Prostate Cancer Treatment Drug Market

Prostate Cancer Treatment Drug Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707851 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Prostate Cancer Treatment Drug Market Size

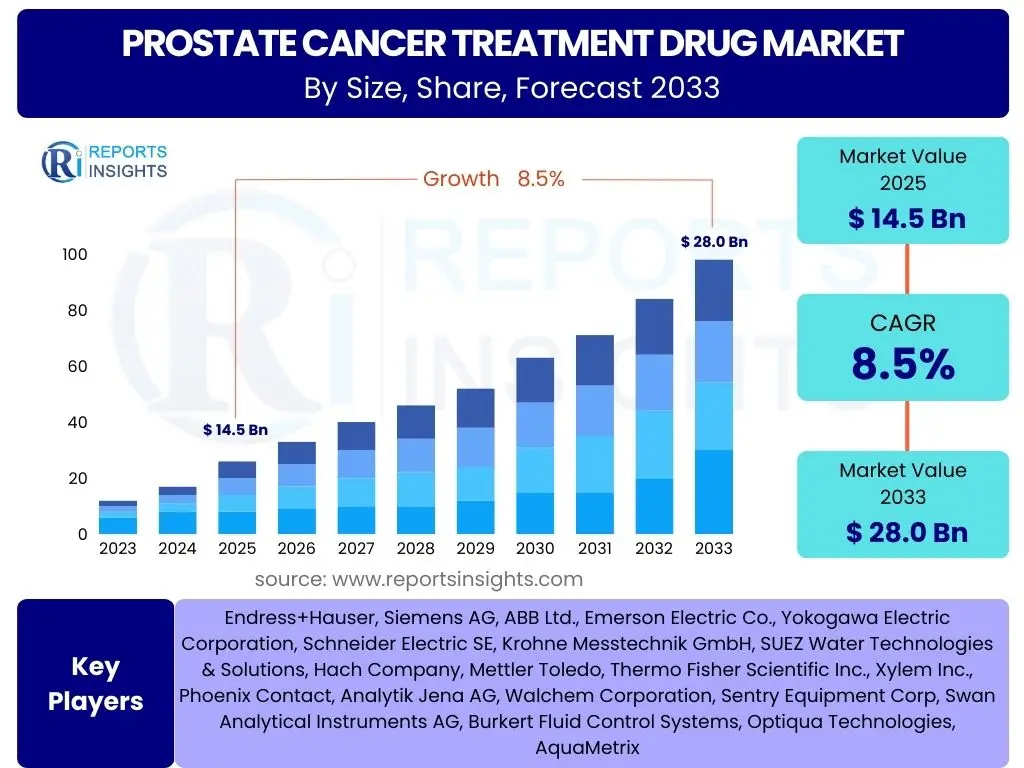

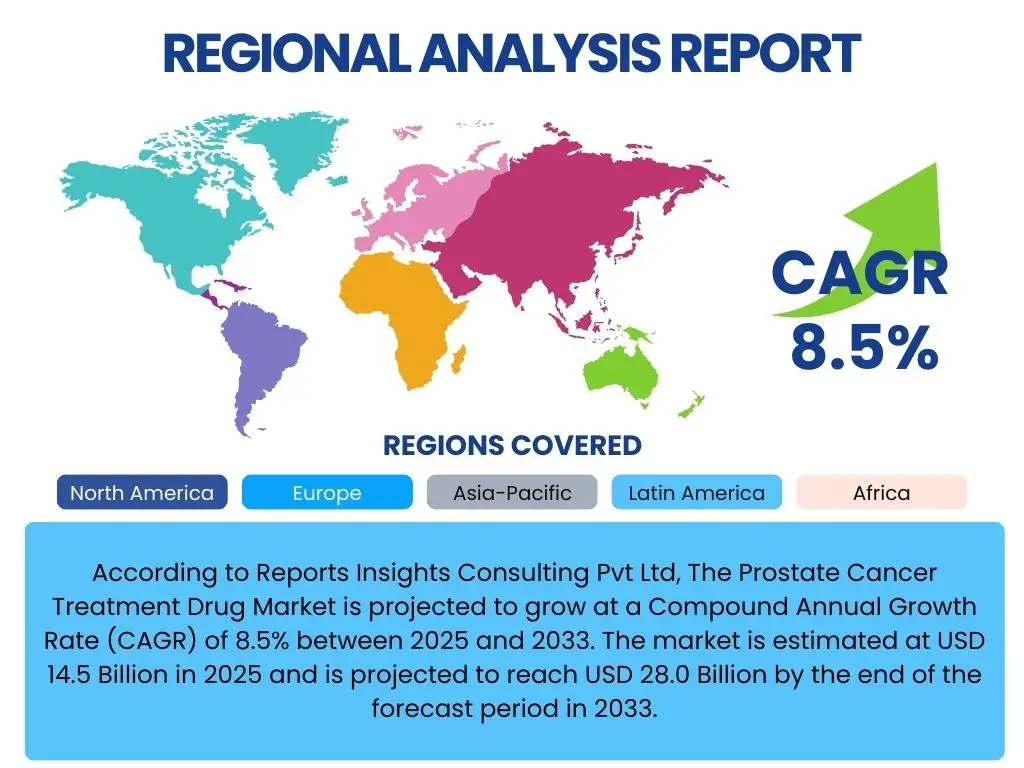

According to Reports Insights Consulting Pvt Ltd, The Prostate Cancer Treatment Drug Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 14.5 Billion in 2025 and is projected to reach USD 28.0 Billion by the end of the forecast period in 2033.

Key Prostate Cancer Treatment Drug Market Trends & Insights

The prostate cancer treatment drug market is experiencing dynamic shifts driven by advancements in precision medicine and a deeper understanding of disease biology. Key inquiries often center on how therapeutic approaches are evolving, particularly with the rise of targeted therapies and immunotherapies that offer more effective and less toxic options compared to traditional treatments. Furthermore, the integration of advanced diagnostics for early detection and personalized treatment selection is a significant trend, allowing for tailored interventions that improve patient outcomes. The market is also witnessing a greater emphasis on improving quality of life for patients, leading to the development of drugs with fewer side effects and more convenient administration routes, reflecting a patient-centric approach to care.

Another prominent area of interest concerns the impact of an aging global population and increasing prostate cancer incidence rates on market demand. This demographic shift inherently drives the need for a broader array of treatment options, including those suitable for elderly patients with co-morbidities. Furthermore, the expansion of research and development into novel drug targets, such as those involved in androgen receptor signaling or DNA repair pathways, is continually reshaping the competitive landscape and offering new avenues for therapeutic innovation. The market's trajectory is also influenced by evolving regulatory landscapes and healthcare reimbursement policies, which dictate access and adoption of these advanced treatments across different regions.

- Increased adoption of precision medicine and targeted therapies.

- Growth in immunotherapy applications for advanced prostate cancer.

- Focus on developing novel oral treatments and less invasive therapies.

- Integration of advanced diagnostics for personalized treatment selection.

- Expansion of drug development into novel mechanisms of action, including PARP inhibitors.

- Rising demand for therapies addressing drug resistance in castration-resistant prostate cancer.

- Enhanced focus on improving patient quality of life through reduced side effects.

AI Impact Analysis on Prostate Cancer Treatment Drug

User inquiries frequently highlight the transformative potential of Artificial intelligence (AI) across the entire drug development and patient care continuum for prostate cancer. There is considerable expectation regarding AI's ability to accelerate drug discovery by identifying novel drug targets and predicting compound efficacy with greater precision, thereby reducing research timelines and costs. Concerns often revolve around the validation of AI algorithms and ensuring data privacy, given the sensitive nature of patient health information. However, the overarching sentiment suggests that AI will revolutionize therapeutic strategies, moving towards highly personalized medicine by analyzing vast datasets to predict individual patient responses to specific treatments and optimize dosing regimens.

Beyond drug discovery, AI is anticipated to significantly impact clinical trial design and execution, enabling more efficient patient recruitment and real-time monitoring of trial outcomes, which can expedite regulatory approval processes. Furthermore, its application in diagnostic imaging and pathology for earlier and more accurate prostate cancer detection is a key area of focus, potentially improving prognoses through timely intervention. Users are keenly interested in how AI can help overcome challenges such as drug resistance by modeling complex biological interactions to identify new therapeutic combinations or alternative treatment pathways. The role of AI in post-market surveillance for drug safety and efficacy also garners attention, promising a more robust and responsive healthcare ecosystem.

- Accelerated drug discovery and target identification.

- Enhanced precision in diagnostic imaging and pathological analysis for early detection.

- Optimization of clinical trial design and patient stratification.

- Development of AI-driven predictive biomarkers for treatment response.

- Personalized treatment planning and dosage optimization.

- Identification of novel therapeutic combinations to overcome drug resistance.

- Improved patient monitoring and post-treatment surveillance for adverse events.

Key Takeaways Prostate Cancer Treatment Drug Market Size & Forecast

Common user questions regarding market takeaways often center on the significant growth trajectory and the underlying factors driving this expansion. The market is poised for robust expansion, primarily fueled by the increasing global incidence of prostate cancer, particularly in an aging population, and continuous advancements in therapeutic innovation. A key takeaway is the shift towards more targeted and personalized treatment modalities, which are not only improving efficacy but also reducing the burden of side effects for patients. This evolution in treatment paradigms, coupled with a strong pipeline of novel drugs, indicates a resilient and evolving market environment.

Another crucial insight is the growing emphasis on combination therapies and the integration of diverse treatment approaches, including hormonal therapies, chemotherapy, immunotherapies, and radiopharmaceuticals, to address various stages and manifestations of the disease. The market is also characterized by strategic collaborations between pharmaceutical companies, research institutions, and technology providers, aiming to leverage synergistic expertise for accelerated drug development and market penetration. Furthermore, the economic impact of these advanced treatments, balancing their high development costs with improved patient outcomes and quality of life, remains a central theme, highlighting the need for value-based healthcare models and accessible treatment options across different socioeconomic strata.

- Significant market growth projected, driven by increasing disease prevalence and an aging population.

- Strong innovation pipeline with a focus on targeted and immunotherapies.

- Increasing adoption of personalized medicine approaches.

- Rising demand for treatments addressing advanced and castration-resistant prostate cancer.

- Strategic collaborations and R&D investments are critical for market expansion.

- Geographic market expansion, particularly in emerging economies.

- Emphasis on improving patient quality of life and long-term survival.

Prostate Cancer Treatment Drug Market Drivers Analysis

The prostate cancer treatment drug market is significantly propelled by several robust drivers that collectively contribute to its expanding valuation and therapeutic advancements. A primary driver is the rising global incidence of prostate cancer, which is intrinsically linked to an aging global population. As life expectancy increases, the demographic cohort most susceptible to prostate cancer grows, thereby escalating the demand for effective diagnostic and therapeutic interventions. This demographic shift places continuous pressure on healthcare systems and pharmaceutical companies to innovate and provide a broader spectrum of treatment options tailored to varying disease stages and patient profiles. The inherent need to address this growing patient pool directly translates into sustained market growth for prostate cancer treatment drugs.

Another powerful catalyst for market expansion is the continuous innovation in drug development, characterized by significant investments in research and development (R&D) by pharmaceutical companies. These efforts lead to the discovery and approval of novel therapies, including advanced hormonal therapies, immunotherapies, targeted agents like PARP inhibitors, and radiopharmaceuticals. These newer treatments often offer improved efficacy, better safety profiles, and enhanced quality of life compared to conventional options, thereby driving their rapid adoption. Furthermore, increasing public awareness campaigns and improved diagnostic screening methods contribute to earlier detection of prostate cancer, which, while beneficial for patient outcomes, also broadens the patient base entering the treatment pipeline, further stimulating market demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Incidence of Prostate Cancer | +2.5% | Global, particularly North America & Europe | 2025-2033 |

| Aging Global Population | +2.0% | Global, particularly developed economies | 2025-2033 |

| Advancements in Therapeutic Modalities | +1.8% | North America, Europe, Asia Pacific (innovative centers) | 2025-2033 |

| Rising Awareness & Early Diagnosis | +1.2% | Developed and rapidly developing countries | 2025-2030 |

| Increased R&D Investment | +1.0% | North America, Europe, select Asian countries | 2025-2033 |

Prostate Cancer Treatment Drug Market Restraints Analysis

Despite the robust growth drivers, the prostate cancer treatment drug market faces several significant restraints that could impede its full potential. A primary limiting factor is the high cost associated with novel and advanced therapies. Many of the recently approved targeted therapies, immunotherapies, and radiopharmaceuticals come with premium price tags, making them less accessible in developing regions or for patients with inadequate insurance coverage. This financial burden often leads to delays in treatment initiation or the adoption of less effective, older therapies, thereby restricting market expansion. Healthcare systems globally are under increasing pressure to manage pharmaceutical expenditures, and the cost-effectiveness of these new drugs is a constant point of contention, leading to stringent reimbursement policies in many markets.

Another substantial restraint is the prevalence of side effects and adverse reactions associated with various prostate cancer treatments. While newer drugs aim for improved safety profiles, many still pose significant challenges to patient quality of life, ranging from hormonal imbalances and fatigue to more severe cardiovascular or metabolic issues. These side effects can lead to treatment discontinuation or non-compliance, undermining therapeutic efficacy and impacting patient outcomes. Furthermore, the expiration of patents for blockbuster drugs introduces generic and biosimilar competition, leading to price erosion and reduced revenue for innovative drug manufacturers. This competitive pressure, combined with increasingly stringent regulatory approval processes that demand extensive clinical data, can prolong time-to-market and elevate development costs, acting as a decelerating force on market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Therapies | -1.5% | Global, particularly developing and emerging markets | 2025-2033 |

| Side Effects and Adverse Drug Reactions | -1.0% | Global | 2025-2033 |

| Patent Expirations and Generic Competition | -0.8% | North America, Europe | 2025-2030 |

| Stringent Regulatory Approval Processes | -0.7% | North America, Europe | 2025-2033 |

| Limited Treatment Options for Advanced Stages | -0.5% | Global | 2025-2030 |

Prostate Cancer Treatment Drug Market Opportunities Analysis

The prostate cancer treatment drug market is replete with significant opportunities for growth and innovation, driven by evolving scientific understanding and unmet patient needs. A key opportunity lies in the development of novel drug targets and therapeutic mechanisms that address resistance to current treatments, particularly in metastatic castration-resistant prostate cancer (mCRPC). Research into epigenetic modifiers, gene therapies, and more refined immunotherapeutic approaches presents substantial avenues for creating breakthrough therapies. Companies investing in these cutting-edge areas can carve out lucrative niches and gain a competitive edge by offering solutions where existing treatments fall short, thereby catering to a patient population with limited options and high medical urgency.

Another major opportunity exists in the expansion into emerging markets, such as those in Asia Pacific, Latin America, and the Middle East and Africa. These regions are experiencing a rapid increase in healthcare expenditure, improving medical infrastructure, and a growing incidence of prostate cancer due to adopting Western lifestyles and an aging demographic. Local governments are often keen to improve healthcare access, creating a fertile ground for pharmaceutical companies willing to navigate regional regulatory complexities and adapt pricing strategies. Furthermore, the integration of companion diagnostics with therapeutic agents offers an opportunity to enhance treatment efficacy through personalized medicine, ensuring that drugs are administered to patients most likely to respond, thereby improving outcomes and market value. This precision approach also supports better resource allocation within healthcare systems and reduces unnecessary treatment cycles.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Drug Targets | +1.8% | Global, particularly R&D hubs | 2025-2033 |

| Expansion in Emerging Markets | +1.5% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Combination Therapies & Adjunctive Treatments | +1.2% | Global | 2025-2033 |

| Personalized Medicine & Companion Diagnostics | +1.0% | North America, Europe, select Asian countries | 2025-2033 |

| Enhanced Early Detection & Screening Programs | +0.8% | Developed and rapidly developing countries | 2025-2030 |

Prostate Cancer Treatment Drug Market Challenges Impact Analysis

The prostate cancer treatment drug market faces several complex challenges that require innovative solutions and strategic adaptation from pharmaceutical companies. One significant challenge is the inherent heterogeneity of prostate cancer itself, which makes developing universally effective treatments difficult. The disease can present with diverse molecular profiles and varying aggressiveness, leading to different responses to the same drug across patient populations. This complexity necessitates highly specialized research and development, often leading to therapies with narrow indications, which can limit their market reach and profitability. Furthermore, drug resistance, especially in advanced stages like metastatic castration-resistant prostate cancer, remains a formidable barrier, as cancer cells often evolve mechanisms to circumvent therapeutic effects, leading to disease progression and treatment failure.

Another substantial challenge stems from the competitive landscape, where multiple pharmaceutical companies are vying for market share with similar drug classes or mechanisms of action. This intense competition can lead to pricing pressures and the need for continuous differentiation, requiring substantial investments in clinical trials to demonstrate superior efficacy or safety. Moreover, the long development cycles and high failure rates associated with oncology drug development pose significant financial risks. Ethical considerations surrounding clinical trial participation, particularly for vulnerable patient populations, and the need to balance therapeutic benefit with potential side effects, add layers of complexity to market navigation. Regulatory hurdles, including stringent efficacy and safety requirements from agencies like the FDA and EMA, further prolong market entry and increase R&D expenditures, making it difficult for smaller biopharmaceutical firms to compete effectively without strategic partnerships.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Drug Resistance and Disease Heterogeneity | -1.3% | Global | 2025-2033 |

| High R&D Costs and Long Development Timelines | -1.0% | Global, particularly R&D intensive regions | 2025-2033 |

| Intense Competition and Market Saturation | -0.9% | North America, Europe | 2025-2030 |

| Side Effect Management and Patient Compliance | -0.7% | Global | 2025-2033 |

| Regulatory Hurdles and Reimbursement Policies | -0.6% | Developed markets (North America, Europe) | 2025-2033 |

Prostate Cancer Treatment Drug Market - Updated Report Scope

This report provides a comprehensive analysis of the Prostate Cancer Treatment Drug Market, offering insights into its current landscape, future projections, and the various factors influencing its trajectory. It delves into the market's size, growth drivers, restraints, opportunities, and challenges, providing a detailed understanding for stakeholders. The scope encompasses a thorough examination of key market segments, regional dynamics, and the competitive environment, including profiles of leading market participants. The aim is to equip readers with strategic information to make informed decisions within this critical healthcare sector, focusing on the latest advancements and evolving patient needs.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 28.0 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AstraZeneca, Pfizer, Johnson & Johnson, Bayer AG, Novartis AG, Sanofi, Bristol Myers Squibb, Merck & Co., Inc., Astellas Pharma Inc., Ipsen Biopharmaceuticals, Amgen Inc., Dendreon Pharmaceuticals LLC, Exelixis, Inc., Genentech (Roche), Clovis Oncology, Eli Lilly and Company, Seagen Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The prostate cancer treatment drug market is intricately segmented to provide a granular view of its diverse components, reflecting the complexity of the disease and the variety of therapeutic approaches available. This segmentation allows for a precise analysis of market dynamics across different drug classes, therapy types, distribution channels, and stages of cancer. Understanding these distinct segments is crucial for stakeholders to identify specific growth areas, assess competitive landscapes, and tailor their strategic initiatives to meet the nuanced demands of the market. The classification of drugs based on their mechanism of action or chemical structure, for instance, highlights the prevalence and evolving preferences for particular therapeutic modalities, such as the increasing adoption of targeted agents or immunotherapies over conventional chemotherapy in certain patient populations.

Further segmentation by therapy type, distinguishing between monotherapy and combination therapy, underscores the shift towards integrated treatment regimens designed to enhance efficacy and overcome drug resistance, particularly in advanced or refractory cases. The channels through which these drugs are distributed also form a critical segment, impacting accessibility and market reach. Finally, categorizing treatments by cancer stage—from localized prostate cancer to metastatic castration-resistant prostate cancer (mCRPC)—is perhaps the most vital, as it directly correlates with the specific drugs approved and prescribed for varying disease progression. This comprehensive segmentation framework ensures that all facets of the market are thoroughly examined, providing a robust foundation for strategic planning and investment decisions within the prostate cancer therapeutic landscape.

- By Drug Class:

- Hormonal Therapy (Androgen Deprivation Therapy, Antiandrogens, GnRH Agonists, GnRH Antagonists)

- Chemotherapy

- Immunotherapy

- Targeted Therapy (PARP Inhibitors, Kinase Inhibitors)

- Radiopharmaceuticals

- Others (e.g., Bisphosphonates)

- By Therapy Type:

- Monotherapy

- Combination Therapy

- By Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Cancer Stage:

- Localized Prostate Cancer

- Advanced Prostate Cancer (Metastatic Castration-Sensitive Prostate Cancer - mCSPC, Metastatic Castration-Resistant Prostate Cancer - mCRPC)

Regional Highlights

- North America: This region consistently holds the largest share of the prostate cancer treatment drug market, driven by high disease prevalence, advanced healthcare infrastructure, significant R&D investments, and rapid adoption of innovative therapies. The presence of major pharmaceutical companies and favorable reimbursement policies further bolsters market growth.

- Europe: Europe represents a substantial market share, characterized by an aging population, increasing cancer incidence, and robust healthcare spending. Countries like Germany, France, and the UK are key contributors, with strong regulatory frameworks and a focus on personalized medicine and advanced therapeutic options.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate during the forecast period. This accelerated growth is attributed to improving healthcare access, increasing awareness about prostate cancer, a large and growing geriatric population, and rising disposable incomes that enable greater access to advanced treatments. China, Japan, and India are emerging as major markets.

- Latin America: This region shows steady growth, driven by increasing healthcare expenditure, improving diagnostic capabilities, and a rising awareness of prostate cancer. Market expansion is supported by government initiatives to enhance public health and a growing demand for cost-effective generic and biosimilar options, alongside branded drugs.

- Middle East and Africa (MEA): While currently a smaller market, MEA is anticipated to experience moderate growth, primarily due to improving healthcare infrastructure, increasing investment in healthcare, and a rising prevalence of non-communicable diseases, including cancer. The adoption of advanced treatments is gradually increasing, albeit with challenges related to affordability and access.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Prostate Cancer Treatment Drug Market.- AstraZeneca

- Pfizer

- Johnson & Johnson

- Bayer AG

- Novartis AG

- Sanofi

- Bristol Myers Squibb

- Merck & Co., Inc.

- Astellas Pharma Inc.

- Ipsen Biopharmaceuticals

- Amgen Inc.

- Dendreon Pharmaceuticals LLC

- Exelixis, Inc.

- Genentech (Roche)

- Clovis Oncology

- Eli Lilly and Company

- Seagen Inc.

- Myovant Sciences

- Medivation (Pfizer)

- Janssen Biotech (Johnson & Johnson)

Frequently Asked Questions

What is the projected growth rate for the Prostate Cancer Treatment Drug Market?

The Prostate Cancer Treatment Drug Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, reaching USD 28.0 Billion by 2033.

What are the primary drivers of the Prostate Cancer Treatment Drug Market?

Key drivers include the increasing global incidence of prostate cancer, an aging population, continuous advancements in therapeutic modalities, rising awareness leading to early diagnosis, and significant investments in research and development for novel drugs.

How is AI impacting the development of prostate cancer treatments?

AI is significantly impacting the market by accelerating drug discovery, enhancing precision in diagnostics, optimizing clinical trial design, facilitating personalized treatment planning, and identifying novel therapeutic combinations to overcome drug resistance.

Which regions are expected to show significant growth in the Prostate Cancer Treatment Drug Market?

The Asia Pacific region is anticipated to exhibit the highest growth rate due to improving healthcare infrastructure, increasing awareness, and a growing geriatric population. North America and Europe will continue to hold substantial market shares.

What types of drugs are primarily used in prostate cancer treatment?

The market primarily utilizes hormonal therapies (such as ADT, antiandrogens, GnRH agonists/antagonists), chemotherapy, immunotherapies, targeted therapies (e.g., PARP inhibitors), and radiopharmaceuticals, often in monotherapy or combination regimens depending on the cancer stage.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted