Radiopharmaceutical in Nuclear Medical Market

Radiopharmaceutical in Nuclear Medical Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704463 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

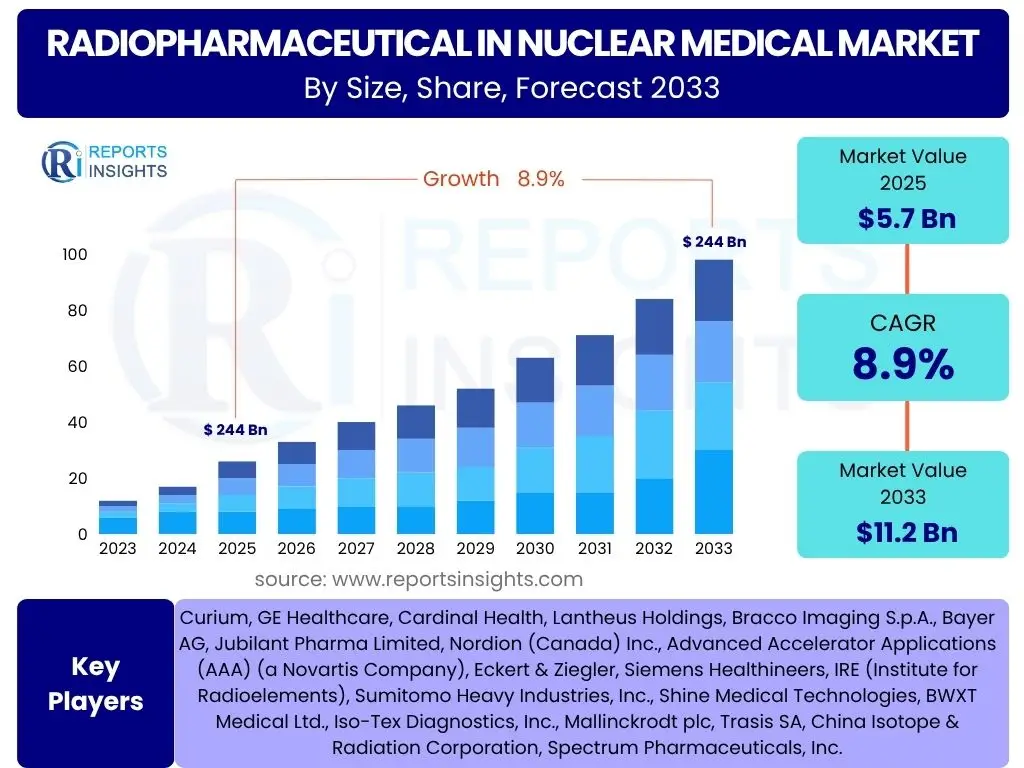

Radiopharmaceutical in Nuclear Medical Market Size

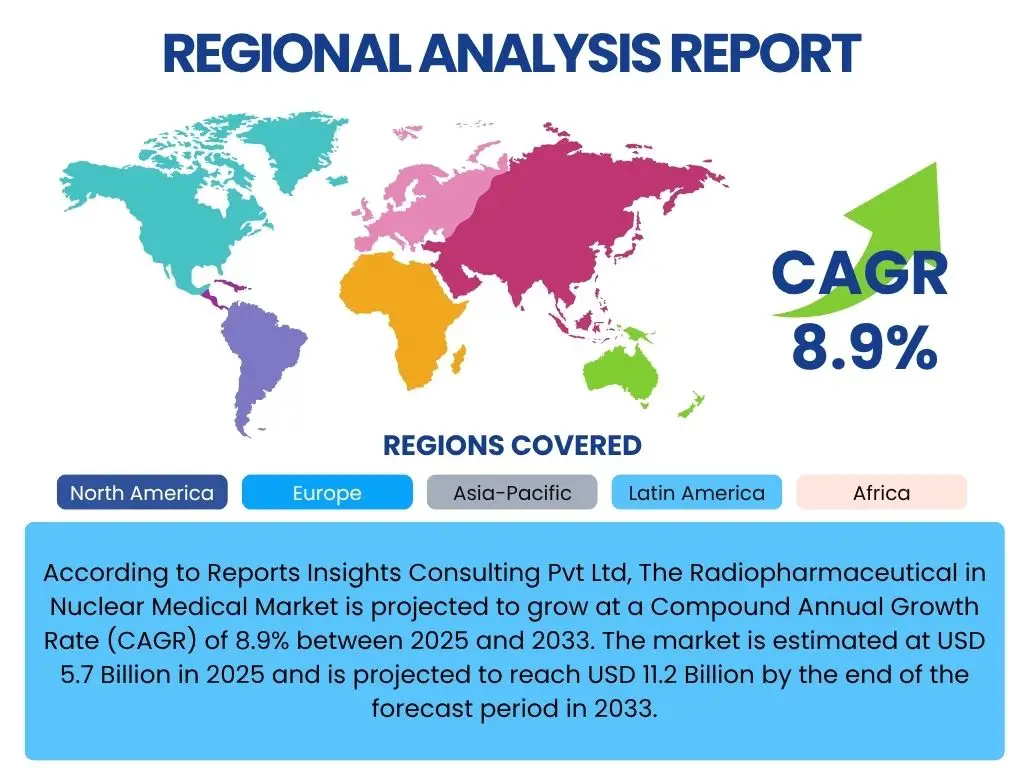

According to Reports Insights Consulting Pvt Ltd, The Radiopharmaceutical in Nuclear Medical Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 5.7 Billion in 2025 and is projected to reach USD 11.2 Billion by the end of the forecast period in 2033.

Key Radiopharmaceutical in Nuclear Medical Market Trends & Insights

The Radiopharmaceutical in Nuclear Medical Market is currently experiencing transformative trends driven by advancements in precision medicine and diagnostic imaging. A significant shift towards theranostics, combining diagnostic imaging with targeted radionuclide therapy, is redefining treatment paradigms for various diseases, particularly oncology. This approach offers a more personalized and effective treatment pathway, moving beyond traditional broad-spectrum therapies. Additionally, the increasing incidence of chronic diseases globally, such as cancer, cardiovascular disorders, and neurological conditions, is fueling demand for advanced diagnostic and therapeutic tools that radiopharmaceuticals provide.

Innovation in isotope production and delivery methods is another pivotal trend, addressing long-standing challenges related to supply chain stability and the short half-life of certain radioisotopes. Research into novel production techniques, including cyclotron-based and generator technologies, is expanding the availability of a wider range of diagnostic and therapeutic agents. Concurrently, the integration of advanced imaging modalities like PET/CT and SPECT/CT continues to enhance diagnostic accuracy and treatment planning, reinforcing the utility of radiopharmaceuticals in clinical practice. These developments collectively underscore a dynamic market characterized by technological progression and a growing emphasis on patient-centric care.

- Growing adoption of theranostics for personalized medicine in oncology.

- Advancements in cyclotron and generator technologies for enhanced isotope production.

- Increasing prevalence of chronic diseases driving demand for advanced diagnostics.

- Integration of artificial intelligence and machine learning in image analysis and drug discovery.

- Development of novel radiopharmaceuticals for neurology and cardiology applications.

AI Impact Analysis on Radiopharmaceutical in Nuclear Medical

Artificial intelligence is profoundly transforming the Radiopharmaceutical in Nuclear Medical Market by optimizing various stages from research and development to patient management. Users are particularly interested in how AI can enhance the diagnostic accuracy of nuclear imaging, reduce interpretation errors, and accelerate the drug discovery process for new radiopharmaceuticals. AI algorithms are proving invaluable in analyzing complex imaging data from PET and SPECT scans, enabling earlier and more precise disease detection. This capability allows for more effective treatment planning and monitoring, leading to improved patient outcomes and more efficient resource utilization within healthcare systems.

Furthermore, AI's role extends to automating and streamlining the synthesis and quality control of radiopharmaceuticals, addressing the challenges associated with their short half-lives and complex production. Predictive analytics powered by AI can optimize isotope production schedules and supply chain logistics, ensuring timely delivery to clinical sites. There is also significant interest in AI's potential to identify novel molecular targets for radiopharmaceutical development and to predict patient responses to radionuclide therapies, thereby fostering the growth of precision medicine. These applications collectively highlight AI as a critical enabler for innovation and efficiency within the nuclear medical domain, promising to unlock new possibilities for diagnostics and therapeutics.

- Enhanced diagnostic accuracy through AI-powered image analysis (e.g., PET/CT, SPECT/CT).

- Acceleration of radiopharmaceutical drug discovery and development by identifying novel targets.

- Optimization of radiopharmaceutical production and supply chain logistics.

- Personalized treatment planning and prediction of patient response to radionuclide therapies.

- Automation of quality control processes, reducing human error and improving efficiency.

Key Takeaways Radiopharmaceutical in Nuclear Medical Market Size & Forecast

The Radiopharmaceutical in Nuclear Medical Market is poised for substantial expansion over the forecast period, driven by persistent innovation and a broadening scope of clinical applications. A primary takeaway is the strong growth trajectory, indicating increasing global reliance on nuclear medicine for advanced diagnostics and therapeutic interventions. This growth is underpinned by rising investments in healthcare infrastructure and research, particularly in emerging economies. The market's resilience is further supported by the continuous development of novel radiopharmaceuticals designed to target specific pathologies with greater precision, reducing side effects and enhancing therapeutic efficacy.

Another crucial insight is the strategic importance of collaborations between pharmaceutical companies, research institutions, and technology providers. These partnerships are instrumental in overcoming the technical and regulatory hurdles associated with radiopharmaceutical development and commercialization. The emphasis on theranostics represents a paradigm shift, signaling a future where diagnostics and therapy are seamlessly integrated, offering more effective and personalized patient care. The market's forecast reflects a positive outlook, where ongoing research, favorable regulatory environments, and the increasing global burden of chronic diseases will continue to spur demand and innovation in the nuclear medical sector.

- Market demonstrates robust growth with an 8.9% CAGR from 2025 to 2033, reaching USD 11.2 Billion.

- Significant growth attributed to the increasing adoption of theranostic approaches and precision medicine.

- Innovation in isotope production and delivery methods is crucial for market expansion.

- Rising prevalence of chronic diseases like cancer, cardiovascular, and neurological disorders drives demand.

- Strategic partnerships and R&D investments are key to overcoming market challenges and fostering innovation.

Radiopharmaceutical in Nuclear Medical Market Drivers Analysis

The Radiopharmaceutical in Nuclear Medical Market is significantly propelled by several key drivers that reflect evolving healthcare needs and technological advancements. A primary driver is the escalating global prevalence of chronic diseases, particularly cancer, cardiovascular diseases, and neurological disorders. These conditions require highly precise diagnostic tools for early detection and targeted therapies for effective management, areas where radiopharmaceuticals excel. The aging global population further contributes to this demand, as geriatric individuals are more susceptible to these diseases, increasing the need for sophisticated medical imaging and treatment options.

Technological innovations in imaging modalities, such as hybrid imaging systems (e.g., PET/CT, SPECT/CT), enhance the diagnostic capabilities of radiopharmaceuticals, providing clearer and more comprehensive anatomical and functional information. This improved diagnostic accuracy leads to better patient outcomes and more informed treatment decisions. Additionally, the growing focus on personalized medicine and theranostics, which integrates diagnostics with therapy, is a substantial growth catalyst. This approach allows for tailored treatments based on individual patient characteristics, making therapies more effective and reducing adverse effects, thereby increasing the clinical utility and adoption of radiopharmaceuticals.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Chronic Diseases | +2.1% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 |

| Technological Advancements in Imaging Modalities | +1.8% | Developed Economies (e.g., US, Germany, Japan) | 2025-2033 |

| Growing Adoption of Personalized Medicine and Theranostics | +1.5% | Global, increasing in emerging markets | 2025-2033 |

| Expanding Geriatric Population | +1.2% | Europe, Japan, North America, China | 2025-2033 |

Radiopharmaceutical in Nuclear Medical Market Restraints Analysis

Despite significant growth prospects, the Radiopharmaceutical in Nuclear Medical Market faces notable restraints that could temper its expansion. One of the primary challenges is the high cost associated with the production, development, and clinical application of radiopharmaceuticals. The specialized infrastructure required for isotope production, synthesis, and safe handling, coupled with stringent regulatory approval processes, contributes to elevated manufacturing expenses. These high costs can lead to higher treatment prices, potentially limiting patient access, especially in price-sensitive markets or regions with less robust healthcare reimbursement systems.

Another significant restraint is the extremely short half-life of many critical radioisotopes, such as Technetium-99m (Tc-99m) and Fluorine-18 (F-18). This characteristic necessitates immediate use after production and rapid, complex logistical chains for transportation and distribution. Supply chain vulnerabilities, often dependent on a limited number of aging nuclear reactors for isotope production, pose a continuous risk of shortages, impacting market stability and clinical operations. Furthermore, the stringent regulatory landscape governing the manufacturing, handling, and disposal of radioactive materials creates significant barriers to market entry and introduces complexities for existing players, requiring substantial investments in compliance and safety protocols.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Radiopharmaceutical Production and Treatment | -1.5% | Global, more pronounced in developing regions | 2025-2033 |

| Short Half-Life of Key Radioisotopes and Supply Chain Vulnerabilities | -1.2% | Global, impacting regions far from production sites | 2025-2033 |

| Stringent Regulatory Landscape and Approval Processes | -0.9% | North America, Europe, Japan | 2025-2033 |

| Lack of Skilled Professionals in Nuclear Medicine | -0.7% | Global, particularly in emerging economies | 2025-2033 |

Radiopharmaceutical in Nuclear Medical Market Opportunities Analysis

The Radiopharmaceutical in Nuclear Medical Market is rich with opportunities stemming from ongoing research, unmet medical needs, and expanding geographical reach. A significant opportunity lies in the continued development and commercialization of novel theranostic agents. As the concept of personalized medicine gains traction, combining diagnostic and therapeutic functions in a single radiopharmaceutical offers unparalleled potential for precise disease management, particularly in oncology and other chronic conditions where targeted approaches are highly beneficial. This focus on theranostics is driving research into new ligand-receptor binding mechanisms and more potent radionuclides.

Furthermore, the exploration of new indications and applications for existing and novel radiopharmaceuticals presents a substantial growth avenue. Beyond traditional oncology applications, there is increasing interest and investment in developing radiopharmaceuticals for neurological disorders (e.g., Alzheimer's, Parkinson's), cardiovascular diseases, and inflammatory conditions. This diversification of applications broadens the market's reach and addresses critical unmet medical needs. Additionally, the rapid growth of healthcare infrastructure and rising awareness of nuclear medicine in emerging economies, particularly in Asia Pacific and Latin America, offer significant market penetration opportunities. These regions represent untapped patient populations and growing investments in advanced medical technologies, presenting fertile ground for market expansion and increased adoption of radiopharmaceutical services.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Theranostic Radiopharmaceuticals | +2.0% | Global, strong R&D in developed nations | 2025-2033 |

| Expansion of Radiopharmaceutical Applications to New Disease Areas | +1.7% | Global, driven by unmet needs | 2025-2033 |

| Growth in Emerging Markets and Improving Healthcare Infrastructure | +1.4% | Asia Pacific, Latin America, Middle East | 2025-2033 |

| Advancements in Cyclotron Technology for Local Isotope Production | +1.0% | Global, reducing reliance on central reactors | 2025-2033 |

Radiopharmaceutical in Nuclear Medical Market Challenges Impact Analysis

The Radiopharmaceutical in Nuclear Medical Market grapples with several formidable challenges that can impede its growth and operational efficiency. One of the most critical challenges is the inherent complexity and vulnerability of the global isotope supply chain. Many key medical isotopes are produced in a limited number of aging nuclear reactors worldwide, making the supply chain susceptible to disruptions due to maintenance shutdowns, technical failures, or geopolitical issues. This dependency often leads to price volatility and potential shortages, directly impacting patient care and research efforts globally. Ensuring a stable and reliable supply of radioisotopes remains a persistent hurdle for the industry.

Another significant challenge revolves around the intricate and often lengthy regulatory approval processes for new radiopharmaceuticals. Due to the radioactive nature of these agents and their direct impact on patient health, regulatory bodies enforce rigorous safety and efficacy standards. This necessitates extensive clinical trials and exhaustive documentation, which can prolong time-to-market and significantly increase development costs, thereby discouraging smaller entities from entering the market. Furthermore, the specialized infrastructure and highly trained personnel required for the safe handling, administration, and disposal of radiopharmaceuticals present ongoing operational challenges. Establishing and maintaining such facilities requires substantial investment, and the scarcity of adequately trained nuclear medicine professionals can limit the widespread adoption of these therapies, particularly in regions with less developed healthcare systems.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Vulnerable Isotope Supply Chain | -1.8% | Global | Ongoing |

| Lengthy and Stringent Regulatory Approval Processes | -1.4% | North America, Europe | Ongoing |

| Need for Specialized Infrastructure and Trained Personnel | -1.0% | Global, particularly in developing regions | 2025-2033 |

| Public Perception and Radiation Safety Concerns | -0.8% | Global | 2025-2033 |

Radiopharmaceutical in Nuclear Medical Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Radiopharmaceutical in Nuclear Medical Market, offering a detailed analysis of its size, growth trajectory, key trends, and competitive landscape. It provides an in-depth examination of market drivers, restraints, opportunities, and challenges, shedding light on factors that will shape the industry from 2025 to 2033. The report segments the market by isotope type, application, and end-user, providing granular insights into each category's performance and future potential across various geographical regions. It also includes an extensive impact analysis of artificial intelligence, highlighting its transformative influence on diagnostics, drug discovery, and operational efficiencies within nuclear medicine.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.7 Billion |

| Market Forecast in 2033 | USD 11.2 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Curium, GE Healthcare, Cardinal Health, Lantheus Holdings, Bracco Imaging S.p.A., Bayer AG, Jubilant Pharma Limited, Nordion (Canada) Inc., Advanced Accelerator Applications (AAA) (a Novartis Company), Eckert & Ziegler, Siemens Healthineers, IRE (Institute for Radioelements), Sumitomo Heavy Industries, Inc., Shine Medical Technologies, BWXT Medical Ltd., Iso-Tex Diagnostics, Inc., Mallinckrodt plc, Trasis SA, China Isotope & Radiation Corporation, Spectrum Pharmaceuticals, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Radiopharmaceutical in Nuclear Medical Market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates targeted analysis of various product types, therapeutic and diagnostic applications, and end-user environments, allowing stakeholders to identify niche opportunities and tailor strategies effectively. Each segment reflects distinct market drivers, challenges, and growth trajectories, influenced by specific technological advancements, regulatory frameworks, and patient demographics.

- By Isotope Type: This segment categorizes radiopharmaceuticals based on the specific radioisotope used, which dictates their half-life, energy, and suitability for different imaging or therapeutic purposes. Key isotopes include Technetium-99m (Tc-99m), Fluorine-18 (F-18), Iodine-131 (I-131), Gallium-68 (Ga-68), Thallium-201 (Tl-201), Lutetium-177 (Lu-177), Yttrium-90 (Y-90), and other emerging isotopes.

- By Application: This segment analyzes the market based on the medical conditions or areas where radiopharmaceuticals are primarily used. It includes Oncology (further segmented by imaging modalities like PET, SPECT, and theranostics), Cardiology (e.g., stress tests, perfusion imaging), Neurology (e.g., Alzheimer's, Parkinson's, epilepsy), Thyroid disorders, Bone Metastasis, and other miscellaneous applications.

- By End-user: This segment delineates the primary facilities or institutions where radiopharmaceuticals are administered and utilized. Key end-users include Hospitals, Diagnostic Centers (including standalone imaging centers), Research Institutions (for clinical trials and drug development), and Ambulatory Surgical Centers.

Regional Highlights

- North America: This region holds a significant market share due to its advanced healthcare infrastructure, high adoption rate of nuclear medicine procedures, strong research and development activities, and presence of key market players. The increasing prevalence of chronic diseases and favorable reimbursement policies further contribute to its dominance. The United States specifically leads in technological adoption and R&D investment.

- Europe: Europe represents a substantial market, driven by a growing elderly population, rising awareness about early disease diagnosis, and increasing investment in healthcare. Countries like Germany, France, and the UK are at the forefront of adopting novel radiopharmaceuticals and advanced imaging technologies. However, variations in regulatory frameworks and reimbursement policies across member states present some regional challenges.

- Asia Pacific (APAC): The Asia Pacific region is projected to exhibit the highest growth rate during the forecast period, attributed to improving healthcare infrastructure, rising disposable incomes, increasing healthcare expenditure, and a large patient pool. Countries like China, India, and Japan are investing heavily in nuclear medicine facilities and research, fostering rapid market expansion and adoption of advanced diagnostic and therapeutic radiopharmaceuticals.

- Latin America: This region is experiencing steady growth in the radiopharmaceutical market, fueled by increasing awareness of nuclear medicine benefits, improving economic conditions, and expanding access to healthcare services. Brazil and Mexico are leading markets, with a growing number of diagnostic centers and hospitals incorporating nuclear imaging into their clinical practices.

- Middle East and Africa (MEA): The MEA region is characterized by nascent but growing demand for radiopharmaceuticals, driven by rising chronic disease prevalence, particularly in oncology, and increasing government investments in healthcare infrastructure. Gulf Cooperation Council (GCC) countries are at the forefront of adopting advanced medical technologies, while challenges remain in broader African nations due to limited access and infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Radiopharmaceutical in Nuclear Medical Market.- Curium

- GE Healthcare

- Cardinal Health

- Lantheus Holdings

- Bracco Imaging S.p.A.

- Bayer AG

- Jubilant Pharma Limited

- Nordion (Canada) Inc.

- Advanced Accelerator Applications (AAA) (a Novartis Company)

- Eckert & Ziegler

- Siemens Healthineers

- IRE (Institute for Radioelements)

- Sumitomo Heavy Industries, Inc.

- Shine Medical Technologies

- BWXT Medical Ltd.

- Iso-Tex Diagnostics, Inc.

- Mallinckrodt plc

- Trasis SA

- China Isotope & Radiation Corporation

- Spectrum Pharmaceuticals, Inc.

Frequently Asked Questions

What are radiopharmaceuticals used for?

Radiopharmaceuticals are primarily used for diagnostic imaging (e.g., PET, SPECT scans) to detect diseases early, monitor disease progression, and assess treatment effectiveness. They are also increasingly used for targeted radionuclide therapies, particularly in oncology, where they deliver radiation directly to cancerous cells while minimizing damage to healthy tissues.

How is artificial intelligence impacting nuclear medicine?

Artificial intelligence is transforming nuclear medicine by enhancing diagnostic accuracy through advanced image analysis, accelerating the discovery and development of new radiopharmaceuticals, optimizing production and supply chain logistics, and enabling more personalized treatment planning based on predictive analytics of patient responses.

What are the primary drivers of growth in the radiopharmaceutical market?

Key growth drivers include the rising global prevalence of chronic diseases (especially cancer), continuous technological advancements in imaging modalities and isotope production, the growing adoption of personalized medicine and theranostics approaches, and an expanding geriatric population requiring advanced diagnostic and therapeutic solutions.

What challenges does the radiopharmaceutical market face?

Major challenges include the complex and often vulnerable supply chain for medical isotopes, the short half-life of many key radioisotopes, stringent and lengthy regulatory approval processes for new products, high production and treatment costs, and the ongoing need for specialized infrastructure and highly trained personnel.

What is theranostics in the context of radiopharmaceuticals?

Theranostics is an innovative approach in nuclear medicine that combines diagnostic imaging with targeted radionuclide therapy using a single molecular agent. It allows for precise identification of disease before treatment and then delivers a therapeutic dose of radiation specifically to diseased cells, minimizing side effects on healthy tissues. This personalized approach is revolutionizing cancer treatment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted