Salt Substitute Market

Salt Substitute Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702398 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

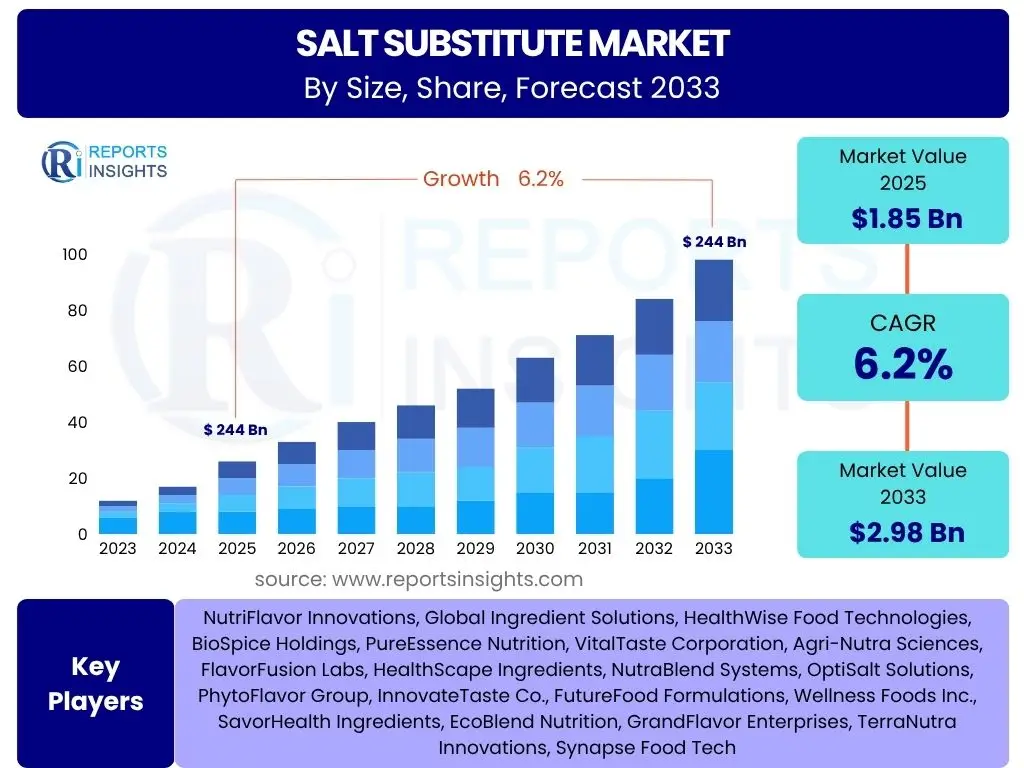

Salt Substitute Market Size

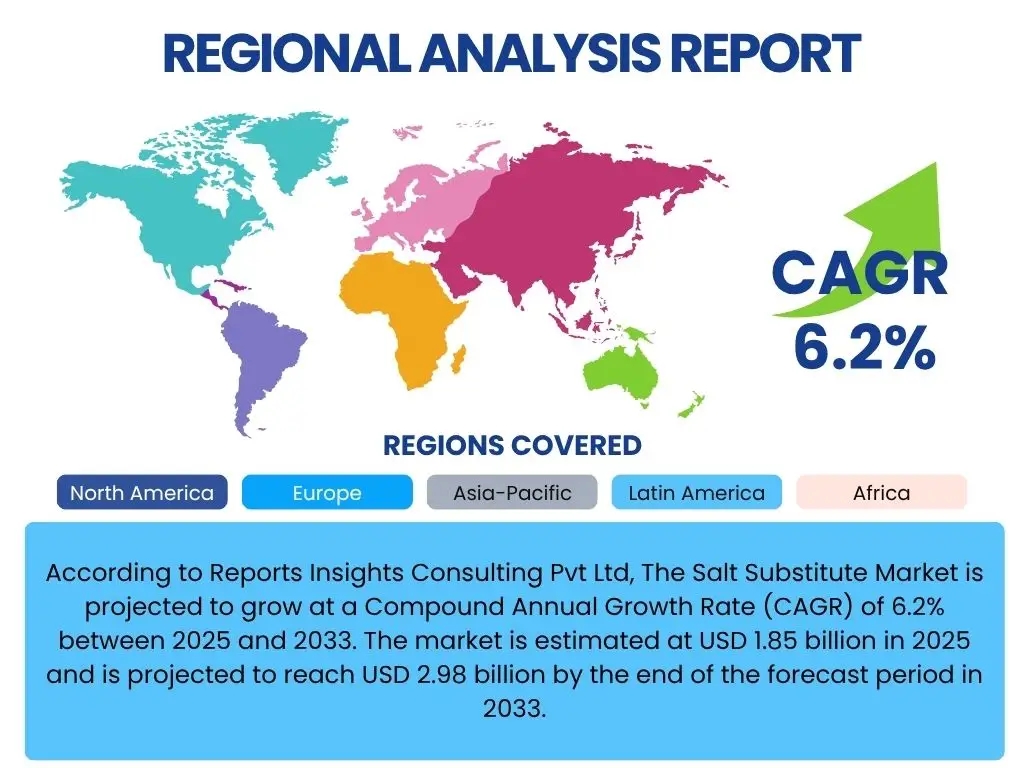

According to Reports Insights Consulting Pvt Ltd, The Salt Substitute Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 1.85 billion in 2025 and is projected to reach USD 2.98 billion by the end of the forecast period in 2033.

Key Salt Substitute Market Trends & Insights

The Salt Substitute market is currently shaped by a confluence of evolving consumer preferences, health-driven regulatory pressures, and advancements in food science. Consumers are increasingly seeking healthier dietary options, particularly those that address cardiovascular health concerns, driving demand for reduced sodium products. This shift is amplified by public health campaigns and nutritional guidelines that emphasize lower sodium intake, compelling food manufacturers to reformulate existing products and develop new ones with healthier profiles. The industry is witnessing a strong trend towards natural, plant-based, and multi-functional ingredient solutions that not only mimic the taste of sodium chloride but also offer additional health benefits.

Technological innovation plays a critical role in overcoming the inherent challenges of taste and texture associated with salt reduction. Companies are investing in research and development to discover novel compounds and ingredient blends that can replicate the functional properties of salt, such as flavor enhancement, preservation, and texture improvement, without compromising palatability. Furthermore, the rising adoption of personalized nutrition approaches and the growing e-commerce penetration are creating new avenues for specialized salt substitute products, catering to niche dietary requirements and delivering directly to consumers. The market is also experiencing a geographical expansion, with strong growth observed in emerging economies where lifestyle diseases linked to diet are on the rise.

- Increasing consumer awareness regarding the health risks of high sodium intake.

- Rising prevalence of hypertension and cardiovascular diseases globally.

- Growing demand for clean label and natural ingredient solutions in food products.

- Technological advancements in flavor science to improve taste profiles of salt substitutes.

- Stringent government regulations and health guidelines promoting sodium reduction.

- Expansion of product applications across various food and beverage categories.

- Surge in demand for plant-based and potassium-rich salt alternative solutions.

- Shift towards personalized nutrition driving demand for tailored low-sodium options.

AI Impact Analysis on Salt Substitute

The integration of Artificial intelligence (AI) is beginning to profoundly influence the Salt Substitute market, primarily through accelerating research and development, optimizing supply chains, and enhancing personalized consumer experiences. AI-driven computational chemistry and bioinformatics are proving invaluable in identifying novel compounds and complex ingredient combinations that effectively mimic salt's sensory attributes while maintaining desired functional properties. This significantly reduces the time and cost traditionally associated with flavor and ingredient discovery, allowing for more rapid iteration and formulation of advanced salt substitutes. Furthermore, AI algorithms can analyze vast datasets of consumer preferences and dietary patterns, enabling manufacturers to predict demand more accurately and tailor product development to specific market needs and regional tastes.

Beyond product innovation, AI's capabilities are extending to manufacturing and distribution processes within the salt substitute industry. Predictive analytics and machine learning models are optimizing production schedules, minimizing waste, and ensuring the efficient procurement of raw materials, thereby enhancing operational efficiency and cost-effectiveness. In terms of consumer engagement, AI-powered platforms can provide personalized dietary recommendations, tracking individual sodium intake and suggesting suitable salt substitute products based on health goals and taste preferences. This level of customization and data-driven insight represents a significant shift, allowing companies to foster deeper relationships with consumers and develop highly targeted marketing strategies for low-sodium solutions. While still in nascent stages, the long-term impact of AI is anticipated to revolutionize the speed of innovation and the precision of market targeting within this sector.

- Accelerated R&D: AI expedites the discovery of novel salt-mimicking compounds and blends.

- Enhanced Formulation: AI tools optimize ingredient ratios for improved taste and texture.

- Predictive Analytics: AI forecasts consumer preferences and market demand for low-sodium products.

- Supply Chain Optimization: AI improves raw material sourcing, inventory management, and logistics efficiency.

- Personalized Nutrition: AI enables customized dietary recommendations and product suggestions for sodium reduction.

- Quality Control: AI-powered systems ensure consistent product quality and compliance.

- Market Trend Analysis: AI identifies emerging dietary trends and regional taste preferences for strategic product development.

Key Takeaways Salt Substitute Market Size & Forecast

The Salt Substitute market is poised for robust growth, driven primarily by an escalating global awareness of the health implications of high sodium consumption and the proactive efforts by governments and health organizations to promote healthier dietary habits. The forecasted CAGR of 6.2% from 2025 to 2033 reflects a sustained and increasing demand for healthier food options, positioning salt substitutes as a crucial component in the reformulation strategies of food manufacturers worldwide. This growth is not merely incremental but indicative of a fundamental shift in consumer behavior towards preventative health measures and a willingness to embrace alternative ingredients that do not compromise on taste or quality.

Key takeaways from the market forecast underscore the significant opportunities for innovation and market penetration. The projected increase in market value from USD 1.85 billion to USD 2.98 billion signifies substantial investment potential in advanced ingredient technologies, flavor enhancers, and product development across diverse food applications. This expansion will necessitate continuous research into novel, natural, and multi-functional substitutes that can effectively replicate salt’s various roles, including preservation and texture. Furthermore, the forecast highlights the importance of strategic partnerships between ingredient suppliers and food manufacturers to accelerate product development and ensure widespread availability, ultimately contributing to improved public health outcomes globally.

- Significant market expansion expected, reflecting strong health consciousness trends.

- Steady CAGR of 6.2% indicates consistent demand for healthier sodium alternatives.

- Total market valuation projected to reach USD 2.98 billion by 2033, demonstrating substantial growth potential.

- Innovation in taste and functionality remains crucial for market adoption and consumer acceptance.

- Increasing regulatory pressure globally to reduce sodium content in processed foods will fuel market growth.

- Strong opportunities for new product development across various food categories, including snacks, processed foods, and ready meals.

Salt Substitute Market Drivers Analysis

The Salt Substitute market is predominantly driven by the surging global health concerns related to excessive sodium intake, primarily the rising incidence of hypertension and cardiovascular diseases. Public health initiatives and dietary guidelines from organizations such as the World Health Organization (WHO) and national health bodies are continually advocating for reduced sodium consumption, placing immense pressure on food manufacturers to reformulate products. This regulatory push, combined with an increasingly health-conscious consumer base, creates a powerful impetus for the adoption and development of innovative salt substitutes.

Furthermore, technological advancements in food science and ingredient development are enabling the creation of more effective and palatable salt substitutes, addressing historical challenges related to taste and functionality. Innovations in potassium chloride blends, yeast extracts, and natural flavor enhancers are making it easier for manufacturers to reduce sodium without compromising sensory appeal. The diversification of product applications, from processed foods and snacks to sauces and ready meals, further expands the market reach. As consumers actively seek healthier food choices and are more informed about nutritional labels, the demand for low-sodium and salt-reduced products will continue to grow, solidifying these drivers as fundamental to market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Incidence of Hypertension & CVD | +1.8% | Global, particularly North America, Europe, Asia Pacific | Long-term (5+ years) |

| Increasing Consumer Health Awareness & Demand for Healthy Foods | +1.5% | Global, especially Developed Economies | Medium-term (3-5 years) |

| Government Regulations & Public Health Initiatives on Sodium Reduction | +1.2% | North America, Europe, China, India | Medium-term (3-5 years) |

| Technological Advancements in Taste Masking & Flavor Enhancement | +0.8% | Global (R&D Hubs in North America, Europe) | Short to Medium-term (1-5 years) |

| Expansion of Product Applications in Food & Beverage Industry | +0.9% | Global, particularly Processed Food Markets | Short to Medium-term (1-5 years) |

Salt Substitute Market Restraints Analysis

Despite significant growth drivers, the Salt Substitute market faces several notable restraints that could impede its full potential. A primary challenge is consumer perception and acceptance, particularly regarding taste. Many consumers are accustomed to the distinct flavor profile of sodium chloride, and salt substitutes often struggle to replicate this exact taste and mouthfeel without introducing metallic notes or other off-flavors. This can lead to consumer dissatisfaction and reluctance to adopt low-sodium products, limiting broader market penetration. Manufacturers must continually invest in advanced flavor technologies to overcome these sensory hurdles and ensure product palatability.

Another significant restraint is the cost of formulation. While potassium chloride is a widely used and relatively inexpensive substitute, developing complex blends that mimic salt's full functionality—including preservation and texture enhancement—can be more expensive than using traditional salt. This higher cost may translate to increased product prices, potentially deterring price-sensitive consumers or creating a barrier for manufacturers operating on thin margins. Furthermore, regulatory complexities surrounding labeling and ingredient approval for novel salt substitutes in different regions can create compliance challenges and extend time-to-market for new products, adding to development costs and hindering innovation.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Taste Perception & Off-flavors Associated with Substitutes | -0.9% | Global | Long-term (5+ years) |

| Higher Cost of Formulation Compared to Sodium Chloride | -0.7% | Global, especially Emerging Markets | Medium-term (3-5 years) |

| Consumer Skepticism & Lack of Awareness of Benefits | -0.5% | Global, particularly Less Developed Regions | Medium-term (3-5 years) |

| Regulatory Hurdles & Approval Processes for New Ingredients | -0.4% | Europe, North America | Short to Medium-term (1-5 years) |

| Limited Functionality of Some Substitutes in Specific Applications | -0.3% | Global | Short-term (1-3 years) |

Salt Substitute Market Opportunities Analysis

Significant opportunities exist in the Salt Substitute market, primarily driven by continuous innovation in ingredient science and the expansion into underserved product categories. The development of advanced, multi-functional salt alternatives that offer not only sodium reduction but also enhanced flavor, improved texture, and potential health benefits (e.g., potassium enrichment, natural antioxidants) presents a major growth avenue. Research into natural sources, such as seaweed extracts, mushroom powders, and savory yeast derivatives, can cater to the growing clean label and plant-based consumer segments. Furthermore, leveraging micro-encapsulation technologies and flavor delivery systems can overcome taste challenges and ensure a consistent flavor profile, making these substitutes more appealing for widespread adoption across various food applications.

Geographical expansion into emerging markets, particularly in Asia Pacific and Latin America, represents another substantial opportunity. As these regions experience rising disposable incomes, urbanization, and increasing prevalence of lifestyle diseases, demand for healthier food options, including low-sodium products, is set to surge. Collaborations between ingredient manufacturers and large food corporations can facilitate the integration of salt substitutes into mainstream product lines, ensuring broader market penetration. Additionally, the personalized nutrition trend offers a niche opportunity for highly customized salt substitute solutions, catering to specific dietary needs or health conditions, and delivered through direct-to-consumer models or specialized health platforms, allowing for premium product offerings and tailored consumer engagement.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Innovation in Natural & Multi-functional Salt Alternatives | +1.1% | Global (Focus on Developed Markets) | Long-term (5+ years) |

| Expansion into Emerging Markets & Developing Economies | +1.0% | Asia Pacific, Latin America, MEA | Medium to Long-term (3-7 years) |

| Increased Adoption in Food Service & Industrial Applications | +0.8% | North America, Europe | Medium-term (3-5 years) |

| Growing Demand for Personalized Nutrition Solutions | +0.7% | North America, Europe, Australia | Short to Medium-term (1-5 years) |

| Strategic Partnerships & Collaborations Across Value Chain | +0.6% | Global | Short to Medium-term (1-5 years) |

Salt Substitute Market Challenges Impact Analysis

The Salt Substitute market faces several critical challenges that can hinder its growth and wider adoption. A significant hurdle is the complexity of replicating the complete sensory and functional profile of sodium chloride. Salt provides not only a distinct taste but also plays vital roles in food preservation, texture development, and overall mouthfeel, which are difficult to replicate perfectly with substitutes. Achieving this balance while ensuring cost-effectiveness and clean-label appeal requires extensive research and development, often leading to prolonged product development cycles and higher investment costs for manufacturers.

Another challenge stems from consumer education and overcoming ingrained dietary habits. Many consumers are unaware of the health benefits of reducing sodium or are resistant to changes in the taste of their favorite foods. Public health campaigns and industry efforts are needed to effectively communicate the advantages of salt substitutes and build consumer trust. Furthermore, the variability in regulatory standards across different countries concerning the allowed levels of certain salt substitutes (e.g., potassium chloride) and labeling requirements can create market fragmentation and compliance complexities for global players, complicating product distribution and market entry strategies. Navigating these challenges requires continuous innovation, effective communication, and adaptive market strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Replicating Full Sensory & Functional Profile of Salt | -0.8% | Global | Long-term (5+ years) |

| Consumer Education & Overcoming Behavioral Resistance | -0.6% | Global, especially developing regions | Medium to Long-term (3-7 years) |

| Navigating Diverse & Evolving Regulatory Landscapes | -0.5% | Europe, North America, Asia Pacific | Medium-term (3-5 years) |

| Ensuring Supply Chain Stability & Raw Material Sourcing | -0.4% | Global | Short to Medium-term (1-5 years) |

| Competitive Pressure from Traditional Sodium Reduction Methods | -0.3% | Global | Short-term (1-3 years) |

Salt Substitute Market - Updated Report Scope

This comprehensive market research report on the Salt Substitute Market provides a detailed analysis of market dynamics, including growth drivers, restraints, opportunities, and challenges. It offers in-depth insights into market segmentation by type, application, and form, providing a granular view of various sub-segments. The report also covers regional market analysis, highlighting key trends and opportunities across major geographies. A competitive landscape section profiles key industry players, offering insights into their strategies, product portfolios, and recent developments. The scope extends to an impact analysis of emerging technologies like Artificial Intelligence on market evolution, providing a forward-looking perspective for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.98 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NutriFlavor Innovations, Global Ingredient Solutions, HealthWise Food Technologies, BioSpice Holdings, PureEssence Nutrition, VitalTaste Corporation, Agri-Nutra Sciences, FlavorFusion Labs, HealthScape Ingredients, NutraBlend Systems, OptiSalt Solutions, PhytoFlavor Group, InnovateTaste Co., FutureFood Formulations, Wellness Foods Inc., SavorHealth Ingredients, EcoBlend Nutrition, GrandFlavor Enterprises, TerraNutra Innovations, Synapse Food Tech |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Salt Substitute market is comprehensively segmented to provide a granular understanding of its diverse components and evolving dynamics. These segmentations are critical for identifying specific growth pockets, tailoring product development, and devising effective market entry strategies. Analysis by type reveals the dominance of potassium chloride due to its efficacy and cost-effectiveness, alongside a growing interest in natural alternatives like yeast extracts and herb blends. Understanding consumer preferences and technological advancements within each type segment is crucial for ingredient suppliers and food manufacturers.

Furthermore, segmenting by application highlights the significant adoption of salt substitutes in processed foods, including snacks, bakery items, and ready meals, driven by reformulation efforts to meet health regulations and consumer demand. The increasing penetration into the food service sector and the household segment also indicates broader acceptance and awareness. Form-based segmentation (powder, granular, liquid) reflects the versatility required for different manufacturing processes and end-user applications. This multi-faceted segmentation allows stakeholders to target specific market niches with precision, optimizing resource allocation and maximizing market share in a highly competitive landscape.

- By Type

- Potassium Chloride

- Yeast Extracts

- Herbs & Spices

- Other Mineral Salts (e.g., Magnesium Sulfate, Calcium Chloride)

- Other Natural Flavor Enhancers

- By Application

- Processed Foods

- Bakery Products

- Snacks

- Soups & Sauces

- Dairy & Frozen Products

- Meat & Poultry Products

- Food Service

- Household

- Processed Foods

- By Form

- Powder

- Granular

- Liquid

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

Regional Highlights

- North America: This region is a leading market, driven by high prevalence of lifestyle diseases, strong consumer health awareness, and stringent government regulations for sodium reduction in processed foods. The U.S. and Canada show robust demand for innovative salt substitute solutions and clean label ingredients.

- Europe: Europe represents a significant market, influenced by well-established health initiatives, sophisticated food safety standards, and a consumer base increasingly seeking healthier food options. Countries like the UK, Germany, and France are at the forefront of adopting salt-reduced food products and new ingredient technologies.

- Asia Pacific (APAC): Expected to be the fastest-growing region, propelled by rising disposable incomes, rapid urbanization, changing dietary habits, and increasing health consciousness, particularly in populous countries like China and India. Government efforts to combat diet-related health issues are also fueling market expansion.

- Latin America: This region is demonstrating steady growth due to rising awareness of hypertension and cardiovascular diseases, coupled with growing investments in the food processing sector. Brazil and Mexico are key contributors to the regional market.

- Middle East and Africa (MEA): The MEA region is an emerging market for salt substitutes, with increasing health awareness, a growing processed food industry, and initiatives to address non-communicable diseases. Demand is gradually increasing, particularly in urban centers.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Salt Substitute Market.- NutriFlavor Innovations

- Global Ingredient Solutions

- HealthWise Food Technologies

- PureEssence Nutrition

- OptiSalt Solutions

Frequently Asked Questions

What is the primary purpose of salt substitutes?

Salt substitutes are designed to reduce the sodium content in food products and diets, primarily to mitigate health risks such as hypertension and cardiovascular diseases, while aiming to maintain taste and functional properties similar to traditional salt.

What are the main types of salt substitutes available?

The main types include potassium chloride, yeast extracts, blends of herbs and spices, other mineral salts like magnesium sulfate and calcium chloride, and various natural flavor enhancers that contribute savory notes without high sodium.

How is AI impacting the salt substitute industry?

AI is accelerating research and development by identifying new compounds and optimal ingredient blends, enhancing supply chain efficiency through predictive analytics, and enabling personalized nutrition recommendations for consumers seeking low-sodium options.

What are the biggest challenges for the salt substitute market?

Key challenges include replicating the complete taste and functional profile of salt, overcoming consumer skepticism and ingrained taste preferences, managing higher production costs, and navigating complex and varied global regulatory landscapes.

Which regions are expected to show significant growth in the salt substitute market?

North America and Europe are mature but growing markets, while Asia Pacific, particularly countries like China and India, is projected to exhibit the fastest growth due to increasing health awareness, urbanization, and changing dietary patterns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted