Round Aluminum Slug Market

Round Aluminum Slug Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707543 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

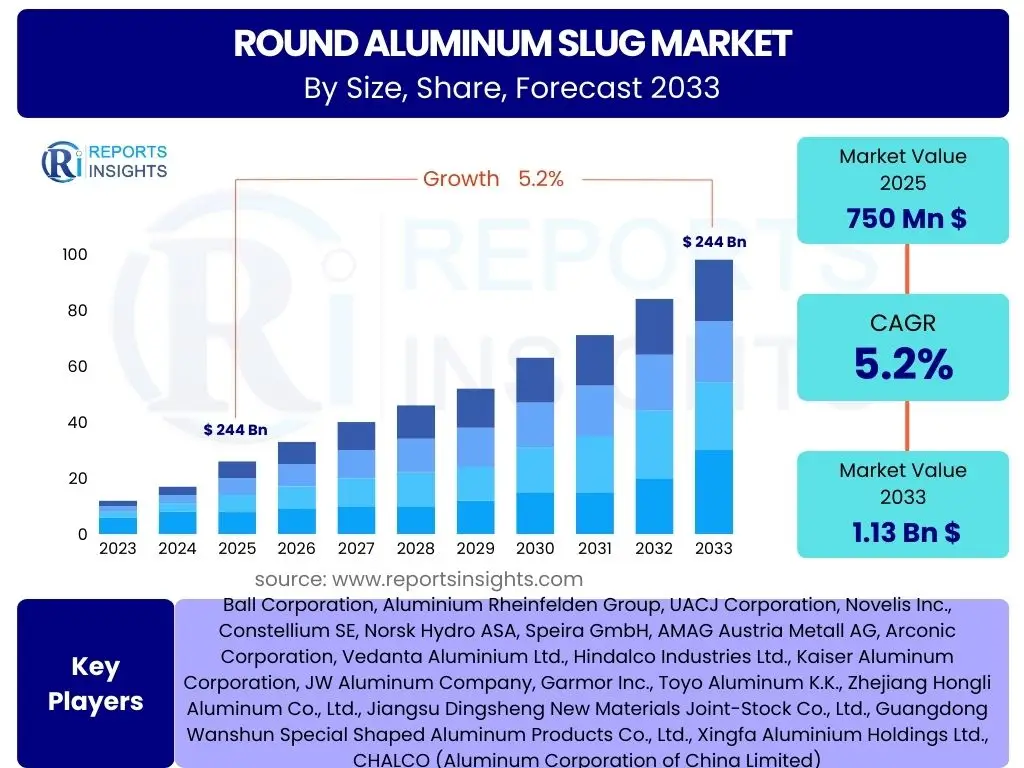

Round Aluminum Slug Market Size

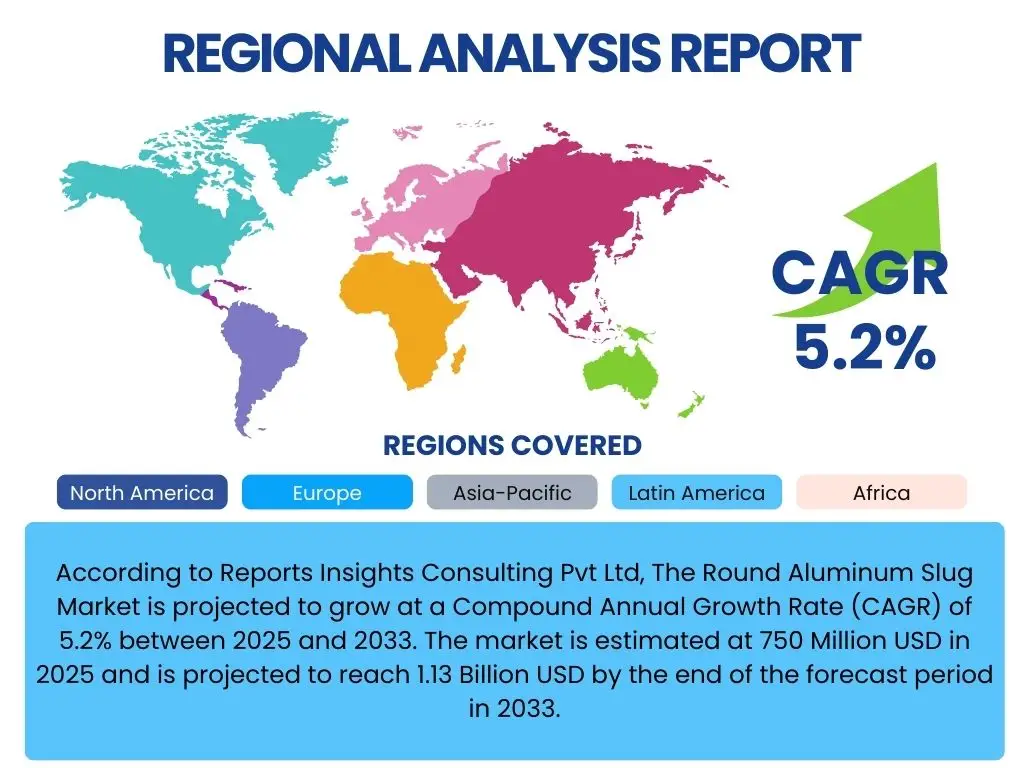

According to Reports Insights Consulting Pvt Ltd, The Round Aluminum Slug Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% between 2025 and 2033. The market is estimated at 750 Million USD in 2025 and is projected to reach 1.13 Billion USD by the end of the forecast period in 2033.

Key Round Aluminum Slug Market Trends & Insights

The global Round Aluminum Slug market is currently experiencing significant shifts driven by evolving consumer preferences, industrial advancements, and increasing regulatory scrutiny. A primary trend observed is the surging demand for sustainable and recyclable packaging solutions, positioning aluminum slugs as a preferred material for various applications. This push towards environmental responsibility is compelling manufacturers across diverse sectors, including cosmetics, pharmaceuticals, and food and beverage, to opt for aluminum over less sustainable alternatives like plastics, thereby directly influencing the demand for slugs.

Furthermore, the automotive industry's continuous pursuit of lightweighting to enhance fuel efficiency and reduce emissions is bolstering the application of aluminum in structural components, where slugs can serve as precursors for specialized parts. Innovations in aluminum alloy compositions are also contributing to this trend, offering improved strength-to-weight ratios and enhanced formability, which broadens the scope of applications for slugs beyond traditional packaging. The expansion of emerging economies and rising disposable incomes are fueling the consumption of products packaged in aluminum, particularly aerosol cans and collapsible tubes, which are primary end-uses for round aluminum slugs.

Technological advancements in manufacturing processes, such as improved extrusion techniques and enhanced quality control systems, are leading to the production of higher quality and more uniformly sized aluminum slugs. This consistency is crucial for automated production lines of end-use products, minimizing waste and improving overall efficiency. The integration of advanced analytics and smart manufacturing principles is also optimizing production cycles, from raw material sourcing to final product delivery, further shaping the operational landscape for aluminum slug manufacturers.

- Increased demand for sustainable and recyclable packaging solutions.

- Growth in automotive lightweighting initiatives.

- Advancements in aluminum alloy compositions and manufacturing processes.

- Expansion of aerosol can and collapsible tube markets in emerging economies.

- Adoption of smart manufacturing and automation in slug production.

AI Impact Analysis on Round Aluminum Slug

Artificial Intelligence (AI) is progressively influencing various facets of the manufacturing and supply chain sectors, and its implications for the Round Aluminum Slug market are becoming increasingly apparent. One significant impact is in optimizing production processes. AI-powered systems can analyze vast amounts of data from manufacturing lines, identifying patterns and anomalies that human operators might miss. This leads to predictive maintenance, reducing downtime by anticipating equipment failures, and enhancing the precision of slug production, ensuring consistent quality, diameter, and surface finish. Such optimization directly translates to reduced waste material and increased operational efficiency, positively affecting profit margins for manufacturers.

Furthermore, AI plays a crucial role in demand forecasting and supply chain management within the aluminum slug ecosystem. By leveraging machine learning algorithms, companies can analyze market trends, consumer behavior, and macroeconomic indicators with greater accuracy, predicting future demand for aluminum slugs. This enables more efficient inventory management, minimizing overstocking or stockouts, and optimizing logistics routes for raw materials and finished products. The ability to react swiftly to market fluctuations and supply chain disruptions through AI-driven insights enhances resilience and responsiveness across the entire value chain.

Beyond operational efficiencies, AI can also accelerate innovation in material science relevant to aluminum slugs. Machine learning models can be used to simulate and predict the properties of new aluminum alloys, reducing the time and cost associated with traditional trial-and-error methods in research and development. This capability allows for the faster development of specialized slugs tailored for specific high-performance applications, such as advanced battery casings or aerospace components. The long-term implications involve a more adaptive and technologically advanced Round Aluminum Slug market, capable of meeting evolving industry demands with precision and sustainability.

- Optimization of manufacturing processes through predictive maintenance and quality control.

- Enhanced demand forecasting and supply chain management for improved inventory and logistics.

- Acceleration of material science research and development for new aluminum alloys.

- Increased operational efficiency and reduction in material waste.

- Improved resilience and responsiveness to market fluctuations.

Key Takeaways Round Aluminum Slug Market Size & Forecast

The Round Aluminum Slug market is poised for robust expansion over the forecast period, driven by fundamental shifts in global manufacturing and consumer preferences. The projected growth indicates a healthy demand for aluminum as a primary material, particularly within the packaging and automotive sectors. This sustained growth trajectory is a clear signal of aluminum slugs' integral role in modern industrial applications, reflecting their versatility, recyclability, and performance advantages over alternative materials. Market players should recognize this underlying strength and align their strategies to capitalize on the increasing adoption of aluminum solutions.

A significant takeaway is the market's resilience to external pressures, largely due to its foundational applications in essential consumer goods and critical industrial components. While raw material price volatility and regulatory landscapes present ongoing challenges, the inherent benefits of aluminum slugs, such as their lightweight properties, barrier capabilities, and infinitely recyclable nature, continue to drive their preference. The forecast underscores that investment in sustainable production methods and innovation in alloy development will be key differentiators for companies aiming to secure a competitive edge and expand their market share.

Furthermore, the market's future growth is heavily reliant on technological integration and regional market dynamics. Emerging economies, with their expanding industrial bases and rising consumer class, are expected to contribute significantly to demand. The emphasis on high-precision manufacturing, enabled by advanced technologies, will ensure the production of high-quality slugs that meet stringent industry standards. Overall, the market's growth forecast underscores a positive outlook, where strategic investments in capacity expansion, technological upgrades, and sustainable practices will yield substantial returns for stakeholders.

- Market size projected to reach 1.13 Billion USD by 2033 with a CAGR of 5.2%.

- Strong demand from packaging (aerosol cans, collapsible tubes) and automotive industries.

- Sustainability and recyclability of aluminum are key growth drivers.

- Technological advancements in production are crucial for market competitiveness.

- Emerging economies are pivotal to future market expansion.

Round Aluminum Slug Market Drivers Analysis

The increasing global emphasis on sustainable packaging solutions is a primary driver for the Round Aluminum Slug market. As consumers and regulations increasingly push for environmentally friendly alternatives, aluminum, with its high recyclability and lightweight properties, stands out as an ideal material. This shift is particularly evident in the food and beverage, pharmaceutical, and personal care industries, where manufacturers are actively replacing plastic and glass containers with aluminum equivalents, thus stimulating demand for slugs as the foundational component for these packaging formats.

Another significant driver stems from the robust growth in the aerosol can and collapsible tube industries. Aerosol cans are widely used for personal care products, household goods, and industrial applications, while collapsible tubes are essential for creams, pastes, and adhesives. The expansion of these end-use sectors, especially in developing regions due to urbanization and rising disposable incomes, directly translates into higher demand for round aluminum slugs, which are the primary raw material for manufacturing these products.

Furthermore, the automotive industry's continuous efforts to reduce vehicle weight to improve fuel efficiency and lower emissions contribute substantially to the market. Aluminum is increasingly replacing heavier materials like steel in various automotive components. While not always directly in slug form, the overall trend towards aluminum usage in automotive manufacturing indirectly supports the demand for primary aluminum products, including slugs for specialized parts or as a broader indicator of aluminum's growing industrial acceptance and application expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for sustainable packaging | +1.5% | Global, particularly Europe and North America | 2025-2033 |

| Expansion of aerosol and collapsible tube industries | +1.2% | Asia Pacific, Latin America, Europe | 2025-2033 |

| Increasing adoption of lightweight materials in automotive | +0.8% | North America, Europe, China | 2025-2030 |

| Urbanization and rising disposable incomes in emerging markets | +1.0% | Asia Pacific, Africa, Latin America | 2025-2033 |

Round Aluminum Slug Market Restraints Analysis

The significant volatility in aluminum raw material prices poses a notable restraint on the Round Aluminum Slug market. Aluminum is a globally traded commodity, and its price is subject to fluctuations driven by geopolitical events, supply-demand imbalances, and energy costs. These price swings directly impact the production costs of aluminum slugs, making it challenging for manufacturers to maintain stable profit margins and competitive pricing, which can deter potential buyers or push them towards alternative, more stable-priced materials.

Intense competition from alternative packaging materials, such as plastics, glass, and composites, also acts as a restraint. While aluminum offers distinct advantages in recyclability and barrier properties, these alternative materials often present lower initial costs or specific functional benefits that appeal to certain industries or product types. Continuous innovation in these alternative materials, improving their performance or cost-effectiveness, can divert demand away from aluminum slugs, particularly in price-sensitive markets.

Furthermore, stringent environmental regulations on aluminum production, particularly concerning energy consumption and carbon emissions, present a challenge. The smelting of aluminum is an energy-intensive process, and increasing pressure to reduce industrial carbon footprints can lead to higher operational costs for primary aluminum producers, which then cascades down to slug manufacturers. Compliance with these regulations may require significant investments in cleaner technologies or carbon offsets, potentially impacting the overall cost-competitiveness of aluminum slugs in the market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of aluminum raw material prices | -0.9% | Global | 2025-2033 |

| Competition from alternative packaging materials | -0.7% | Global, particularly in emerging markets | 2025-2033 |

| High energy consumption and environmental regulations in aluminum production | -0.5% | Europe, North America, China | 2025-2033 |

Round Aluminum Slug Market Opportunities Analysis

The increasing focus on circular economy principles and enhanced recycling infrastructure presents a significant opportunity for the Round Aluminum Slug market. As governments and industries worldwide prioritize sustainability, the demand for materials that can be infinitely recycled without loss of quality, like aluminum, is set to grow. Investments in advanced sorting and recycling technologies will enable a more efficient recovery of aluminum scrap, which can then be repurposed into new slugs, reducing reliance on primary aluminum production and improving the environmental footprint of the industry.

Expansion into new application areas beyond traditional packaging offers substantial growth opportunities. While aerosol cans and collapsible tubes remain core markets, there is potential for aluminum slugs in emerging fields such as battery casings for electric vehicles, specialized electronic components, and high-performance industrial parts. As technologies evolve and miniaturization trends continue, the unique properties of aluminum, including its conductivity, corrosion resistance, and lightweight nature, make slugs an attractive material for innovative product designs, opening up new revenue streams.

Furthermore, the rapid industrialization and urbanization in emerging economies, particularly in Asia Pacific and Latin America, present vast untapped market potential. Rising middle-class populations in these regions are driving increased consumption of packaged goods, personal care products, and automotive components. As manufacturing capabilities expand and consumer spending power grows, the demand for aluminum slugs as a versatile and reliable material for these diverse applications is expected to surge, offering manufacturers opportunities for market penetration and capacity expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in circular economy and recycling initiatives | +1.3% | Global | 2025-2033 |

| Expansion into new applications (e.g., EV battery casings) | +1.0% | Global, particularly advanced economies | 2027-2033 |

| Untapped market potential in emerging economies | +1.1% | Asia Pacific, Latin America, Africa | 2025-2033 |

Round Aluminum Slug Market Challenges Impact Analysis

One of the primary challenges facing the Round Aluminum Slug market is the complexity and potential for disruption within the global supply chain. The production of aluminum slugs relies on a continuous supply of primary aluminum, which often originates from a limited number of major producing regions. Geopolitical tensions, trade disputes, natural disasters, or pandemics can significantly disrupt the flow of raw materials, leading to supply shortages, increased lead times, and inflated costs. This vulnerability makes strategic sourcing and diversification of suppliers critical, yet challenging, for manufacturers.

Maintaining stringent quality control and achieving consistent product specifications across large-scale production runs is another significant challenge. Round aluminum slugs must meet precise dimensions, surface finishes, and metallurgical properties to function optimally in high-speed manufacturing processes for end products like aerosol cans or collapsible tubes. Any deviation can lead to defects in the final product, resulting in waste, customer dissatisfaction, and potential financial losses. Achieving this level of consistency requires significant investment in advanced manufacturing technologies, skilled labor, and rigorous quality assurance protocols.

Furthermore, the escalating energy costs, particularly for electricity, pose a considerable challenge to the aluminum slug manufacturing industry. The production of aluminum from bauxite through electrolysis is highly energy-intensive, making energy prices a major component of operational expenditures. Fluctuating energy markets or rising electricity tariffs can directly erode profit margins for slug manufacturers and affect their competitiveness against producers in regions with access to cheaper energy sources. This necessitates continuous efforts towards energy efficiency and exploring renewable energy options, which often require substantial capital expenditure.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply chain disruptions and raw material availability | -0.8% | Global | 2025-2030 |

| Maintaining stringent quality control and product consistency | -0.6% | Global | 2025-2033 |

| Volatile and increasing energy costs | -0.7% | Europe, Asia Pacific | 2025-2033 |

Round Aluminum Slug Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Round Aluminum Slug market, offering critical insights into its current state, historical performance, and future growth prospects. It encompasses a detailed examination of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry. The scope extends to a meticulous segmentation analysis by application, alloy type, and end-use industry, alongside a thorough regional assessment to pinpoint key growth areas and market dynamics worldwide. The report also profiles leading industry players, providing a competitive landscape and strategic insights for stakeholders. Designed to inform strategic decision-making, it integrates advanced market forecasting methodologies to project market trajectory through 2033, serving as an invaluable resource for investors, manufacturers, and industry participants.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | 750 Million USD |

| Market Forecast in 2033 | 1.13 Billion USD |

| Growth Rate | 5.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ball Corporation, Aluminium Rheinfelden Group, UACJ Corporation, Novelis Inc., Constellium SE, Norsk Hydro ASA, Speira GmbH, AMAG Austria Metall AG, Arconic Corporation, Vedanta Aluminium Ltd., Hindalco Industries Ltd., Kaiser Aluminum Corporation, JW Aluminum Company, Garmor Inc., Toyo Aluminum K.K., Zhejiang Hongli Aluminum Co., Ltd., Jiangsu Dingsheng New Materials Joint-Stock Co., Ltd., Guangdong Wanshun Special Shaped Aluminum Products Co., Ltd., Xingfa Aluminium Holdings Ltd., CHALCO (Aluminum Corporation of China Limited) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Round Aluminum Slug market is comprehensively segmented to provide a granular understanding of its diverse applications, material types, and end-use industries, enabling stakeholders to identify precise growth avenues. This detailed segmentation highlights the dominant market sectors and emerging niches, showcasing how different product attributes cater to specific industrial requirements. Understanding these segments is crucial for manufacturers to tailor their product offerings, optimize production capabilities, and focus marketing efforts on the most promising areas of demand, thereby maximizing their market penetration and profitability.

- By Application: Aerosol Cans, Collapsible Tubes, Battery Casings, Other Industrial Applications.

- By Alloy Type: 1050 Series, 1070 Series, 6061 Series, Other Alloys.

- By End-Use Industry: Packaging, Automotive, Electronics, Pharmaceuticals, Cosmetics, Industrial.

- By Diameter/Size: Small (up to 20mm), Medium (20mm-40mm), Large (above 40mm).

Regional Highlights

- Asia Pacific: Expected to dominate the market due to rapid industrialization, increasing disposable incomes, and the expansion of the packaging, automotive, and electronics manufacturing sectors in countries like China, India, and Southeast Asian nations. This region benefits from a large consumer base and significant investments in manufacturing capabilities.

- Europe: A mature market characterized by stringent environmental regulations driving the adoption of recyclable packaging and strong demand from established cosmetic, pharmaceutical, and household product industries. Focus on sustainability and high-quality product manufacturing sustains regional demand.

- North America: Exhibits stable demand, propelled by the personal care and pharmaceutical industries, alongside continued efforts in automotive lightweighting. The region is also at the forefront of adopting advanced manufacturing technologies and sustainable practices.

- Latin America: An emerging market with significant growth potential, driven by improving economic conditions, urbanization, and increasing consumption of packaged goods and personal care products. Brazil and Mexico are key contributors to regional demand.

- Middle East and Africa (MEA): Projected to show steady growth due to infrastructure development, rising living standards, and increasing investments in manufacturing and packaging industries. The growing demand for consumer goods and pharmaceuticals contributes to market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Round Aluminum Slug Market.- Ball Corporation

- Aluminium Rheinfelden Group

- UACJ Corporation

- Novelis Inc.

- Constellium SE

- Norsk Hydro ASA

- Speira GmbH

- AMAG Austria Metall AG

- Arconic Corporation

- Vedanta Aluminium Ltd.

- Hindalco Industries Ltd.

- Kaiser Aluminum Corporation

- JW Aluminum Company

- Garmor Inc.

- Toyo Aluminum K.K.

- Zhejiang Hongli Aluminum Co., Ltd.

- Jiangsu Dingsheng New Materials Joint-Stock Co., Ltd.

- Guangdong Wanshun Special Shaped Aluminum Products Co., Ltd.

- Xingfa Aluminium Holdings Ltd.

- CHALCO (Aluminum Corporation of China Limited)

Frequently Asked Questions

What is a Round Aluminum Slug and its primary uses?

A Round Aluminum Slug is a solid, cylindrical piece of aluminum, typically produced through continuous casting and cutting, or by punching from aluminum sheets. Its primary uses are as a raw material for impact extrusion processes, particularly in the manufacturing of seamless aluminum products such as aerosol cans, collapsible tubes (for pharmaceuticals, cosmetics, adhesives), and battery casings. They are valued for their consistent quality, specific dimensions, and suitability for forming complex shapes.

What are the key drivers for the growth of the Round Aluminum Slug market?

The key drivers for market growth include the increasing global demand for sustainable and recyclable packaging solutions, the continuous expansion of the aerosol can and collapsible tube industries, and the growing adoption of lightweight materials in the automotive and electronics sectors. Urbanization and rising disposable incomes in emerging economies also significantly contribute to the market's expansion by boosting consumer product consumption.

How do environmental regulations impact the Round Aluminum Slug market?

Environmental regulations significantly impact the market by increasing pressure on aluminum producers to adopt more sustainable and energy-efficient manufacturing processes. While this can lead to higher operational costs due to investments in cleaner technologies or carbon offsets, it also drives demand for aluminum slugs as a preferred material due to their inherent recyclability and lower environmental footprint compared to many alternative packaging materials.

What role does technology play in the Round Aluminum Slug industry?

Technology plays a crucial role in enhancing production efficiency, ensuring consistent product quality, and enabling the development of new alloy compositions. Advanced manufacturing techniques, automation, and AI-powered systems optimize the slug production process, reduce waste, and improve operational resilience. Furthermore, technological advancements support the expansion of slugs into new high-performance applications.

Which regions are leading in the consumption and production of Round Aluminum Slugs?

Asia Pacific is currently the leading region in both consumption and production of Round Aluminum Slugs, driven by robust industrial growth and a large consumer base in countries like China and India. Europe and North America also represent significant markets, characterized by established packaging industries, stringent sustainability norms, and advanced manufacturing capabilities.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted