Recycled Packaging Material Market

Recycled Packaging Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709421 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

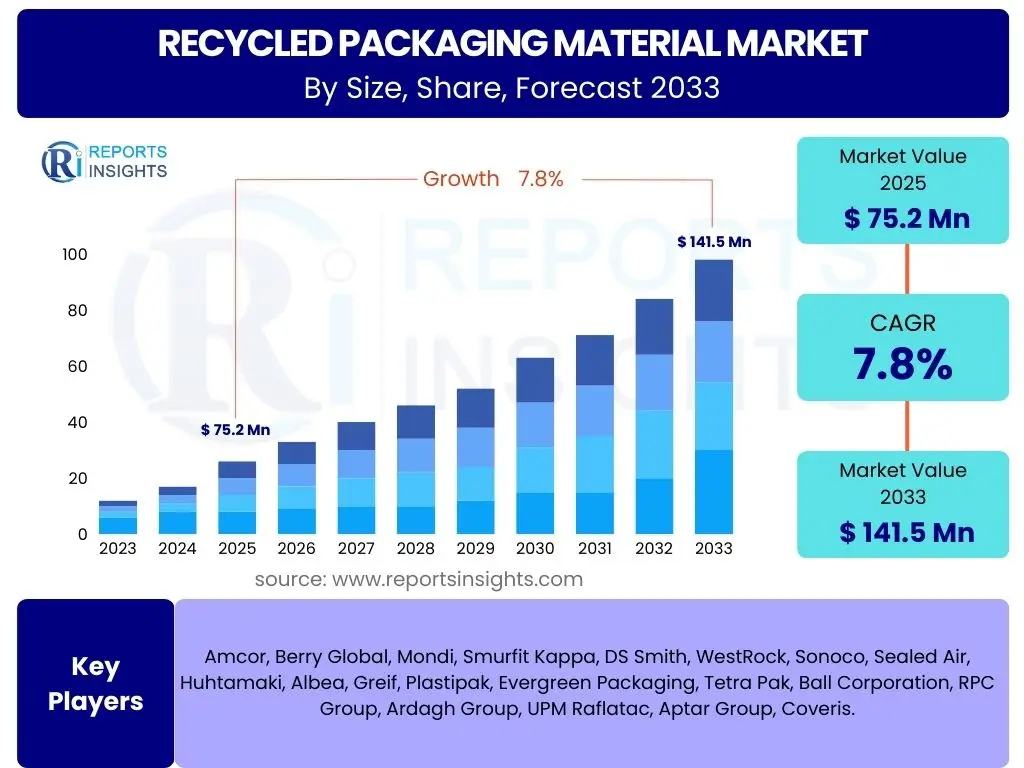

Recycled Packaging Material Market Size

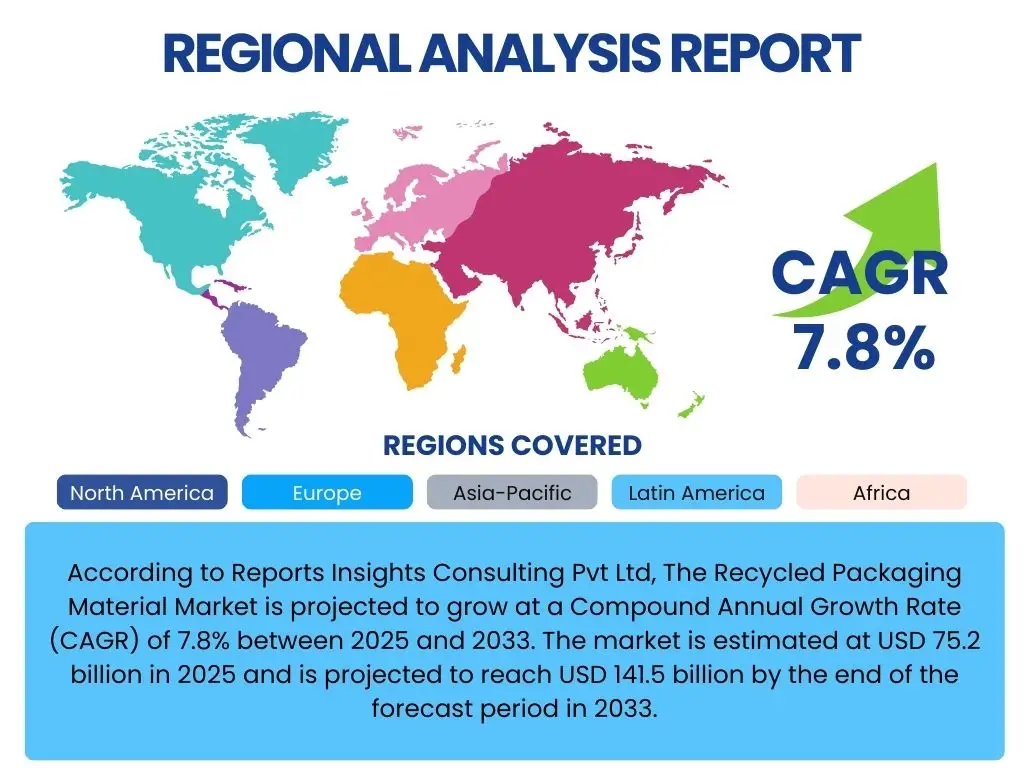

According to Reports Insights Consulting Pvt Ltd, The Recycled Packaging Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 75.2 billion in 2025 and is projected to reach USD 141.5 billion by the end of the forecast period in 2033.

Key Recycled Packaging Material Market Trends & Insights

The market for recycled packaging material is currently shaped by a confluence of environmental consciousness, regulatory pressures, and technological advancements. Consumers are increasingly prioritizing sustainable products, compelling brands to adopt eco-friendlier packaging solutions. This shift is driving innovation in material science and recycling processes, leading to higher quality recycled content and expanding its application across various industries. Furthermore, the global push towards a circular economy model is integrating recycling into the core design and lifecycle of packaging, moving beyond mere waste management to value creation.

A significant trend involves the enhancement of recycling infrastructure and the development of advanced recycling technologies, such as chemical recycling, which can process previously unrecyclable plastics into virgin-like raw materials. This technological leap addresses limitations of traditional mechanical recycling, offering solutions for complex plastic waste streams and potentially increasing the overall availability of high-quality recycled content. Additionally, collaborations across the value chain, from material producers to brand owners and waste management companies, are becoming more prevalent, aiming to create closed-loop systems and standardize recycling practices globally, further accelerating market growth and the adoption of recycled materials.

- Growing consumer demand for sustainable and eco-friendly packaging solutions.

- Increasing stringency of global environmental regulations and extended producer responsibility (EPR) schemes.

- Technological advancements in recycling processes, including chemical recycling and enhanced sorting.

- Shift towards a circular economy model emphasizing resource efficiency and waste reduction.

- Brand commitment and corporate sustainability initiatives driving adoption of recycled content.

- Innovation in packaging design for improved recyclability and increased recycled content incorporation.

AI Impact Analysis on Recycled Packaging Material

Artificial intelligence (AI) is poised to significantly transform the recycled packaging material landscape by enhancing efficiency, optimizing resource utilization, and fostering greater sustainability. User inquiries frequently center on AI's ability to streamline the sorting and identification of waste materials, a critical bottleneck in the recycling value chain. AI-powered optical sorting systems can accurately distinguish between different types of plastics, papers, and metals at high speeds, dramatically improving the purity and quality of recycled feedstock. This precision helps reduce contamination, a long-standing challenge that limits the usability of recycled materials and increases processing costs, thereby making the recycling process more economically viable and environmentally effective.

Beyond sorting, AI applications extend to predictive analytics for optimizing supply chains, forecasting demand for recycled materials, and even assisting in the design of packaging for optimal recyclability. By analyzing vast datasets related to waste streams, market prices, and consumer behavior, AI can provide insights that enable manufacturers to make more informed decisions regarding material sourcing and product development. Additionally, AI-driven quality control systems can monitor the integrity of recycled content throughout the manufacturing process, ensuring that the end products meet stringent performance standards. This comprehensive integration of AI across various stages is expected to reduce operational inefficiencies, minimize waste, and accelerate the transition towards a fully circular packaging economy, addressing key concerns about scalability and material quality.

- Enhanced waste sorting and identification through AI-powered optical systems, improving purity and efficiency.

- Optimization of recycling plant operations and resource allocation using AI-driven analytics.

- Predictive maintenance for recycling machinery, reducing downtime and operational costs.

- Improved quality control and material characterization of recycled feedstock.

- AI-assisted design for recyclability, guiding packaging engineers towards optimal material choices and structures.

- Supply chain optimization for recycled materials, balancing demand and supply more effectively.

Key Takeaways Recycled Packaging Material Market Size & Forecast

The Recycled Packaging Material Market is undergoing robust expansion, driven by an interplay of environmental imperatives, regulatory mandates, and evolving consumer preferences. Key takeaways emphasize a sustained upward trajectory in market valuation, signifying a fundamental shift in industry practices towards sustainability. The forecast projects substantial growth, reflecting increasing investments in recycling infrastructure and a wider adoption of circular economy principles across diverse sectors. This growth is not merely incremental but indicative of a transformative period where recycled content is becoming a standard rather than an alternative, fundamentally reshaping the packaging supply chain and offering significant long-term market opportunities.

A critical insight is the strengthening correlation between corporate sustainability goals and financial performance, compelling businesses to integrate recycled packaging as a core strategic objective. This commitment, coupled with technological advancements, is steadily overcoming traditional barriers such as quality concerns and cost parity. The market's resilience and projected expansion highlight a collective global effort to mitigate environmental impact, reduce reliance on virgin resources, and build a more resource-efficient economy. The increasing CAGR underscores the escalating importance of recycled materials in achieving these broader environmental and economic objectives, cementing their role as a crucial component of future packaging solutions.

- The Recycled Packaging Material Market is projected for substantial growth, indicating a strong industry shift towards sustainability.

- Significant market expansion is fueled by rising environmental awareness and stringent regulations globally.

- Technological advancements in recycling are enhancing material quality and expanding application possibilities.

- Corporate sustainability commitments and consumer demand are primary drivers of market adoption.

- The market's trajectory reflects a global transition towards a circular economy model for packaging.

Recycled Packaging Material Market Drivers Analysis

The growth of the recycled packaging material market is fundamentally propelled by a global paradigm shift towards environmental responsibility and resource efficiency. Consumers are increasingly vocal in their demand for sustainable products, exerting considerable pressure on brands to incorporate eco-friendly packaging solutions. This demand directly translates into a higher adoption rate for recycled materials. Concurrently, governments worldwide are implementing and tightening environmental regulations, including extended producer responsibility (EPR) schemes and single-use plastic bans, which mandate the use of recycled content and create a robust regulatory framework supportive of market expansion.

Furthermore, significant technological advancements in recycling processes are making it possible to produce higher quality recycled materials, addressing previous concerns about performance and aesthetics. Innovations in sorting, cleaning, and chemical recycling techniques enable a wider range of post-consumer waste to be reprocessed, reducing the dependency on virgin resources and lowering the carbon footprint associated with packaging production. The fluctuating prices of virgin raw materials also play a role, making recycled alternatives a more economically attractive option for manufacturers, especially when considering the long-term benefits of stable supply chains and enhanced brand reputation for sustainability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Consumer Demand for Sustainable Products | +2.5% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Stringent Environmental Regulations and EPR Schemes | +2.0% | Europe, North America, rapidly growing in Asia Pacific | Medium to Long-term (2025-2033) |

| Corporate Sustainability Goals and Brand Image | +1.8% | Global, concentrated in multinational corporations | Medium to Long-term (2025-2033) |

| Technological Advancements in Recycling Processes | +1.5% | Global, led by developed economies | Medium to Long-term (2025-2033) |

| Fluctuating Virgin Material Prices | +1.0% | Global, especially in regions with high import reliance | Short to Medium-term (2025-2029) |

Recycled Packaging Material Market Restraints Analysis

Despite significant growth drivers, the recycled packaging material market faces several formidable restraints that could impede its full potential. A primary challenge is the inconsistency and inefficiency of waste collection and sorting infrastructure across many regions. Inadequate collection systems lead to a substantial amount of recyclable material being sent to landfills or incinerators, limiting the available feedstock for recycling. Moreover, the lack of standardized collection methods and consumer confusion regarding recycling guidelines contribute to high contamination rates, which significantly increase processing costs and reduce the quality of recycled materials, making them less competitive with virgin alternatives.

Another critical restraint is the technical difficulty and cost associated with recycling certain complex packaging formats, such as multi-layer flexible packaging or items with mixed materials. These structures are often designed for performance rather than recyclability, making their separation and reprocessing economically unviable with current technologies. Furthermore, concerns regarding the aesthetic quality, mechanical properties, and food safety compliance of recycled content, particularly for direct food contact applications, can limit its adoption by brand owners. Overcoming these quality perception barriers and ensuring regulatory compliance requires substantial investment in advanced processing and certification, posing an ongoing challenge to market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Inconsistent Waste Collection and Sorting Infrastructure | -1.5% | Emerging economies, rural areas in developed nations | Long-term (2025-2033) |

| High Processing Costs and Economic Viability | -1.2% | Global, particularly competitive markets | Medium to Long-term (2025-2033) |

| Quality Concerns and Contamination of Recycled Material | -1.0% | Global, especially for high-grade applications | Medium to Long-term (2025-2033) |

| Limited Availability of High-Quality Recycled Feedstock | -0.8% | Global, depending on specific material types | Medium to Long-term (2025-2033) |

| Complexities of Recycling Multi-material Packaging | -0.7% | Global, impacting flexible packaging sector | Long-term (2025-2033) |

Recycled Packaging Material Market Opportunities Analysis

The Recycled Packaging Material Market is brimming with opportunities stemming from an accelerating global commitment to sustainability and the relentless pursuit of innovative solutions. One significant opportunity lies in the advancement and commercialization of chemical recycling technologies. These processes can break down plastic waste into its molecular components, yielding raw materials that are indistinguishable from virgin plastics, thus overcoming many limitations of traditional mechanical recycling regarding quality and type of plastic waste. This opens doors for recycling historically "hard-to-recycle" plastics, significantly expanding the available feedstock and enabling recycled content to meet stringent food-grade and medical-grade standards, which were previously difficult to achieve.

Another substantial opportunity resides in the expansion into emerging economies and the development of localized circular economy models. As industrialization and consumption rise in regions like Asia Pacific and Latin America, so does waste generation, creating a vast untapped resource for recycling. Investing in local collection, sorting, and processing infrastructure in these regions can not only address environmental concerns but also create new economic avenues, reduce reliance on imports, and foster sustainable industrial growth. Furthermore, the burgeoning e-commerce sector presents a unique opportunity for lightweight, durable, and easily recyclable packaging solutions, as online retailers face increasing pressure to demonstrate environmental responsibility throughout their supply chain, driving demand for innovative recycled packaging formats.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Advanced (Chemical) Recycling Technologies | +2.3% | Global, particularly in developed economies | Medium to Long-term (2025-2033) |

| Expansion into Emerging Economies with Growing Waste Streams | +1.9% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Increasing Demand from the E-commerce Sector | +1.7% | Global | Medium to Long-term (2025-2033) |

| Innovation in Bio-based and Blended Recycled Materials | +1.4% | Global, focused on R&D hubs | Long-term (2027-2033) |

| Strategic Partnerships and Investments Across the Value Chain | +1.1% | Global, cross-industry collaborations | Medium-term (2025-2030) |

Recycled Packaging Material Market Challenges Impact Analysis

The Recycled Packaging Material Market, while growing, confronts significant challenges that demand innovative and collaborative solutions. One major hurdle is the energy intensity and environmental footprint of certain recycling processes. While recycling generally offers environmental benefits over virgin material production, the energy consumption for collection, sorting, washing, and reprocessing, particularly for plastics and metals, can be substantial. This raises concerns about the overall sustainability of the recycling loop if not managed with renewable energy sources and optimized efficiencies. Moreover, the issue of microplastic generation during the recycling of plastics and the release of pollutants from certain reprocessing techniques are growing environmental concerns that need to be addressed through technological improvements and stricter operational controls.

Another persistent challenge is consumer skepticism and the need for greater education regarding recycling practices and the benefits of recycled content. Despite increasing awareness, inconsistencies in local recycling rules, confusion over what materials are actually recyclable, and a lack of trust in the recycling system can lead to lower participation rates and higher contamination in waste streams. Furthermore, the harmonization of regulatory standards and recycling infrastructure across different regions and countries remains a complex challenge. Disparate policies and collection systems create inefficiencies, hinder cross-border material flow, and complicate the development of global markets for recycled materials, preventing economies of scale and slowing market maturation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Energy Intensity and Environmental Footprint of Recycling Processes | -0.9% | Global, impacting operational costs and sustainability claims | Long-term (2025-2033) |

| Consumer Education and Engagement for Effective Recycling | -0.8% | Global, particularly in regions with nascent recycling cultures | Long-term (2025-2033) |

| Regulatory Harmonization and Policy Consistency Across Regions | -0.7% | Global, hindering international trade of recycled materials | Long-term (2025-2033) |

| Investment in New Infrastructure and Technology Upgrades | -0.6% | Global, requires significant capital expenditure | Medium to Long-term (2025-2033) |

| Maintaining Quality and Performance Parity with Virgin Materials | -0.5% | Global, especially for demanding applications | Medium to Long-term (2025-2033) |

Recycled Packaging Material Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Recycled Packaging Material Market, offering a detailed examination of market size, growth trends, drivers, restraints, opportunities, and challenges across various segments and regions. It encapsulates current market dynamics, assesses the competitive landscape, and projects future growth trajectories, delivering actionable insights for stakeholders seeking to navigate and capitalize on the evolving sustainable packaging sector. The report specifically addresses the impact of emerging technologies and evolving consumer and regulatory demands on market development.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 75.2 Billion |

| Market Forecast in 2033 | USD 141.5 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor, Berry Global, Mondi, Smurfit Kappa, DS Smith, WestRock, Sonoco, Sealed Air, Huhtamaki, Albea, Greif, Plastipak, Evergreen Packaging, Tetra Pak, Ball Corporation, RPC Group, Ardagh Group, UPM Raflatac, Aptar Group, Coveris. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Recycled Packaging Material Market is segmented to provide a granular view of its diverse components and understand the varied dynamics within each category. This segmentation allows for a detailed analysis of how different material types and end-use industries contribute to the overall market growth and where the most significant opportunities and challenges lie. Understanding these segments is crucial for stakeholders to tailor strategies, identify niche markets, and make informed investment decisions in an increasingly complex and evolving industry.

The segmentation highlights the dominance of certain materials like plastics and paper & cardboard due to their widespread use and established recycling infrastructures, while also shedding light on the expanding applications across critical industries such as food & beverages and e-commerce. This detailed breakdown ensures that market participants can pinpoint areas of high growth, assess competitive landscapes within specific categories, and adapt to emerging trends effectively, thereby optimizing their market positioning and capitalizing on the shift towards sustainable packaging solutions.

- By Material Type:

- Plastics: PET, HDPE, LDPE, PP, PS, PVC, Other Plastics

- Paper & Cardboard

- Glass

- Metals: Aluminum, Steel, Tin

- Others

- By End-Use Industry:

- Food & Beverages

- Healthcare

- Personal Care & Cosmetics

- Industrial

- Consumer Goods

- E-commerce

- Others

Regional Highlights

- North America: This region is a significant market for recycled packaging materials, driven by strong consumer awareness regarding environmental issues, robust corporate sustainability initiatives, and increasing regulatory pressure, particularly in the United States and Canada. Innovations in recycling technologies and a well-developed waste management infrastructure also contribute to its prominent market share.

- Europe: Europe stands as a leader in the adoption of recycled packaging, largely due to ambitious circular economy packages, stringent EU directives on plastics and packaging waste, and high recycling targets. Countries like Germany, France, and the UK are at the forefront, implementing advanced collection systems and fostering strong industry-wide collaborations to increase recycled content across various applications.

- Asia Pacific (APAC): The APAC region is projected to exhibit the fastest growth, propelled by rapid industrialization, burgeoning population, and a surging consumer market that is becoming increasingly conscious of environmental impacts. Governments in countries like China, India, and Japan are investing in upgrading recycling infrastructure and implementing policies to manage vast waste streams, creating immense opportunities for recycled packaging.

- Latin America: This region presents an emerging market with growing potential, characterized by increasing environmental awareness and developing regulatory frameworks aimed at improving waste management and recycling rates. Countries like Brazil and Mexico are seeing initial investments in recycling infrastructure and a rising demand for sustainable packaging from both local and international brands.

- Middle East and Africa (MEA): The MEA market for recycled packaging material is currently nascent but holds significant long-term growth prospects. Growing environmental concerns, coupled with economic diversification efforts away from fossil fuels, are prompting governments and industries to explore sustainable waste management and packaging solutions, fostering investment opportunities in recycling infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Recycled Packaging Material Market.- Amcor

- Berry Global

- Mondi

- Smurfit Kappa

- DS Smith

- WestRock

- Sonoco

- Sealed Air

- Huhtamaki

- Albea

- Greif

- Plastipak

- Evergreen Packaging

- Tetra Pak

- Ball Corporation

- RPC Group

- Ardagh Group

- UPM Raflatac

- Aptar Group

- Coveris

Frequently Asked Questions

What is recycled packaging material?

Recycled packaging material refers to any packaging product manufactured, in whole or in part, from post-consumer or post-industrial waste that has been reprocessed into new raw materials. This process reduces the need for virgin resources, minimizes landfill waste, and lowers the environmental impact of packaging production.

Why is recycled packaging important?

Recycled packaging is crucial for environmental sustainability as it conserves natural resources, reduces energy consumption during manufacturing, and significantly decreases greenhouse gas emissions compared to producing packaging from virgin materials. It also plays a vital role in mitigating plastic pollution and advancing the circular economy.

What types of materials are commonly recycled for packaging?

Common materials recycled for packaging include various plastics (such as PET, HDPE, LDPE, PP), paper and cardboard, glass, and metals (like aluminum and steel). The specific types and quality of materials can vary based on local recycling infrastructure and technological capabilities.

What are the main challenges in the recycled packaging market?

Key challenges include inconsistent waste collection and sorting infrastructure, high processing costs, contamination issues affecting material quality, limited availability of high-grade recycled feedstock, and the complexities of recycling multi-material packaging formats.

How does government regulation influence the recycled packaging market?

Government regulations, such as Extended Producer Responsibility (EPR) schemes, mandatory recycled content targets, and bans on single-use plastics, significantly drive the market by compelling manufacturers to adopt recycled materials and invest in sustainable packaging solutions, fostering market growth and innovation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted