the accelerating global trend towards industrial automation and digitalization, where organizations seek to optimize processes, reduce manual intervention, and enhance overall operational efficiency. This includes the widespread adoption of IoT and Industry 4.0 technologies, which necessitate sophisticated control and monitoring systems like SCADA to manage interconnected devices and leverage vast amounts of real-time data. The imperative for remote monitoring and control, especially post-pandemic, has also significantly propelled the demand for advanced SCADA solutions, enabling operators to manage geographically dispersed assets effectively.

Furthermore, the continuous development and modernization of critical infrastructure, such as smart grids, water treatment facilities, and transportation networks, present substantial growth opportunities for SCADA systems. Governments and private entities are investing heavily in upgrading these systems to improve reliability, enhance security, and meet increasing consumer demands. The stringent regulatory compliance requirements across sectors, particularly in areas like environmental monitoring, safety protocols, and data reporting, also mandate the implementation of robust SCADA systems capable of providing auditable and precise operational data. These factors collectively contribute to the sustained demand and growth of the SCADA market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Automation & Digitalization | +2.1% | Global, particularly North America, Europe, Asia Pacific | Immediate to Long-Term (2025-2033) |

| Modernization of Aging Infrastructure & Smart City Initiatives | +1.8% | North America, Europe, Emerging APAC, MEA | Mid to Long-Term (2027-2033) |

| Growing Adoption of IoT and Industry 4.0 Technologies | +1.5% | Global, especially Manufacturing & Energy Sectors | Immediate to Mid-Term (2025-2029) |

| Enhanced Need for Operational Efficiency & Cost Reduction | +1.3% | Global, across all industrial sectors | Immediate and Ongoing (2025-2033) |

| Rise in Demand for Remote Monitoring & Control Solutions | +1.0% | Global, especially Utilities and Distributed Assets | Immediate to Mid-Term (2025-2028) |

SCADA Market Restraints Analysis

Despite the strong growth drivers, the SCADA market faces several significant restraints that could impede its full potential. One of the primary barriers is the high initial investment cost associated with implementing new SCADA systems, particularly for large-scale industrial operations. This cost includes not only hardware and software but also extensive installation, integration with existing infrastructure, and personnel training, making it prohibitive for some small and medium-sized enterprises (SMEs) or organizations with limited capital budgets. The complexity of integrating modern SCADA solutions with legacy systems, which are prevalent in older industrial facilities, also poses a significant challenge. This integration often requires custom solutions and extensive downtime, increasing both cost and operational risk.

Furthermore, cybersecurity vulnerabilities represent a critical restraint. As SCADA systems become increasingly connected to enterprise networks and the internet, they become more susceptible to sophisticated cyberattacks, including ransomware, data breaches, and industrial espionage. The potential for disruption to critical infrastructure due to a successful cyberattack is immense, making organizations hesitant to adopt advanced, highly networked SCADA solutions without guaranteed robust security. The ongoing shortage of skilled professionals capable of designing, implementing, and maintaining complex SCADA systems, particularly those incorporating advanced analytics and AI, further exacerbates these challenges. These restraints necessitate innovative solutions and strategic planning to ensure broader adoption and market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Implementation Costs | -1.2% | Developing Regions, SMEs Globally | Immediate to Mid-Term (2025-2029) |

| Complexity of Integrating with Legacy Systems | -1.0% | Mature Industrial Economies (North America, Europe) | Ongoing (2025-2033) |

| Persistent Cybersecurity Threats & Vulnerabilities | -0.8% | Global, particularly Critical Infrastructure | Ongoing (2025-2033) |

| Shortage of Skilled Workforce & Technical Expertise | -0.7% | Global, across all sectors | Long-Term (2027-2033) |

| Interoperability and Standardization Issues | -0.5% | Global, especially for multi-vendor environments | Ongoing (2025-2033) |

SCADA Market Opportunities Analysis

Despite existing restraints, the SCADA market is replete with significant opportunities driven by technological innovation and evolving industrial demands. The increasing shift towards cloud-based SCADA solutions presents a tremendous opportunity for vendors. Cloud deployments offer enhanced scalability, flexibility, reduced infrastructure overheads, and improved data accessibility, appealing to organizations looking for more agile and cost-effective operational technology solutions. This trend is particularly relevant for enabling remote operations and facilitating data-driven decision-making from anywhere. Furthermore, the burgeoning potential of integrating Artificial Intelligence (AI) and Machine Learning (ML) into SCADA systems offers a distinct competitive advantage. AI/ML capabilities enable predictive analytics, advanced anomaly detection, and autonomous control, transforming raw operational data into actionable intelligence and leading to unprecedented levels of efficiency and reliability.

Another significant opportunity lies in the expansion of SCADA applications into new vertical markets that have historically been less automated but are now recognizing the benefits of real-time control and monitoring. These include smart agriculture, renewable energy generation (solar and wind farms), and intelligent building management systems. As these sectors mature and seek optimization, the demand for tailored SCADA solutions will rise. Moreover, the focus on developing more resilient and cyber-secure SCADA systems presents an opportunity for manufacturers and service providers to innovate and offer advanced security features, thereby addressing a critical industry concern and building trust. The continuous need for system upgrades and maintenance of existing SCADA installations also creates a recurring revenue stream and market for specialized services.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Cloud-based SCADA Solutions | +1.9% | Global, particularly North America, Europe, APAC | Immediate to Mid-Term (2025-2029) |

| Integration of AI and Machine Learning Capabilities | +1.7% | Global, across high-value industrial assets | Mid to Long-Term (2027-2033) |

| Expansion into New Vertical Markets (e.g., Renewable Energy, Smart Agriculture) | +1.4% | Emerging APAC, Latin America, Europe | Mid to Long-Term (2028-2033) |

| Development of Cyber-Resilient SCADA Systems | +1.1% | Global, especially Critical Infrastructure & Utilities | Immediate and Ongoing (2025-2033) |

| Increased Demand for Data Analytics & Business Intelligence Integration | +0.9% | Global, large enterprises seeking actionable insights | Immediate to Mid-Term (2025-2029) |

SCADA Market Challenges Impact Analysis

The SCADA market, while promising, contends with several significant challenges that necessitate strategic responses from vendors and users alike. Data security and privacy remain paramount concerns. As SCADA systems become more interconnected and data-intensive, protecting sensitive operational data from unauthorized access, manipulation, and cyberattacks is a continuous battle. The sheer volume and velocity of data generated also pose challenges in terms of storage, processing, and analysis, requiring robust infrastructure and advanced analytical tools. Furthermore, ensuring interoperability between diverse SCADA components, protocols, and third-party systems from multiple vendors continues to be a complex hurdle, often leading to vendor lock-in or difficult, expensive integrations.

Another critical challenge is the inherent complexity of modern SCADA systems. Integrating advanced features like AI, IoT, and cloud connectivity into existing operational technology (OT) environments demands sophisticated technical expertise and careful planning, which can be daunting for organizations. This complexity often leads to higher implementation risks, longer deployment times, and increased training requirements for personnel. Moreover, the rapid pace of technological advancements means that SCADA systems require continuous upgrades and maintenance to remain effective and secure, adding to the ongoing operational costs. Addressing these challenges effectively will be crucial for sustained growth and broader adoption of advanced SCADA solutions in the evolving industrial landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Security & Privacy Concerns | -1.1% | Global, Critical Infrastructure, Utilities | Ongoing (2025-2033) |

| Interoperability and Lack of Standardized Protocols | -0.9% | Global, across multi-vendor industrial environments | Ongoing (2025-2033) |

| System Complexity & Integration Difficulties | -0.7% | Global, especially for brownfield deployments | Immediate to Mid-Term (2025-2029) |

| High Cost of Continuous Upgrades & Maintenance | -0.6% | Global, particularly for large-scale implementations | Ongoing (2025-2033) |

| Compliance with Evolving Regulations & Standards | -0.5% | Regional (Europe, North America), Industry-specific | Ongoing (2025-2033) |

SCADA Market - Updated Report Scope

This market research report provides an in-depth, comprehensive analysis of the global SCADA market, offering granular insights into market dynamics, segmentation, and regional landscapes. The report meticulously examines the market size, historical trends, and future growth projections, identifying key drivers, restraints, opportunities, and challenges influencing market expansion. It also includes an extensive competitive analysis, profiling leading companies and their strategic initiatives, alongside a detailed exploration of technological advancements such as AI integration and cloud adoption within SCADA systems. The aim is to provide stakeholders with actionable intelligence for strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 45.6 Billion |

| Market Forecast in 2033 | USD 91.2 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens, Schneider Electric, ABB, Rockwell Automation, Emerson Electric, Honeywell, Yokogawa Electric Corporation, General Electric, Hitachi, Mitsubishi Electric, Fuji Electric, Omron, ICONICS, Inductive Automation, Advantech, Valmet, PTC (Kepware), Efacec, Landis+Gyr, NovaTech LLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The SCADA market is comprehensively segmented to provide a granular understanding of its diverse components and applications, enabling precise market analysis and strategic planning. These segmentations are critical for identifying key growth areas, understanding competitive landscapes, and tailoring solutions to specific industry needs. The market is primarily broken down by component, distinguishing between hardware elements such as RTUs, PLCs, and HMI units, and the crucial software that facilitates data acquisition, processing, and visualization, alongside essential support services. This allows for an analysis of expenditure distribution and technological preferences within the SCADA ecosystem.

Further segmentation by architecture, application, and deployment method provides deeper insights. Architectural segmentation, for instance, highlights the shift from traditional monolithic systems to more flexible networked and cloud-based solutions. Application-based segmentation reveals the pervasive adoption of SCADA across critical industries like oil & gas, power, water, and manufacturing, while also identifying emerging opportunities in sectors such as renewable energy and smart agriculture. Deployment models, whether on-premise or cloud-based, reflect varying preferences for control, security, and scalability. This multi-faceted segmentation ensures a thorough and actionable understanding of the SCADA market's intricate structure and growth dynamics.

- By Component: Hardware (RTUs, PLCs, HMI, Communication Systems), Software (HMI Software, Supervisory Software, Data Historians), Services (Installation, Maintenance, Consulting, Training).

- By Architecture: Monolithic SCADA, Distributed SCADA, Networked SCADA, Cloud-based SCADA.

- By Application/Industry: Oil & Gas, Power & Energy (Generation, Transmission & Distribution), Water & Wastewater Management, Manufacturing (Process Manufacturing, Discrete Manufacturing), Chemicals & Pharmaceuticals, Food & Beverages, Transportation Systems, Mining & Metals, Building Management Systems, Others.

- By Deployment: On-premise, Cloud-based.

Regional Highlights

Regionally, the SCADA market exhibits diverse growth patterns and adoption rates, influenced by industrialization levels, infrastructure development, and technological maturity. North America and Europe currently represent significant market shares, driven by early adoption of automation, ongoing modernization of critical infrastructure, and substantial investments in smart grid technologies and Industry 4.0 initiatives. These regions also have stringent regulatory frameworks that mandate efficient and secure operational control systems, further fueling SCADA demand. The presence of key market players and a robust R&D ecosystem also contributes to their dominance in the SCADA market.

Asia Pacific (APAC) is projected to emerge as the fastest-growing region, propelled by rapid industrialization, increasing governmental investments in smart city projects, and the expansion of manufacturing and energy sectors, particularly in countries like China, India, and Japan. Latin America, the Middle East, and Africa (MEA) are also expected to witness steady growth, albeit from a smaller base, driven by new infrastructure projects, resource exploration activities, and the growing need for efficient utility management. Each region presents unique opportunities and challenges, with localized market dynamics shaping the demand for specific SCADA solutions and services.

- North America: Dominant market share due to advanced industrial infrastructure, high adoption of digital technologies, and significant investments in smart grid and cybersecurity.

- Europe: Strong market presence driven by stringent environmental regulations, smart utility initiatives, and significant automation in manufacturing and energy sectors.

- Asia Pacific (APAC): Fastest-growing region, fueled by rapid industrialization, smart city development, increasing manufacturing activity, and renewable energy projects in China, India, and Southeast Asia.

- Latin America: Emerging market with growth potential stemming from infrastructure development in utilities, oil & gas, and mining sectors.

- Middle East & Africa (MEA): Growing market driven by large-scale infrastructure projects, expansion in oil & gas, and initiatives towards diversifying economies through industrialization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the SCADA Market.- Siemens

- Schneider Electric

- ABB

- Rockwell Automation

- Emerson Electric

- Honeywell

- Yokogawa Electric Corporation

- General Electric

- Hitachi

- Mitsubishi Electric

- Fuji Electric

- Omron

- ICONICS

- Inductive Automation

- Advantech

- Valmet

- PTC (Kepware)

- Efacec

- Landis+Gyr

- NovaTech LLC

Frequently Asked Questions

What is SCADA and its primary function?

SCADA, an acronym for Supervisory Control and Data Acquisition, is a computer-based system used for controlling and monitoring industrial processes across various sectors. Its primary function is to collect real-time data from remote locations, process it, and present it in an easily understandable format to operators. This allows for centralized control and supervision of complex operations, enabling efficient decision-making, automated control, and accurate record-keeping for performance analysis and compliance.

How is SCADA different from DCS (Distributed Control System)?

While both SCADA and DCS are control systems, they differ primarily in scope and architecture. SCADA systems are typically used for large-scale, geographically dispersed processes, often spanning vast distances, focusing on data acquisition and supervisory control. DCS, conversely, is designed for localized, intricate processes within a single facility or plant, providing highly integrated and continuous control over a smaller, more centralized area. SCADA emphasizes remote monitoring and data logging, whereas DCS prioritizes precise, real-time regulatory control within a confined process.

What are the key benefits of implementing SCADA systems?

Implementing SCADA systems offers numerous benefits, including enhanced operational efficiency through automated control and real-time monitoring, leading to significant cost reductions by optimizing resource utilization and minimizing downtime. SCADA improves decision-making capabilities by providing operators with accurate and timely data for informed actions. It also boosts safety and security by enabling rapid detection and response to abnormal conditions, and facilitates regulatory compliance through comprehensive data logging and reporting capabilities.

What are the main challenges facing SCADA adoption?

The SCADA market faces several challenges, notably the high initial investment costs for system implementation and integration, especially with legacy infrastructure. Cybersecurity vulnerabilities pose a significant threat, requiring robust protective measures as systems become more interconnected. Additionally, the complexity of managing and integrating diverse components, coupled with a persistent shortage of skilled professionals, creates hurdles for seamless adoption and optimized operation of advanced SCADA solutions across various industries.

How is cloud computing impacting SCADA systems?

Cloud computing is profoundly impacting SCADA systems by introducing new levels of scalability, flexibility, and remote accessibility. Cloud-based SCADA eliminates the need for extensive on-premise hardware infrastructure, reducing upfront costs and maintenance. It enables operators to monitor and control industrial processes from virtually any location with an internet connection, enhancing operational agility. Furthermore, cloud platforms facilitate advanced data analytics, AI integration, and improved collaboration, transforming how SCADA data is processed, stored, and utilized for intelligent automation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted