Radio Frequency Chip Market

Radio Frequency Chip Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701012 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Radio Frequency Chip Market Size

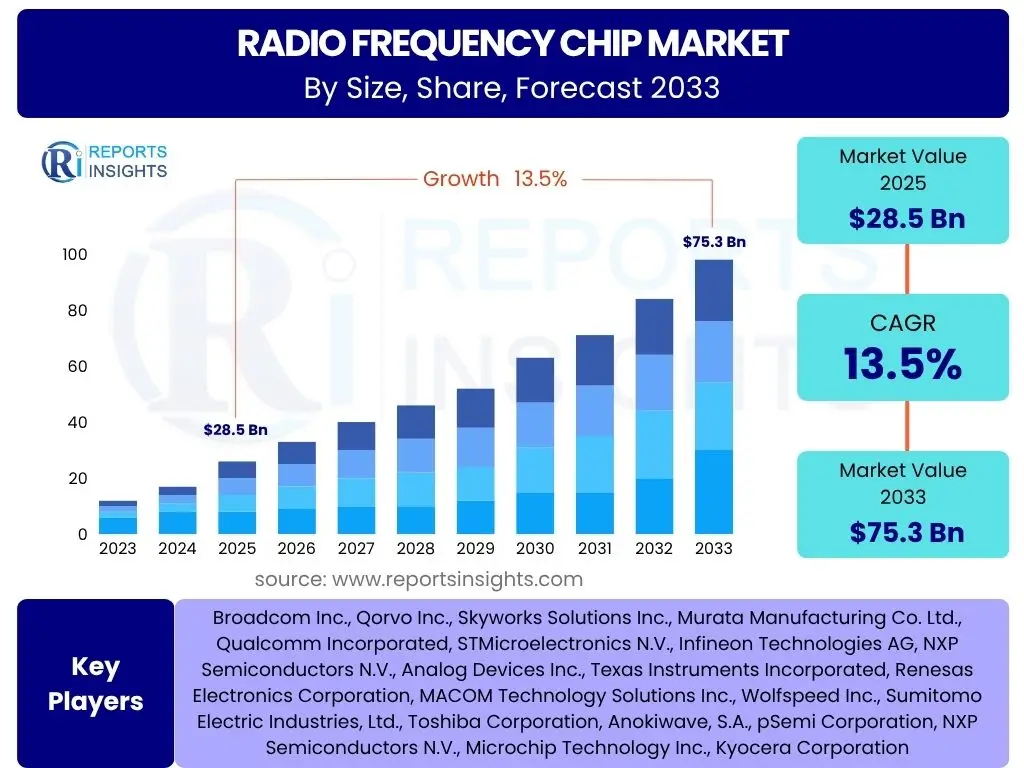

According to Reports Insights Consulting Pvt Ltd, The Radio Frequency Chip Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.5% between 2025 and 2033. The market is estimated at USD 28.5 billion in 2025 and is projected to reach USD 75.3 billion by the end of the forecast period in 2033.

Key Radio Frequency Chip Market Trends & Insights

The Radio Frequency Chip market is experiencing transformative growth, driven primarily by the global rollout of 5G networks and the pervasive expansion of the Internet of Things (IoT). Users are keen to understand how these foundational technological shifts are influencing chip design, functionality, and demand across various sectors. Furthermore, there's significant interest in advanced packaging technologies, the emergence of millimeter-wave (mmWave) applications, and the increasing integration of artificial intelligence for enhanced performance and efficiency within RF systems. The ongoing miniaturization of components and the demand for higher power efficiency in portable and smart devices also represent critical areas of inquiry regarding market trends.

As the demand for seamless connectivity and high-speed data transfer intensifies, RF chip manufacturers are focusing on developing solutions that support wider bandwidths and operate across diverse frequency spectrums. This includes advancements in compound semiconductors like Gallium Nitride (GaN) and Silicon Carbide (SiC) for high-power applications, alongside silicon-germanium (SiGe) and complementary metal-oxide-semiconductor (CMOS) technologies for integrated, cost-effective solutions. The convergence of communication, sensing, and processing capabilities within single RF chipsets is also a notable trend, enhancing system-level integration and reducing overall device footprints.

- Accelerated 5G infrastructure deployment and device proliferation.

- Explosive growth of IoT devices requiring diverse connectivity options.

- Increasing adoption of millimeter-wave (mmWave) technology for high-bandwidth applications.

- Advancements in compound semiconductor materials (GaN, SiC) for high-power and high-frequency RF applications.

- Greater integration of RF functions into System-on-Chip (SoC) solutions.

- Rising demand for RF front-end modules (FEMs) for space-saving and simplified design.

- Growing prevalence of RF sensing and radar applications in automotive and industrial sectors.

AI Impact Analysis on Radio Frequency Chip

Common user questions regarding AI's impact on Radio Frequency (RF) chips frequently revolve around how artificial intelligence can optimize chip design, enhance signal processing capabilities, and enable more intelligent wireless communication systems. There is considerable interest in AI's role in improving the efficiency of RF components, predicting performance degradation, and facilitating adaptive beamforming and spectrum management. Users also seek to understand if AI can accelerate the development cycle of new RF technologies and reduce the complexity of RF system integration, while simultaneously addressing concerns about data privacy and the computational overhead associated with on-chip AI functionalities.

AI is poised to revolutionize the RF chip landscape by fundamentally changing how these components are designed, operated, and utilized within complex systems. In the design phase, AI-powered Electronic Design Automation (EDA) tools can significantly optimize circuit layouts, antenna designs, and power amplifier linearity, leading to faster time-to-market and superior performance. During operation, AI algorithms can enable RF chips to intelligently adapt to changing environmental conditions, optimize power consumption, and improve signal integrity through dynamic adjustments. This translates to more robust and energy-efficient wireless communication, particularly critical for demanding applications in 5G, satellite communications, and autonomous vehicles.

- Enabling intelligent RF front-ends for adaptive beamforming and antenna management.

- Optimizing RF circuit design and simulation through AI-powered EDA tools, reducing development cycles.

- Enhancing signal processing and noise reduction for improved communication quality and efficiency.

- Facilitating predictive maintenance and fault detection in RF systems.

- Enabling cognitive radio capabilities for dynamic spectrum access and interference mitigation.

- Improving power efficiency and thermal management in RF components through AI-driven control.

- Developing advanced sensing and radar capabilities with AI for enhanced object detection and classification.

Key Takeaways Radio Frequency Chip Market Size & Forecast

Analysis of common user questions regarding the Radio Frequency Chip market size and forecast consistently highlights interest in the market's robust growth trajectory, driven by fundamental technological shifts. Users are keen to grasp the primary factors propelling this expansion, particularly the profound influence of 5G deployments and the burgeoning Internet of Things ecosystem. There is also significant emphasis on identifying the key application areas that will underpin demand, such as consumer electronics, automotive, and telecommunications, and understanding how regional dynamics will shape future market distribution. The overarching insight is a market poised for substantial expansion, underpinned by relentless innovation in connectivity and sensing technologies.

The forecast indicates a sustained high growth rate for the RF chip market, reflecting its critical role in the digital transformation across industries. The increasing complexity of wireless communication, coupled with the need for higher bandwidth, lower latency, and enhanced reliability, necessitates continuous advancements in RF chip technology. This market's future will be defined by the ability of manufacturers to deliver highly integrated, energy-efficient, and versatile RF solutions that can support the diverse requirements of emerging applications, from smart cities to advanced robotics and space exploration. Strategic investments in R&D and manufacturing capacity will be crucial for capitalizing on these growth opportunities.

- The RF chip market is projected for significant growth, reaching USD 75.3 billion by 2033, driven by a 13.5% CAGR.

- 5G expansion and IoT proliferation are the primary catalysts for market expansion.

- Automotive, consumer electronics, and telecommunications are key application segments driving demand.

- Technological advancements in mmWave and advanced materials like GaN are crucial for future growth.

- Asia Pacific is expected to remain the largest and fastest-growing region due to manufacturing hubs and large-scale 5G deployments.

- Integration of AI for design optimization and operational efficiency will be a key differentiator.

Radio Frequency Chip Market Drivers Analysis

The Radio Frequency Chip market is propelled by several robust macroeconomic and technological factors. The global proliferation of 5G networks stands out as the most significant driver, demanding sophisticated RF front-end modules, power amplifiers, and filters to handle higher frequencies and wider bandwidths. Concurrently, the exponential growth of the Internet of Things (IoT) across consumer, industrial, and enterprise applications necessitates a diverse range of low-power, compact, and highly integrated RF chips for connectivity. These trends collectively underscore the increasing reliance on seamless and high-speed wireless communication, which directly translates into heightened demand for advanced RF chip solutions.

Beyond telecommunications and IoT, the burgeoning automotive industry is also a substantial driver, with the increasing adoption of advanced driver-assistance systems (ADAS), infotainment, and vehicle-to-everything (V2X) communication technologies. These applications rely heavily on RF chips for radar, GPS, and wireless connectivity, contributing significantly to market expansion. Furthermore, the growth in satellite communications, aerospace and defense applications, and the industrial automation sector, all requiring robust and reliable wireless links, further amplifies the demand for specialized RF components capable of operating in diverse and challenging environments. Continuous innovation in RF material science and packaging technologies supports these demanding applications, sustaining market momentum.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Network Rollout | +4.5% | Global, particularly APAC, North America, Europe | Short-term (2025-2028) & Mid-term (2028-2030) |

| Proliferation of IoT Devices | +3.8% | Global, across all developing and developed economies | Short-term (2025-2028) & Long-term (2030-2033) |

| Increasing Adoption of ADAS & V2X in Automotive | +2.7% | North America, Europe, Asia Pacific (Japan, South Korea, China) | Mid-term (2028-2030) & Long-term (2030-2033) |

| Expansion of Satellite Communication & Aerospace | +1.5% | North America, Europe, select APAC countries | Mid-term (2028-2030) & Long-term (2030-2033) |

Radio Frequency Chip Market Restraints Analysis

Despite robust growth prospects, the Radio Frequency Chip market faces several significant restraints that could impede its full potential. One primary challenge is the escalating cost of research and development (R&D) associated with advanced RF technologies. Developing chips for higher frequencies, greater integration, and enhanced power efficiency requires substantial investment in cutting-edge materials, intricate design tools, and complex manufacturing processes. This high entry barrier can limit market participation and innovation, particularly for smaller enterprises, concentrating market power among a few large players with deep pockets. Moreover, the intricate nature of RF design often leads to longer development cycles, delaying time-to-market for new products.

Another crucial restraint involves the complexities and vulnerabilities within the global supply chain for semiconductor components. Geopolitical tensions, trade disputes, and natural disasters can disrupt the availability of critical raw materials, manufacturing capacities, and logistics, leading to shortages, price volatility, and delayed production of RF chips. Additionally, the increasing demand for spectrum efficiency presents a technical constraint; as wireless communication densifies, managing interference and ensuring clear spectrum access becomes more challenging. Regulatory hurdles and varying spectrum allocation policies across different regions can also complicate the design and deployment of global RF solutions, adding another layer of complexity for manufacturers and service providers alike.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research and Development Costs | -1.2% | Global, impacting all major R&D hubs | Short-term (2025-2028) |

| Complex Global Supply Chain Volatility | -1.0% | Global, particularly East Asia (manufacturing) & consuming regions | Short-term (2025-2028) & Mid-term (2028-2030) |

| Spectrum Scarcity and Regulatory Challenges | -0.8% | Region-specific, varies by country regulations | Mid-term (2028-2030) & Long-term (2030-2033) |

| Thermal Management and Power Consumption Issues | -0.5% | Global, impacting high-density applications | Short-term (2025-2028) |

Radio Frequency Chip Market Opportunities Analysis

The Radio Frequency Chip market is rich with opportunities, particularly in the realm of emerging technologies and untapped application areas. The expansion into millimeter-wave (mmWave) frequencies for 5G offers significant avenues for growth, enabling ultra-high bandwidth and low-latency communication previously unattainable. This necessitates the development of new RF components, including advanced antennas, transceivers, and power amplifiers optimized for these higher frequency bands. Furthermore, the increasing integration of RF capabilities into non-traditional sectors such as healthcare (for remote monitoring and diagnostics) and precision agriculture (for sensor networks) presents substantial new market segments for specialized RF chip solutions, moving beyond conventional communication applications.

Another compelling opportunity lies in the development of next-generation materials like Gallium Nitride (GaN) and Silicon Carbide (SiC) for high-power and high-frequency RF applications. These materials offer superior performance characteristics compared to traditional silicon, enabling more efficient power amplifiers and robust components crucial for 5G base stations, radar systems, and electric vehicles. The growing demand for satellite-based connectivity, driven by initiatives for global internet access and specialized industrial applications, also presents a lucrative market for RF chips designed for space-grade reliability and performance. Moreover, the continuous pursuit of miniaturization and energy efficiency opens doors for innovative packaging technologies and highly integrated system-on-chip (SoC) solutions, reducing overall system costs and enabling new form factors for connected devices.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into mmWave Applications | +3.0% | North America, APAC (China, South Korea), Europe | Mid-term (2028-2030) & Long-term (2030-2033) |

| Advancements in GaN and SiC Materials | +2.2% | Global, driven by high-power applications | Mid-term (2028-2030) & Long-term (2030-2033) |

| Growth in Satellite Communication and Non-Terrestrial Networks | +1.8% | Global, particularly North America, Europe | Mid-term (2028-2030) & Long-term (2030-2033) |

| Integration in New Verticals (Healthcare, Smart Cities) | +1.5% | Global, varying by regional adoption pace | Long-term (2030-2033) |

Radio Frequency Chip Market Challenges Impact Analysis

The Radio Frequency Chip market, while dynamic, contends with several significant challenges that demand innovative solutions. One primary challenge is the relentless pressure for miniaturization and higher integration. As devices become smaller and more feature-rich, RF chips must integrate multiple functionalities (transceiver, power amplifier, filter, switch) into increasingly compact footprints, often pushing the limits of current manufacturing capabilities. This drives up design complexity and manufacturing costs, requiring sophisticated packaging technologies and multi-chip modules. Furthermore, managing the thermal dissipation in these highly integrated, high-frequency chips is a critical engineering hurdle, as excessive heat can degrade performance and reliability, posing a substantial barrier to efficient operation, especially in densely packed electronic systems.

Another significant challenge lies in achieving optimal power efficiency across diverse operating conditions. With the proliferation of battery-powered IoT devices and the growing demand for sustainable technology, RF chips must consume minimal power while maintaining high performance. This often involves trade-offs between linearity, efficiency, and bandwidth, requiring advanced circuit designs and material science innovations to balance these competing requirements. Additionally, ensuring electromagnetic compatibility (EMC) and mitigating interference in increasingly crowded wireless environments poses a constant challenge. Cybersecurity threats to wireless communication, particularly in critical infrastructure and sensitive data transmission, also present an evolving challenge, demanding robust security features integrated directly into RF chip architectures to protect data integrity and prevent unauthorized access.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization and High Integration Demands | -1.0% | Global, impacting consumer electronics & telecom | Short-term (2025-2028) |

| Thermal Management and Power Efficiency | -0.9% | Global, crucial for battery-powered & high-power applications | Short-term (2025-2028) & Mid-term (2028-2030) |

| Maintaining Signal Integrity and Mitigating Interference | -0.7% | Global, especially in dense urban environments | Mid-term (2028-2030) |

| Rising Cybersecurity Concerns in Wireless Communication | -0.5% | Global, critical for sensitive applications | Mid-term (2028-2030) & Long-term (2030-2033) |

Radio Frequency Chip Market - Updated Report Scope

This market research report offers a comprehensive analysis of the Radio Frequency Chip market, covering historical trends, current market dynamics, and future growth projections from 2025 to 2033. It delves into the key drivers, restraints, opportunities, and challenges shaping the industry, providing a granular view of market segmentation by product type, application, frequency band, and material. The report includes an in-depth competitive landscape analysis, profiling leading companies and their strategic initiatives, alongside a detailed regional outlook highlighting market performance across major geographical areas. Special emphasis is placed on the impact of emerging technologies like 5G, IoT, AI, and advanced materials, ensuring stakeholders receive actionable insights for strategic decision-making in this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 billion |

| Market Forecast in 2033 | USD 75.3 billion |

| Growth Rate | 13.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Broadcom Inc., Qorvo Inc., Skyworks Solutions Inc., Murata Manufacturing Co. Ltd., Qualcomm Incorporated, STMicroelectronics N.V., Infineon Technologies AG, NXP Semiconductors N.V., Analog Devices Inc., Texas Instruments Incorporated, Renesas Electronics Corporation, MACOM Technology Solutions Inc., Wolfspeed Inc., Sumitomo Electric Industries, Ltd., Toshiba Corporation, Anokiwave, S.A., pSemi Corporation, NXP Semiconductors N.V., Microchip Technology Inc., Kyocera Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Radio Frequency Chip market is meticulously segmented to provide a comprehensive understanding of its diverse components and their respective contributions to overall market dynamics. This granular breakdown allows for precise analysis of market trends, opportunities, and competitive landscapes within specific product categories, application sectors, frequency ranges, and material compositions. Understanding these segmentations is crucial for stakeholders to identify high-growth areas, develop targeted strategies, and innovate in response to specific market demands. Each segment reflects unique technological requirements, market drivers, and competitive pressures, shaping its individual trajectory within the broader RF chip ecosystem.

The segmentation by type categorizes chips based on their primary function within an RF system, such as signal amplification, filtering, or mixing, highlighting the varied needs across wireless communication chains. Application segmentation reveals the end-use industries driving demand, from high-volume consumer electronics to specialized aerospace and defense systems. Frequency band segmentation distinguishes between chips operating in established sub-6 GHz bands and emerging millimeter-wave frequencies, critical for next-generation wireless technologies. Lastly, material segmentation examines the underlying semiconductor technologies, such as Gallium Arsenide (GaAs), Silicon Germanium (SiGe), Silicon (CMOS), Gallium Nitride (GaN), and Silicon Carbide (SiC), each offering distinct advantages in terms of power, frequency, and cost efficiency, thereby influencing their adoption across different market niches.

- By Type:

- Transceivers

- Power Amplifiers

- Filters

- Switches

- Mixers

- Oscillators

- Modulators/Demodulators

- Others (e.g., Duplexers, Attenuators)

- By Application:

- Consumer Electronics (Smartphones, Wearables, Laptops, IoT Devices)

- Telecommunications (5G Base Stations, Network Infrastructure, CPE)

- Automotive (ADAS, Infotainment, V2X Communication, Radar Systems)

- Industrial (Industrial IoT, Automation, Smart Manufacturing)

- Aerospace & Defense (Radar, Satellite Communication, Electronic Warfare)

- Healthcare (Medical Imaging, Remote Patient Monitoring, Wearable Diagnostics)

- Others (e.g., Smart Cities, Agriculture, Energy)

- By Frequency Band:

- Sub-6 GHz

- Millimeter-Wave (mmWave)

- Others (e.g., Ultra-Wideband)

- By Material:

- Gallium Arsenide (GaAs)

- Silicon Germanium (SiGe)

- Silicon (CMOS)

- Gallium Nitride (GaN)

- Silicon Carbide (SiC)

Regional Highlights

- North America: A leading region in RF chip innovation and adoption, particularly in aerospace and defense, advanced telecommunications (5G deployment), and automotive radar. Strong R&D capabilities and early adoption of new technologies drive market growth.

- Europe: Significant growth fueled by the automotive sector's demand for radar and connectivity chips, robust industrial IoT applications, and ongoing 5G expansion. Germany, France, and the UK are key contributors.

- Asia Pacific (APAC): The largest and fastest-growing market for RF chips, propelled by massive 5G infrastructure investments, high production volumes of consumer electronics (smartphones, wearables), and expanding automotive manufacturing. China, South Korea, Japan, and Taiwan are major hubs for both manufacturing and consumption.

- Latin America: Emerging market with growing investments in telecommunications infrastructure and increasing penetration of smartphones and IoT devices, leading to rising demand for RF chips.

- Middle East and Africa (MEA): Gradually increasing adoption of 5G technologies and smart city initiatives, driving demand for RF communication components. Developing regions offer long-term growth potential as infrastructure matures.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Radio Frequency Chip Market.- Broadcom Inc.

- Qorvo Inc.

- Skyworks Solutions Inc.

- Murata Manufacturing Co. Ltd.

- Qualcomm Incorporated

- STMicroelectronics N.V.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Analog Devices Inc.

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- MACOM Technology Solutions Inc.

- Wolfspeed Inc.

- Sumitomo Electric Industries, Ltd.

- Toshiba Corporation

- Anokiwave, S.A.

- pSemi Corporation

- Microchip Technology Inc.

- Kyocera Corporation

Frequently Asked Questions

Analyze common user questions about the Radio Frequency Chip market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Radio Frequency (RF) Chips?

Radio Frequency (RF) chips are semiconductor devices designed to operate within the radio frequency spectrum, enabling wireless communication by processing radio signals. They are essential components in virtually all wireless electronic devices, responsible for transmitting, receiving, and managing signals for technologies like Wi-Fi, Bluetooth, cellular networks (including 5G), GPS, and various sensing applications.

What is driving the growth of the RF Chip Market?

The primary drivers include the accelerated global rollout of 5G networks, the pervasive expansion of the Internet of Things (IoT) across consumer and industrial applications, and the increasing adoption of wireless technologies in sectors such as automotive (ADAS, V2X), aerospace, and industrial automation. These trends demand advanced RF chips for high-speed, low-latency, and reliable wireless connectivity.

How is 5G impacting the demand for RF Chips?

5G significantly impacts RF chip demand by requiring chips capable of operating at higher frequencies (including millimeter-wave), supporting wider bandwidths, and handling more complex modulation schemes. This drives demand for advanced RF front-end modules, power amplifiers, filters, and transceivers that offer enhanced performance, integration, and power efficiency for 5G smartphones, base stations, and connected devices.

What are the key applications of RF Chips?

Key applications span diverse sectors including consumer electronics (smartphones, wearables, laptops, smart home devices), telecommunications (5G infrastructure, cellular networks), automotive (radar systems, V2X communication, infotainment), industrial IoT (sensor networks, automation), aerospace and defense (radar, satellite communication), and healthcare (remote monitoring, medical imaging).

What are the major challenges faced by the RF Chip Market?

Major challenges include the escalating costs and complexity of R&D for advanced RF technologies, the need for extreme miniaturization and higher integration while managing thermal issues, achieving optimal power efficiency for battery-powered devices, and navigating global supply chain volatilities. Spectrum scarcity and cybersecurity concerns also present ongoing hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted