Recuperator Market

Recuperator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708827 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

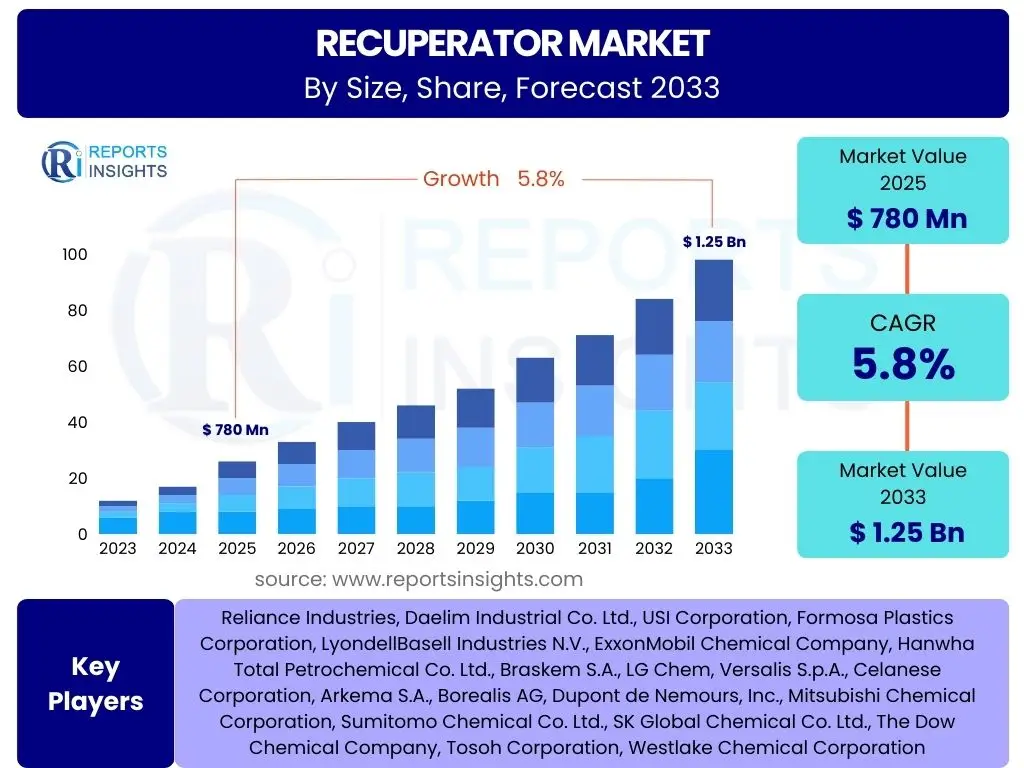

Recuperator Market Size

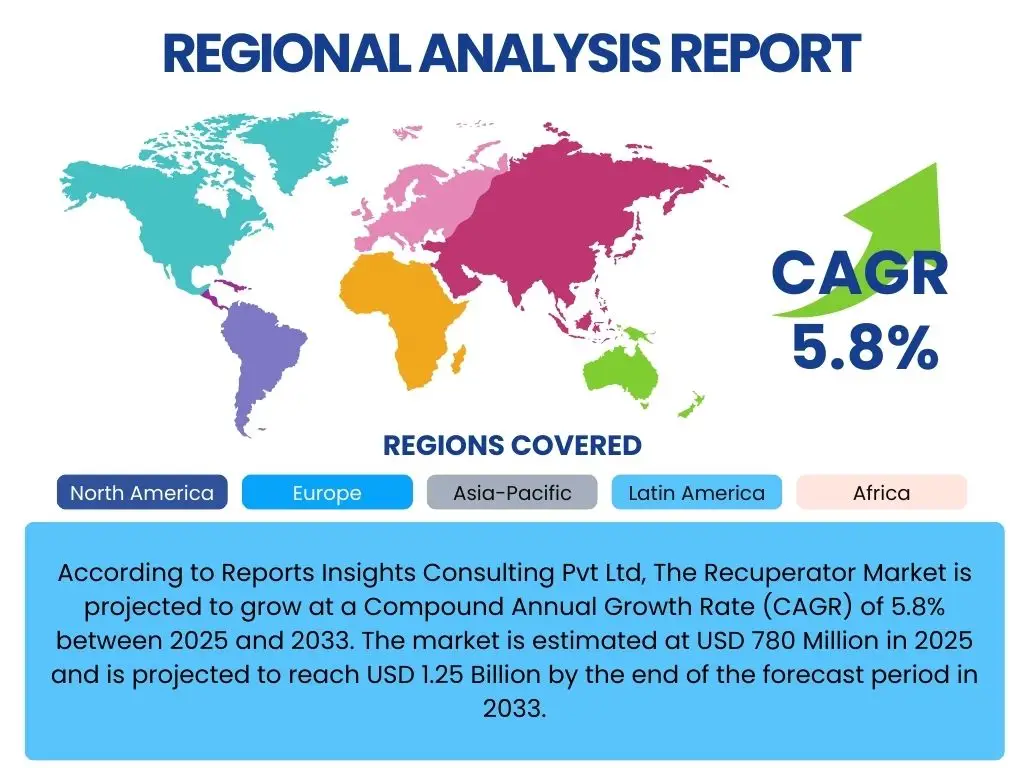

According to Reports Insights Consulting Pvt Ltd, The Recuperator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 780 Million in 2025 and is projected to reach USD 1.25 Billion by the end of the forecast period in 2033.

Key Recuperator Market Trends & Insights

User queries frequently focus on emerging technologies, sustainability drivers, and industrial application shifts within the recuperator market. A primary trend observed is the increasing adoption of advanced materials and designs aimed at enhancing thermal efficiency and durability. This is particularly critical in high-temperature industrial processes where energy recovery directly translates into significant operational cost savings and reduced environmental impact. Furthermore, there is a growing emphasis on smart recuperator systems integrated with IoT for real-time monitoring and predictive maintenance, allowing for optimized performance and prolonged operational lifespans.

Another significant insight revolves around the global push for decarbonization and energy conservation. Industries are under increasing pressure to comply with stringent environmental regulations and achieve net-zero targets, making recuperators an indispensable component in their energy management strategies. The demand is also being shaped by the expansion of key end-use industries, such as metals, glass, chemicals, and power generation, all seeking more efficient heat recovery solutions to improve their overall energy footprint. The customization of recuperator designs for specific industrial environments and process requirements is also gaining traction, moving away from one-size-fits-all solutions.

- Growing demand for energy-efficient industrial processes globally.

- Increasing adoption of advanced materials like ceramics and alloys for high-temperature applications.

- Integration of smart technologies, IoT, and AI for real-time monitoring and predictive maintenance.

- Stricter environmental regulations and carbon emission reduction targets driving adoption.

- Rise in demand from emerging economies undergoing rapid industrialization.

- Development of compact and modular recuperator designs for easier installation and maintenance.

- Shift towards customized recuperator solutions tailored for specific industrial needs.

AI Impact Analysis on Recuperator

Common user questions regarding AI's impact on recuperators center on how artificial intelligence can optimize performance, predict failures, and enhance design processes. AI is poised to revolutionize recuperator operations by enabling highly efficient predictive maintenance strategies. Instead of relying on fixed maintenance schedules or reacting to failures, AI algorithms can analyze vast datasets from sensors monitoring temperature, pressure, and flow rates to anticipate potential issues before they escalate. This proactive approach minimizes downtime, reduces maintenance costs, and extends the operational life of the equipment, directly contributing to higher efficiency and reliability in industrial settings.

Beyond maintenance, AI is also influencing recuperator design and optimization. Generative design principles, powered by AI, can explore a multitude of design iterations that would be impossible for human engineers to consider, identifying optimal geometries and material distributions for maximum heat transfer efficiency and minimal pressure drop. Furthermore, AI-driven control systems can dynamically adjust recuperator parameters in real-time based on fluctuating process conditions, ensuring the system operates at its peak performance under varying loads. This adaptability translates into consistent energy savings and improved overall process stability, making recuperators smarter and more responsive to industrial demands.

- Predictive maintenance through AI for reduced downtime and extended lifespan.

- Optimized operational control and energy management via real-time AI analytics.

- AI-driven generative design for enhanced thermal efficiency and compact structures.

- Improved fault detection and diagnostics using machine learning algorithms.

- Automated system calibration and performance tuning in dynamic industrial environments.

Key Takeaways Recuperator Market Size & Forecast

User inquiries frequently aim to understand the core implications of the recuperator market's growth trajectory and future outlook. A key takeaway is the sustained and robust growth anticipated, driven predominantly by the global imperative for energy efficiency across diverse industrial sectors. The market's expansion signifies a widespread recognition of recuperators as essential tools for cost reduction, compliance with environmental regulations, and enhancement of overall operational sustainability. This growth is not merely incremental but reflective of a fundamental shift towards more resource-efficient industrial practices worldwide.

Another crucial insight highlights the evolving technological landscape within the recuperator industry. Innovations in materials, smart sensing, and integration with advanced control systems are continuously enhancing the performance and applicability of recuperators. This technological progression is widening the scope of their use, enabling them to operate effectively in more demanding environments and delivering greater value to end-users. The projected market growth underscores an expanding opportunity for manufacturers and service providers who can offer cutting-edge, customized, and digitally integrated recuperator solutions that address the specific energy recovery challenges of modern industries.

- Significant market growth fueled by global energy efficiency demands and industrial expansion.

- Continuous technological advancements driving higher performance and wider application scope.

- Strategic importance of recuperators in achieving sustainability goals and reducing operational costs.

- Emerging opportunities for innovative solutions in high-temperature and harsh industrial environments.

- Increased investment potential in smart recuperator technologies and digital integration.

Recuperator Market Drivers Analysis

The recuperator market is significantly driven by the escalating global energy demand and the parallel need for energy conservation. Industries worldwide are facing increasing operational costs associated with energy consumption, making efficient heat recovery solutions a critical investment. Recuperators, by capturing and reusing waste heat, directly contribute to reducing fuel consumption and lowering energy bills, thereby providing a compelling economic incentive for their adoption across various manufacturing and processing sectors. This financial benefit is a primary catalyst for market growth, particularly in regions with high energy prices.

Furthermore, stringent environmental regulations aimed at reducing carbon emissions and air pollution are powerful drivers for the recuperator market. Governments and international bodies are imposing stricter limits on industrial emissions, compelling companies to adopt technologies that improve energy efficiency and minimize their environmental footprint. Recuperators play a vital role in achieving these objectives by optimizing fuel combustion and reducing the release of harmful pollutants. The move towards sustainable industrial practices and the increasing corporate emphasis on environmental, social, and governance (ESG) factors further bolster the demand for these systems, positioning them as essential components of modern, responsible industrial operations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Energy Efficiency Mandates | +0.9% | Europe, North America, China | Mid-to-Long Term |

| Rising Fuel Prices and Operational Cost Reduction Needs | +1.1% | Global | Short-to-Mid Term |

| Growing Industrialization and Infrastructure Development | +0.8% | Asia Pacific (China, India), Latin America | Mid-to-Long Term |

| Technological Advancements in Material Science | +0.7% | Global | Long Term |

| Supportive Government Policies and Incentives for Green Technologies | +0.6% | Germany, Japan, South Korea, USA | Short-to-Mid Term |

Recuperator Market Restraints Analysis

The recuperator market faces significant restraints, primarily stemming from the substantial initial capital investment required for these systems. For many businesses, especially small and medium-sized enterprises (SMEs), the upfront cost of purchasing and installing recuperators, particularly high-efficiency or specialized units, can be a major barrier. Despite the long-term operational savings and environmental benefits, the immediate financial outlay often deters potential adopters, especially in an economic climate where capital allocation is meticulously scrutinized. This high initial cost can slow down market penetration, particularly in cost-sensitive industrial sectors or developing regions.

Another prominent restraint involves the technical complexities associated with recuperator integration and maintenance. Designing and installing recuperators requires specialized engineering expertise to ensure optimal performance and compatibility with existing industrial processes. Furthermore, these systems operate in harsh environments, often involving high temperatures and corrosive gases, necessitating regular maintenance and potential component replacement. The availability of skilled personnel for installation, operation, and troubleshooting, coupled with the need for specialized spare parts, can increase the total cost of ownership and present operational challenges, thereby limiting their broader adoption in industries lacking such technical capabilities or resources.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.8% | Global, particularly SMEs | Short-to-Mid Term |

| Technical Complexities in Integration and Maintenance | -0.7% | Developing Regions, Industries with Limited Expertise | Mid-to-Long Term |

| Corrosion and Fouling Issues in Harsh Environments | -0.6% | Chemical, Metallurgy, Waste Incineration Industries | Ongoing |

| Lack of Awareness or Perceived Value in Certain Sectors | -0.5% | Specific Niche Industries, Smaller Markets | Long Term |

| Space Constraints for Installation in Existing Facilities | -0.4% | Brownfield Industrial Sites, Urban Manufacturing | Short-to-Mid Term |

Recuperator Market Opportunities Analysis

Significant opportunities in the recuperator market arise from the expanding applications in diverse industrial sectors, particularly those undergoing modernization and efficiency upgrades. Industries such as glass, steel, chemicals, and cement are continually seeking ways to reduce energy consumption and improve their environmental performance. The development of specialized recuperator designs tailored for the unique process conditions and waste heat streams of these sectors opens new avenues for market penetration. Furthermore, the global trend towards circular economy principles and industrial symbiosis creates demand for integrated heat recovery solutions that can capture and utilize waste energy across multiple facilities or processes, driving innovation in system design and deployment.

Another major opportunity lies in the development and commercialization of smart and modular recuperator systems. As industries move towards Industry 4.0, there is a growing demand for equipment that offers connectivity, real-time monitoring, and remote diagnostics. Recuperators integrated with IoT sensors and AI-driven analytics can provide predictive maintenance, optimized performance, and greater operational flexibility. Moreover, modular designs facilitate easier installation, scalability, and maintenance, reducing downtime and making these systems more attractive to a wider range of industrial clients. These technological advancements not only enhance the value proposition of recuperators but also align with the broader digital transformation strategies of manufacturing enterprises.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Industry 4.0 and Smart Manufacturing | +1.0% | Developed Economies (Europe, North America, Japan) | Mid-to-Long Term |

| Expansion into New End-use Applications (e.g., Waste-to-Energy) | +0.9% | Asia Pacific, Europe | Long Term |

| Demand for Advanced Material-Based Recuperators | +0.8% | Global, High-Temperature Industries | Mid-to-Long Term |

| Retrofitting Opportunities in Aging Industrial Infrastructure | +0.7% | Europe, North America, Older Industrial Belts | Short-to-Mid Term |

| Development of Modular and Compact Recuperator Designs | +0.6% | Global | Mid-to-Long Term |

Recuperator Market Challenges Impact Analysis

The recuperator market faces significant challenges, particularly related to the harsh operating conditions encountered in many industrial applications. High temperatures, corrosive gases, and abrasive particles are common in environments such as metal processing, glass manufacturing, and chemical production. These conditions can lead to rapid material degradation, fouling, and stress on recuperator components, diminishing their efficiency and lifespan. Addressing these issues requires the use of specialized, often expensive, materials and complex design considerations, which can increase the overall cost and complexity of the recuperator systems, making them less attractive to some potential buyers. Overcoming these material science and engineering challenges remains a critical hurdle for widespread adoption and long-term reliability.

Another substantial challenge is the fluctuating regulatory landscape and the variability in incentive programs across different regions and countries. While environmental regulations generally drive demand, inconsistencies in their enforcement or the periodic changes in government subsidies and tax incentives for energy-efficient technologies can create market uncertainty. Businesses require clear, consistent policy signals to justify significant capital investments in recuperators. When policies are unpredictable or insufficient, it can hinder investment decisions, delay project implementations, and create an uneven playing field for manufacturers and end-users alike. Navigating this complex and dynamic regulatory environment poses a continuous challenge for market players seeking to expand their footprint globally.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Temperature and Corrosive Operating Environments | -0.7% | Global, Specific Heavy Industries | Ongoing |

| Lack of Standardization and Customization Requirements | -0.6% | Global | Mid-to-Long Term |

| Competition from Alternative Heat Recovery Technologies | -0.5% | Global | Short-to-Mid Term |

| Fluctuating Raw Material Prices and Supply Chain Disruptions | -0.4% | Global | Short-term |

| Limited Skilled Workforce for Design, Installation, and Maintenance | -0.3% | Developing Regions | Long Term |

Recuperator Market - Updated Report Scope

This report provides a comprehensive analysis of the global Recuperator Market, encompassing detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It offers an updated assessment of market size and growth projections from 2025 to 2033, building upon historical data from 2019 to 2023. The scope includes an in-depth examination of key drivers, restraints, opportunities, and challenges shaping the industry, alongside an analysis of technological advancements and their impact on market evolution. The objective is to equip stakeholders with actionable intelligence for strategic decision-making in this vital energy recovery sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 780 Million |

| Market Forecast in 2033 | USD 1.25 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | S&P Global, Kanthal, Fives, Schack Engineering, Exchanger Industries Limited, IHI Corporation, Nippon Steel Engineering, Thermax, Koch Industries (John Zink Hamworthy Combustion), Airex Corporation, Recupair Inc., Vairex Air Systems, Goessling, Zander & Ingestrom, GEA Group, Kelvion, Alfa Laval, Danfoss, Atlas Copco (LEYBOLD), Universal Recuperator Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The recuperator market is analyzed across several key dimensions, including type, flow type, application, and end-use industry, providing a granular view of market dynamics. This comprehensive segmentation allows for a deeper understanding of specific product preferences, technological adoption patterns, and demand drivers within various industrial contexts. Each segment represents distinct market characteristics and growth opportunities, shaped by operational requirements, material science advancements, and regional industrial development.

Understanding these segments is crucial for stakeholders to identify lucrative niches and tailor their product offerings and market strategies effectively. For instance, the demand for ceramic recuperators is often concentrated in high-temperature applications where metallic options may fail, while counter-flow designs are preferred for maximum thermal efficiency. Similarly, the specific needs of industries such as steel and glass dictate the type and configuration of recuperators most suited for their unique waste heat recovery challenges, underscoring the importance of specialized solutions within a diverse market landscape.

- By Type

- Ceramic Recuperators

- Metallic Recuperators

- Hybrid Recuperators

- By Flow Type

- Cross-Flow Recuperators

- Counter-Flow Recuperators

- Parallel-Flow Recuperators

- By Application

- Industrial Furnaces & Ovens

- Steel & Metals Industry

- Glass Industry

- Chemical Processing

- Power Generation

- Waste Incineration

- Other Industrial Applications

- By End-Use Industry

- Manufacturing

- Power & Energy

- Chemicals

- Mining & Metallurgy

- Food & Beverages

- Others

Regional Highlights

- North America: A mature market driven by strict environmental regulations, high energy costs, and the presence of established heavy industries. Significant investments in retrofitting existing facilities with energy-efficient technologies.

- Europe: Leading the charge in decarbonization and energy efficiency initiatives. Strong governmental support, R&D investments in advanced materials, and a robust manufacturing base contribute to market growth, particularly in Germany and the UK.

- Asia Pacific (APAC): The fastest-growing market, propelled by rapid industrialization, increasing energy demand, and government policies promoting sustainable manufacturing in China, India, and Southeast Asian countries.

- Latin America: Emerging market with increasing industrial investments in mining, metallurgy, and food processing, driving demand for cost-effective energy recovery solutions.

- Middle East and Africa (MEA): Growing market with significant potential, especially in the oil and gas, petrochemical, and manufacturing sectors, as the region diversifies its industrial base and focuses on energy optimization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Recuperator Market.- S&P Global

- Kanthal

- Fives

- Schack Engineering

- Exchanger Industries Limited

- IHI Corporation

- Nippon Steel Engineering

- Thermax

- Koch Industries (John Zink Hamworthy Combustion)

- Airex Corporation

- Recupair Inc.

- Vairex Air Systems

- Goessling

- Zander & Ingestrom

- GEA Group

- Kelvion

- Alfa Laval

- Danfoss

- Atlas Copco (LEYBOLD)

- Universal Recuperator Inc.

Frequently Asked Questions

What is a recuperator and how does it work?

A recuperator is a type of heat exchanger that recovers waste heat from exhaust gases and uses it to preheat incoming combustion air or process fluids, thereby improving energy efficiency and reducing fuel consumption in industrial processes.

Which industries primarily utilize recuperators?

Recuperators are widely used in energy-intensive industries such as steel and metals, glass manufacturing, chemical processing, power generation, and industrial furnaces and ovens, where high temperatures and significant waste heat are prevalent.

What are the main benefits of installing a recuperator?

The primary benefits include substantial fuel savings, reduced operational costs, lower carbon emissions, improved process efficiency, and enhanced compliance with environmental regulations by effectively recovering and reusing waste heat.

What are the differences between metallic and ceramic recuperators?

Metallic recuperators are generally more compact and cost-effective for lower temperature applications, while ceramic recuperators are preferred for extremely high-temperature (above 1000°C) and corrosive environments due to their superior thermal stability and chemical resistance.

How does technological innovation impact the recuperator market?

Technological innovation, including advanced materials, smart sensors, and AI integration, is leading to more efficient, durable, and intelligent recuperator systems that offer predictive maintenance, real-time optimization, and wider application across diverse industrial challenges.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted