Retiniti Pigmentosa Treatment Market

Retiniti Pigmentosa Treatment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704954 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

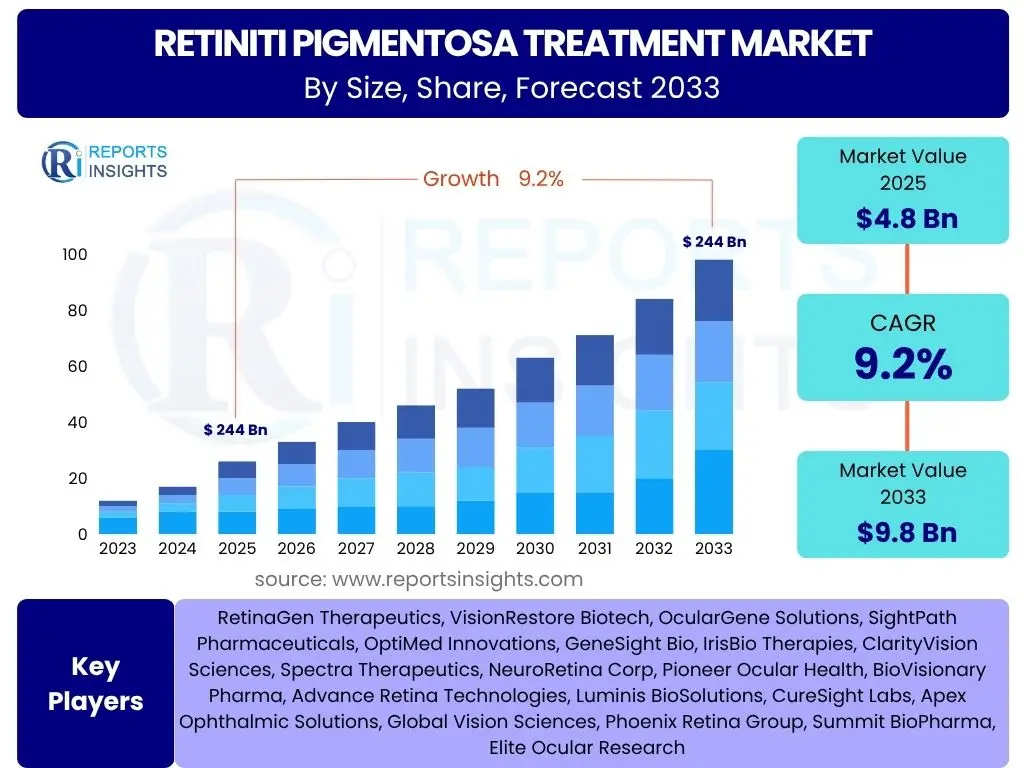

Retiniti Pigmentosa Treatment Market Size

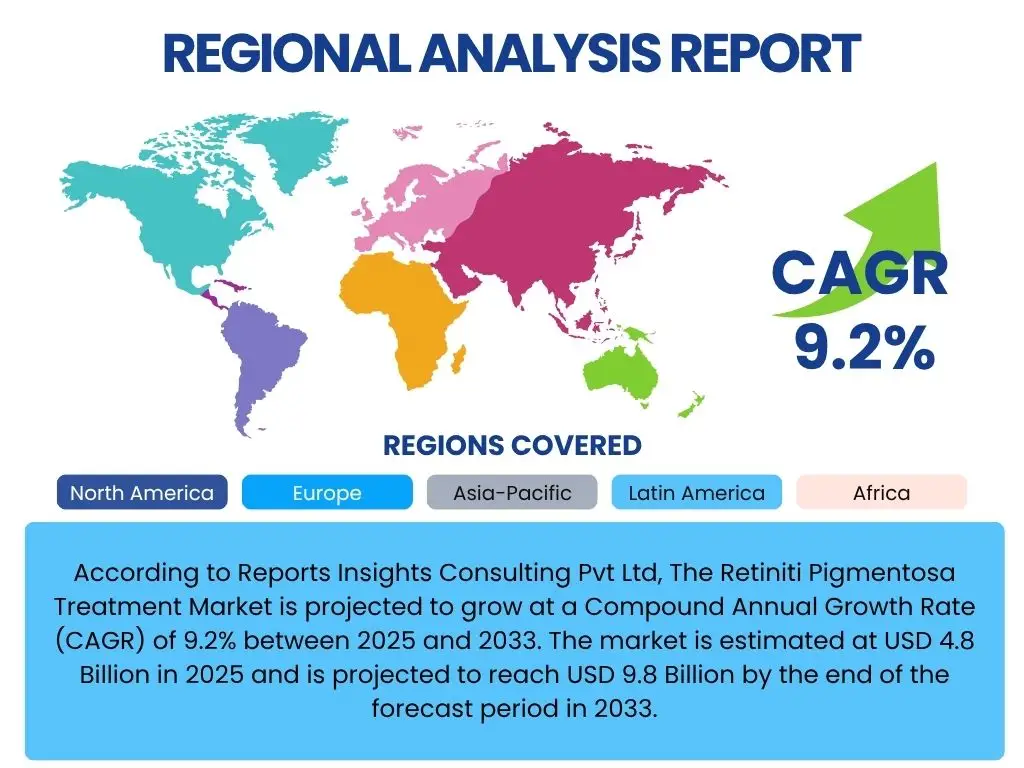

According to Reports Insights Consulting Pvt Ltd, The Retiniti Pigmentosa Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2025 and 2033. The market is estimated at USD 4.8 Billion in 2025 and is projected to reach USD 9.8 Billion by the end of the forecast period in 2033.

Key Retiniti Pigmentosa Treatment Market Trends & Insights

The Retiniti Pigmentosa (RP) treatment market is witnessing a dynamic shift driven by groundbreaking scientific advancements and an increased understanding of the genetic underpinnings of the disease. A significant trend is the accelerating pace of gene therapy research and development, which holds immense promise for addressing the root cause of various forms of RP. The focus has moved beyond symptomatic relief to gene replacement and gene editing strategies, aiming for more durable and potentially curative outcomes for patients with specific genetic mutations.

Another prominent trend is the growing emphasis on personalized medicine approaches. Given the high genetic heterogeneity of Retiniti Pigmentosa, tailoring treatments based on an individual's specific genetic mutation is becoming increasingly feasible and effective. This involves detailed genetic diagnostics and the development of mutation-specific therapies, moving away from a one-size-fits-all model. This precision medicine approach is expected to improve treatment efficacy and minimize adverse effects, enhancing patient quality of life.

Furthermore, there is a rising interest in combination therapies that target multiple pathways involved in photoreceptor degeneration, including neuroprotection, inflammation modulation, and metabolic support. Complementary to this, the development of advanced drug delivery systems, such as sustained-release intraocular implants, is gaining traction. These innovations aim to reduce the frequency of administrations, improve drug bioavailability to the retina, and enhance overall patient compliance, thereby optimizing therapeutic outcomes in the long term.

- Accelerated development and commercialization of gene therapies for specific RP mutations.

- Increased adoption of personalized medicine and genetic diagnostics for tailored treatment plans.

- Emergence of combination therapies addressing multiple disease pathways.

- Advancements in sustained-release drug delivery systems for improved patient adherence.

- Growing investment in stem cell research for retinal regeneration.

AI Impact Analysis on Retiniti Pigmentosa Treatment

Artificial Intelligence (AI) is rapidly transforming various facets of healthcare, and its impact on Retiniti Pigmentosa treatment is becoming increasingly profound. Common user inquiries often revolve around AI's ability to enhance diagnostic accuracy, predict disease progression, and personalize therapeutic interventions. AI-powered algorithms are excelling in analyzing complex retinal imaging data, such as optical coherence tomography (OCT) and fundus photography, to detect subtle signs of RP earlier and with greater precision than traditional methods, leading to earlier intervention opportunities.

Beyond diagnostics, AI's role extends into the realm of drug discovery and development. Users are keen to understand how AI can accelerate the identification of novel therapeutic targets and screen vast libraries of compounds more efficiently. Machine learning models are being utilized to predict the efficacy and safety profiles of potential drug candidates, significantly reducing the time and cost associated with preclinical research. This streamlined process could bring new RP treatments to market faster, addressing unmet patient needs more effectively.

Moreover, AI is poised to revolutionize clinical trial design and patient monitoring. By leveraging predictive analytics, AI can help identify suitable patient cohorts for trials based on genetic profiles and disease progression rates, optimizing trial efficiency. During treatment, AI tools can continuously monitor patient responses, identify optimal dosing regimens, and alert clinicians to potential complications, thereby enhancing individualized treatment strategies and improving overall patient outcomes. The integration of AI is expected to lead to more precise diagnoses, accelerated therapy development, and optimized patient management in the fight against Retiniti Pigmentosa.

- Enhanced diagnostic accuracy and early detection of Retiniti Pigmentosa through image analysis.

- Acceleration of drug discovery and development by identifying novel therapeutic targets and screening compounds.

- Optimization of clinical trial design and patient selection using predictive analytics.

- Personalized treatment optimization through continuous patient monitoring and response prediction.

- Improved understanding of disease progression and prognosis through big data analysis.

Key Takeaways Retiniti Pigmentosa Treatment Market Size & Forecast

The Retiniti Pigmentosa (RP) treatment market is poised for substantial growth, driven primarily by the rapid advancements in gene and cell therapies. A key takeaway is the shift towards disease-modifying treatments rather than purely symptomatic management. The significant projected increase in market size underscores the increasing investment in research and development, as well as the commercialization potential of novel therapeutic modalities that offer the promise of vision preservation or restoration for RP patients.

Another crucial insight is the impact of genetic diagnostics on market dynamics. The ability to precisely identify the genetic mutation causing RP in patients is increasingly guiding treatment decisions, particularly for mutation-specific gene therapies. This precision medicine approach is not only enhancing treatment efficacy but also segmenting the market based on genetic subtypes, requiring pharmaceutical companies to develop targeted therapies and diagnostic tools in tandem to capture market share.

Furthermore, the forecast indicates a growing emphasis on collaborative efforts among pharmaceutical companies, academic institutions, and patient advocacy groups. Such partnerships are vital for overcoming the complexities of rare disease research, facilitating clinical trials, and ensuring patient access to emerging high-cost therapies. The market's future growth is intrinsically linked to the successful translation of cutting-edge research into accessible and affordable treatment options globally, presenting both opportunities and challenges for stakeholders.

- Significant market expansion driven by gene and cell therapy innovations.

- Increasing importance of genetic testing for targeted therapeutic interventions.

- Shift from symptomatic relief to disease-modifying and potentially curative treatments.

- Growing collaboration among research entities, industry, and patient organizations.

- High unmet medical need continues to fuel research and market growth.

Retiniti Pigmentosa Treatment Market Drivers Analysis

The Retiniti Pigmentosa (RP) treatment market is significantly propelled by several key drivers, most notably the increasing global prevalence of the disease and the substantial advancements in molecular biology and genetic engineering. A greater understanding of the diverse genetic mutations underlying RP has opened new avenues for targeted therapeutic interventions, moving beyond traditional symptomatic management. Furthermore, the rising investment in research and development by both public and private sectors, coupled with the growing number of clinical trials for innovative treatments, is a major force behind market expansion. Favorable regulatory designations, such as Orphan Drug status, are also incentivizing pharmaceutical companies to develop therapies for rare diseases like RP, accelerating their path to market and driving commercial interest.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Prevalence of Retiniti Pigmentosa | +1.5% | Global, particularly populous regions like APAC | Short to Mid-Term (2025-2029) |

| Advancements in Gene & Cell Therapies | +2.0% | North America, Europe, parts of Asia Pacific | Mid to Long-Term (2027-2033) |

| Increasing R&D Investment and Clinical Trials | +1.8% | North America, Europe | Mid-Term (2026-2030) |

| Favorable Regulatory Designations (e.g., Orphan Drug) | +1.2% | Developed Economies (US, EU, Japan) | Short to Mid-Term (2025-2028) |

| Growing Awareness and Diagnostic Capabilities | +1.0% | Global, especially emerging markets | Long-Term (2029-2033) |

Retiniti Pigmentosa Treatment Market Restraints Analysis

Despite the promising growth trajectory, the Retiniti Pigmentosa (RP) treatment market faces several significant restraints. A primary concern is the exorbitant cost associated with advanced gene and cell therapies. These cutting-edge treatments often carry price tags that can be prohibitive for healthcare systems and individual patients, leading to limited accessibility, especially in regions with less developed healthcare infrastructure or inadequate insurance coverage. Furthermore, the high genetic heterogeneity of RP, with over 100 identified causative genes, poses a considerable challenge, making it difficult to develop broadly applicable treatments and requiring highly specific and costly diagnostic processes. The relatively small patient population for each specific genetic mutation can also deter large-scale investment, as the return on investment for such niche therapies may be perceived as lower compared to more prevalent conditions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Therapies | -1.5% | Global, particularly developing economies | Mid to Long-Term (2026-2033) |

| Genetic Heterogeneity of RP | -1.0% | Global | Short to Mid-Term (2025-2029) |

| Stringent Regulatory Approval Processes | -0.8% | Developed Economies (US, EU) | Short-Term (2025-2027) |

| Limited Patient Pool for Specific Genetic Mutations | -0.7% | Global | Mid-Term (2026-2030) |

| Ethical Concerns Related to Gene Editing | -0.5% | Europe, parts of Asia | Long-Term (2030-2033) |

Retiniti Pigmentosa Treatment Market Opportunities Analysis

Significant opportunities exist within the Retiniti Pigmentosa (RP) treatment market, predominantly centered around the untapped potential of emerging markets and the continuous evolution of gene editing technologies. Regions such as Asia Pacific and Latin America represent growing healthcare markets with increasing awareness of rare diseases and improving healthcare infrastructure, offering new patient populations and investment avenues. Furthermore, the advancements in gene editing tools like CRISPR-Cas9 present an unparalleled opportunity for permanent correction of disease-causing mutations, moving beyond gene replacement therapies to more precise genetic interventions that could address a broader spectrum of RP types. The expansion of personalized medicine, leveraging individual genetic profiles to design highly effective therapies, is also a key growth area, promising superior patient outcomes and a highly segmented, value-driven market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Markets Expansion | +1.3% | Asia Pacific, Latin America, MEA | Mid to Long-Term (2027-2033) |

| Advancements in Gene Editing Technologies (CRISPR) | +1.7% | Global Research Hubs (US, EU, China) | Long-Term (2029-2033) |

| Development of Combination Therapies | +1.1% | Global | Mid-Term (2026-2030) |

| Increased Focus on Early Diagnosis & Intervention | +0.9% | Developed Economies | Short to Mid-Term (2025-2028) |

| Telemedicine and Remote Monitoring for RP Patients | +0.6% | Global | Short-Term (2025-2027) |

Retiniti Pigmentosa Treatment Market Challenges Impact Analysis

The Retiniti Pigmentosa (RP) treatment market faces several intricate challenges that could impede its growth. One significant hurdle is the limited understanding of the heterogeneous disease progression and variable phenotype across different genetic mutations. This complexity makes it difficult to standardize treatment protocols and predict individual patient responses, thus complicating clinical trial design and therapeutic development. Another substantial challenge is the relatively small patient population, particularly for specific rare mutations, which can make it difficult to recruit sufficient participants for clinical trials, thereby prolonging the development and approval timelines for new therapies. Furthermore, the need for highly specialized infrastructure and skilled professionals for administering advanced treatments, such as subretinal injections for gene therapies, presents a logistical and accessibility challenge, especially in underserved regions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexities in Disease Understanding and Heterogeneity | -1.2% | Global | Mid to Long-Term (2027-2033) |

| Patient Recruitment for Clinical Trials | -1.0% | Global | Short to Mid-Term (2025-2029) |

| Logistical Challenges of Drug Delivery | -0.9% | Global, particularly rural areas | Mid-Term (2026-2030) |

| Reimbursement and Market Access Issues | -0.8% | Developed Economies (US, EU) | Short-Term (2025-2027) |

| Long-term Safety and Efficacy Data Gaps | -0.6% | Global | Long-Term (2030-2033) |

Retiniti Pigmentosa Treatment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Retiniti Pigmentosa Treatment Market, offering critical insights into its current landscape, historical performance, and future projections. The scope encompasses detailed market sizing, growth rate estimations, and segmentation analysis across various treatment types, routes of administration, disease types, end-users, and distribution channels. It also highlights key market trends, drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. The report profiles leading market players and covers regional dynamics, offering a robust framework for understanding the evolving competitive environment and investment potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 9.8 Billion |

| Growth Rate | 9.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | RetinaGen Therapeutics, VisionRestore Biotech, OcularGene Solutions, SightPath Pharmaceuticals, OptiMed Innovations, GeneSight Bio, IrisBio Therapies, ClarityVision Sciences, Spectra Therapeutics, NeuroRetina Corp, Pioneer Ocular Health, BioVisionary Pharma, Advance Retina Technologies, Luminis BioSolutions, CureSight Labs, Apex Ophthalmic Solutions, Global Vision Sciences, Phoenix Retina Group, Summit BioPharma, Elite Ocular Research |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Retiniti Pigmentosa (RP) treatment market is extensively segmented to reflect the diverse approaches and targeted therapies developed for this complex genetic disorder. Understanding these segments is crucial for stakeholders to identify key growth areas and tailor their strategies. The segmentation primarily revolves around the type of treatment modality, which includes groundbreaking gene therapies, regenerative stem cell therapies, and various drug therapies aimed at neuroprotection or inflammation control. Furthermore, the route of administration plays a significant role, with invasive intravitreal or subretinal injections being common for advanced therapies, alongside conventional oral or topical applications.

Disease type segmentation, based on specific genetic mutations causing RP, is increasingly important as therapies become more mutation-specific, highlighting the shift towards personalized medicine. End-user categories like hospitals and specialty clinics represent the primary points of care delivery, while research institutions are vital for ongoing therapeutic development. Finally, the distribution channels, encompassing hospital pharmacies and retail/online pharmacies, dictate how these treatments reach patients. This multi-faceted segmentation provides a granular view of the market landscape, enabling a precise evaluation of market dynamics and potential investment opportunities across different therapeutic areas and patient demographics.

- By Treatment Type: Gene Therapy, Stem Cell Therapy, Drug Therapy, Surgical Interventions, Assistive Devices.

- By Route of Administration: Intravitreal Injections, Subretinal Injections, Oral, Topical.

- By Disease Type (Genetic Mutation): RPE65 Mutation Associated RP, USH2A Mutation Associated RP, RPGR Mutation Associated RP, Other Genetic Mutations.

- By End-User: Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Research & Academic Institutions.

- By Distribution Channel: Hospital Pharmacies, Retail Pharmacies, Online Pharmacies.

Regional Highlights

- North America: North America, particularly the United States, represents the largest and most dominant market for Retiniti Pigmentosa treatment. This is primarily attributed to robust research and development activities, significant investment in biotechnology and pharmaceutical companies, and the presence of advanced healthcare infrastructure. High per capita healthcare expenditure, a strong emphasis on personalized medicine, and a supportive regulatory environment that facilitates expedited approval for orphan drugs further contribute to the region's leadership. The region also benefits from a high level of awareness among patients and healthcare professionals regarding rare genetic disorders and available cutting-edge treatments, including pioneering gene therapies.

- Europe: Europe holds a substantial share in the Retiniti Pigmentosa treatment market, driven by a strong focus on rare disease research, government funding for scientific advancements, and the presence of numerous reputable academic and research institutions. Countries such as Germany, the United Kingdom, and France are at the forefront of clinical trials and the adoption of novel therapies. While facing challenges related to varied reimbursement policies across different nations, the European market benefits from a well-established healthcare system and increasing collaboration between public and private entities to develop and deliver innovative treatments for RP patients.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for Retiniti Pigmentosa treatment. This growth is fueled by a large patient pool, improving healthcare infrastructure, and increasing awareness of genetic disorders. Countries like China, Japan, and India are witnessing significant investments in healthcare, including a rising number of clinical trials and research initiatives. While access to advanced therapies may still be a challenge in some parts of the region due to economic disparities, the expanding middle class, growing medical tourism, and government initiatives to enhance healthcare accessibility are creating substantial opportunities for market expansion.

- Latin America: The Latin American market for Retiniti Pigmentosa treatment is emerging, characterized by increasing healthcare expenditure and a growing focus on specialty care. While still smaller than developed regions, countries such as Brazil and Mexico are showing potential due to improving diagnostic capabilities and a rising demand for advanced medical treatments. Challenges include limited healthcare infrastructure in remote areas and economic constraints that may affect the adoption of high-cost therapies. However, efforts to improve healthcare access and partnerships with international pharmaceutical companies are expected to drive gradual market growth.

- Middle East and Africa (MEA): The Middle East and Africa region presents nascent opportunities for the Retiniti Pigmentosa treatment market. Growth is primarily observed in wealthier Middle Eastern countries, which have modern healthcare facilities and the financial capacity to invest in advanced treatments and medical technologies. In Africa, the market is still in its nascent stages, constrained by lower healthcare spending, limited access to specialized care, and a lack of awareness. However, increasing government initiatives to develop healthcare infrastructure and address unmet medical needs for rare diseases could gradually contribute to market expansion in select countries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Retiniti Pigmentosa Treatment Market.- RetinaGen Therapeutics

- VisionRestore Biotech

- OcularGene Solutions

- SightPath Pharmaceuticals

- OptiMed Innovations

- GeneSight Bio

- IrisBio Therapies

- ClarityVision Sciences

- Spectra Therapeutics

- NeuroRetina Corp

- Pioneer Ocular Health

- BioVisionary Pharma

- Advance Retina Technologies

- Luminis BioSolutions

- CureSight Labs

- Apex Ophthalmic Solutions

- Global Vision Sciences

- Phoenix Retina Group

- Summit BioPharma

- Elite Ocular Research

Frequently Asked Questions

Analyze common user questions about the Retiniti Pigmentosa Treatment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the primary driver of growth in the Retiniti Pigmentosa Treatment Market?

The primary driver is the significant advancement and increasing commercialization of gene and cell therapies, offering the potential for disease modification and vision restoration, moving beyond traditional symptomatic treatments.

How is AI impacting the development of Retiniti Pigmentosa treatments?

AI is revolutionizing RP treatment by enhancing diagnostic accuracy through advanced image analysis, accelerating drug discovery and development, and optimizing clinical trial design and personalized patient monitoring for better therapeutic outcomes.

What are the main challenges faced by the Retiniti Pigmentosa Treatment Market?

Key challenges include the high cost of advanced therapies, the genetic heterogeneity of Retiniti Pigmentosa making broad treatment difficult, complexities in clinical trial recruitment for rare mutations, and the need for specialized drug delivery infrastructure.

Which region is expected to dominate the Retiniti Pigmentosa Treatment Market, and why?

North America is projected to dominate the market due to robust R&D activities, substantial investment in biotech, advanced healthcare infrastructure, high patient awareness, and supportive regulatory frameworks for orphan drugs.

What types of treatments are currently available or under development for Retiniti Pigmentosa?

Currently, treatments range from symptomatic management (e.g., assistive devices) to cutting-edge therapies like gene therapy (AAV-based, CRISPR), stem cell therapy (embryonic, iPSC), and various neuroprotective or anti-inflammatory drug therapies, with a strong focus on personalized and mutation-specific approaches.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted