Retail Self scanning Solution Market

Retail Self scanning Solution Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704395 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

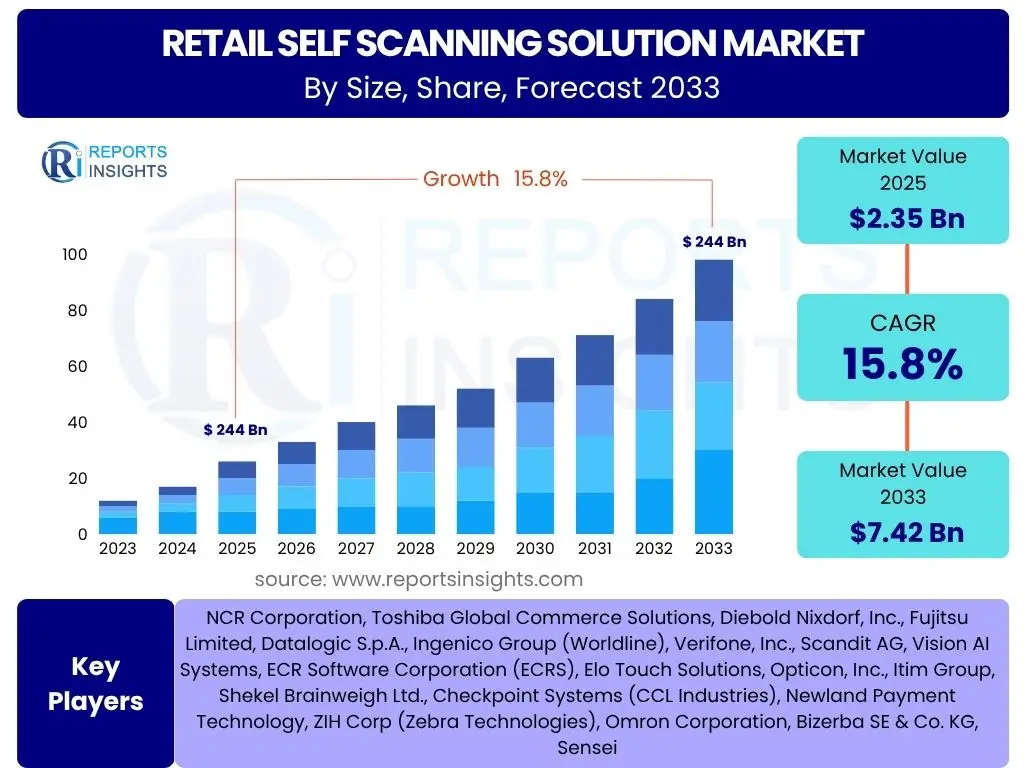

Retail Self scanning Solution Market Size

According to Reports Insights Consulting Pvt Ltd, The Retail Self scanning Solution Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2025 and 2033. This robust growth is primarily driven by retailers' increasing demand for operational efficiency, enhanced customer experience, and reduced labor costs. The market is estimated at USD 2.35 billion in 2025 and is projected to reach USD 7.42 billion by the end of the forecast period in 2033, indicating a significant expansion across various retail formats globally.

The market's expansion is further supported by the continuous technological advancements in self-scanning hardware and software, including improvements in barcode recognition, payment integration, and anti-theft measures. Consumers' growing preference for faster and more convenient shopping experiences, especially in urban areas and during peak hours, also contributes significantly to the adoption of these solutions. Retailers are actively investing in these technologies to modernize their checkout processes and free up staff for other customer-facing tasks, thereby improving overall store productivity and customer satisfaction.

Key Retail Self scanning Solution Market Trends & Insights

Common user inquiries concerning the Retail Self scanning Solution market trends revolve around the evolution of checkout technologies, consumer adoption rates, and the integration of these systems into broader retail ecosystems. Users frequently seek information on how self-scanning solutions are becoming more sophisticated, moving beyond traditional barcode scanning to encompass computer vision and AI-powered product recognition. There is also significant interest in understanding the factors driving or hindering consumer willingness to use these systems, including ease of use, perceived benefits, and security concerns. Furthermore, the market is witnessing a trend towards more versatile solutions that can be deployed across various retail formats, from large supermarkets to convenience stores, addressing diverse operational needs and space constraints.

- Shift towards frictionless shopping experiences, including scan-and-go mobile applications.

- Integration of advanced analytics for inventory management and customer behavior insights.

- Increasing deployment of hybrid self-checkout systems offering both cash and cashless options.

- Enhanced security features, such as AI-powered fraud detection and weight-based verification.

- Personalization through self-scanning interfaces, offering tailored promotions and loyalty program integration.

- Modularity and scalability of self-scanning hardware to fit diverse retail environments.

- Growing adoption in specialized retail sectors beyond groceries, including apparel and DIY stores.

AI Impact Analysis on Retail Self scanning Solution

User questions regarding the impact of AI on Retail Self scanning Solutions frequently center on its potential to revolutionize accuracy, prevent loss, and personalize the shopping experience. There is considerable interest in how AI can move self-scanning beyond manual barcode entry, enabling faster and more accurate item identification through computer vision, even for unpackaged goods. Concerns often arise about the sophistication of AI in detecting subtle forms of theft, such as produce swapping or barcode manipulation, and whether AI can truly create a 'frictionless' experience without compromising security or requiring constant human intervention. Users also inquire about AI's role in predictive maintenance for the systems and in providing real-time data for operational improvements.

The integration of artificial intelligence is fundamentally transforming the capabilities and efficacy of retail self-scanning solutions. AI algorithms can analyze vast datasets from past transactions, security footage, and product databases to identify anomalous behaviors indicative of theft, thereby significantly reducing shrinkage. Beyond loss prevention, AI enhances the user experience by enabling natural language processing for assistance, optimizing queue management through predictive analytics, and offering personalized recommendations directly at the point of sale. This intelligent automation not only streamlines operations but also elevates customer satisfaction by making the self-checkout process more intuitive, efficient, and secure. Retailers are increasingly leveraging AI to gain deeper insights into shopper preferences and operational bottlenecks, driving more informed business decisions and fostering innovation in the retail landscape.

- Enhanced theft detection through computer vision and behavioral analysis.

- Faster and more accurate product recognition, including fresh produce and un-barcoded items.

- Personalized recommendations and dynamic pricing based on shopper history.

- Predictive maintenance for self-scanning units, reducing downtime.

- Optimized queue management and staffing through real-time data analysis.

- Improved customer assistance via AI-powered chatbots or voice interfaces.

- Automated age verification for restricted items.

Key Takeaways Retail Self scanning Solution Market Size & Forecast

Common user questions about the key takeaways from the Retail Self scanning Solution market size and forecast often focus on the investment viability, the sustainability of growth, and the primary drivers that will sustain market expansion over the next decade. There's a strong interest in understanding which factors contribute most significantly to the projected CAGR and what opportunities arise for technology providers and retailers alike. Users seek concise summaries of why this market is expanding, how quickly, and what key trends underpin this growth. The core insight desired is a clear understanding of the market's trajectory and its implications for future retail operations and consumer interactions.

- Significant market expansion with a projected CAGR of 15.8% from 2025 to 2033.

- Market value poised to triple from USD 2.35 billion to USD 7.42 billion, indicating strong demand.

- Operational efficiency and improved customer experience are primary growth accelerators.

- Technological advancements, especially in AI and computer vision, are crucial for continued innovation.

- Retailers are increasingly prioritizing self-scanning solutions for labor optimization and enhanced throughput.

Retail Self scanning Solution Market Drivers Analysis

The expansion of the Retail Self scanning Solution market is primarily fueled by a confluence of economic pressures, technological advancements, and evolving consumer behaviors. Retailers face persistent challenges related to rising labor costs, a scarcity of skilled workers, and the need to optimize store operational expenses. Self-scanning solutions directly address these issues by automating the checkout process, reducing reliance on manual cashier interventions, and reallocating staff to value-added tasks such as customer service or merchandising. This strategic shift enhances store efficiency and directly impacts profitability, making self-scanning an attractive investment for retail chains seeking to streamline their operations.

Moreover, the modern consumer increasingly values speed, convenience, and autonomy in their shopping journey. Self-scanning systems provide an expedited checkout experience, particularly beneficial during peak hours, and empower shoppers with greater control over their purchases. The growing familiarity and acceptance of self-service technologies across various sectors have also lowered the adoption barrier for self-scanning, transforming it from a niche offering into a mainstream expectation. As digital literacy continues to rise globally, coupled with a preference for contactless transactions, the demand for sophisticated and user-friendly self-scanning solutions is set to escalate further.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand for operational efficiency and labor cost reduction | +4.2% | North America, Europe, Asia Pacific | Short to Mid-term (2025-2029) |

| Growing consumer preference for faster and convenient shopping experiences | +3.8% | Global | Mid to Long-term (2027-2033) |

| Technological advancements in self-scanning hardware and software (e.g., AI, computer vision) | +3.5% | Global | Mid to Long-term (2028-2033) |

| Rising adoption of contactless payment methods | +2.3% | Europe, Asia Pacific, North America | Short-term (2025-2027) |

| Focus on enhancing customer experience and reducing queue times | +2.0% | Global | Short to Mid-term (2025-2029) |

Retail Self scanning Solution Market Restraints Analysis

Despite the substantial growth opportunities, the Retail Self scanning Solution market faces several significant restraints that could impede its full potential. A primary concern for retailers is the high initial investment required for the procurement and installation of self-scanning hardware, software, and necessary infrastructure upgrades. This capital expenditure can be particularly daunting for small to medium-sized retailers (SMEs) with limited budgets, potentially slowing down broader market adoption. Furthermore, ongoing maintenance, software updates, and potential repair costs add to the total cost of ownership, making a robust return on investment (ROI) a critical consideration for prospective adopters.

Another prevalent restraint is the issue of inventory shrinkage and theft, commonly associated with self-checkout systems. While advanced AI and security features are being developed to mitigate this, the perception and reality of increased theft can deter retailers from fully embracing these solutions. Technical glitches, system malfunctions, and the need for frequent human intervention to resolve customer issues (such as age verification or item look-up) can also undermine the promised efficiency and customer satisfaction benefits. These operational challenges, if not adequately addressed by solution providers, can lead to negative customer experiences and retailer skepticism, thus restraining widespread deployment across diverse retail environments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial investment and operational costs | -2.8% | Global (especially emerging markets) | Short to Mid-term (2025-2029) |

| Concerns over inventory shrinkage and theft | -2.5% | Global | Short to Mid-term (2025-2030) |

| Technical glitches, system malfunctions, and maintenance issues | -1.9% | Global | Short-term (2025-2027) |

| Resistance from certain consumer demographics (e.g., elderly, tech-averse) | -1.5% | Developed markets (aging populations) | Long-term (2028-2033) |

| Integration complexities with existing POS and ERP systems | -1.2% | Global | Short to Mid-term (2025-2029) |

Retail Self scanning Solution Market Opportunities Analysis

The Retail Self scanning Solution market presents significant opportunities for innovation and expansion, particularly through the integration of emerging technologies and the penetration of underserved market segments. The growing trend towards omnichannel retail, where physical and digital shopping experiences converge, creates a strong demand for self-scanning solutions that seamlessly integrate with online shopping carts, loyalty programs, and personalized digital promotions. This convergence allows retailers to gather richer customer data, offer targeted incentives, and provide a truly cohesive shopping journey, unlocking new revenue streams and enhancing customer lifetime value.

Furthermore, there is immense untapped potential in emerging economies and specialized retail formats. As retail infrastructure develops in regions like Latin America, the Middle East, and parts of Asia Pacific, the adoption of modern retail technologies like self-scanning is expected to accelerate. Beyond traditional supermarkets, opportunities abound in convenience stores, pharmacies, specialized boutiques, and even pop-up shops, where smaller footprints and lower transaction volumes still benefit from the efficiency and customer autonomy offered by compact or mobile self-scanning units. The development of flexible, scalable, and cost-effective solutions tailored to these diverse environments will be key to capitalizing on these emerging market niches.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with omnichannel retail strategies and loyalty programs | +3.0% | Global | Mid to Long-term (2027-2033) |

| Expansion into emerging economies and new retail formats (e.g., convenience, specialized stores) | +2.5% | Asia Pacific, Latin America, MEA | Long-term (2029-2033) |

| Development of advanced mobile self-scanning and "scan-and-go" solutions | +2.0% | Global | Mid-term (2026-2030) |

| Leveraging AI and machine learning for enhanced personalization and predictive analytics | +1.8% | Developed markets | Long-term (2028-2033) |

| Focus on user-friendly interfaces and accessibility features to broaden adoption | +1.5% | Global | Mid-term (2026-2031) |

Retail Self scanning Solution Market Challenges Impact Analysis

The Retail Self scanning Solution market faces distinct challenges that require strategic responses from both retailers and technology providers. A significant hurdle is managing the potential for customer frustration and negative experiences, especially when systems malfunction, require manual intervention, or are perceived as overly complicated. While self-scanning offers convenience, a poorly designed or unreliable system can lead to longer queue times than traditional checkouts, resulting in customer dissatisfaction and a reluctance to use the technology again. Addressing this challenge necessitates robust system design, intuitive user interfaces, and effective on-site support to ensure a consistently positive user journey.

Another critical challenge revolves around data security and privacy, particularly with the increasing collection of customer purchase data and payment information. Retailers must ensure that self-scanning systems are compliant with global data protection regulations (like GDPR or CCPA) and employ strong encryption and security protocols to prevent data breaches. Consumer trust is paramount, and any perceived vulnerability can significantly hinder adoption. Furthermore, integrating new self-scanning solutions with existing legacy Point of Sale (POS) and Enterprise Resource Planning (ERP) systems can be complex, time-consuming, and expensive, often requiring significant IT resources and custom development, posing a barrier for retailers looking for seamless transitions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring customer satisfaction and minimizing friction in user experience | -2.0% | Global | Short to Mid-term (2025-2029) |

| Addressing security vulnerabilities and data privacy concerns | -1.8% | Global | Mid-term (2026-2031) |

| Overcoming consumer resistance and fostering adoption among hesitant demographics | -1.5% | Developed markets (aging populations, tech-skeptics) | Long-term (2028-2033) |

| Managing maintenance costs and ensuring long-term system reliability | -1.3% | Global | Short to Mid-term (2025-2029) |

| Sustaining innovation to differentiate solutions in a competitive market | -1.0% | Global | Long-term (2029-2033) |

Retail Self scanning Solution Market - Updated Report Scope

This market research report offers an in-depth analysis of the global Retail Self scanning Solution market, providing a comprehensive overview of market dynamics, competitive landscape, and future growth trajectories. It delves into the market size estimations, historical trends, and future forecasts, segmented by various solution types, components, and applications across key regional markets. The report aims to equip stakeholders with actionable insights into market drivers, restraints, opportunities, and challenges, facilitating informed strategic decision-making and investment planning within the evolving retail technology sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.35 Billion |

| Market Forecast in 2033 | USD 7.42 Billion |

| Growth Rate | 15.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NCR Corporation, Toshiba Global Commerce Solutions, Diebold Nixdorf, Inc., Fujitsu Limited, Datalogic S.p.A., Ingenico Group (Worldline), Verifone, Inc., Scandit AG, Vision AI Systems, ECR Software Corporation (ECRS), Elo Touch Solutions, Opticon, Inc., Itim Group, Shekel Brainweigh Ltd., Checkpoint Systems (CCL Industries), Newland Payment Technology, ZIH Corp (Zebra Technologies), Omron Corporation, Bizerba SE & Co. KG, Sensei |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Retail Self scanning Solution market is comprehensively segmented to provide a granular view of its diverse components and applications, enabling a detailed understanding of market dynamics across various dimensions. This segmentation facilitates targeted analysis of specific product offerings, technological configurations, and end-user adoption patterns, highlighting key growth areas and competitive landscapes within each category. Understanding these segments is crucial for stakeholders to identify niche opportunities, tailor their offerings, and formulate effective market penetration strategies.

- By Component: This segment includes the essential hardware, software, and services that collectively constitute a complete self-scanning solution. Hardware encompasses fixed kiosks, mobile scanners, and handheld devices that facilitate item scanning and payment. Software solutions involve Point of Sale (POS) software, inventory management systems, and data analytics tools that power the self-checkout process and provide actionable insights. Services cover the crucial aspects of installation, ongoing maintenance and support, and expert consulting to ensure optimal system deployment and performance.

- By Type: This category differentiates solutions based on their operational model. Standalone Self-Checkout systems are traditional fixed units. Mobile Self-Scanning solutions allow customers to scan items using their own smartphones (BYOD) or retailer-provided handheld devices. Hybrid Self-Checkout Systems offer flexibility, supporting both self-service and assisted checkout options, catering to varied customer preferences and operational needs.

- By Application: The application segment illustrates the diverse retail environments where self-scanning solutions are deployed. This includes large-format stores like Supermarkets & Hypermarkets, smaller outlets such as Convenience Stores and Pharmacies, and specialized retailers like Department Stores, Specialty Stores, and DIY Stores. The versatility of these solutions allows for adoption across a broad spectrum of retail formats, each with unique requirements and customer flows.

- By Payment Method: This segmentation highlights the various payment options supported by self-scanning systems. It covers traditional Card Payments (Credit/Debit), increasingly popular Mobile Payments (NFC, QR Codes), Digital Wallets for enhanced convenience, and Cash options to cater to all consumer preferences and payment habits. The evolution of payment methods significantly influences the design and integration requirements of self-scanning technologies.

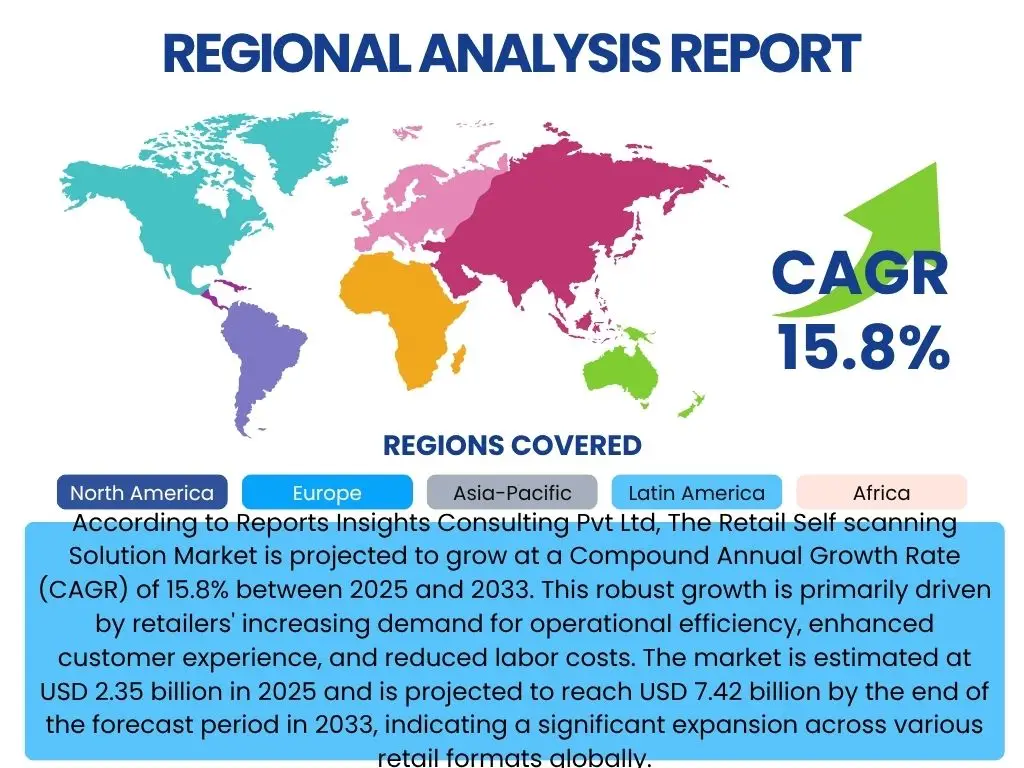

Regional Highlights

- North America: This region represents a mature market with high adoption rates, driven by a strong focus on enhancing customer experience, reducing labor costs, and early adoption of technological innovations. The presence of major retail chains and a digitally-savvy consumer base contribute to sustained growth, particularly in urban and suburban areas.

- Europe: Characterized by a mix of mature markets (Western Europe) and developing ones (Eastern Europe), this region shows robust growth fueled by increasing consumer demand for convenience and retailers' efforts to improve operational efficiency. Regulatory frameworks around data privacy and payment security also shape market development.

- Asia Pacific (APAC): Expected to be the fastest-growing region, driven by rapid urbanization, the expansion of modern retail infrastructure, and a booming e-commerce sector. Emerging economies within APAC are investing heavily in retail automation to cater to a growing middle class and tech-literate population.

- Latin America: This region is experiencing nascent but accelerating growth, spurred by the modernization of retail landscapes and increasing foreign investment. Opportunities lie in catering to diverse retail formats and adapting solutions to local payment preferences and infrastructure.

- Middle East and Africa (MEA): Growth in MEA is primarily influenced by significant investments in retail infrastructure in the GCC countries and increasing disposable incomes. The adoption of self-scanning solutions is gaining traction as retailers seek to enhance competitiveness and improve service quality in growing retail sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Retail Self scanning Solution Market.- NCR Corporation

- Toshiba Global Commerce Solutions

- Diebold Nixdorf, Inc.

- Fujitsu Limited

- Datalogic S.p.A.

- Ingenico Group (Worldline)

- Verifone, Inc.

- Scandit AG

- Vision AI Systems

- ECR Software Corporation (ECRS)

- Elo Touch Solutions

- Opticon, Inc.

- Itim Group

- Shekel Brainweigh Ltd.

- Checkpoint Systems (CCL Industries)

- Newland Payment Technology

- ZIH Corp (Zebra Technologies)

- Omron Corporation

- Bizerba SE & Co. KG

- Sensei

Frequently Asked Questions

Analyze common user questions about the Retail Self scanning Solution market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Retail Self scanning Solution Market?

The Retail Self scanning Solution Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2025 and 2033, reaching an estimated value of USD 7.42 billion by 2033.

How does AI impact Retail Self scanning Solutions?

AI significantly impacts self-scanning by enabling advanced theft detection, faster product recognition, personalized customer experiences, and predictive maintenance for systems, enhancing efficiency and security.

What are the primary drivers for the adoption of Retail Self scanning Solutions?

Key drivers include the increasing demand for operational efficiency, labor cost reduction, growing consumer preference for faster and convenient shopping, and continuous technological advancements in scanning and payment systems.

What challenges does the Retail Self scanning Solution Market face?

Challenges include high initial investment costs, concerns over inventory shrinkage and theft, potential technical glitches, and ensuring a consistently positive and user-friendly customer experience to maintain adoption rates.

Which regions are leading in the adoption of Retail Self scanning Solutions?

North America and Europe currently lead in adoption, driven by mature retail markets. Asia Pacific is projected to be the fastest-growing region due to rapid modernization of its retail infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted