Proton Therapy Market

Proton Therapy Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703136 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

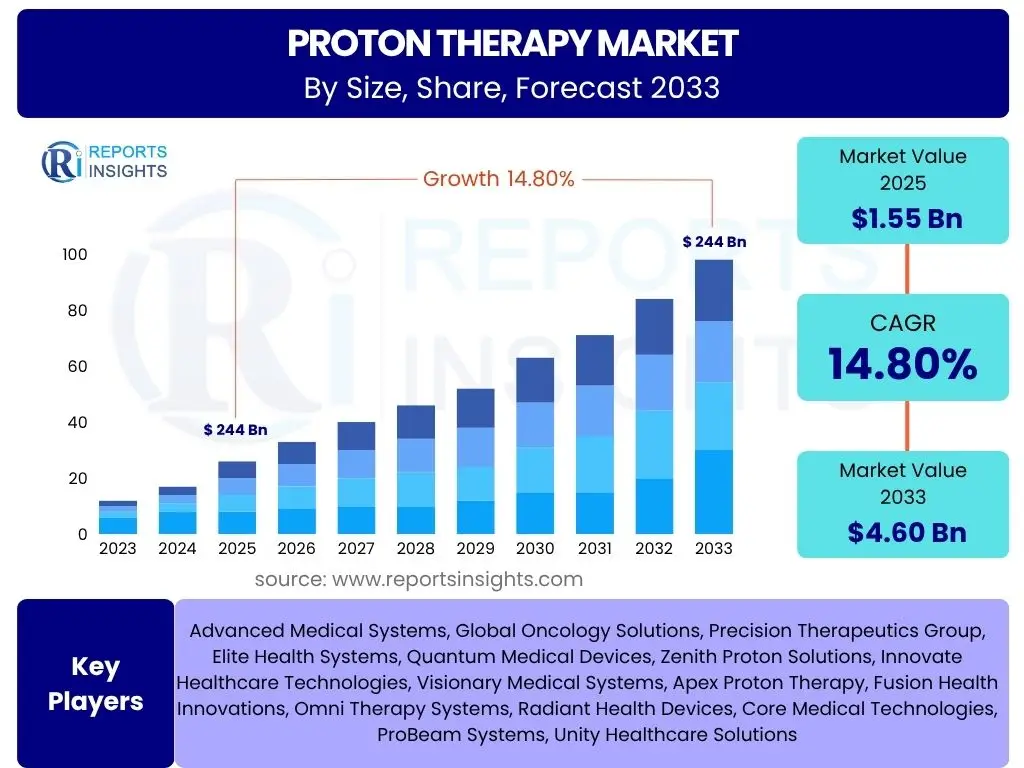

Proton Therapy Market Size

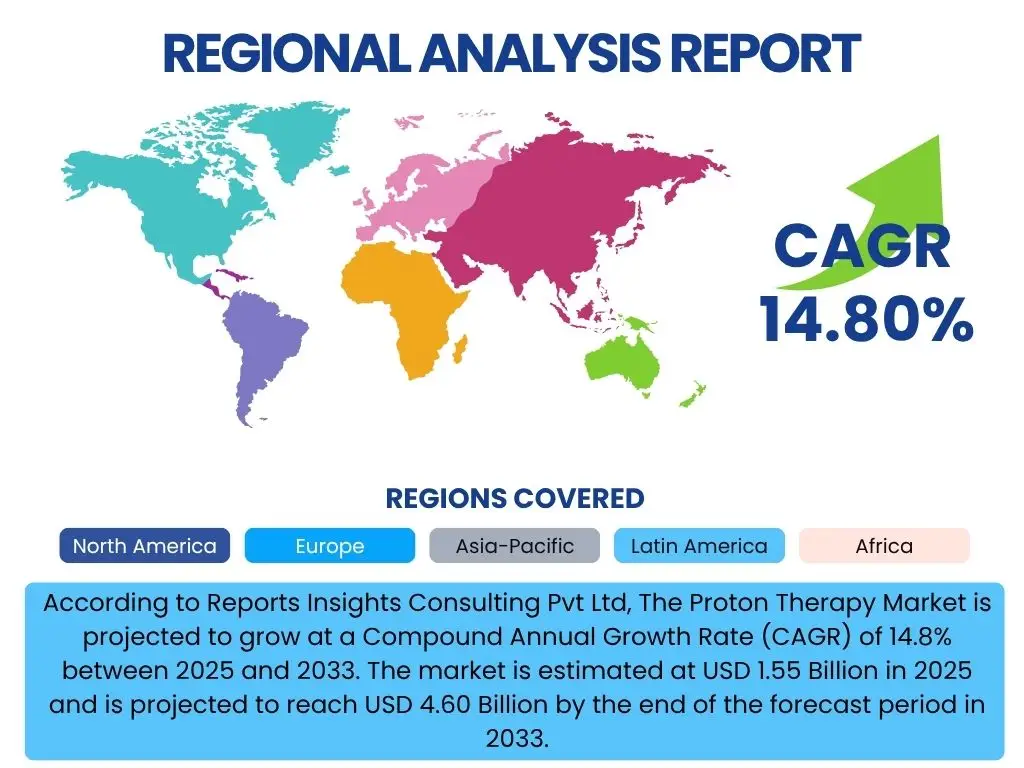

According to Reports Insights Consulting Pvt Ltd, The Proton Therapy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.8% between 2025 and 2033. The market is estimated at USD 1.55 Billion in 2025 and is projected to reach USD 4.60 Billion by the end of the forecast period in 2033.

The growth trajectory of the proton therapy market is driven by several synergistic factors, including the increasing incidence of cancer worldwide, the continuous advancements in proton therapy technology, and a growing body of clinical evidence supporting its efficacy and reduced side effects compared to traditional radiation therapy. As healthcare systems globally seek more precise and patient-friendly cancer treatment options, the adoption of proton therapy is expected to accelerate, contributing significantly to its market expansion over the forecast period.

Key Proton Therapy Market Trends & Insights

The proton therapy market is experiencing dynamic shifts, characterized by significant technological advancements and expanding clinical applications. Common user inquiries often revolve around the evolution of treatment delivery, the integration of advanced imaging, and the diversification of treatable cancer types. Key trends indicate a move towards more compact and cost-effective systems, a broader acceptance of proton therapy for various malignancies, and an increasing focus on personalized treatment plans, all contributing to enhanced patient outcomes and market growth.

Moreover, the market is witnessing an emphasis on improving the accessibility of proton therapy. This includes efforts to reduce the footprint and capital cost of new centers, facilitating their establishment in more diverse geographical locations. There is also a growing push for greater insurance coverage and reimbursement policies, which are critical for increasing patient access and driving demand. The development of advanced treatment planning software and real-time motion management systems further refines the precision of proton delivery, addressing prior limitations and expanding the utility of this advanced radiotherapy modality.

- Miniaturization of proton therapy systems, enabling more cost-effective and space-efficient installations.

- Expansion of clinical indications beyond traditional pediatric and brain cancers to include prostate, lung, and gastrointestinal cancers.

- Integration of artificial intelligence (AI) and machine learning (ML) for enhanced treatment planning, dose optimization, and patient selection.

- Development of personalized and adaptive proton therapy techniques, tailoring treatment delivery to individual patient anatomies and tumor responses.

- Increasing number of partnerships between technology developers and healthcare providers to establish new proton therapy centers globally.

- Growing emphasis on real-time imaging and motion management technologies to improve treatment precision and reduce side effects.

AI Impact Analysis on Proton Therapy

Users frequently inquire about the transformative potential of artificial intelligence in proton therapy, particularly regarding its ability to enhance precision, efficiency, and accessibility. The consensus indicates high expectations for AI to revolutionize various aspects, from initial diagnosis and patient selection to treatment planning, real-time monitoring, and adaptive therapy. Concerns often center on data privacy, the need for robust validation, and the potential for job displacement, though the overarching sentiment is positive regarding AI's capacity to optimize treatment outcomes and streamline clinical workflows.

AI's influence is anticipated to extend beyond mere operational improvements, potentially unlocking new frontiers in research and development. By analyzing vast datasets of patient outcomes and treatment parameters, AI algorithms can identify optimal treatment strategies, predict patient responses, and even personalize dose delivery with unprecedented accuracy. This analytical capability is expected to accelerate the development of more effective and safer proton therapy protocols, making it a cornerstone for future advancements in radiation oncology.

- Enhancement of treatment planning accuracy and speed through AI-driven contouring and dose optimization algorithms.

- Development of predictive analytics for patient response to proton therapy, aiding in personalized treatment selection.

- Real-time adaptive therapy enabled by AI, allowing for dynamic adjustments to treatment delivery based on tumor motion and anatomical changes.

- Automation of quality assurance processes, improving safety and reducing human error in proton therapy delivery.

- Accelerated discovery of novel treatment protocols and optimization of existing ones through AI-powered data analysis.

Key Takeaways Proton Therapy Market Size & Forecast

Common user questions regarding the proton therapy market size and forecast typically center on understanding the core drivers of growth, the segments offering the most promising opportunities, and the overall trajectory of market expansion. Key insights reveal that the market is poised for substantial growth, driven by increasing cancer incidence, technological innovation leading to more accessible systems, and a rising preference for precise, less invasive treatment modalities. The forecast indicates sustained momentum, with significant investments expected in infrastructure and research.

Furthermore, the market's future outlook is strongly tied to evolving reimbursement policies and the global expansion of proton therapy centers, particularly in emerging economies. The growing body of clinical evidence supporting proton therapy's benefits in various cancer types, including pediatric, prostate, and lung cancers, is a critical factor influencing its adoption. Strategic collaborations and competitive landscape dynamics also play a pivotal role, shaping the market's direction and highlighting opportunities for innovation and market penetration.

- The proton therapy market is set for robust double-digit CAGR growth through 2033, driven by expanding clinical applications and technological advancements.

- Increasing global cancer burden is a primary catalyst for market expansion, pushing demand for advanced radiation therapies.

- Technological innovations focusing on smaller, more affordable, and precise systems are critical for broader adoption and market penetration.

- Reimbursement policies and insurance coverage improvements are crucial determinants for patient accessibility and market growth.

- North America and Europe currently dominate the market, but Asia Pacific is emerging as a high-growth region due to increasing healthcare investments and awareness.

Proton Therapy Market Drivers Analysis

The increasing global incidence of various cancer types serves as a fundamental driver for the proton therapy market. As cancer rates rise, so does the demand for effective and advanced treatment modalities that offer superior outcomes and reduced side effects. Proton therapy, with its precise dose delivery, minimizes damage to healthy tissues, making it an attractive option for patients and clinicians, especially for tumors located near critical organs or in pediatric cases.

Technological advancements in proton therapy systems, including the development of compact systems, improved treatment planning software, and enhanced imaging capabilities, significantly contribute to market growth. These innovations make proton therapy more accessible, efficient, and safer, broadening its applicability and encouraging more healthcare facilities to invest in this technology. Additionally, a growing body of clinical evidence supporting the efficacy and benefits of proton therapy over traditional photon radiation further solidifies its position as a preferred treatment option, leading to increased adoption rates globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Cancer Incidence | +4.5% | Global, particularly high-income and rapidly developing nations | Long-term (2025-2033) |

| Technological Advancements in Proton Therapy Systems | +3.8% | North America, Europe, East Asia | Medium-term (2025-2029) |

| Growing Clinical Evidence and Research Supporting Efficacy | +3.2% | Global, especially academic and research institutions | Long-term (2025-2033) |

| Rising Demand for Non-Invasive Cancer Treatments with Reduced Side Effects | +2.7% | Global, driven by patient preference and quality of life focus | Long-term (2025-2033) |

Proton Therapy Market Restraints Analysis

The high capital cost associated with establishing and maintaining a proton therapy center represents a significant restraint on market growth. Building a single center can cost hundreds of millions of dollars, making it a substantial investment that only large hospital networks or research institutions can typically afford. This high entry barrier limits the proliferation of centers, especially in regions with constrained healthcare budgets, thus impacting accessibility and slowing market expansion.

Furthermore, the complex infrastructure requirements and the need for highly specialized personnel to operate proton therapy systems contribute to operational expenses and logistical challenges. These factors, combined with limited reimbursement policies in some regions, can make proton therapy less accessible to a wider patient population. The current limitations in the number of operational proton therapy centers globally also mean that many patients who could benefit from this treatment do not have easy access to it, thereby restraining market growth despite its clinical advantages.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Operational Costs | -3.5% | Global, particularly emerging economies | Long-term (2025-2033) |

| Limited Availability of Reimbursement Policies in Some Regions | -2.8% | Asia Pacific, Latin America, Middle East & Africa | Medium-term (2025-2029) |

| Requirement for Highly Specialized Infrastructure and Personnel | -2.0% | Global, affecting smaller healthcare providers | Long-term (2025-2033) |

| Perception of Proton Therapy as a Niche or Experimental Treatment | -1.5% | Specific regions with lower awareness/acceptance | Short-term (2025-2027) |

Proton Therapy Market Opportunities Analysis

The expanding clinical applications of proton therapy present a significant opportunity for market growth. Initially used primarily for pediatric cancers and tumors near sensitive organs, advancements in technology and increasing clinical evidence are allowing proton therapy to be effectively applied to a broader range of malignancies, including prostate, lung, liver, and head and neck cancers. This diversification of treatable conditions opens up new patient populations and revenue streams for existing and future proton therapy centers.

Furthermore, the development of compact and more affordable single-room proton therapy systems offers a crucial opportunity to increase market penetration by making the technology accessible to a wider range of hospitals and healthcare networks. These smaller systems reduce the immense capital investment and space requirements, thereby lowering the barrier to entry and enabling the establishment of proton therapy facilities in more diverse geographical locations, including developing regions. This improved accessibility is expected to drive significant growth and democratize access to this advanced treatment modality.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expanding Clinical Applications for Various Cancer Types | +4.0% | Global, particularly North America, Europe, and Asia Pacific | Long-term (2025-2033) |

| Development of Compact and More Affordable Proton Therapy Systems | +3.5% | Global, enabling market expansion into new regions | Medium-term (2026-2030) |

| Growth in Medical Tourism for Advanced Cancer Treatments | +2.8% | Asia Pacific, Middle East, Europe | Medium-term (2025-2029) |

| Increasing Investments in Healthcare Infrastructure in Emerging Economies | +2.2% | China, India, Brazil, Southeast Asia | Long-term (2025-2033) |

Proton Therapy Market Challenges Impact Analysis

One of the primary challenges facing the proton therapy market is the significant cost-effectiveness debate compared to conventional radiation therapy. While proton therapy offers superior precision and reduced side effects, its higher upfront capital costs and ongoing operational expenses often lead to scrutiny regarding its economic viability, especially when clinical outcomes for certain cancer types may not significantly outweigh those of advanced photon therapies. This debate can hinder widespread adoption and limit reimbursement in cost-conscious healthcare systems.

Another critical challenge is the limited number of trained medical professionals, including radiation oncologists, medical physicists, and dosimetrists, who are proficient in proton therapy. The specialized nature of the technology requires extensive training and experience, leading to a shortage of qualified personnel. This talent gap can impede the establishment and efficient operation of new proton therapy centers, thereby constraining market expansion and the ability to meet growing patient demand. Overcoming this requires significant investment in specialized education and training programs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost-Effectiveness Concerns vs. Conventional Therapies | -2.5% | Global, particularly cost-sensitive markets | Long-term (2025-2033) |

| Shortage of Trained and Qualified Medical Personnel | -2.0% | Global, affecting new center establishment | Medium-term (2025-2029) |

| Complex Regulatory Approval Processes for New Systems | -1.8% | North America, Europe | Short-term (2025-2027) |

| Competitive Pressure from Advanced Photon Radiation Technologies | -1.2% | Global, offering alternative precision treatments | Long-term (2025-2033) |

Proton Therapy Market - Updated Report Scope

This report provides a comprehensive analysis of the global Proton Therapy Market, offering an in-depth understanding of its current state, key trends, and future growth prospects. It encompasses a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and major geographical regions. The scope also includes an assessment of the competitive landscape, highlighting the strategies of key players and emerging trends that are shaping the industry. The objective is to equip stakeholders with actionable insights for strategic decision-making and investment planning within the proton therapy sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.55 Billion |

| Market Forecast in 2033 | USD 4.60 Billion |

| Growth Rate | 14.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Medical Systems, Global Oncology Solutions, Precision Therapeutics Group, Elite Health Systems, Quantum Medical Devices, Zenith Proton Solutions, Innovate Healthcare Technologies, Visionary Medical Systems, Apex Proton Therapy, Fusion Health Innovations, Omni Therapy Systems, Radiant Health Devices, Core Medical Technologies, ProBeam Systems, Unity Healthcare Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The proton therapy market is meticulously segmented to provide a granular view of its diverse components and their respective contributions to overall market growth. These segments are primarily defined by the type of system, the specific medical application, and the end-user facilities, reflecting the varied landscape of proton therapy adoption. This detailed segmentation allows for a precise understanding of market dynamics, growth opportunities within niche areas, and the identification of high-potential sectors. Each segment and sub-segment exhibits unique growth drivers and market potential, influenced by technological advancements, patient demographics, and healthcare infrastructure development.

Understanding these segments is crucial for stakeholders to identify optimal investment areas, develop targeted marketing strategies, and align product development with evolving market needs. For instance, the demand for single-room systems is rising due to their lower installation costs and smaller footprint, making proton therapy more accessible to a broader range of healthcare providers. Similarly, the expanding list of oncology applications, especially for prevalent cancers like prostate and lung cancer, significantly influences segment growth. The end-user analysis further differentiates demand patterns between large hospital networks, specialized cancer clinics, and research institutions, each with distinct procurement priorities and usage patterns.

- By Type:

- Single-Room Systems: These compact systems require less space and capital investment, making them increasingly popular for broader adoption.

- Multi-Room Systems: Larger facilities offering treatment to a higher volume of patients, often associated with major academic and research centers.

- By Application:

- Oncology:

- Prostate Cancer: A significant application due to the ability to spare surrounding healthy tissue.

- Lung Cancer: Benefits from precise targeting to reduce radiation to heart and lungs.

- Brain & Spine Cancer: Critical for protecting sensitive neural structures.

- Pediatric Cancer: Preferred due to reduced long-term side effects in growing children.

- Head & Neck Cancer: Ideal for preserving salivary glands and other critical structures.

- Others: Includes liver, breast, and gastrointestinal cancers, with expanding clinical evidence.

- Non-Oncology: Emerging applications such as arteriovenous malformations (AVMs) and other non-malignant conditions.

- Oncology:

- By End-User:

- Hospitals: The primary end-users, integrating proton therapy into comprehensive cancer care programs.

- Specialty Cancer Clinics: Dedicated centers focused on advanced cancer treatments.

- Academic & Research Institutions: Key players in clinical trials, research, and training of future specialists.

Regional Highlights

The global proton therapy market exhibits distinct regional dynamics driven by varying healthcare infrastructures, cancer incidence rates, reimbursement policies, and technological adoption rates. North America currently leads the market, primarily due to high healthcare expenditure, a significant number of established proton therapy centers, and robust research and development activities. The region benefits from strong governmental support for cancer research and advanced treatment modalities, alongside a high level of patient awareness and accessibility to innovative therapies.

Europe closely follows North America, characterized by a growing number of operational proton therapy facilities and increasing adoption rates driven by supportive government initiatives and a strong emphasis on precision medicine. Countries like Germany, the UK, and France are witnessing significant investments in proton therapy. The Asia Pacific region is anticipated to demonstrate the highest growth rate during the forecast period, propelled by rising cancer prevalence, improving healthcare infrastructure, increasing healthcare spending, and a growing medical tourism sector. Countries such as China, Japan, and South Korea are actively investing in new proton therapy centers and technology, aiming to meet the escalating demand for advanced cancer treatments.

Latin America and the Middle East & Africa regions are also projected to experience steady growth, albeit from a smaller base. Factors contributing to growth in these regions include increasing awareness about advanced cancer treatments, improvements in healthcare access, and the gradual establishment of specialized cancer care facilities. However, these regions often face challenges related to high capital costs and the need for greater investment in specialized medical training and infrastructure to fully capitalize on the potential of proton therapy.

- North America: Dominant market share due to advanced healthcare infrastructure, high incidence of cancer, significant R&D investments, and favorable reimbursement landscape. The United States accounts for the majority of proton therapy centers globally.

- Europe: Second largest market, driven by increasing awareness, governmental support for precision oncology, and the establishment of new centers in countries like Germany, the UK, and France.

- Asia Pacific (APAC): Fastest growing region, fueled by rising cancer prevalence, improving healthcare expenditure, increasing disposable incomes, and the emergence of medical tourism hubs in countries such as China, Japan, South Korea, and India.

- Latin America: Emerging market with nascent growth, characterized by increasing investments in healthcare infrastructure and rising awareness of advanced cancer treatments, particularly in Brazil and Mexico.

- Middle East & Africa (MEA): Gradual adoption, with growth spurred by increasing healthcare investments, particularly in Gulf Cooperation Council (GCC) countries, and a focus on improving cancer care capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Proton Therapy Market.- Advanced Medical Systems

- Global Oncology Solutions

- Precision Therapeutics Group

- Elite Health Systems

- Quantum Medical Devices

- Zenith Proton Solutions

- Innovate Healthcare Technologies

- Visionary Medical Systems

- Apex Proton Therapy

- Fusion Health Innovations

- Omni Therapy Systems

- Radiant Health Devices

- Core Medical Technologies

- ProBeam Systems

- Unity Healthcare Solutions

- ProCure Cancer Treatment Centers

- Optima Healthcare Innovations

- Synergy Medical Technologies

- Integral Radiation Systems

- Pinnacle Oncology Solutions

Frequently Asked Questions

What is proton therapy?

Proton therapy is an advanced form of radiation therapy that uses high-energy proton beams to treat cancer. Unlike traditional X-rays, protons can be precisely controlled to deposit their energy directly into a tumor, minimizing radiation exposure to surrounding healthy tissues and organs.

How is proton therapy different from conventional radiation therapy?

The primary difference lies in the way radiation is delivered. Conventional radiation uses photons (X-rays) which release energy along their path and beyond the tumor. Protons, however, exhibit a unique property called the "Bragg Peak," allowing them to release most of their energy at a specific, controlled depth within the tumor, then stopping, thus sparing healthy tissue beyond the target.

What are the key benefits of proton therapy?

Key benefits include reduced side effects, higher precision in targeting tumors, decreased radiation exposure to healthy tissues and critical organs, and a lower risk of secondary cancers. These advantages are particularly significant for pediatric patients and individuals with tumors located near vital structures.

What factors are driving the growth of the proton therapy market?

The market is primarily driven by the increasing global incidence of cancer, continuous technological advancements leading to more compact and efficient systems, growing clinical evidence supporting its efficacy, and rising patient and physician awareness of its benefits compared to conventional therapies.

What are the main challenges facing the proton therapy market?

Major challenges include the high capital and operational costs associated with establishing and maintaining proton therapy centers, the limited availability of trained medical professionals, complex regulatory approval processes, and ongoing debates regarding its cost-effectiveness relative to other advanced radiation techniques.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted