Refractory Cement Market

Refractory Cement Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700116 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

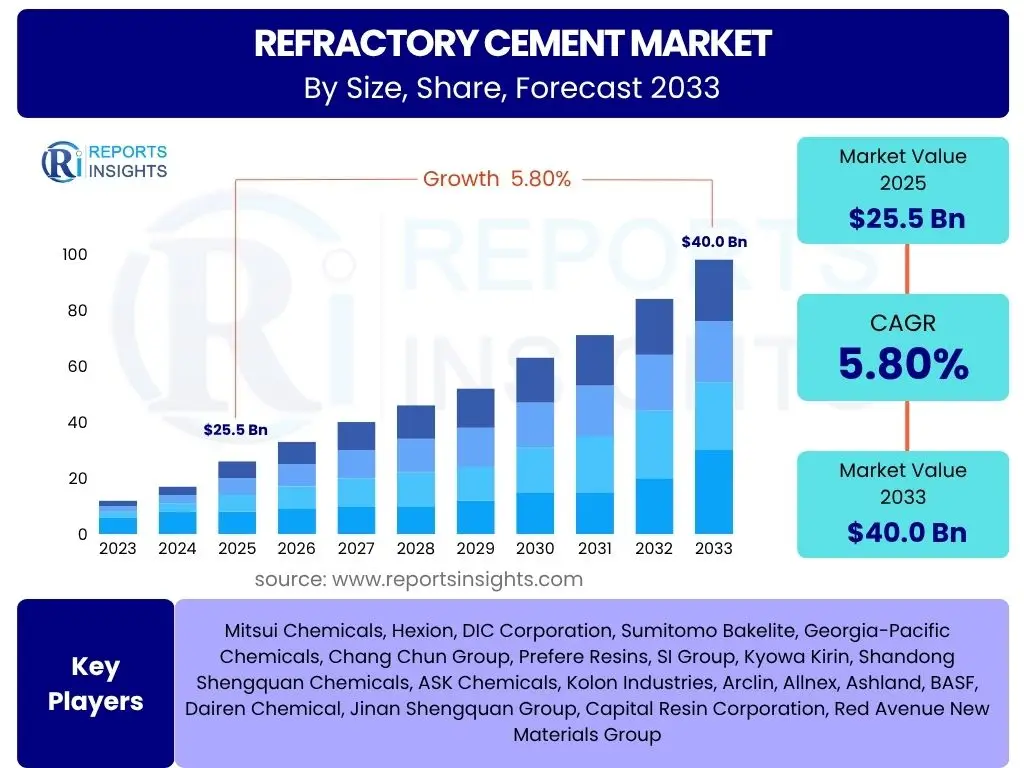

Refractory Cement Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, reaching USD 25.5 Billion in 2025 and is projected to grow by USD 40.0 Billion by 2033 the end of the forecast period.

Key Refractory Cement Market Trends & Insights

The refractory cement market is currently undergoing significant transformation, driven by evolving industrial demands and technological advancements. Key trends shaping this sector include a growing emphasis on high-performance materials capable of withstanding extreme temperatures and corrosive environments, alongside an increasing adoption of sustainable manufacturing practices. The industry is also witnessing a surge in research and development activities focused on innovative compositions to enhance durability and energy efficiency in various high-temperature applications. Furthermore, the expansion of industrial infrastructure in developing economies is fueling demand for advanced refractory solutions, while the integration of digital technologies is optimizing production processes and supply chain management.

- Increasing demand for energy-efficient refractory materials.

- Technological advancements in material composition and manufacturing processes.

- Growing adoption in waste-to-energy and alternative fuel applications.

- Focus on sustainable and environmentally friendly refractory solutions.

- Rising industrialization and infrastructure development in emerging economies.

- Shift towards specialized and high-performance refractory products.

AI Impact Analysis on Refractory Cement

Artificial Intelligence (AI) is poised to revolutionize various aspects of the refractory cement market, from raw material sourcing and quality control to production optimization and predictive maintenance. AI-driven analytics can significantly enhance the precision of material blending, reducing waste and improving product consistency. Furthermore, machine learning algorithms can analyze performance data to predict equipment failures in high-temperature industrial settings, enabling proactive maintenance and minimizing downtime. This transformative technology also offers immense potential for accelerating the discovery and development of novel refractory compositions by simulating material properties and performance under diverse conditions, thereby driving innovation and efficiency across the value chain.

- AI-driven optimization of raw material sourcing and inventory management.

- Enhanced quality control through AI-powered anomaly detection in production.

- Predictive maintenance for refractory linings and industrial furnaces, reducing downtime.

- Accelerated R&D for new material formulations using machine learning.

- Improved process efficiency and energy consumption monitoring in manufacturing plants.

- Data-driven insights for market forecasting and strategic decision-making.

Key Takeaways Refractory Cement Market Size & Forecast

- The global refractory cement market is projected for substantial growth, indicating robust demand across various industrial sectors.

- The market size is anticipated to reach USD 25.5 Billion in 2025, signifying its current valuation and expansive reach.

- By 2033, the market is forecasted to grow to USD 40.0 Billion, highlighting a significant expansion potential over the forecast period.

- This growth trajectory is underpinned by a Compound Annual Growth Rate (CAGR) of 5.8% from 2025 to 2033.

- Key growth drivers include escalating demand from steel, cement, glass, and non-ferrous metal industries, alongside increasing focus on energy efficiency and infrastructure development.

- Emerging economies, particularly in Asia Pacific, are expected to be pivotal in driving market expansion due to rapid industrialization and urbanization.

- Technological advancements in refractory material formulations and manufacturing processes will contribute significantly to market evolution and performance improvements.

Refractory Cement Market Drivers Analysis

The refractory cement market is propelled by a confluence of macroeconomic trends and industry-specific demands. A primary driver is the sustained growth in core industrial sectors such as steel, cement, glass, and non-ferrous metals, all of which are heavily reliant on high-temperature processing units that require durable refractory linings. The increasing global population and rapid urbanization are fueling demand for infrastructure development, leading to higher production volumes in these industries. Additionally, stringent regulations and a growing emphasis on energy efficiency across manufacturing processes necessitate the adoption of advanced, high-performance refractory materials that can minimize heat loss and extend equipment lifespan, thereby reducing operational costs and environmental impact. This demand for more efficient and resilient materials continues to expand the market for refractory cement.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Steel and Non-Ferrous Metals Industry | +1.5% | Asia Pacific, Europe, North America | Short to Medium Term |

| Increasing Demand from Cement and Ceramics Industry | +1.2% | Global, particularly Asia Pacific, Latin America | Short to Medium Term |

| Focus on Energy Efficiency and Cost Reduction | +1.0% | Developed Economies, Europe, North America | Medium to Long Term |

| Rapid Infrastructure Development and Urbanization | +0.8% | Emerging Economies, Asia Pacific, Africa | Short to Medium Term |

| Technological Advancements in Refractory Materials | +0.7% | Global, key R&D hubs | Medium to Long Term |

Refractory Cement Market Restraints Analysis

Despite robust growth drivers, the refractory cement market faces several significant restraints that could impede its expansion. One major challenge is the inherent volatility of raw material prices, including bauxite, alumina, and various minerals, which are susceptible to supply chain disruptions, geopolitical events, and fluctuating demand from other industries. This price instability can directly impact manufacturing costs and profitability for refractory cement producers. Furthermore, the increasing stringency of environmental regulations regarding emissions, waste disposal, and energy consumption in industrial processes poses a significant compliance burden. Adhering to these regulations often requires substantial investments in new technologies and processes, which can limit market growth, especially for smaller players. Additionally, the high initial investment required for installing and maintaining refractory linings can be a deterrent for some end-use industries, particularly when considering alternative materials with lower upfront costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8% | Global | Short to Medium Term |

| Stringent Environmental Regulations | -0.7% | Europe, North America, specific Asian countries | Medium to Long Term |

| High Initial Investment and Maintenance Costs | -0.5% | Global, particularly SMEs | Short to Medium Term |

| Competition from Alternative Materials | -0.4% | Global | Medium Term |

Refractory Cement Market Opportunities Analysis

Significant opportunities exist within the refractory cement market, particularly driven by innovation and expansion into new applications. The continuous development of advanced refractory materials, including low-cement and ultra-low cement castables, offers enhanced performance characteristics such as higher strength, better thermal shock resistance, and longer service life, creating new avenues for market penetration. Furthermore, the increasing global emphasis on waste management and energy recovery is driving the adoption of refractory cement in waste-to-energy plants and biomass gasifiers, where extreme temperatures and corrosive environments demand robust lining solutions. The expansion into niche applications, such as specialized furnaces for advanced materials processing and hydrogen production, also presents untapped potential. Lastly, growing awareness and initiatives around green building and sustainable manufacturing practices create a demand for refractory solutions with reduced environmental footprints, opening opportunities for eco-friendly product development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Refractory Materials | +1.3% | Global, R&D focused regions | Medium to Long Term |

| Increasing Adoption in Waste-to-Energy Plants | +1.0% | Europe, Asia Pacific, North America | Short to Medium Term |

| Expansion into Niche and Specialized Applications | +0.9% | Global, specialized industrial sectors | Medium to Long Term |

| Growth in Green Building and Sustainable Manufacturing | +0.8% | Developed Economies | Medium Term |

Refractory Cement Market Challenges Impact Analysis

The refractory cement market is not without its challenges, which can influence its growth trajectory and operational efficiency. A notable concern is the persistent shortage of skilled labor required for the precise installation and maintenance of refractory linings. The specialized nature of this work demands specific expertise, and a lack of trained professionals can lead to installation errors, reduced lining lifespan, and increased operational costs for end-users. Furthermore, the safe and environmentally compliant disposal of spent refractory materials presents a significant challenge, as these materials often contain hazardous components and require specialized waste management solutions, adding to overall project expenses. Intense market competition, characterized by numerous regional and global players, exerts downward pressure on pricing and profit margins, compelling companies to continuously innovate and optimize their processes. Lastly, geopolitical instability and unforeseen global events can lead to significant supply chain disruptions, impacting the availability and cost of critical raw materials and finished products, thereby challenging market stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Skilled Labor for Installation | -0.6% | Global, particularly developed regions | Medium to Long Term |

| Managing Waste Disposal and Recycling | -0.5% | Global, stricter in Europe, North America | Medium Term |

| Intense Market Competition and Price Pressures | -0.4% | Global | Short to Medium Term |

| Supply Chain Disruptions and Geopolitical Risks | -0.3% | Global, especially for key raw materials | Short Term (variable) |

Refractory Cement Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the global refractory cement market, providing critical insights into its current state, historical performance, and future projections. The report delves into market dynamics, identifying key drivers, restraints, opportunities, and challenges that influence market growth. It also presents a detailed segmentation analysis, regional breakdown, and profiles of leading market players, equipping stakeholders with actionable intelligence for strategic decision-making. The scope includes a thorough examination of market size and forecast, technological advancements, and the impact of emerging trends on the industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 40.0 Billion |

| Growth Rate | 5.8% (2025 to 2033) |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Vesuvius plc, RHI Magnesita, Saint-Gobain S.A., Krosaki Harima Corporation, Shinagawa Refractories Co., Ltd., Imerys S.A., Allied Mineral Products, Inc., Morgan Advanced Materials plc, Refratechnik Group, Calderys, Resco Products, Inc., Puyang Refractories Group Co., Ltd., Beijing LIRR High Temperature Materials Co., Ltd., J.R. Refractory Materials Co., Ltd., Qingdao Refractory Co., Ltd., Kerui Refractories, HarbisonWalker International (HWI), Minerals Technologies Inc. (MinTeC), Industrial Refractory Products (IRP), Shandong Luyang Refractories Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The refractory cement market is comprehensively segmented to provide a granular view of its various components, enabling a detailed analysis of market dynamics across different product types, forms, end-use industries, and applications. This segmentation allows for a precise understanding of specific market niches and their respective growth trajectories, offering valuable insights into demand patterns and technological preferences. The detailed breakdown supports strategic planning by identifying high-growth segments and areas requiring focused attention within the broader refractory cement landscape.

- By Type: This segment categorizes refractory cements based on their chemical composition and primary raw materials.

- Calcium Aluminate Cement: Known for its high early strength and resistance to chemical attack, widely used in various industrial applications.

- Magnesium Aluminate Cement: Valued for its excellent refractoriness and slag resistance, often used in steel and cement industries.

- Others: Includes specialized formulations like silica cement, chromite cement, and mullite cement, designed for specific high-performance requirements.

- By Form: This segment differentiates refractory cement products by their density and thermal properties.

- Normal Weight: Refers to standard density refractory cements, offering robust mechanical strength and thermal stability.

- Lightweight: Designed for lower thermal conductivity, providing enhanced insulation properties and reducing energy consumption.

- By End-Use Industry: This segment identifies the major industrial sectors consuming refractory cement.

- Iron & Steel: Largest consumer, used in blast furnaces, ladles, tundishes, and continuous casting.

- Cement & Lime: Utilized in rotary kilns, preheaters, and coolers for high temperature resistance.

- Glass: Essential for furnace linings, regenerators, and feeders in glass melting processes.

- Non-ferrous Metals: Applied in furnaces for aluminum, copper, and other metal smelting and refining.

- Petrochemical: Used in reformers, heaters, and reactors in the oil and gas industry.

- Energy & Waste Incineration: Critical for linings in boilers, incinerators, and waste-to-energy facilities.

- Others: Includes applications in ceramics, fertilizers, chemical processing, and power generation.

- By Application: This segment outlines the specific ways refractory cement products are applied.

- Linings: Primary application for furnaces, kilns, and other high-temperature vessels.

- Mortars: Used as bonding agents for refractory bricks and shapes.

- Coatings: Applied as protective layers to enhance surface properties and extend lifespan.

- Castables: Versatile application method for forming monolithic structures and repairs.

- Bricks: Refractory cement is often a component in the binding of pre-formed refractory bricks.

Regional Highlights

The global refractory cement market exhibits diverse growth patterns across various regions, influenced by industrial development, regulatory frameworks, and technological adoption.- Asia Pacific (APAC): This region dominates the refractory cement market, driven by robust industrial growth in countries like China, India, and Southeast Asian nations. Rapid urbanization, significant infrastructure development, and expanding steel, cement, and glass manufacturing sectors are the primary catalysts. China and India, with their massive industrial bases, are key demand centers, constantly expanding production capacities that require high volumes of refractory materials. The focus on enhancing energy efficiency in these industrial processes also fuels the demand for advanced refractory cement solutions.

- Europe: The European market for refractory cement is characterized by a strong emphasis on sustainability, technological innovation, and stringent environmental regulations. While traditional industries like steel and cement are mature, the region sees demand driven by upgrades to existing facilities, adoption of energy-efficient technologies, and growth in specialized applications such as waste-to-energy plants. Countries like Germany, France, and Italy are at the forefront of adopting advanced and eco-friendly refractory solutions, leveraging research and development for superior material performance and circular economy principles.

- North America: This region presents a stable market for refractory cement, primarily supported by the modernization of existing industrial infrastructure and a strong focus on high-performance and specialty refractory products. The steel, petrochemical, and glass industries are significant consumers. Investments in advanced manufacturing technologies and the need for durable, long-lasting refractory linings to reduce maintenance downtime are key factors. The United States and Canada are leading in the adoption of innovative refractory solutions that offer improved thermal insulation and extended service life.

- Latin America: The refractory cement market in Latin America is poised for growth, fueled by increasing industrialization and investments in mining, metals, and energy sectors. Countries like Brazil, Mexico, and Argentina are witnessing expanding production capacities in steel, cement, and other energy-intensive industries, creating a steady demand for refractory materials. While growth may be influenced by economic stability, long-term infrastructure projects and regional industrial expansion contribute to market potential.

- Middle East and Africa (MEA): This region is emerging as a promising market for refractory cement, propelled by significant investments in oil and gas, petrochemicals, and basic metal industries. The construction of new industrial facilities and the expansion of existing ones, particularly in Gulf Cooperation Council (GCC) countries, drive demand. Diversification efforts away from oil economies, leading to the development of robust manufacturing sectors, are expected to further bolster the market for refractory cement in the coming years.

Top Key Players:

The market research report covers the analysis of key stakeholders of the Refractory Cement Market. Some of the leading players profiled in the report include -- Vesuvius plc

- RHI Magnesita

- Saint-Gobain S.A.

- Krosaki Harima Corporation

- Shinagawa Refractories Co., Ltd.

- Imerys S.A.

- Allied Mineral Products, Inc.

- Morgan Advanced Materials plc

- Refratechnik Group

- Calderys

- Resco Products, Inc.

- Puyang Refractories Group Co., Ltd.

- Beijing LIRR High Temperature Materials Co., Ltd.

- J.R. Refractory Materials Co., Ltd.

- Qingdao Refractory Co., Ltd.

- Kerui Refractories

- HarbisonWalker International (HWI)

- Minerals Technologies Inc. (MinTeC)

- Industrial Refractory Products (IRP)

- Shandong Luyang Refractories Co., Ltd.

Frequently Asked Questions:

What is refractory cement?

Refractory cement is a specialized binder used in the construction and repair of high-temperature industrial equipment such as furnaces, kilns, incinerators, and reactors. It is designed to withstand extreme heat, thermal shock, chemical attack, and mechanical abrasion, maintaining its structural integrity and performance in environments exceeding 1000°C (1832°F). Unlike conventional cements, refractory cement is formulated with specific aggregates and binders that provide superior thermal resistance and insulation properties, making it essential for various high-temperature industrial processes.

What are the primary applications of refractory cement?

Refractory cement finds extensive applications across a multitude of heavy industries where high-temperature processes are integral. Its primary uses include lining and repairing furnaces, kilns, and ladles in the iron and steel industry; constructing and maintaining rotary kilns in cement and lime production; building and relining glass melting furnaces; and providing durable linings for petrochemical reactors and power generation boilers. It is also increasingly utilized in emerging sectors such as waste-to-energy plants and specialized metallurgical processes that require materials capable of enduring severe thermal and chemical stresses.

What factors are driving the growth of the refractory cement market?

The growth of the refractory cement market is significantly driven by several key factors. Foremost among these is the expansion and modernization of core industrial sectors such as steel, cement, glass, and non-ferrous metals, particularly in rapidly industrializing economies. Additionally, increasing global focus on energy efficiency prompts industries to adopt advanced refractory materials that minimize heat loss and prolong equipment lifespan. Rapid urbanization and infrastructure development worldwide further fuel demand for basic materials like steel and cement, consequently boosting the need for refractory cement. Technological advancements in material science also contribute, leading to the development of higher-performance and more sustainable refractory solutions.

What challenges does the refractory cement market face?

The refractory cement market encounters several challenges that can influence its growth trajectory. One significant obstacle is the volatility in raw material prices, which can impact production costs and market stability. Environmental regulations regarding emissions and waste disposal pose a compliance burden, requiring significant investment in cleaner technologies. The market also faces the challenge of a shortage of skilled labor for precise installation and maintenance of refractory linings, which can affect performance and longevity. Intense competition among market players and potential disruptions in global supply chains further contribute to the complexities of operating within this industry.

What is the projected market size for refractory cement by 2033?

The global refractory cement market is projected to reach an estimated market size of USD 40.0 Billion by the end of 2033. This forecast indicates a substantial growth trajectory from its estimated value of USD 25.5 Billion in 2025. This expansion is attributed to a Compound Annual Growth Rate (CAGR) of 5.8% over the forecast period from 2025 to 2033, reflecting sustained demand from various end-use industries and ongoing advancements in material technology.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted