Residential Used Water Meter Market

Residential Used Water Meter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704535 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

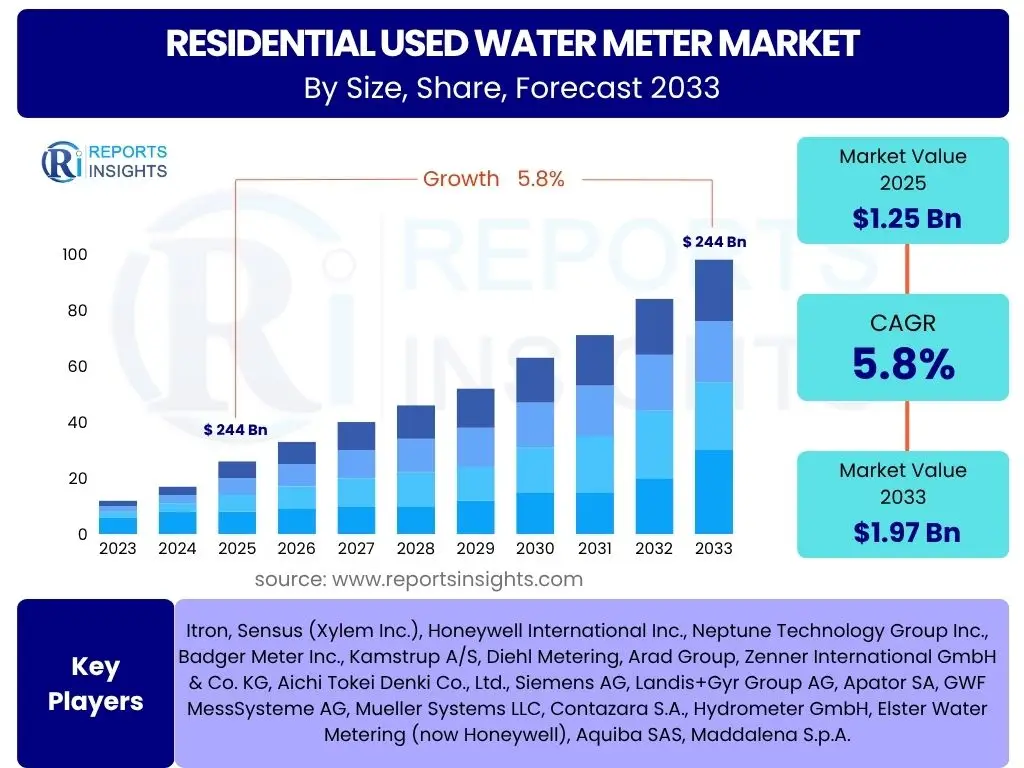

Residential Used Water Meter Market Size

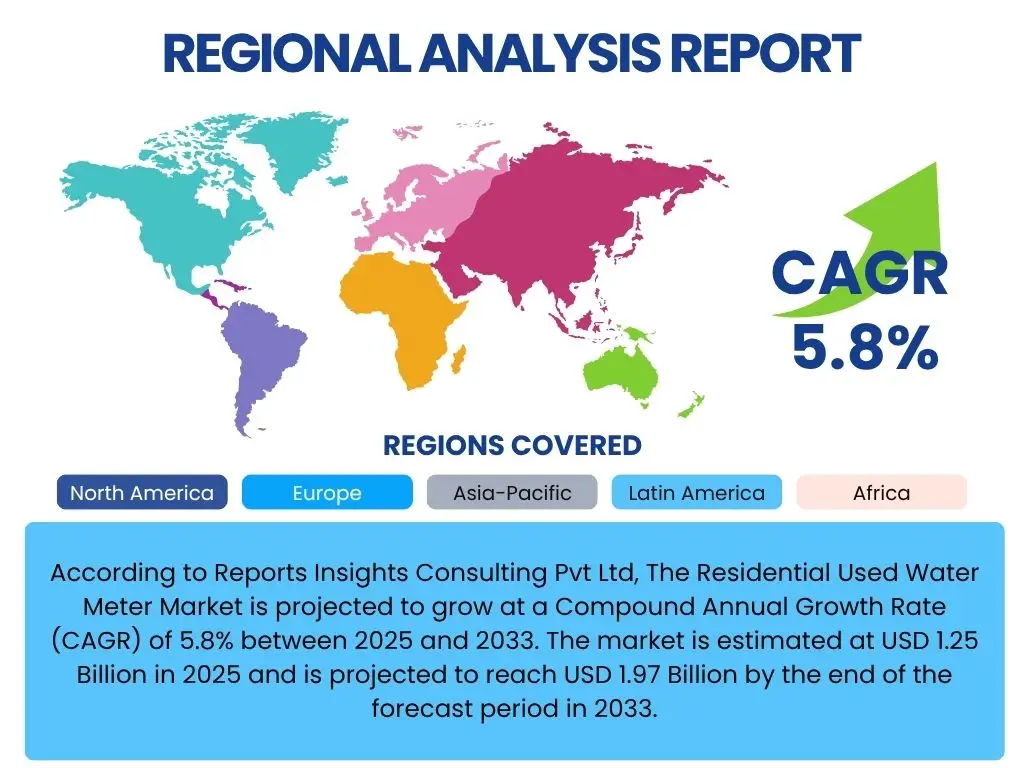

According to Reports Insights Consulting Pvt Ltd, The Residential Used Water Meter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 1.97 Billion by the end of the forecast period in 2033.

Key Residential Used Water Meter Market Trends & Insights

The residential used water meter market is currently experiencing significant shifts driven by technological advancements, increasing awareness of water conservation, and evolving regulatory landscapes. Common user inquiries often revolve around the adoption of smart metering technologies, the integration of Internet of Things (IoT) solutions for enhanced data collection, and the demand for more accurate and reliable metering systems to combat water loss and optimize billing. Furthermore, there is growing interest in solutions that provide consumers with real-time water usage data to promote more responsible consumption habits.

Another prevalent theme in user questions concerns the environmental impact and sustainability aspects of water metering, particularly regarding how new technologies can contribute to reducing water waste and improving overall water resource management. Users are also interested in the longevity and maintenance requirements of modern water meters, seeking solutions that offer durability and lower operational costs over time. The transition from traditional mechanical meters to advanced digital and smart meters is a key trend, reflecting a broader industry move towards intelligent utility management and greater operational efficiency.

- Smart Meter Adoption: Accelerating integration of Automatic Meter Reading (AMR) and Advanced Metering Infrastructure (AMI) for remote monitoring and data collection.

- IoT Integration: Increased use of IoT platforms for real-time water usage insights, leak detection, and predictive maintenance.

- Water Conservation Focus: Growing demand for accurate meters to support water efficiency programs and reduce non-revenue water.

- Consumer Engagement: Development of user-friendly interfaces and mobile applications providing homeowners with direct access to their consumption data.

- Data Analytics: Utilization of big data analytics to identify consumption patterns, detect anomalies, and optimize water distribution.

- Sustainable Metering Solutions: Emphasis on durable materials and eco-friendly manufacturing processes for water meters.

AI Impact Analysis on Residential Used Water Meter

The integration of Artificial Intelligence (AI) is set to profoundly transform the residential water meter sector, moving beyond basic measurement to intelligent water management. Common user questions frequently address how AI can enhance efficiency, improve leak detection, and optimize water resource allocation. Users are keen to understand AI's capability in processing vast amounts of meter data to identify abnormal consumption patterns, predict infrastructure failures, and even forecast future demand with greater accuracy than traditional methods. The expectation is that AI will enable proactive rather than reactive management of residential water networks.

Further concerns and expectations highlight AI's potential to personalize water usage insights for homeowners, offering tailored advice for conservation or alerting them to potential issues like hidden leaks. There is also significant interest in how AI can streamline billing processes by ensuring greater accuracy and reducing the need for manual interventions, thereby improving customer satisfaction. While the benefits are clear, users also ponder the data privacy implications and the computational resources required for widespread AI deployment in residential water systems, indicating a need for secure and scalable solutions.

- Predictive Maintenance: AI algorithms analyze meter data to predict potential failures or maintenance needs before they occur.

- Advanced Leak Detection: AI models identify subtle anomalies in water flow patterns, pinpointing leaks more accurately and rapidly.

- Optimized Billing & Usage Insights: AI processes consumption data to provide precise billing and personalized insights for consumers to manage their water use.

- Demand Forecasting: AI-driven analytics improve the accuracy of water demand predictions, aiding utilities in resource allocation and infrastructure planning.

- Anomaly Detection: AI systems automatically flag unusual water consumption, helping identify potential issues like burst pipes or tampering.

- Resource Optimization: AI supports efficient water distribution by analyzing usage trends and optimizing pump schedules and pressure management.

Key Takeaways Residential Used Water Meter Market Size & Forecast

The Residential Used Water Meter market is poised for consistent growth throughout the forecast period, driven primarily by the global imperative for water conservation, advancements in smart metering technology, and increasing government initiatives aimed at modernizing aging water infrastructure. Key insights from the market forecast indicate a strong shift towards digital and smart meter solutions, which offer utilities and consumers unparalleled data accuracy and real-time insights into water consumption. This transition is not merely about replacing old meters but about implementing comprehensive solutions that contribute to overall water efficiency and sustainability.

Furthermore, the market's trajectory suggests that investment in robust data analytics platforms and integrated IoT ecosystems will be crucial for stakeholders. The ability to leverage meter data for predictive analysis, leak detection, and personalized consumer engagement will differentiate market leaders. Despite initial investment costs, the long-term benefits of reduced non-revenue water, improved operational efficiency, and enhanced customer satisfaction are expected to fuel continued adoption. The market's future will be characterized by greater connectivity, intelligence, and a focus on resilience in water management systems.

- Steady Market Expansion: Consistent growth projected, fueled by technology adoption and environmental concerns.

- Smart Meter Dominance: Shift from mechanical to smart meters (AMR/AMI) as a key growth driver.

- Water Loss Reduction: Significant focus on reducing non-revenue water through accurate metering and data insights.

- Regulatory Influence: Government mandates and incentives for efficient water management accelerating market development.

- Enhanced Consumer Awareness: Greater transparency in water usage empowering consumers to conserve.

- Data-Driven Decisions: Increasing reliance on meter data for operational optimization, infrastructure planning, and proactive maintenance.

Residential Used Water Meter Market Drivers Analysis

The residential used water meter market is significantly propelled by a confluence of factors centered around resource management, technological evolution, and regulatory impetus. One primary driver is the escalating global concern over water scarcity, which mandates efficient usage and accurate measurement to conserve this vital resource. Governments and utility providers worldwide are increasingly implementing policies that promote the reduction of water loss and the adoption of technologies that enable precise monitoring of consumption. This push for conservation directly translates into demand for advanced, reliable water meters in residential settings.

Another crucial driver is the rapid advancement in smart technology and IoT, making intelligent water meters more accessible and cost-effective. These technologies offer capabilities like remote reading, real-time data analysis, and immediate leak detection, which were previously unavailable or too expensive for widespread residential deployment. The desire to improve operational efficiency for utility companies, reduce manual labor associated with meter reading, and provide consumers with greater transparency over their water usage also significantly fuels market growth. Furthermore, aging water infrastructure in many developed regions necessitates upgrades, presenting a substantial opportunity for the replacement of older, less efficient meters with modern counterparts.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Water Scarcity & Conservation Needs | +1.5% | Global, particularly MEA, Asia Pacific | 2025-2033 |

| Advancements in Smart Metering & IoT Technologies | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Aging Water Infrastructure & Replacement Cycles | +1.0% | North America, Europe | 2025-2030 |

| Favorable Government Regulations & Initiatives | +0.8% | Global | 2025-2033 |

Residential Used Water Meter Market Restraints Analysis

Despite the strong growth drivers, the residential used water meter market faces several notable restraints that could temper its expansion. One significant hurdle is the high initial capital expenditure associated with the deployment of advanced smart water meters and their accompanying infrastructure. While the long-term benefits, such as reduced non-revenue water and operational efficiencies, are evident, the upfront cost can be prohibitive for smaller municipalities or utilities with limited budgets. This financial barrier often leads to slower adoption rates, particularly in developing regions where infrastructure investments are already constrained.

Another restraint involves the complexities of data privacy and cybersecurity concerns related to smart meters. As these devices collect and transmit sensitive consumption data, ensuring the security and privacy of this information is paramount. Public skepticism or resistance to smart meter adoption due to perceived privacy intrusions can slow down rollout programs. Furthermore, a lack of standardized communication protocols and interoperability issues between different meter technologies and utility systems can create integration challenges, leading to higher implementation costs and a fragmented market landscape, thereby impeding seamless upgrades and widespread adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -0.9% | Global, particularly Emerging Markets | 2025-2033 |

| Data Privacy & Cybersecurity Concerns | -0.7% | North America, Europe | 2025-2033 |

| Lack of Standardization & Interoperability Issues | -0.6% | Global | 2025-2030 |

| Consumer Resistance to New Technologies | -0.4% | Specific Pockets in Developed Nations | 2025-2028 |

Residential Used Water Meter Market Opportunities Analysis

The residential used water meter market presents a multitude of growth opportunities stemming from technological innovation, expanding infrastructure needs, and the evolving demands of utility management. A significant opportunity lies in the burgeoning demand for advanced analytics and software solutions that can transform raw meter data into actionable insights. Utilities are increasingly seeking solutions beyond mere data collection, focusing on platforms that offer leak detection, predictive maintenance, and personalized consumption reports for homeowners. This shift creates a strong market for software and service providers specializing in smart water management ecosystems.

Geographically, immense opportunities exist in emerging economies within the Asia Pacific, Latin America, and Middle East & Africa regions. These areas are experiencing rapid urbanization, population growth, and significant investments in new residential infrastructure, often lacking established water metering systems. This greenfield development provides a fertile ground for the direct adoption of smart metering technologies, bypassing the need to replace outdated mechanical meters. Furthermore, the retrofitting market in developed countries, where millions of legacy meters are due for replacement, offers a sustained revenue stream for manufacturers. The integration of water meters with broader smart home automation systems also represents a future growth avenue, enabling comprehensive resource management at the household level.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Demand for Advanced Data Analytics & Software Solutions | +1.3% | Global | 2025-2033 |

| Expansion in Emerging Economies & New Construction | +1.1% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Retrofitting & Replacement of Legacy Meters | +0.9% | North America, Europe | 2025-2033 |

| Integration with Smart Home & Building Automation | +0.7% | Developed Regions | 2028-2033 |

Residential Used Water Meter Market Challenges Impact Analysis

The residential used water meter market faces several complex challenges that necessitate strategic responses from industry players and policymakers. One significant challenge is the ongoing issue of cybersecurity threats, which could compromise the integrity and privacy of meter data. As more meters become interconnected and transmit sensitive information, ensuring robust security protocols and safeguarding against potential cyberattacks becomes critical. A major breach could erode public trust and severely hinder smart meter adoption programs.

Another prominent challenge involves the lack of skilled labor and technical expertise required for the installation, maintenance, and data management of advanced smart metering systems. Many traditional utility workforces may not possess the necessary IT and data analytics skills, leading to deployment delays or suboptimal system performance. Furthermore, supply chain disruptions, particularly those affecting the availability of electronic components and semiconductors, can impact production schedules and increase manufacturing costs. Regulatory hurdles, including varied local ordinances and slow approval processes for new technologies, also pose a challenge, creating inconsistencies in market penetration and adoption rates across different regions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Risks & Data Privacy Concerns | -0.8% | Global | 2025-2033 |

| Skilled Labor Shortage & Training Needs | -0.6% | Global | 2025-2030 |

| Supply Chain Disruptions & Component Shortages | -0.5% | Global | 2025-2027 |

| Regulatory Hurdles & Slow Approval Processes | -0.4% | Specific Countries/Regions | 2025-2033 |

Residential Used Water Meter Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Residential Used Water Meter Market, covering market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report offers a detailed competitive landscape, profiles of leading market players, and insights into the technological advancements shaping the industry. It aims to deliver strategic intelligence for stakeholders seeking to understand market dynamics and make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 1.97 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Itron, Sensus (Xylem Inc.), Honeywell International Inc., Neptune Technology Group Inc., Badger Meter Inc., Kamstrup A/S, Diehl Metering, Arad Group, Zenner International GmbH & Co. KG, Aichi Tokei Denki Co., Ltd., Siemens AG, Landis+Gyr Group AG, Apator SA, GWF MessSysteme AG, Mueller Systems LLC, Contazara S.A., Hydrometer GmbH, Elster Water Metering (now Honeywell), Aquiba SAS, Maddalena S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Residential Used Water Meter market is comprehensively segmented to provide granular insights into its diverse components and sub-sectors. This detailed segmentation allows for a precise understanding of market dynamics, identifying key growth areas, and analyzing specific technology and application trends. The primary segmentation categories include meter type, underlying technology, specific application within residential settings, communication technologies utilized, and the various end-users benefiting from these systems.

Analyzing these segments reveals shifts in consumer preferences, technological advancements driving new product development, and the impact of different communication infrastructures on market adoption. For instance, the transition from traditional mechanical meters to advanced smart meters with robust communication capabilities is a central theme across all segments, reflecting the industry's move towards intelligence and connectivity. This multi-faceted segmentation provides a holistic view of the market's structure and its future evolution.

- By Type:

- Mechanical Water Meters: Traditional meters relying on mechanical parts for measurement.

- Smart Water Meters:

- Automatic Meter Reading (AMR): One-way communication for remote data collection.

- Advanced Metering Infrastructure (AMI): Two-way communication for real-time data, control, and advanced functionalities.

- By Technology:

- Ultrasonic Water Meters: Utilize sound waves for highly accurate, non-moving part measurement.

- Electromagnetic Water Meters: Employ electromagnetic fields, suitable for various water qualities.

- Volumetric Water Meters: Measure by displacing a known volume of water, offering high accuracy.

- Single Jet Water Meters: Feature a single jet of water impacting an impeller.

- Multi Jet Water Meters: Direct multiple jets of water at an impeller, enhancing accuracy and durability.

- By Application:

- Single-Family Homes: Water meters installed in individual residential houses.

- Multi-Family Dwellings (Apartments/Condos): Meters used in multi-unit residential buildings, often with sub-metering.

- By Communication Technology:

- LoRaWAN: Low-power, wide-area network protocol for IoT devices.

- NB-IoT: Narrowband IoT, a cellular technology for low-power IoT devices.

- Cellular (2G/3G/4G/5G): Utilizes existing mobile network infrastructure.

- Radio Frequency (RF): Wireless communication for short to medium ranges.

- Wired (M-Bus): Traditional wired communication protocol, often used in multi-dwelling units.

- By End User:

- Utilities: Public or private organizations responsible for water supply and distribution.

- Municipalities: Local government bodies managing water services.

- Property Management Companies: Companies managing residential properties that often handle sub-metering and billing.

Regional Highlights

- North America: This region is characterized by aging water infrastructure requiring significant modernization and replacement initiatives. Strong governmental support for smart city projects and water conservation mandates drives the adoption of advanced metering solutions. The presence of major market players and early technology adopters further contributes to market growth.

- Europe: Europe exhibits a mature market with a high focus on sustainability, strict environmental regulations, and energy efficiency. Countries like Germany and the UK are leading in smart meter deployments, driven by regulatory frameworks promoting precise water billing and leak detection to comply with water efficiency targets.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid urbanization, significant new residential construction, and increasing disposable incomes. Countries such as China, India, and Southeast Asian nations are investing heavily in new water infrastructure and smart city development, leading to widespread adoption of new water metering technologies.

- Latin America: This region faces significant challenges related to water scarcity and non-revenue water, creating a strong impetus for adopting efficient water management solutions. Investments in infrastructure development and the need to improve billing accuracy are key drivers for the residential water meter market here.

- Middle East and Africa (MEA): MEA is experiencing severe water stress, making water conservation a top priority. Government initiatives to improve water supply efficiency and reduce losses, coupled with investments in new residential developments, are accelerating the demand for advanced water metering solutions across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Residential Used Water Meter Market.- Itron

- Sensus (Xylem Inc.)

- Honeywell International Inc.

- Neptune Technology Group Inc.

- Badger Meter Inc.

- Kamstrup A/S

- Diehl Metering

- Arad Group

- Zenner International GmbH & Co. KG

- Aichi Tokei Denki Co., Ltd.

- Siemens AG

- Landis+Gyr Group AG

- Apator SA

- GWF MessSysteme AG

- Mueller Systems LLC

- Contazara S.A.

- Hydrometer GmbH

- Elster Water Metering (now Honeywell)

- Aquiba SAS

- Maddalena S.p.A.

Frequently Asked Questions

What is a smart water meter and how does it benefit homeowners?

A smart water meter is a digital device that measures water consumption and transmits data wirelessly to the utility company and often to the homeowner. It benefits homeowners by providing real-time usage insights, enabling early leak detection, improving billing accuracy, and supporting water conservation efforts through greater transparency.

Why is water metering important for residential properties?

Water metering for residential properties is crucial for accurate billing, promoting water conservation by making consumption visible, identifying leaks and inefficiencies, and supporting effective water resource management by utilities. It helps reduce non-revenue water and ensures fair usage.

What are the primary differences between mechanical and smart water meters?

Mechanical water meters use physical gears and impellers to measure water flow, requiring manual readings. Smart water meters use electronic sensors and wireless communication for automated, remote data collection, offering real-time insights, leak detection, and two-way communication capabilities not available with mechanical meters.

How do smart water meters contribute to water conservation?

Smart water meters contribute to water conservation by providing homeowners with immediate feedback on their water usage, which encourages more mindful consumption. They also enable utilities to detect leaks and bursts quickly, minimizing water loss from infrastructure, and support demand management programs.

What are the future trends for residential water metering technology?

Future trends for residential water metering technology include enhanced integration with IoT and AI for predictive analytics, further miniaturization and increased accuracy of sensors, improved battery life, and greater interoperability with smart home systems. Emphasis will also be on robust cybersecurity and sustainable materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted