Reverse Logistic Market

Reverse Logistic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703470 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Reverse Logistic Market Size

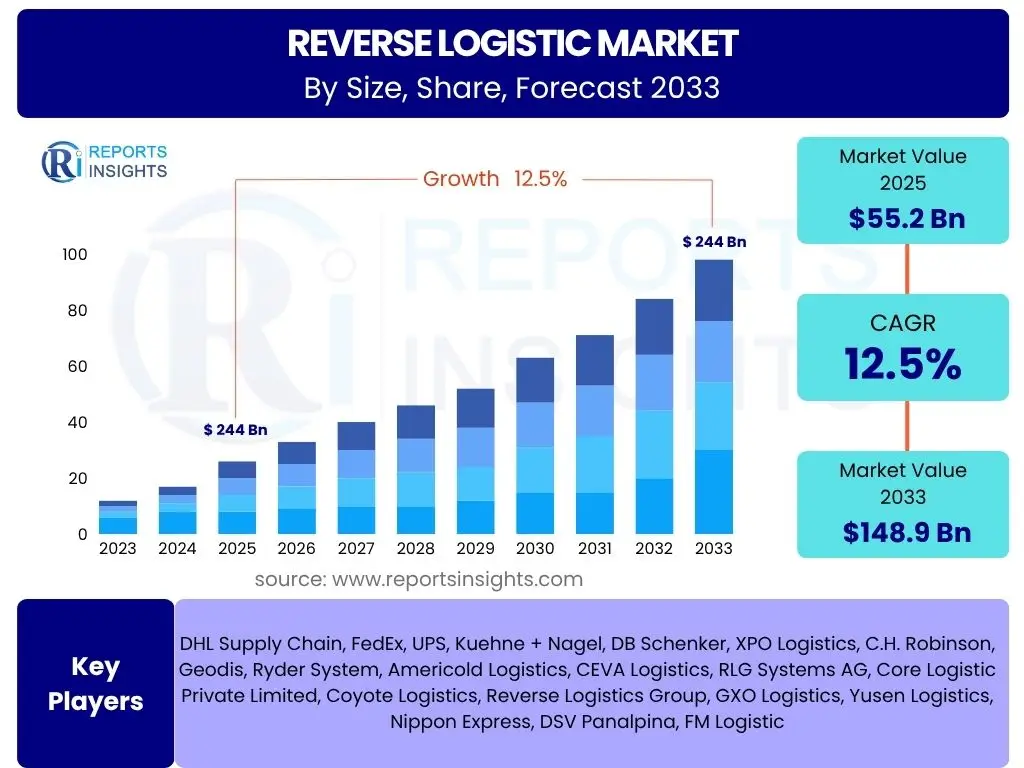

According to Reports Insights Consulting Pvt Ltd, The Reverse Logistic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 55.2 Billion in 2025 and is projected to reach USD 148.9 Billion by the end of the forecast period in 2033.

Key Reverse Logistic Market Trends & Insights

User inquiries frequently highlight the evolving landscape of consumer behavior, particularly the rise of e-commerce and its direct correlation with product returns. There is a strong interest in how businesses are adapting their operational strategies to manage increased return volumes efficiently and cost-effectively. Furthermore, discussions often revolve around the integration of advanced technologies and the adoption of sustainable practices within reverse logistics operations. Consumers and businesses alike are seeking transparency and efficiency in the return process, which is driving innovation and the adoption of new business models.

Another area of significant user concern is the impact of global supply chain disruptions and regulatory changes on reverse logistics. Businesses are looking for ways to build more resilient return networks that can withstand external shocks while complying with increasingly stringent environmental and waste management regulations. The focus is shifting from merely processing returns to transforming them into a value-adding component of the supply chain, emphasizing recovery, refurbishment, and resale to minimize waste and maximize asset utilization.

- Exponential growth of e-commerce driving increased return volumes.

- Rising consumer expectations for seamless and convenient return experiences.

- Focus on sustainability and circular economy principles, leading to higher rates of repair, refurbishment, and recycling.

- Increased adoption of automation and data analytics for optimized return processing.

- Strategic shift towards viewing reverse logistics as a value-added activity rather than a cost center.

- Implementation of advanced tracking and traceability solutions for returned goods.

- Expansion of third-party logistics (3PL) providers offering specialized reverse logistics services.

AI Impact Analysis on Reverse Logistic

User queries regarding AI's impact on reverse logistics often center on its potential to enhance operational efficiency, reduce costs, and improve customer satisfaction. There is a keen interest in how artificial intelligence can forecast return volumes, optimize routing for collections, and automate inspection and sorting processes for returned goods. Concerns are sometimes raised about the initial investment required for AI implementation and the need for skilled personnel to manage these advanced systems effectively. Users are looking for tangible examples of how AI translates into measurable improvements in reverse logistics operations.

Additionally, common questions explore AI's role in fraud detection, particularly in preventing fraudulent returns, and its application in dynamic pricing for returned or refurbished items. Users also inquire about AI's capacity to support predictive maintenance for products still in use, thereby potentially reducing the need for returns due to defects. The overarching expectation is that AI will transform reverse logistics from a reactive, manual process into a proactive, intelligent, and highly automated system that can adapt to fluctuating market demands and consumer behaviors.

- Enhanced forecasting of return volumes, optimizing resource allocation.

- Automated defect detection and quality inspection using computer vision.

- Route optimization for reverse pickups, reducing transportation costs and emissions.

- Predictive analytics for product lifecycle management, minimizing potential returns.

- Improved inventory management of returned goods, facilitating faster re-entry into sales channels.

- Personalized return experiences based on customer history and preferences.

- Fraud detection and prevention through pattern recognition in return data.

- Dynamic pricing strategies for refurbished or resold products based on condition and market demand.

Key Takeaways Reverse Logistic Market Size & Forecast

User inquiries frequently seek a concise understanding of the market's growth trajectory and the primary factors contributing to its expansion. There is a strong emphasis on identifying the core drivers that will sustain the projected CAGR, particularly concerning consumer behavior shifts and the broader economic landscape. Users are also interested in the strategic implications of this growth, such as the increasing importance of efficient return management for customer retention and profitability.

Furthermore, common questions highlight the need to understand potential hurdles or challenges that could impede market growth, as well as emerging opportunities that businesses can leverage. The focus is on gaining actionable insights that inform investment decisions, operational improvements, and strategic planning within the reverse logistics domain. The market's significant financial projection underscores its transition from a niche operational concern to a critical component of mainstream supply chain management.

- The Reverse Logistic Market is poised for substantial growth, driven by escalating e-commerce penetration.

- Customer experience and loyalty are increasingly tied to efficient and hassle-free return processes.

- Sustainability initiatives and circular economy models are transforming return management into a value-recovery process.

- Technological advancements, including AI and automation, are crucial for optimizing reverse logistics operations.

- Strategic investment in reverse logistics infrastructure and expertise will be vital for market players.

Reverse Logistic Market Drivers Analysis

The burgeoning e-commerce sector stands as a paramount driver for the reverse logistics market. As online retail continues its rapid expansion globally, the volume of goods purchased and subsequently returned has surged dramatically. This phenomenon creates an inherent demand for sophisticated reverse logistics solutions capable of handling diverse product types, managing varying return reasons, and facilitating efficient processing to mitigate losses and maximize value recovery. Consumers' increasing comfort with online shopping, coupled with generous return policies offered by retailers to encourage purchases, directly contributes to the heightened activity in the reverse logistics domain.

Furthermore, the growing emphasis on sustainability and circular economy principles is significantly influencing the market. Businesses are under increasing pressure from consumers, regulators, and investors to adopt more environmentally responsible practices. Reverse logistics, by facilitating the repair, refurbishment, recycling, and responsible disposal of products, plays a pivotal role in reducing waste, conserving resources, and minimizing environmental impact. This shift from a linear "take-make-dispose" model to a circular one drives investment and innovation in reverse logistics capabilities, as companies seek to enhance their corporate social responsibility profile and unlock new revenue streams from recovered materials or refurbished goods.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| E-commerce Growth and High Return Rates | +3.5% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Increasing Focus on Sustainability and Circular Economy | +2.8% | Europe, North America, developing Asia Pacific | Mid to Long-term (2027-2033) |

| Stringent Environmental Regulations and Compliance | +2.0% | Europe, North America, Japan, China | Mid-term (2026-2031) |

| Technological Advancements in Logistics and Supply Chain | +1.8% | Global | Short to Mid-term (2025-2030) |

| Growing Awareness of Customer Experience | +1.5% | Global, especially developed economies | Short to Mid-term (2025-2029) |

| Rising Value of Returned and Recovered Assets | +0.9% | Global | Mid to Long-term (2027-2033) |

Reverse Logistic Market Restraints Analysis

A significant restraint in the reverse logistics market is the inherent complexity and high cost associated with managing returns. Unlike forward logistics, which follows a predictable path from manufacturer to consumer, reverse logistics involves unpredictable volumes, varied product conditions, diverse return reasons, and multiple potential destinations (e.g., repair centers, recycling facilities, liquidation channels). This unpredictability complicates planning, requires specialized handling, and often leads to higher per-unit costs compared to outbound shipments. The absence of standardized processes across different industries and product types further exacerbates this complexity, demanding tailored solutions that can be expensive to implement and maintain.

Another key restraint is the lack of proper infrastructure and technological integration, particularly in emerging markets. While developed economies are investing in advanced logistics technologies, many regions still rely on manual processes and fragmented systems. This deficit hinders efficient data collection, tracking, and analysis, making it difficult to optimize return flows, identify root causes of returns, and achieve economies of scale. The initial capital investment required for implementing sophisticated reverse logistics systems, including automation, AI, and advanced analytics, can be prohibitive for many businesses, especially small and medium-sized enterprises (SMEs), thereby limiting market penetration and widespread adoption of best practices.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Operational Costs and Complexity of Returns | -2.0% | Global | Short to Mid-term (2025-2029) |

| Lack of Standardized Processes and Infrastructure | -1.5% | Emerging Markets (Asia Pacific, Latin America, MEA) | Mid-term (2026-2031) |

| Data Management Challenges and System Integration Issues | -1.2% | Global | Short to Mid-term (2025-2030) |

| Brand Reputation Risk from Inefficient Returns | -0.8% | Global | Short-term (2025-2028) |

| Limited Expertise and Skilled Workforce | -0.7% | Global | Mid-term (2026-2032) |

Reverse Logistic Market Opportunities Analysis

The increasing adoption of subscription-based models and the sharing economy presents a significant opportunity for the reverse logistics market. In these models, products are often leased or rented rather than sold, necessitating efficient processes for product collection, refurbishment, and redeployment at the end of a usage cycle. This creates a predictable and recurring demand for reverse logistics services, moving beyond just handling returns of purchased goods to managing the lifecycle of assets that remain under the ownership of the service provider. Companies specializing in reverse logistics can forge strong partnerships with businesses in these emerging sectors, developing tailored solutions for asset recovery, maintenance, and remarketing, thereby opening up new revenue streams and market segments.

Furthermore, the growing emphasis on value recovery and the development of specialized markets for refurbished and recycled goods offer substantial opportunities. Instead of viewing returned products merely as waste, businesses are increasingly recognizing their inherent value, whether through repair for resale, harvesting components, or recycling materials. This shift is fueling the demand for sophisticated reverse logistics capabilities that can assess product condition, perform quality checks, and channel items to the most profitable disposition options. Companies that can efficiently process, repair, and market these recovered assets will gain a competitive edge, tapping into a growing consumer base interested in more affordable or environmentally friendly alternatives, particularly in the electronics, automotive, and consumer goods sectors.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Subscription Models and Sharing Economy | +2.5% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Development of New Value Recovery Channels | +2.2% | Global | Mid-term (2026-2031) |

| Expansion into New End-Use Industries | +1.8% | Global | Mid-term (2026-2030) |

| Increased Outsourcing to 3PL Providers | +1.5% | Global | Short to Mid-term (2025-2029) |

| Technological Innovation in Product Life Cycle Management | +1.0% | Global | Long-term (2028-2033) |

Reverse Logistic Market Challenges Impact Analysis

One of the persistent challenges in the reverse logistics market is managing the unpredictable volume and varied condition of returned goods. Unlike forward logistics where volume is largely predictable based on sales forecasts, return volumes can fluctuate significantly due to seasonal peaks, promotional activities, or changes in consumer preferences. Furthermore, products returned can range from unopened and pristine to heavily damaged or defective, each requiring different handling, inspection, and disposition processes. This variability makes it difficult to optimize resource allocation, staffing levels, and warehouse space, leading to inefficiencies and increased operational costs. Companies must develop highly flexible and adaptable systems to cope with these inherent uncertainties.

Another significant challenge revolves around data visibility and system integration. Many organizations operate with disparate IT systems for sales, inventory, customer service, and logistics, making it difficult to gain a holistic view of the return process from initiation to final disposition. This lack of end-to-end visibility hinders effective tracking, root cause analysis of returns, and performance measurement. Integrating these systems requires substantial investment in technology and skilled personnel, and often faces resistance due to organizational silos. Without robust data infrastructure, businesses struggle to identify trends, optimize return policies, and make data-driven decisions that could improve profitability and customer satisfaction.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Unpredictable Return Volumes and Product Conditions | -1.8% | Global | Short to Mid-term (2025-2029) |

| Lack of Data Visibility and System Integration | -1.5% | Global | Mid-term (2026-2031) |

| Increasing Consumer Expectations for Easy Returns | -1.2% | Developed Economies | Short to Mid-term (2025-2030) |

| Fraudulent Returns and Abuse of Policies | -0.9% | Global | Short-term (2025-2028) |

| Environmental Compliance and Disposal Regulations | -0.6% | Europe, North America | Mid to Long-term (2027-2033) |

Reverse Logistic Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Reverse Logistic Market, offering an updated scope that encompasses the latest industry trends, technological advancements, and evolving regulatory landscapes. It provides a meticulous analysis of market size, growth drivers, restraints, opportunities, and challenges, along with detailed segmentations by return type, end-use industry, service type, and mode of transport. The report also highlights regional market performance, key competitive landscapes, and strategic insights for market participants seeking to navigate the complexities of product returns and value recovery efficiently.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 55.2 Billion |

| Market Forecast in 2033 | USD 148.9 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DHL Supply Chain, FedEx, UPS, Kuehne + Nagel, DB Schenker, XPO Logistics, C.H. Robinson, Geodis, Ryder System, Americold Logistics, CEVA Logistics, RLG Systems AG, Core Logistic Private Limited, Coyote Logistics, Reverse Logistics Group, GXO Logistics, Yusen Logistics, Nippon Express, DSV Panalpina, FM Logistic |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Reverse Logistic Market is broadly segmented based on return type, end-use industry, service type, and mode of transport, reflecting the diverse operational needs and complexities across various sectors. Each segment addresses specific aspects of the return journey, from initial customer interaction to final disposition, ensuring a comprehensive understanding of market dynamics. This detailed segmentation allows for a nuanced analysis of market trends, identifying key growth areas and challenges within each category.

Understanding these segments is crucial for businesses looking to optimize their reverse logistics strategies and service providers aiming to tailor their offerings to specific client needs. For instance, the requirements for managing consumer e-commerce returns differ significantly from those for handling complex industrial equipment recalls or end-of-life electronics recycling, necessitating distinct approaches in terms of infrastructure, technology, and expertise. This multi-faceted segmentation provides valuable insights into the market's structure and potential for innovation across its varied components.

- By Return Type: Commercial Returns, Repairable Returns, End-of-Life Returns, Recall Returns.

- By End-Use Industry: E-commerce & Retail, Automotive, Electronics & High-Tech, Pharmaceutical & Healthcare, Consumer Goods, Heavy Machinery & Equipment, Aerospace & Defense, Others.

- By Service Type: Returns Management, Remanufacturing & Refurbishment, Packaging, Warehousing & Storage, Transportation Management, Recycling & Waste Management, Replacement Management, Asset Recovery.

- By Mode of Transport: Roadways, Railways, Waterways, Airways.

Regional Highlights

The North American market, encompassing the United States and Canada, represents a significant portion of the global reverse logistics market, largely driven by its mature e-commerce landscape and robust consumer spending. The region's advanced logistics infrastructure, coupled with a high volume of online sales and a consumer culture that often encourages returns, fuels demand for sophisticated reverse logistics solutions. Both large retailers and specialized 3PL providers are heavily investing in automation and data analytics to streamline return processes, manage inventory of returned goods efficiently, and enhance customer satisfaction. Stringent environmental regulations also push companies towards sustainable recovery and recycling practices, further boosting the market.

Europe stands as another prominent region, characterized by its strong emphasis on circular economy principles and comprehensive environmental directives, such as the Waste Electrical and Electronic Equipment (WEEE) Directive. Countries like Germany, the UK, and France are at the forefront of adopting advanced reverse logistics practices to facilitate product repair, reuse, and recycling. The presence of a highly developed logistics network and increasing cross-border e-commerce activities further support market growth. European consumers are increasingly environmentally conscious, compelling businesses to adopt more sustainable return and disposal methods, which in turn drives innovation in reverse logistics technologies and services.

The Asia Pacific (APAC) region is projected to exhibit the highest growth rate in the reverse logistics market, primarily due to the explosive growth of e-commerce in countries like China, India, and Southeast Asian nations. The rapidly expanding consumer base, coupled with improving internet penetration and logistics infrastructure, is leading to an unprecedented volume of product returns. While challenges related to fragmented logistics networks and varying regulatory environments exist, significant investments in logistics technology and warehousing capacity are underway. The sheer market size and emerging middle-class population make APAC a critical growth hub for reverse logistics, with a focus on cost-effective and scalable solutions.

Latin America is experiencing steady growth in the reverse logistics market, albeit from a smaller base, driven by the increasing adoption of e-commerce and a rising awareness of sustainability. Countries like Brazil and Mexico are leading the charge, with developing logistics infrastructures and a growing demand for efficient return management processes. While the region faces challenges such as complex customs procedures and varying logistical capabilities across countries, businesses are recognizing the importance of optimized reverse flows to reduce losses and improve customer loyalty. Investment in localized solutions and partnerships with regional logistics providers are key trends.

The Middle East and Africa (MEA) region is also witnessing nascent growth in reverse logistics, propelled by urbanization, increasing e-commerce penetration, and governmental initiatives promoting economic diversification and sustainability. Countries within the GCC (Gulf Cooperation Council) are investing heavily in logistics hubs, which indirectly supports the development of reverse logistics capabilities. However, the market here is still in its early stages, characterized by less mature logistics infrastructure and diverse regulatory frameworks. Opportunities exist for international reverse logistics providers to partner with local entities and introduce advanced solutions to meet the growing demand for efficient product returns and asset recovery.

- North America: Driven by mature e-commerce, advanced logistics infrastructure, high consumer returns, and increasing focus on sustainability. Countries like the United States and Canada are leading.

- Europe: Strong regulatory push for circular economy and WEEE directives, developed logistics networks, and growing cross-border e-commerce. Key markets include Germany, UK, and France.

- Asia Pacific (APAC): Highest growth potential fueled by explosive e-commerce expansion in China, India, and Southeast Asia; increasing disposable income and improving infrastructure.

- Latin America: Emerging e-commerce market, growing awareness of sustainability, and developing logistics infrastructure in countries such as Brazil and Mexico.

- Middle East and Africa (MEA): Nascent market growth supported by urbanization, e-commerce penetration, and strategic logistics investments, particularly in the GCC region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Reverse Logistic Market.- DHL Supply Chain

- FedEx

- UPS

- Kuehne + Nagel

- DB Schenker

- XPO Logistics

- C.H. Robinson

- Geodis

- Ryder System

- Americold Logistics

- CEVA Logistics

- RLG Systems AG

- Core Logistic Private Limited

- Coyote Logistics

- Reverse Logistics Group

- GXO Logistics

- Yusen Logistics

- Nippon Express

- DSV Panalpina

- FM Logistic

Frequently Asked Questions

What is reverse logistics?

Reverse logistics encompasses all operations related to the reuse of products and materials. It involves the process of moving goods from their typical final destination back through the supply chain for purposes such as returns, repairs, recycling, or disposal. Its primary goal is to recover value or ensure proper disposal.

Why is reverse logistics important for businesses?

Reverse logistics is crucial for businesses as it impacts customer satisfaction, sustainability goals, and cost management. Efficient reverse processes can reduce losses from returns, improve brand reputation by offering seamless return experiences, and unlock value from returned or end-of-life products through refurbishment and recycling.

How does e-commerce influence the reverse logistics market?

E-commerce significantly drives the reverse logistics market by increasing the volume of product returns. The ease of online purchasing often leads to higher return rates, requiring robust reverse logistics systems to manage the influx of goods, process refunds, and decide on the most cost-effective disposition for returned items.

What are the key challenges in reverse logistics?

Key challenges include managing unpredictable return volumes, varying product conditions, high operational costs, lack of standardized processes, and limited data visibility. Fraudulent returns and the complexity of regulatory compliance, particularly for hazardous waste, also pose significant hurdles.

How do technologies like AI and automation impact reverse logistics?

AI and automation enhance reverse logistics by enabling better forecasting of returns, optimizing collection routes, automating inspection and sorting processes, and improving inventory management of returned goods. These technologies contribute to increased efficiency, reduced operational costs, and improved decision-making for asset recovery and disposition.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted