PVC Cling Film Market

PVC Cling Film Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705415 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

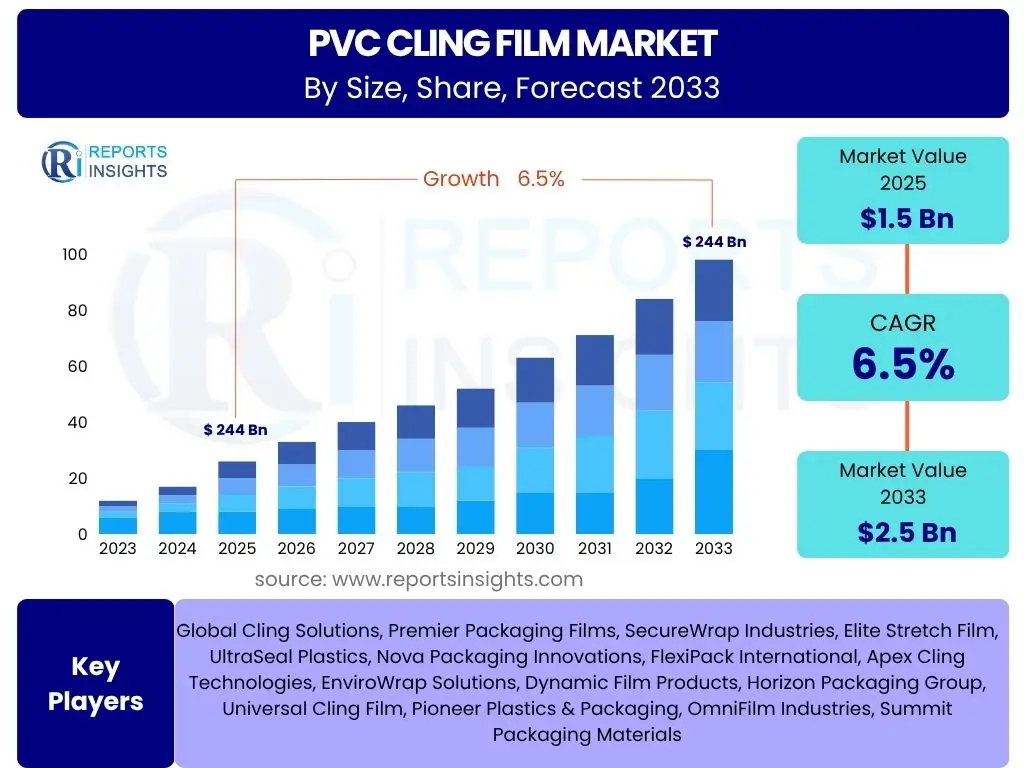

PVC Cling Film Market Size

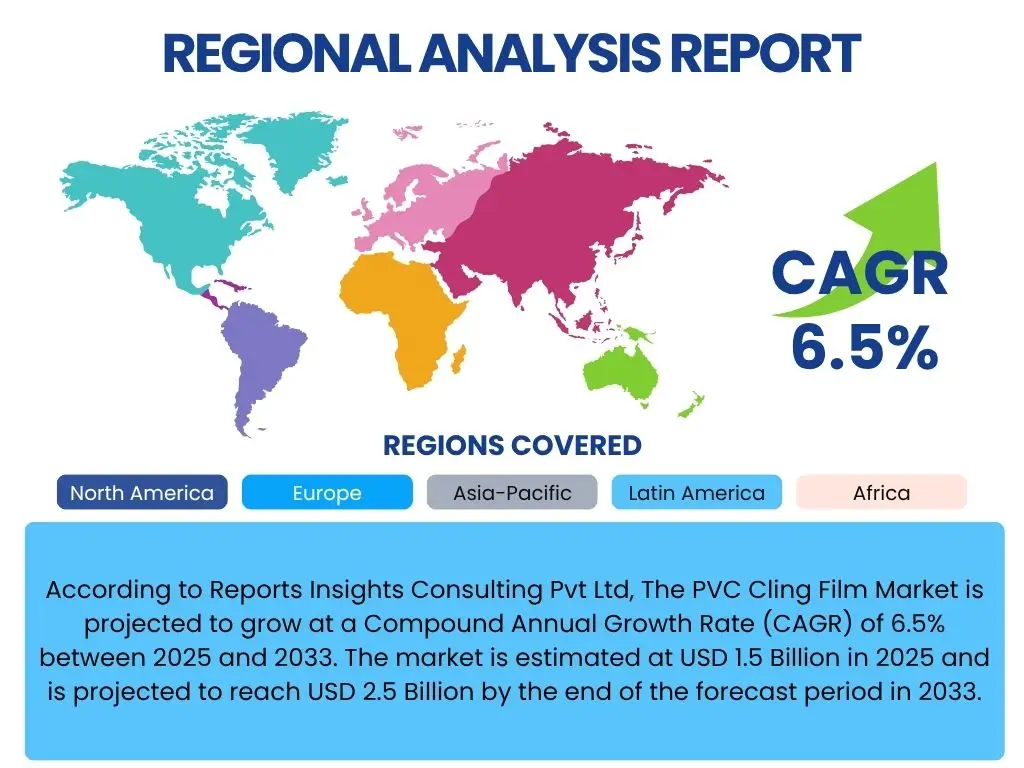

According to Reports Insights Consulting Pvt Ltd, The PVC Cling Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 1.5 Billion in 2025 and is projected to reach USD 2.5 Billion by the end of the forecast period in 2033.

Key PVC Cling Film Market Trends & Insights

The PVC cling film market is undergoing significant transformations driven by evolving consumer demands, regulatory shifts, and technological advancements. Key trends indicate a dual focus on enhanced functional properties, such as improved barrier performance and stretchability, alongside a growing imperative for sustainability. Users are keenly interested in understanding how these trends impact product innovation, market adoption, and long-term viability, especially concerning environmental considerations and the search for more eco-friendly alternatives without compromising essential packaging attributes like freshness preservation and food safety. The convergence of convenience and responsible consumption is a central theme shaping current and future market dynamics.

Furthermore, the expansion of the food delivery and e-commerce sectors has substantially boosted the demand for effective and reliable packaging solutions, including PVC cling film. This has led to an increased emphasis on packaging that can withstand transport, maintain product integrity, and offer clear visibility. Simultaneously, there is a rising awareness among consumers regarding food waste, driving demand for packaging solutions that extend the shelf life of perishable goods. These factors collectively underscore the market's dynamic nature, requiring continuous adaptation and innovation from manufacturers to meet diverse and often conflicting stakeholder expectations.

- Growing demand for extended shelf life solutions in food packaging, particularly for fresh produce, meats, and dairy products.

- Increased adoption in the foodservice and catering industries due to its convenience, hygiene, and cost-effectiveness.

- Rising consumer preference for transparent packaging that allows for product visibility and aesthetic appeal.

- Emphasis on enhancing barrier properties to improve food preservation and reduce spoilage.

- Development of specialized PVC cling films with enhanced stretch, clarity, and anti-fog capabilities for specific applications.

AI Impact Analysis on PVC Cling Film

The integration of Artificial intelligence (AI) within the PVC cling film industry is poised to revolutionize various operational facets, from raw material procurement to distribution. Users frequently inquire about AI's potential to optimize manufacturing processes, improve quality control, and enhance supply chain efficiency. AI-driven analytics can predict machinery failures, optimize energy consumption, and fine-tune production parameters, leading to substantial cost reductions and improved output consistency. Furthermore, AI can provide granular insights into market demand and consumer behavior, enabling manufacturers to adjust production volumes and product specifications proactively, thereby minimizing waste and maximizing responsiveness.

Beyond manufacturing, AI holds significant promise in managing the complex supply chains characteristic of the packaging industry. Predictive analytics powered by AI can forecast demand fluctuations with greater accuracy, optimize inventory levels, and streamline logistics, ensuring timely delivery and reducing storage costs. Moreover, AI is being explored for its role in developing more sustainable practices, such as optimizing material usage to reduce waste and identifying opportunities for circular economy models within the packaging lifecycle. While the direct application of AI to the chemical composition of PVC cling film is limited, its influence on the operational and strategic aspects of production, distribution, and market analysis is substantial and growing.

- Optimized production lines: AI algorithms can analyze real-time data from manufacturing equipment to predict maintenance needs, prevent breakdowns, and optimize production speeds and temperatures, leading to higher efficiency and reduced downtime.

- Enhanced quality control: AI-powered vision systems can detect even minute defects in PVC film during production, ensuring consistent product quality and reducing waste from flawed batches, surpassing the limitations of manual inspection.

- Predictive demand forecasting: AI tools analyze historical sales data, seasonal trends, and external factors to provide highly accurate demand forecasts, enabling manufacturers to optimize inventory levels and reduce overproduction or stockouts.

- Supply chain optimization: AI can improve logistics and distribution by optimizing routes, managing warehouse operations, and predicting potential disruptions, leading to faster delivery times and lower transportation costs for PVC cling film.

- Sustainable manufacturing initiatives: AI can identify opportunities for energy savings in production processes and optimize material usage, contributing to a reduced carbon footprint and more resource-efficient operations within PVC cling film manufacturing.

Key Takeaways PVC Cling Film Market Size & Forecast

The PVC cling film market is set for robust expansion over the forecast period, driven primarily by the sustained demand from the food packaging sector and the burgeoning e-commerce industry. A critical takeaway is the dual emphasis on product functionality and environmental responsibility, where innovations in barrier properties and the exploration of sustainable alternatives will be pivotal for market leadership. Manufacturers are increasingly focused on balancing the convenience and efficacy of PVC cling film with the imperative to address global concerns regarding plastic waste and circularity. This necessitates a strategic pivot towards resource-efficient production and the development of films that meet evolving regulatory and consumer expectations.

Moreover, the market's growth trajectory is influenced by global urbanization, rising disposable incomes, and the expansion of organized retail and foodservice industries, particularly in emerging economies. These factors contribute to a higher consumption of packaged food items, directly stimulating demand for effective wrapping solutions. The forecast indicates a market poised for continued innovation, with companies investing in research and development to create films that offer superior performance characteristics while mitigating their environmental footprint. Understanding these key dynamics is essential for stakeholders navigating the complexities and opportunities within this essential packaging segment.

- The PVC cling film market demonstrates significant growth potential, driven primarily by the expanding food and beverage industry and increasing demand for convenient packaging solutions.

- Innovations focusing on improved barrier properties and stretchability are critical for maintaining competitive advantage and meeting diverse application requirements.

- Sustainability concerns and regulatory pressures are prompting manufacturers to explore alternative materials and more eco-friendly production processes, influencing long-term market trends.

- The rise of e-commerce and food delivery services significantly contributes to market expansion, increasing the need for robust and reliable food preservation packaging.

- Emerging economies, particularly in Asia Pacific, are expected to be key growth regions due to rapid urbanization, changing lifestyles, and growing organized retail sectors.

PVC Cling Film Market Drivers Analysis

The PVC cling film market is propelled by a confluence of factors, primarily centered around the pervasive demand for efficient food packaging and the expansion of the retail sector. The global population's increasing reliance on packaged and convenience foods, coupled with a heightened awareness of food hygiene and preservation, directly stimulates the need for reliable wrapping solutions. PVC cling film's inherent properties, such as excellent stretchability, adhesion, and transparency, make it an ideal choice for extending the shelf life of perishable goods, thereby reducing food waste and supporting retail display appeal. This sustained demand from households, commercial kitchens, and large-scale food processing units forms the bedrock of market growth.

Furthermore, the rapid growth of the e-commerce and food delivery industries has significantly augmented the demand for secure and protective packaging. As more consumers opt for online grocery shopping and prepared meal deliveries, the need for packaging that can maintain freshness and prevent contamination during transit becomes paramount. This shift in consumer purchasing habits, alongside continuous advancements in food processing and distribution logistics, reinforces PVC cling film's position as an indispensable packaging material. Consequently, manufacturers are focusing on optimizing film properties to meet these evolving logistical challenges and consumer expectations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for food packaging | +1.8% | Global, particularly APAC and Europe | 2025-2033 |

| Expansion of organized retail and foodservice | +1.5% | North America, Europe, China, India | 2025-2033 |

| Rising awareness of food safety and hygiene | +1.2% | Global | 2025-2033 |

| Increasing adoption in e-commerce and food delivery | +1.0% | Global, high impact in urban areas | 2025-2033 |

PVC Cling Film Market Restraints Analysis

Despite its widespread utility, the PVC cling film market faces significant restraints, primarily stemming from mounting environmental concerns and the evolving regulatory landscape surrounding plastic materials. The non-biodegradable nature of conventional PVC film and its perceived contribution to plastic pollution have led to increased scrutiny from environmental organizations, governments, and consumers alike. This has prompted several regions to implement stringent regulations or even bans on certain single-use plastic products, including some forms of PVC film, which directly impacts market growth. The negative public perception often associated with PVC, despite its functional advantages, also creates a challenging operating environment for manufacturers.

Furthermore, the market faces intense competition from alternative packaging materials that are often marketed as more sustainable or environmentally friendly, such as polyethylene (PE) cling film, bio-based films, and various paper-based solutions. While these alternatives may not always offer the same cost-effectiveness or performance as PVC in all applications, their growing acceptance poses a significant challenge. Additionally, fluctuations in the prices of raw materials, particularly crude oil derivatives, can impact production costs and profit margins for PVC cling film manufacturers, contributing to market volatility. These combined pressures necessitate continuous innovation and strategic adaptation from industry players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental concerns and plastic pollution | -1.5% | Global, particularly Europe and North America | 2025-2033 |

| Strict government regulations and bans on plastics | -1.3% | Europe, North America, some Asian countries | 2025-2033 |

| Competition from alternative packaging materials | -1.0% | Global | 2025-2033 |

| Fluctuations in raw material prices | -0.8% | Global | 2025-2033 |

PVC Cling Film Market Opportunities Analysis

Despite existing restraints, significant opportunities are emerging within the PVC cling film market, primarily driven by technological advancements and the pursuit of enhanced product attributes. The development of advanced formulations that improve film properties such as anti-fogging, enhanced barrier protection, and greater stretchability presents a notable avenue for growth. These innovations allow PVC cling film to serve more demanding applications, particularly in specialized food packaging where maintaining visual clarity and extending freshness are paramount. Investing in research and development to create "smart" films or films with integrated features can open new market segments and reinforce PVC's competitive edge.

Furthermore, the expansion into untapped or underserved markets, particularly in developing regions with burgeoning retail and food service sectors, represents a substantial opportunity. As urbanization and disposable incomes rise in these areas, the demand for packaged food and convenient solutions is expected to surge. Manufacturers can leverage their expertise to cater to these growing markets by offering cost-effective and functionally superior PVC cling film products. Moreover, collaboration with food processing companies and retailers to develop customized packaging solutions tailored to specific product needs and supply chain requirements can unlock new revenue streams and foster stronger market relationships.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological advancements in film properties | +1.5% | Global, high impact in developed markets | 2025-2033 |

| Expansion into emerging markets with growing retail sectors | +1.3% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Development of specialized and customized films | +1.0% | Global | 2025-2033 |

| Increasing demand for convenience foods and ready-to-eat meals | +0.8% | Global | 2025-2033 |

PVC Cling Film Market Challenges Impact Analysis

The PVC cling film market faces notable challenges, primarily centered on navigating the complex landscape of environmental sustainability and public perception. The pervasive concern over plastic waste and its impact on ecosystems compels manufacturers to continually justify the use of PVC, which is often perceived negatively compared to other materials. This necessitates significant investment in advocating for PVC's benefits in specific applications, such as its superior cling and barrier properties, while also exploring avenues for end-of-life solutions. Addressing these public and regulatory pressures effectively requires a proactive approach to communication and potential innovation in material science or recycling infrastructure.

Furthermore, managing the volatility of raw material costs and ensuring supply chain resilience pose continuous operational challenges. The production of PVC is dependent on petrochemical derivatives, making it susceptible to global oil price fluctuations and geopolitical events. Companies must implement robust supply chain management strategies and potentially diversify their sourcing to mitigate these risks. Additionally, evolving food safety regulations across different regions demand continuous compliance and adaptation in film formulations and manufacturing processes, adding to the operational complexities and compliance costs for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative public perception regarding plastics and PVC | -1.2% | Global, stronger in developed regions | 2025-2033 |

| Complexity of waste management and recycling infrastructure | -1.0% | Global | 2025-2033 |

| Intense competition and pricing pressures | -0.9% | Global | 2025-2033 |

| Compliance with evolving food safety and packaging regulations | -0.7% | Regional specific (Europe, North America, etc.) | 2025-2033 |

PVC Cling Film Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the PVC Cling Film market, encompassing historical data from 2019 to 2023, current market estimations for 2024, and detailed forecasts stretching through 2033. The scope includes an exhaustive examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report is designed to offer strategic insights into market dynamics, competitive landscapes, and emerging trends, aiding stakeholders in informed decision-making and identifying potential growth avenues within the PVC cling film industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.5 Billion |

| Growth Rate | 6.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Cling Solutions, Premier Packaging Films, SecureWrap Industries, Elite Stretch Film, UltraSeal Plastics, Nova Packaging Innovations, FlexiPack International, Apex Cling Technologies, EnviroWrap Solutions, Dynamic Film Products, Horizon Packaging Group, Universal Cling Film, Pioneer Plastics & Packaging, OmniFilm Industries, Summit Packaging Materials |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The PVC cling film market is comprehensively segmented to provide a granular understanding of its diverse applications and target audiences. This segmentation allows for precise analysis of consumer behavior, industry-specific demands, and regional preferences, enabling stakeholders to identify key growth pockets and tailor their strategies accordingly. The market's structure reflects the varied requirements of household consumers, commercial enterprises, and industrial clients, highlighting the versatility and adaptability of PVC cling film in a multitude of settings. Each segment presents unique opportunities and challenges, necessitating distinct approaches for market penetration and expansion.

Further subdivision within these broad categories, such as distinguishing between food-grade and non-food-grade films, or analyzing usage across different food product categories, provides deeper insights into specific market dynamics. Understanding these nuances is crucial for product development, marketing, and distribution strategies. The robust growth in segments like commercial food service and e-commerce-driven household consumption underscores the adaptability of PVC cling film in meeting modern packaging needs, despite the overarching focus on sustainability and regulatory compliance.

- By Type: Food Grade, Non-Food Grade

- By Application: Household, Commercial (Food Service, Retail), Industrial (Medical, Others)

- By End-Use Industry: Food & Beverages (Meat, Poultry & Seafood, Dairy & Bakery, Fruits & Vegetables, Others), Supermarkets & Hypermarkets, Hospitality & Catering, Healthcare & Pharmaceutical, Logistics & Packaging

- By Distribution Channel: Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Direct Sales/B2B

Regional Highlights

- North America: This region is characterized by a mature market with high awareness of food safety and strong regulatory frameworks. Growth is driven by the robust organized retail sector, demand for convenience foods, and the expanding e-commerce segment. Innovation in sustainable packaging solutions and advanced film properties is a key focus.

- Europe: Europe is a highly regulated market with increasing emphasis on environmental sustainability and circular economy principles. While facing stringent regulations concerning plastic use, the demand for PVC cling film persists due to its performance benefits in food preservation. Focus is on developing films with reduced environmental impact and optimizing recycling infrastructure.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for PVC cling film, fueled by rapid urbanization, increasing disposable incomes, and the burgeoning food processing and retail industries, particularly in China and India. The region exhibits high demand for cost-effective packaging solutions and is a major manufacturing hub.

- Latin America: This region shows steady growth driven by expanding retail chains, improving living standards, and increasing consumption of packaged food. Brazil and Mexico are key markets, with opportunities arising from growing food service sectors and developing e-commerce infrastructure.

- Middle East and Africa (MEA): The MEA region is experiencing growth due to rising population, changing dietary habits, and investments in the hospitality and food processing sectors. The demand for effective food preservation is increasing, especially in countries like Saudi Arabia and UAE. Market expansion is also supported by infrastructural development and tourism.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the PVC Cling Film Market.- Global Cling Solutions

- Premier Packaging Films

- SecureWrap Industries

- Elite Stretch Film

- UltraSeal Plastics

- Nova Packaging Innovations

- FlexiPack International

- Apex Cling Technologies

- EnviroWrap Solutions

- Dynamic Film Products

- Horizon Packaging Group

- Universal Cling Film

- Pioneer Plastics & Packaging

- OmniFilm Industries

- Summit Packaging Materials

Frequently Asked Questions

What is PVC Cling Film primarily used for?

PVC Cling Film is primarily used for food packaging, particularly for wrapping fresh produce, meats, dairy products, and baked goods. Its excellent cling, stretch, and barrier properties help preserve freshness, prevent contamination, and extend the shelf life of perishable items, making it indispensable in households, supermarkets, and commercial kitchens globally.

What are the main advantages of PVC Cling Film?

The main advantages of PVC Cling Film include its superior stretchability and self-adhesion, which allow it to tightly conform to various shapes and seal containers effectively. It offers good clarity for product visibility, excellent barrier properties against oxygen and moisture to extend food freshness, and is generally cost-effective. Additionally, many formulations include anti-fog properties, crucial for displaying chilled foods.

Are there environmental concerns associated with PVC Cling Film?

Yes, environmental concerns associated with PVC Cling Film primarily revolve around its non-biodegradability and the challenges in recycling it through conventional municipal waste streams. There are also concerns about potential plasticizer migration and the environmental impact of PVC production and disposal. These factors drive ongoing research into more sustainable alternatives and improved end-of-life solutions.

How do regulations impact the PVC Cling Film market?

Regulations significantly impact the PVC Cling Film market by dictating material safety standards, permissible additives (e.g., plasticizers), and increasingly, requirements for recyclability or restrictions on single-use plastics. Governments and food safety authorities impose strict rules to ensure the film's safety for food contact and to mitigate environmental impact, leading manufacturers to adapt formulations and production processes to ensure compliance and market access.

What are the emerging alternatives to PVC Cling Film?

Emerging alternatives to PVC Cling Film include polyethylene (PE) cling film, which is more readily recyclable in some regions, and bio-based films derived from renewable resources like polylactic acid (PLA) or starch. Additionally, wax paper, silicone wraps, reusable containers, and various paper-based packaging solutions are gaining traction as consumers and industries seek more sustainable options to reduce plastic dependency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted