Public Sector Outsourcing Market

Public Sector Outsourcing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709699 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

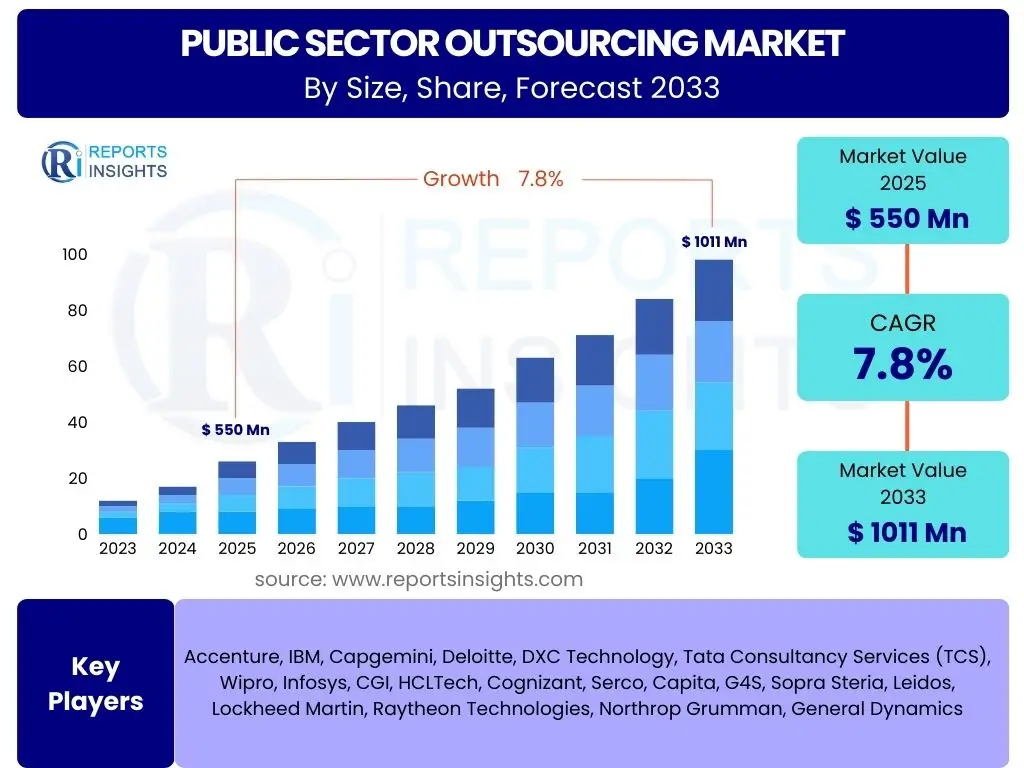

Public Sector Outsourcing Market Size

According to Reports Insights Consulting Pvt Ltd, The Public Sector Outsourcing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 550 Billion in 2025 and is projected to reach USD 1011 Billion by the end of the forecast period in 2033.

Key Public Sector Outsourcing Market Trends & Insights

User queries regarding public sector outsourcing trends frequently highlight the shift towards digital transformation, the increasing demand for specialized expertise, and the imperative for cost optimization. Organizations are increasingly looking beyond traditional IT outsourcing to encompass a broader range of business processes, including back-office functions, citizen services, and infrastructure management. This evolution is driven by government initiatives to modernize public services, enhance operational efficiency, and address budget constraints.

Furthermore, there is a growing emphasis on outcome-based contracts and flexible service models that can adapt to changing public needs and technological advancements. Cloud adoption within the public sector is accelerating, providing a foundation for scalable and secure outsourced services. The integration of advanced analytics and automation technologies is also becoming a critical trend, enabling more data-driven decision-making and streamlined service delivery across various government agencies.

- Accelerated digital transformation initiatives across government agencies.

- Increased adoption of cloud-based services and Software-as-a-Service (SaaS) models.

- Growing demand for specialized cybersecurity and data privacy expertise.

- Shift towards outcome-based and agile outsourcing contracts.

- Integration of automation, artificial intelligence, and machine learning for efficiency.

- Focus on enhancing citizen experience through improved service delivery.

- Emphasis on sustainable and environmentally responsible sourcing practices.

- Expansion into complex business process outsourcing (BPO) beyond traditional IT.

AI Impact Analysis on Public Sector Outsourcing

Common user questions regarding AI's impact on public sector outsourcing center on efficiency gains, cost reduction, job displacement, and data security concerns. The general sentiment points towards a significant transformative potential, where AI is seen as a tool to automate repetitive tasks, improve data analysis, and enhance citizen services, thereby freeing public servants to focus on more complex, value-added work. However, there are also prevalent concerns about the ethical implications of AI, the need for robust data governance frameworks, and the potential for a skills gap among the public sector workforce.

AI's role is evolving from mere task automation to enabling predictive analytics, personalized public services, and intelligent decision support systems. This shift mandates that outsourcing providers not only offer AI-powered solutions but also possess the expertise to integrate these technologies securely and ethically within existing public sector infrastructures. The long-term impact is expected to redefine the scope of outsourced services, placing a premium on providers capable of delivering advanced AI-driven solutions while ensuring transparency and accountability.

- Enhanced efficiency and automation of routine administrative tasks, reducing operational costs.

- Improved data analytics for better policy formulation, resource allocation, and predictive maintenance.

- Personalized and more responsive citizen services through AI-powered chatbots and virtual assistants.

- Increased demand for AI implementation and management expertise from outsourcing providers.

- Potential for workforce re-skilling and up-skilling within the public sector as AI takes over certain roles.

- Heightened focus on data privacy, security, and ethical AI development in public sector applications.

- Development of AI-driven tools for fraud detection, cybersecurity threat analysis, and anomaly detection.

- Transformation of procurement processes through AI-powered vendor selection and contract management.

Key Takeaways Public Sector Outsourcing Market Size & Forecast

User inquiries about key takeaways frequently focus on the primary growth drivers, the segments showing the most promise, and the critical success factors for public sector outsourcing initiatives. A central insight is the robust and sustained growth projected for the market, largely propelled by governments' unceasing pursuit of efficiency, digital modernization, and specialized expertise to meet evolving citizen expectations. The market's expansion is not merely incremental but reflective of a deeper strategic shift towards leveraging external capabilities for core and support functions.

Another crucial takeaway is the increasing complexity and sophistication of outsourcing engagements, moving beyond simple cost-cutting to strategic partnerships that deliver tangible outcomes, foster innovation, and build resilience. This necessitates a focus on flexible, secure, and technologically advanced solutions, with a strong emphasis on data governance and cybersecurity. Regional variations in adoption rates and service requirements also highlight the need for tailored strategies, ensuring that outsourcing initiatives align with local regulatory frameworks and specific public service demands.

- The public sector outsourcing market is experiencing significant and consistent growth, driven by digital transformation and efficiency mandates.

- Technological advancements, particularly in cloud computing, AI, and automation, are pivotal growth accelerators.

- Governments are increasingly seeking specialized expertise in areas like cybersecurity, data analytics, and citizen experience management.

- The market's future will be characterized by more strategic, outcome-focused partnerships rather than transactional engagements.

- Emphasis on robust data security, ethical considerations, and compliance will remain paramount for outsourcing success.

- Emerging markets and specific service segments like smart city solutions and healthcare IT present substantial opportunities.

Public Sector Outsourcing Market Drivers Analysis

The public sector outsourcing market is primarily driven by governments' continuous efforts to enhance operational efficiency, reduce costs, and access specialized capabilities not readily available in-house. Budgetary pressures often compel public entities to seek external providers who can deliver services more cost-effectively while maintaining or improving quality. This pursuit of fiscal prudence is a fundamental catalyst for outsourcing decisions across various levels of government.

Furthermore, the accelerating pace of digital transformation and technological innovation necessitates expertise that public sector organizations may lack or find challenging to develop internally at speed. Outsourcing allows governments to rapidly adopt cutting-edge technologies like cloud computing, artificial intelligence, and advanced cybersecurity solutions, which are crucial for modernizing public services and meeting evolving citizen expectations. The focus on core competencies also plays a significant role, as agencies aim to offload non-core functions to external specialists, enabling internal resources to concentrate on their primary missions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cost Efficiency and Budgetary Constraints | +2.1% | Global, particularly Developed Economies | Short to Mid-term (2025-2030) |

| Digital Transformation Initiatives | +1.9% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Access to Specialized Expertise and Technology | +1.5% | Global | Short to Long-term (2025-2033) |

| Focus on Core Government Functions | +1.1% | Global | Mid-term (2026-2031) |

| Demand for Enhanced Citizen Services | +1.2% | Developed and Emerging Economies | Mid to Long-term (2027-2033) |

Public Sector Outsourcing Market Restraints Analysis

Despite its growth potential, the public sector outsourcing market faces several significant restraints that can impede its expansion. Foremost among these are concerns related to data security and privacy, particularly when handling sensitive citizen information. The potential for data breaches, compliance failures, or unauthorized access poses substantial risks and often leads to heightened scrutiny and reluctance to outsource certain functions.

Another prominent restraint is the inherent complexity of government procurement processes, which are often characterized by lengthy tender procedures, stringent regulatory requirements, and multiple stakeholder approvals. This can deter potential providers, especially smaller, innovative firms, and prolong the time required to initiate and implement outsourcing contracts. Public and union resistance, driven by fears of job losses, reduced service quality, or loss of governmental control, also frequently acts as a significant barrier to the widespread adoption of outsourcing initiatives, leading to political pushback and public scrutiny.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Security and Privacy Concerns | -1.8% | Global | Short to Long-term (2025-2033) |

| Complexity of Government Procurement and Regulations | -1.2% | Global, particularly Europe and North America | Short to Mid-term (2025-2030) |

| Resistance from Public Sector Employees and Unions | -0.9% | Developed Economies (e.g., France, Germany, UK) | Short-term (2025-2028) |

| Perception of Loss of Control and Accountability | -0.8% | Global | Mid-term (2026-2031) |

| Vendor Lock-in and Contractual Rigidities | -0.7% | Global | Mid to Long-term (2027-2033) |

Public Sector Outsourcing Market Opportunities Analysis

The public sector outsourcing market is rich with opportunities, particularly those stemming from rapid technological advancements and evolving government priorities. The burgeoning focus on smart city initiatives across urban centers worldwide presents a significant avenue for growth, as these projects require sophisticated integration of IT, infrastructure management, and data analytics that external providers are well-equipped to deliver. This includes areas such as intelligent transportation systems, sustainable energy management, and public safety solutions.

Furthermore, the increasing demand for advanced cybersecurity solutions to protect critical national infrastructure and sensitive citizen data offers substantial opportunities for specialized outsourcing firms. As cyber threats become more sophisticated, governments are keen to partner with experts to enhance their defensive capabilities. The adoption of cloud-based services and Robotic Process Automation (RPA) also continues to expand, enabling governments to achieve greater agility, scalability, and cost efficiencies in their operations, thereby creating new market segments for providers capable of implementing and managing these transformative technologies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Cloud Computing and SaaS Solutions | +1.8% | Global | Mid to Long-term (2027-2033) |

| Increasing Demand for Cybersecurity Services | +1.6% | Global | Short to Long-term (2025-2033) |

| Growth in Smart City and Digital Government Initiatives | +1.4% | Asia Pacific, Europe, North America | Mid to Long-term (2027-2033) |

| Adoption of AI and Robotic Process Automation (RPA) | +1.3% | Developed Economies | Mid-term (2026-2031) |

| Outsourcing for Healthcare IT and Public Health Systems | +1.0% | North America, Europe | Short to Mid-term (2025-2030) |

Public Sector Outsourcing Market Challenges Impact Analysis

The public sector outsourcing market faces several inherent challenges that demand strategic navigation from both government entities and service providers. A primary concern is ensuring consistent service quality and performance in outsourced operations, especially given the high public expectations and critical nature of government functions. Maintaining service level agreements (SLAs) and delivering measurable outcomes often proves challenging due to the dynamic nature of public needs and the intricacies of government processes.

Another significant challenge lies in effectively managing complex contracts and fostering robust vendor relationships. Public sector contracts are frequently characterized by long durations, multiple amendments, and stringent compliance requirements, necessitating sophisticated contract management capabilities. Additionally, the need to navigate diverse political and regulatory landscapes, which can vary significantly across different government levels and regions, adds another layer of complexity. Providers must be adept at adapting to evolving legal frameworks and public policy shifts, which can impact project scope and delivery.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Service Quality and Performance Adherence | -1.5% | Global | Short to Long-term (2025-2033) |

| Managing Complex Contracts and Vendor Relationships | -1.3% | Global | Short to Long-term (2025-2033) |

| Navigating Political and Regulatory Changes | -1.0% | Global, especially highly regulated regions | Short to Mid-term (2025-2030) |

| Public Perception and Trust Issues | -0.9% | Developed Economies | Short-term (2025-2028) |

| Cybersecurity Incident Response and Remediation | -0.8% | Global | Mid-term (2026-2031) |

Public Sector Outsourcing Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Public Sector Outsourcing Market, covering historical trends from 2019 to 2023, current market estimations for 2024, and detailed forecasts up to 2033. It examines market size, growth drivers, restraints, opportunities, and challenges across various service types and end-use sectors. The scope also includes a thorough regional analysis, insights into the competitive landscape, and an assessment of emerging technologies like AI and cloud computing impact on market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 550 Billion |

| Market Forecast in 2033 | USD 1011 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Accenture, IBM, Capgemini, Deloitte, DXC Technology, Tata Consultancy Services (TCS), Wipro, Infosys, CGI, HCLTech, Cognizant, Serco, Capita, G4S, Sopra Steria, Leidos, Lockheed Martin, Raytheon Technologies, Northrop Grumman, General Dynamics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The public sector outsourcing market is intricately segmented to reflect the diverse range of services demanded by various government entities. These segmentations allow for a granular understanding of market dynamics, growth pockets, and specialized service needs. Service type segmentation distinguishes between traditional IT Outsourcing, comprehensive Business Process Outsourcing, and specialized Consulting and Managed Services, each catering to distinct operational requirements and technological maturities.

End-use sector segmentation further refines this view, highlighting the unique demands of areas such as Defense, Healthcare, Education, and Public Utilities. Each sector exhibits specific regulatory frameworks, security imperatives, and citizen interaction models, thereby influencing the type and scale of outsourced solutions adopted. Understanding these segmentations is critical for market players to tailor their offerings effectively and for government agencies to identify suitable partners for their specific needs, enabling more targeted and efficient service delivery across the public domain.

- By Service Type:

- IT Outsourcing (ITO): Includes application development, infrastructure management, help desk, data center, cybersecurity, and cloud services.

- Business Process Outsourcing (BPO): Encompasses human resources, finance and accounting, customer service, procurement, and back-office operations.

- Consulting Services: Strategic advisory and implementation support for various government initiatives.

- Managed Services: Comprehensive management of specific IT or business functions on an ongoing basis.

- Facilities Management: Maintenance and operation of public infrastructure and buildings.

- By End-Use Sector:

- Defense and Military: Specialized IT and BPO services for national security agencies.

- Healthcare and Social Services: Outsourcing for patient records, billing, claims processing, and digital health platforms.

- Education: IT infrastructure, administrative support, and learning management systems for educational institutions.

- Public Utilities: Management of IT systems, customer service, and infrastructure for water, electricity, and gas providers.

- Transportation: IT solutions for traffic management, public transport systems, and logistical support.

- Justice and Law Enforcement: Data management, forensic IT, and administrative support for legal and police departments.

- General Administration: Core back-office functions for central and local government bodies.

Regional Highlights

- North America: This region holds the largest market share, driven by robust digital government initiatives, significant investments in cloud computing, and a strong emphasis on cybersecurity and data analytics. The United States and Canada lead in adopting advanced outsourcing models across federal, state, and local governments.

- Europe: Characterized by a mature outsourcing market, Europe demonstrates strong growth due to ongoing public sector modernization programs, particularly in the UK, Germany, and France. Regulatory compliance, such as GDPR, and the push for digital public services are key drivers.

- Asia Pacific (APAC): Expected to exhibit the fastest growth, propelled by rapid urbanization, smart city projects, and increasing government spending on digital infrastructure in countries like India, China, and Australia. The region is witnessing a surge in demand for cost-effective IT and BPO services.

- Latin America: The market here is emerging, with governments in Brazil, Mexico, and Argentina focusing on improving public service delivery and operational efficiency through outsourcing. Investments are growing in cloud adoption and citizen service platforms.

- Middle East and Africa (MEA): This region presents significant growth potential, particularly with large-scale government visions like Saudi Arabia's Vision 2030 and UAE's digital transformation agenda. Focus areas include infrastructure management, smart government initiatives, and cybersecurity in critical sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Public Sector Outsourcing Market.- Accenture

- IBM

- Capgemini

- Deloitte

- DXC Technology

- Tata Consultancy Services (TCS)

- Wipro

- Infosys

- CGI

- HCLTech

- Cognizant

- Serco

- Capita

- G4S

- Sopra Steria

- Leidos

- Lockheed Martin

- Raytheon Technologies

- Northrop Grumman

- General Dynamics

Frequently Asked Questions

What is public sector outsourcing?

Public sector outsourcing involves government entities contracting with external, third-party organizations to perform specific tasks, deliver services, or manage functions that would otherwise be handled in-house. This can range from IT support and infrastructure management to human resources, finance, and customer service operations.

Why do governments outsource services?

Governments outsource services primarily to achieve cost efficiencies, access specialized expertise not available internally, enhance service quality, manage increasing workloads, and focus internal resources on core strategic functions. It also aids in modernizing public services and adopting new technologies more rapidly.

What are the primary benefits of public sector outsourcing?

Key benefits include significant cost savings through economies of scale and specialized processes, improved service delivery and efficiency, access to advanced technologies and skilled personnel, increased flexibility to adapt to changing demands, and reduced operational risks by leveraging external providers' expertise.

What are the main risks associated with public sector outsourcing?

The main risks include potential data security breaches and privacy violations, loss of governmental control over critical functions, challenges in managing complex contracts and vendor relationships, public and union opposition due to job displacement concerns, and potential for vendor lock-in or service quality inconsistencies.

How is AI impacting public sector outsourcing?

AI is transforming public sector outsourcing by enabling automation of repetitive tasks, enhancing data analysis for better decision-making, improving citizen service delivery through virtual assistants, and strengthening cybersecurity defenses. It drives demand for providers with AI integration capabilities while also raising new considerations for data ethics and workforce adaptation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted