Robotic Process Automation in the Telecommunication Market

Robotic Process Automation in the Telecommunication Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710264 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

Robotic Process Automation in the Telecommunication Market Size

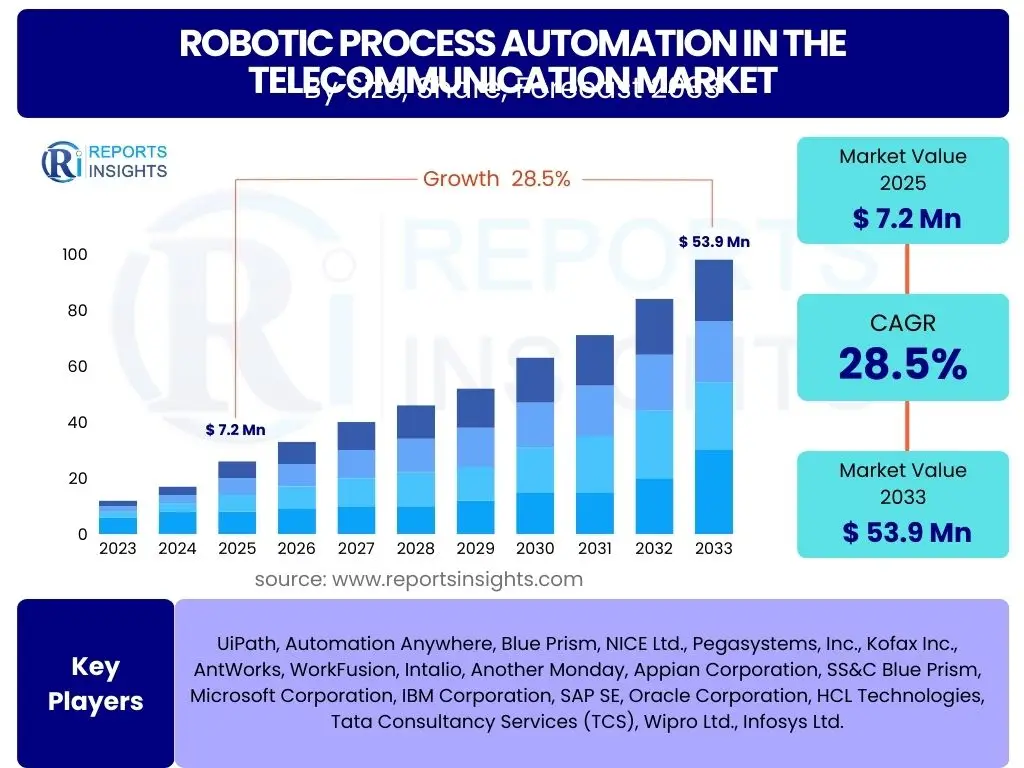

According to Reports Insights Consulting Pvt Ltd, The Robotic Process Automation in the Telecommunication Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2025 and 2033. The market is estimated at USD 7.2 Billion in 2025 and is projected to reach USD 53.9 Billion by the end of the forecast period in 2033.

The rapid expansion is primarily driven by the imperative for telecommunication companies to enhance operational efficiencies, reduce costs, and improve customer experience in an increasingly competitive and data-intensive landscape. As network infrastructures evolve with 5G and fiber deployments, the complexity of managing operations across customer service, network provisioning, and back-office functions escalates, making RPA an indispensable tool for automation and streamlining. The market's significant growth trajectory reflects a widespread strategic shift towards digital transformation initiatives within the telecom sector, recognizing RPA's capability to deliver substantial ROI by automating repetitive, rule-based processes.

Key Robotic Process Automation in the Telecommunication Market Trends & Insights

The Robotic Process Automation in the Telecommunication market is experiencing transformative shifts driven by the industry's need for agility and efficiency. Key trends indicate a move beyond basic task automation towards more intelligent and integrated solutions, emphasizing customer-centric processes and network optimization. Telecommunication companies are increasingly exploring hyperautomation, combining RPA with Artificial Intelligence (AI) and Machine Learning (ML), to address complex challenges such as managing vast data volumes, predictive network maintenance, and offering highly personalized customer interactions. This strategic evolution underscores a broader industry pivot towards digital-first operating models, leveraging automation to navigate technological advancements like 5G and the Internet of Things (IoT).

- Hyperautomation adoption: Integrating RPA with AI, ML, and process mining for end-to-end automation.

- Enhanced customer experience: Automating service desk operations, complaint resolution, and personalized offerings.

- Network operations optimization: RPA for proactive monitoring, fault management, and service provisioning.

- Increased focus on compliance and security: Automating regulatory reporting and data privacy adherence.

- Cloud-based RPA solutions: Driving scalability, flexibility, and reduced infrastructure costs for telecom operators.

- AI-powered intelligent automation: Leveraging cognitive capabilities for unstructured data processing and decision support.

AI Impact Analysis on Robotic Process Automation in the Telecommunication

Artificial Intelligence profoundly impacts Robotic Process Automation within the telecommunication sector by transforming traditional RPA from rule-based task automation to intelligent process automation. Users are highly interested in how AI enhances RPA's capabilities, moving beyond simple data entry and repetitive tasks to handle more complex, cognitive processes. This integration is crucial for addressing unstructured data, making informed decisions, and providing predictive insights in areas such as customer service, network management, and fraud detection. Concerns often revolve around the ethical implications of AI, the need for robust data governance, and ensuring that AI-powered RPA solutions maintain accuracy and transparency while delivering significant operational benefits.

The synergistic relationship between AI and RPA is central to the future of telecom operations, enabling companies to achieve a higher degree of automation and efficiency. AI capabilities, such as natural language processing (NLP), machine learning, and computer vision, empower RPA bots to understand context, learn from data, and adapt to changing conditions. This leads to more sophisticated automation solutions that can analyze customer sentiment, optimize network traffic in real-time, or even predict potential system failures before they occur. The primary expectation is that AI will unlock new levels of efficiency, cost savings, and innovation, allowing telecom providers to offer superior services and maintain a competitive edge in a rapidly evolving market.

- Enhanced decision-making: AI algorithms provide insights for RPA bots to make more intelligent choices.

- Predictive analytics: AI enables RPA to anticipate issues in network operations and customer behavior.

- Cognitive automation: Handling unstructured data and complex processes requiring human-like intelligence.

- Improved customer interaction: NLP-powered bots for sophisticated chatbot and virtual assistant functionalities.

- Dynamic process adaptation: RPA solutions can self-learn and adapt to new scenarios with AI integration.

- Fraud detection and security: AI-driven pattern recognition enhances RPA's ability to identify and prevent fraudulent activities.

Key Takeaways Robotic Process Automation in the Telecommunication Market Size & Forecast

The Robotic Process Automation in the Telecommunication market is poised for significant growth, reflecting a strategic imperative for telecom operators to optimize operations and enhance customer experience. The key takeaway from the market size and forecast analysis is the undeniable trend towards digital transformation, with RPA serving as a foundational technology. Stakeholders are keen to understand the specific areas of investment that yield the highest returns, whether in back-office automation, network management, or customer service. The forecast underscores that early adopters and those who strategically integrate RPA with other emerging technologies, particularly AI, will gain a considerable competitive advantage.

Furthermore, the market's robust CAGR projection indicates that RPA is no longer a niche solution but a core component of future-proof telecom infrastructure. It suggests that companies lagging in RPA adoption risk falling behind in efficiency, cost management, and service delivery. The forecast also highlights the growing demand for specialized RPA solutions tailored to the unique complexities of the telecommunication sector, including its stringent regulatory environment and extensive data processing requirements. Understanding these dynamics is crucial for investors, solution providers, and telecom enterprises planning their long-term automation strategies.

- Substantial market expansion expected, driven by operational efficiency demands.

- Significant investment opportunities in both software and services components of RPA.

- Integration with AI and Machine Learning is critical for maximizing RPA's value proposition.

- Customer experience and network optimization remain primary areas of RPA application.

- Cloud-based RPA deployment models are gaining traction due to scalability benefits.

- Regional variations in adoption rates and regulatory environments will influence market penetration.

Robotic Process Automation in the Telecommunication Market Drivers Analysis

The Robotic Process Automation market in telecommunication is propelled by several robust drivers, primarily the escalating demand for operational efficiency and cost reduction across the complex telecom value chain. As telecommunication companies grapple with managing vast customer bases, intricate network infrastructures, and the rollout of new technologies like 5G, the need to automate repetitive and high-volume tasks becomes paramount. RPA offers a tangible solution to streamline processes such as customer onboarding, billing, network provisioning, and fraud management, leading to significant time and resource savings. This drive for efficiency is further fueled by intense competition, compelling operators to innovate and deliver superior services at lower operational costs.

Another significant driver is the continuous pressure to enhance customer experience. In an era where customer churn is a constant threat, telecom providers are leveraging RPA to automate customer service interactions, personalize offerings, and speed up issue resolution. By freeing human agents from mundane tasks, RPA allows them to focus on more complex, value-added customer engagements. Additionally, the increasing complexity of regulatory compliance and data security mandates in the telecom sector necessitates automated processes to ensure accuracy, consistency, and adherence to industry standards. The digital transformation initiatives widely adopted across the globe further accelerate RPA adoption, positioning it as a foundational technology for modernization.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Need for Operational Efficiency and Cost Reduction | +8.5% | Global | Short to Mid-term |

| Enhanced Customer Experience and Service Delivery | +6.2% | North America, Europe, APAC | Mid to Long-term |

| Increasing Complexity of Network Management (e.g., 5G, IoT) | +5.8% | Global | Mid to Long-term |

| Demand for Digital Transformation and Automation Initiatives | +7.0% | All Regions | Short to Mid-term |

| Competitive Pressure in the Telecommunication Industry | +4.5% | Global | Short to Long-term |

Robotic Process Automation in the Telecommunication Market Restraints Analysis

Despite its significant growth potential, the Robotic Process Automation market in telecommunication faces several notable restraints. One primary challenge is the high initial investment required for RPA software licenses, implementation services, and infrastructure upgrades. Many telecommunication companies operate with legacy IT systems, which can complicate RPA integration and necessitate substantial upfront capital expenditure, deterring smaller operators or those with limited budgets. This financial barrier can slow down the adoption rate, especially in price-sensitive emerging markets. Furthermore, the perceived complexity of integrating RPA with existing, often monolithic, enterprise systems poses a technical hurdle, leading to extended deployment times and potential project overruns.

Another significant restraint is the resistance to change within organizations and the fear of job displacement among employees. While RPA aims to augment human capabilities, concerns about automation leading to workforce reduction can create internal friction and hinder successful implementation. The lack of skilled personnel capable of deploying, managing, and optimizing RPA solutions is also a critical constraint. Telecommunication companies often struggle to find employees with the right mix of technical and domain expertise, leading to reliance on external consultants which adds to costs. Moreover, data security and privacy concerns are paramount in the heavily regulated telecom sector. Ensuring that RPA bots comply with stringent data protection laws (like GDPR) and prevent unauthorized access to sensitive customer data requires robust governance frameworks, which can be complex and costly to establish and maintain.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Implementation Costs | -3.5% | Global, particularly SMEs | Short to Mid-term |

| Integration Challenges with Legacy Systems | -4.0% | Mature Markets, Older Operators | Short to Mid-term |

| Data Security and Privacy Concerns | -2.8% | Europe (GDPR), North America | Mid to Long-term |

| Lack of Skilled Workforce and Talent Gap | -3.0% | Global | Short to Mid-term |

| Resistance to Change and Employee Concerns | -2.0% | Global | Short to Mid-term |

Robotic Process Automation in the Telecommunication Market Opportunities Analysis

The Robotic Process Automation market in telecommunication is rich with opportunities, driven by the sector's ongoing digital transformation and the emergence of new technologies. One significant opportunity lies in the expansion of RPA applications beyond traditional back-office tasks to more complex, front-office, and network-centric operations. This includes leveraging RPA for proactive network monitoring, predictive maintenance, and managing the intricate service provisioning associated with 5G and IoT ecosystems. As telecom networks become more software-defined and virtualized, RPA can play a crucial role in orchestrating these complex environments, leading to unprecedented levels of automation and efficiency gains. Furthermore, the increasing adoption of cloud-based RPA solutions presents an opportunity for greater scalability, reduced infrastructure costs, and easier deployment, especially for smaller telecom operators.

Another promising avenue is the development of hyperautomation strategies, which combine RPA with Artificial Intelligence, Machine Learning, and process mining. This integration allows telecommunication companies to automate end-to-end processes that require cognitive capabilities, such as advanced analytics for customer churn prediction, intelligent document processing for contract management, and AI-driven chatbots for sophisticated customer interactions. The opportunity also extends to personalized customer service offerings, where RPA, combined with customer data analytics, can create highly tailored experiences, driving customer loyalty and retention. Emerging markets, with their rapidly expanding subscriber bases and nascent digital infrastructure, present a greenfield opportunity for RPA adoption, allowing new operators to implement automation from the ground up, avoiding legacy system challenges prevalent in developed markets.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Use Cases (5G, IoT Network Management) | +7.0% | Global | Mid to Long-term |

| Growing Demand for Hyperautomation Solutions | +6.5% | North America, Europe, APAC | Mid to Long-term |

| Development of Cloud-Based RPA Offerings | +5.0% | Global | Short to Mid-term |

| Personalization of Customer Services through Automation | +4.8% | Mature Markets | Mid to Long-term |

| Untapped Potential in Emerging Markets | +5.5% | APAC, Latin America, MEA | Long-term |

Robotic Process Automation in the Telecommunication Market Challenges Impact Analysis

The Robotic Process Automation market in telecommunication faces significant challenges that can impact its growth and widespread adoption. One critical challenge is the inherent complexity of integrating RPA solutions with the diverse and often fragmented IT landscapes prevalent in telecom companies. Many operators rely on a mix of legacy systems, proprietary software, and newer cloud-based applications, making seamless integration a formidable technical and operational hurdle. This complexity can lead to extended deployment timelines, increased costs, and potential disruptions to existing services, deterring operators from committing to large-scale RPA initiatives.

Another key challenge revolves around ensuring data privacy and regulatory compliance, particularly with sensitive customer data. Telecommunication companies operate under stringent data protection regulations globally (e.g., GDPR in Europe), and the automation of processes involving personal information requires robust governance, auditing, and security measures. Any breach or non-compliance due to an RPA implementation can have severe financial and reputational consequences. Furthermore, scaling RPA initiatives beyond initial pilot projects presents a challenge, as companies encounter difficulties in identifying suitable processes for automation, managing a growing fleet of bots, and maintaining the accuracy and reliability of automated tasks across an expansive organizational structure. The rapid evolution of technology also means that RPA solutions must continuously adapt to new network architectures, service models, and emerging customer demands, requiring ongoing investment in development and training.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Complex Legacy Systems | -4.2% | Mature Markets | Short to Mid-term |

| Ensuring Data Privacy and Regulatory Compliance | -3.8% | Global, especially Europe | Mid to Long-term |

| Scalability and Governance of RPA Deployments | -3.0% | Global | Mid to Long-term |

| Managing Change and Organizational Adoption | -2.5% | Global | Short to Mid-term |

| Rapidly Evolving Technological Landscape | -2.0% | Global | Long-term |

Robotic Process Automation in the Telecommunication Market - Updated Report Scope

This comprehensive report provides a detailed analysis of the Robotic Process Automation in the Telecommunication Market, offering a strategic overview of market dynamics, growth drivers, restraints, opportunities, and challenges. It delves into the segmentation of the market by component, deployment, application, and enterprise size, providing granular insights into each category. The report also includes an in-depth regional analysis, highlighting key trends and adoption rates across major geographies. A significant focus is placed on the competitive landscape, profiling leading players and their strategic initiatives, alongside an AI impact analysis to understand the evolving role of cognitive technologies in telecom automation.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.2 Billion |

| Market Forecast in 2033 | USD 53.9 Billion |

| Growth Rate | 28.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | UiPath, Automation Anywhere, Blue Prism, NICE Ltd., Pegasystems, Inc., Kofax Inc., AntWorks, WorkFusion, Intalio, Another Monday, Appian Corporation, SS&C Blue Prism, Microsoft Corporation, IBM Corporation, SAP SE, Oracle Corporation, HCL Technologies, Tata Consultancy Services (TCS), Wipro Ltd., Infosys Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Robotic Process Automation in the Telecommunication market is comprehensively segmented to provide a granular view of its diverse applications and technological deployments. This segmentation helps in understanding specific adoption patterns, market drivers, and opportunities within various facets of the telecom industry. The market is primarily categorized by component, distinguishing between RPA software, which includes platforms and development tools, and RPA services, encompassing consulting, implementation, and ongoing support. This split reflects the complete lifecycle of RPA adoption, from initial strategy to deployment and maintenance.

Further segmentation by deployment model differentiates between on-premises solutions, favored by organizations with stringent data security requirements or extensive legacy infrastructure, and cloud-based deployments, which offer greater scalability, flexibility, and reduced upfront costs. Application-based segmentation highlights RPA's utility across critical telecom operations, including customer service automation, network operations and management, various back-office functions like billing and finance, and specialized areas such as compliance and fraud detection. Finally, enterprise size segmentation distinguishes adoption trends and solution requirements between large telecommunication corporations and small to medium-sized enterprises (SMEs), acknowledging their varied resource capabilities and automation needs.

- By Component:

- Software (Platform, Tools)

- Services (Consulting, Implementation, Support & Maintenance)

- By Deployment:

- On-Premises

- Cloud

- By Application:

- Customer Service (e.g., call center automation, complaint management)

- Network Operations & Management (e.g., service provisioning, fault resolution)

- Back-Office Operations (e.g., Billing & Invoicing, HR & Finance, Supply Chain Management)

- Marketing & Sales (e.g., lead qualification, campaign management)

- Data Management (e.g., data migration, data validation)

- Compliance & Fraud Detection (e.g., regulatory reporting, anomaly detection)

- By Enterprise Size:

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Regional Highlights

- North America: This region is a leader in RPA adoption within the telecommunication sector, driven by technological advancements, high investment in digital transformation, and the presence of major telecom operators and RPA solution providers. The focus here is on leveraging RPA for advanced customer service, 5G network optimization, and combating fraud.

- Europe: The European market demonstrates significant growth, influenced by stringent regulatory compliance (like GDPR) driving the need for automated data handling and strong emphasis on enhancing customer experience. Countries like the UK, Germany, and France are at the forefront of implementing RPA for operational efficiencies and innovation.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid digital infrastructure development, increasing mobile penetration, and government initiatives promoting automation and smart cities. Emerging economies like India and China are experiencing a boom in RPA adoption to manage large subscriber bases and scale operations efficiently.

- Latin America: This region is characterized by nascent but growing adoption of RPA in telecommunications, primarily driven by the need for cost optimization and improved customer service in competitive markets. Investments are gradually increasing as operators seek to modernize their legacy systems.

- Middle East and Africa (MEA): The MEA market is witnessing steady growth, particularly in the GCC countries, propelled by ambitious digital transformation agendas and smart infrastructure projects. RPA is being deployed to enhance public services, streamline utility operations, and improve telecom service delivery across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Robotic Process Automation in the Telecommunication Market.- UiPath

- Automation Anywhere

- Blue Prism

- NICE Ltd.

- Pegasystems, Inc.

- Kofax Inc.

- AntWorks

- WorkFusion

- Intalio

- Another Monday

- Appian Corporation

- SS&C Blue Prism

- Microsoft Corporation

- IBM Corporation

- SAP SE

- Oracle Corporation

- HCL Technologies

- Tata Consultancy Services (TCS)

- Wipro Ltd.

- Infosys Ltd.

Frequently Asked Questions

What is Robotic Process Automation (RPA) in the telecommunication sector?

Robotic Process Automation (RPA) in telecommunication involves using software robots (bots) to automate repetitive, rule-based tasks within telecom operations, such as customer service, network management, billing, and back-office processes, enhancing efficiency and reducing manual effort.

Why is RPA important for telecommunication companies?

RPA is crucial for telecom companies to improve operational efficiency, reduce costs, enhance customer experience, accelerate service delivery, ensure regulatory compliance, and enable digital transformation in a highly competitive and evolving technological landscape, especially with 5G and IoT.

What are the primary applications of RPA in telecommunication?

Key applications include automating customer onboarding and support, managing network provisioning and fault resolution, streamlining billing and invoice processing, handling HR and finance operations, and facilitating data management and fraud detection.

How does AI impact RPA in the telecommunication market?

AI significantly enhances RPA by enabling intelligent automation, allowing bots to handle unstructured data, make cognitive decisions, and provide predictive insights, thereby transforming traditional RPA into hyperautomation for more complex telecom processes like predictive network maintenance and personalized customer interactions.

What are the main challenges for RPA adoption in telecommunications?

Challenges include high initial investment, complex integration with legacy IT systems, ensuring data privacy and regulatory compliance, the shortage of skilled personnel for deployment and management, and potential organizational resistance to change.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted