Propylene Oxide Market

Propylene Oxide Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709928 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

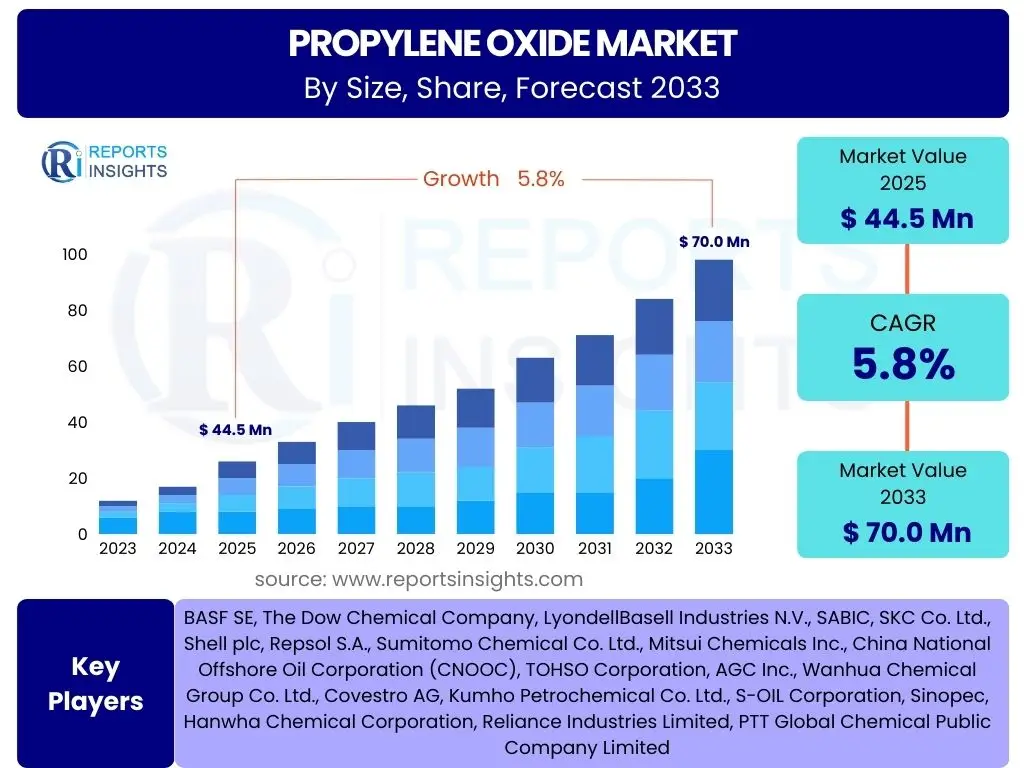

Propylene Oxide Market Size

According to Reports Insights Consulting Pvt Ltd, The Propylene Oxide Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 44.5 Billion in 2025 and is projected to reach USD 70.0 Billion by the end of the forecast period in 2033.

Key Propylene Oxide Market Trends & Insights

The global propylene oxide market is currently experiencing significant shifts driven by evolving industrial demands and technological advancements. A prominent trend involves the increasing adoption of sustainable and environmentally friendly production processes, moving away from traditional methods that generate considerable by-products. This pivot is largely influenced by stringent environmental regulations and a growing corporate emphasis on green chemistry principles, fostering innovation in areas such as hydrogen peroxide to propylene oxide (HPPO) technology, which offers reduced waste generation and energy consumption.

Furthermore, the market is observing a sustained demand from the automotive and construction sectors, particularly for polyurethane applications. The lightweighting trend in automotive manufacturing, aiming for improved fuel efficiency, fuels the demand for polyurethane foams derived from propylene oxide. Similarly, the rapid urbanization and infrastructure development in emerging economies, notably in Asia Pacific, continue to boost the construction industry's need for insulation and protective coatings, anchoring propylene oxide's market growth despite global economic fluctuations.

Another crucial insight is the increasing integration of bio-based propylene oxide precursors and derivatives. Research and development efforts are intensifying to explore renewable feedstocks and biotechnological routes for propylene oxide synthesis, offering a pathway to reduce reliance on fossil resources and align with circular economy models. This trend, while still in its nascent stages, presents long-term potential for market disruption and sustainable growth, attracting investments from major chemical manufacturers.

- Shift towards sustainable and cleaner production technologies (e.g., HPPO process).

- Growing demand from polyurethane manufacturing for automotive lightweighting and construction insulation.

- Rising focus on bio-based propylene oxide derivatives and renewable feedstocks.

- Increasing application in specialty chemicals and performance materials.

- Strategic capacity expansions in Asia Pacific to meet regional demand.

AI Impact Analysis on Propylene Oxide

The integration of Artificial Intelligence (AI) across various industrial sectors is beginning to significantly influence the propylene oxide market, primarily through optimizing production processes and enhancing supply chain efficiency. User inquiries frequently center on how AI can streamline complex chemical reactions, predict equipment failures, and improve energy consumption in manufacturing plants. AI-driven predictive analytics can analyze vast datasets from sensors and operational parameters to identify optimal reaction conditions, leading to higher yields and reduced operational costs for propylene oxide producers. This level of optimization is crucial for maintaining competitiveness in a capital-intensive industry.

Beyond the manufacturing floor, AI's impact extends to supply chain management and demand forecasting. Concerns often arise regarding the accuracy of market predictions and the ability to respond swiftly to fluctuating raw material prices and customer demands. AI algorithms can process global economic indicators, historical sales data, and real-time logistics information to provide more precise demand forecasts for propylene oxide and its derivatives. This enables companies to optimize inventory levels, reduce waste, and manage logistics more effectively, ensuring timely delivery to end-use industries like automotive and construction.

Furthermore, AI is anticipated to play a role in research and development, particularly in discovering new catalytic processes and material formulations for propylene oxide applications. Users are keen to understand how AI can accelerate the development of sustainable production routes or novel derivatives with enhanced properties. While the direct application of AI in the core chemical synthesis of propylene oxide is still evolving, its ancillary benefits in process control, quality assurance, and market intelligence are already creating efficiency gains and fostering innovation within the industry, preparing it for future technological shifts.

- Enhanced process optimization and control in propylene oxide manufacturing, improving yield and energy efficiency.

- Predictive maintenance for production equipment, reducing downtime and operational costs.

- Advanced supply chain optimization and demand forecasting, leading to better inventory management.

- Data-driven quality control and product consistency improvements.

- Acceleration of R&D for new catalysts and sustainable production pathways through AI-driven simulations.

Key Takeaways Propylene Oxide Market Size & Forecast

The global propylene oxide market is poised for robust expansion, driven by its critical role in various downstream industries and ongoing innovation in production technologies. A key takeaway for stakeholders is the sustained and healthy Compound Annual Growth Rate (CAGR) projected through 2033, indicating a resilient market despite economic volatility. This growth is predominantly fueled by the insatiable demand for polyurethane products in rapidly expanding sectors such as automotive, building and construction, and packaging, particularly in emerging economies where industrialization and urbanization continue to accelerate.

Another crucial insight is the strategic importance of technological advancement in shaping the market's future. The increasing adoption of more efficient and environmentally benign production methods, such as the HPPO process, is not merely a regulatory compliance measure but a significant competitive differentiator. Companies investing in these advanced technologies are likely to gain market share due to lower operational costs, reduced environmental footprint, and enhanced product quality, addressing both economic and ecological imperatives.

Finally, the market's trajectory emphasizes the growing influence of sustainability and circular economy principles. As global industries pivot towards greener alternatives, the demand for bio-based propylene oxide and derivatives is expected to rise, presenting both challenges and lucrative opportunities for innovation and market leadership. Understanding these dynamics and strategically positioning within the evolving regulatory and consumer landscape will be paramount for long-term success in the propylene oxide market.

- Significant market expansion anticipated with a CAGR of 5.8% by 2033.

- Polyurethane demand from automotive, construction, and packaging sectors remains the primary growth engine.

- Technological advancements in greener production processes (e.g., HPPO) are critical for competitive advantage.

- Asia Pacific continues to be a pivotal region for both production and consumption growth.

- Increasing focus on sustainable and bio-based propylene oxide solutions to drive future innovation and market trends.

Propylene Oxide Market Drivers Analysis

The propylene oxide market's expansion is fundamentally propelled by the consistent and expanding demand from its primary end-use industries. The automotive sector, for instance, is a significant consumer of polyurethane foams, which are essential for lightweighting vehicles to improve fuel efficiency and reduce emissions. As global automotive production recovers and electric vehicle adoption increases, the need for advanced polymer materials that offer both structural integrity and reduced weight drives the demand for propylene oxide. This trend is particularly pronounced in Asia Pacific, where vehicle ownership is rapidly growing, and stringent emission standards are being implemented.

Parallel to the automotive industry, the building and construction sector represents another robust driver. Propylene oxide is a key precursor for polyether polyols, which are used to produce rigid and flexible polyurethane foams. These foams are extensively utilized in insulation, roofing, and sealants due to their excellent thermal properties and durability. With global efforts towards energy-efficient buildings and the sustained pace of infrastructure development in emerging economies, the demand for high-performance insulation materials continues to surge. This contributes significantly to the overall market growth, especially in urbanizing regions that prioritize sustainable construction practices.

Furthermore, advancements in production technology, particularly the shift towards more cost-effective and environmentally friendly processes like HPPO (Hydrogen Peroxide to Propylene Oxide), are enhancing the attractiveness and viability of propylene oxide production. These innovations reduce reliance on co-product formation, lower energy consumption, and minimize waste, thereby improving profit margins for manufacturers and encouraging capacity expansions. Such technological progress allows for a more sustainable supply chain, aligning with global environmental objectives and fostering market expansion by making propylene oxide production more efficient and competitive.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for polyurethanes in automotive sector | +1.5% | Global, particularly Asia Pacific, North America | Mid-term to Long-term |

| Increased use in building & construction for insulation | +1.2% | Asia Pacific, Europe, North America | Mid-term to Long-term |

| Technological advancements in production (e.g., HPPO process) | +0.8% | Global | Short-term to Mid-term |

| Expansion of flexible packaging industry | +0.7% | Asia Pacific, Latin America | Short-term to Mid-term |

| Rising demand for propylene glycol derivatives | +0.6% | Global | Mid-term |

Propylene Oxide Market Restraints Analysis

Despite its robust growth prospects, the propylene oxide market faces several significant restraints that could impede its trajectory. A primary concern is the volatility in raw material prices, particularly for propylene and hydrogen peroxide. Propylene, a petrochemical derivative, is directly linked to crude oil prices, which are subject to geopolitical tensions and global supply-demand dynamics. Fluctuations in these feedstock costs can directly impact the production economics of propylene oxide, leading to unpredictable profit margins for manufacturers and potentially deterring investments in new capacities or technologies. This price instability creates considerable challenges for long-term planning and cost management across the industry.

Another considerable restraint is the stringent environmental regulations surrounding the production and handling of propylene oxide. Traditional chlorohydrin processes generate significant amounts of chlorinated by-products, necessitating costly waste treatment and disposal methods. While newer processes like HPPO offer cleaner alternatives, their adoption requires substantial capital expenditure and technological expertise. Companies must navigate complex regulatory landscapes, especially in developed regions like Europe and North America, which can add to operational costs and slow down market expansion. The increasing focus on sustainability also pressures manufacturers to invest in more expensive, greener technologies, potentially impacting profitability in the short term.

Furthermore, the market faces challenges from the oversupply of certain derivatives in specific regions, which can lead to price erosion and reduced profitability. For instance, the expansion of polyols capacity in some Asian countries might temporarily exceed demand, creating a buyer's market for propylene oxide derivatives. This regional imbalance in supply and demand, coupled with intense competition among key players, can create downward pressure on prices, impacting overall market revenue. Navigating these regional oversupply scenarios requires careful strategic planning and diversification of end-use applications to maintain healthy market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of raw material (propylene, hydrogen peroxide) prices | -0.9% | Global | Short-term to Mid-term |

| Stringent environmental regulations on production processes | -0.7% | Europe, North America, China | Mid-term to Long-term |

| High capital expenditure for new production technologies | -0.5% | Global | Long-term |

| Oversupply of specific derivatives in regional markets | -0.4% | Asia Pacific, North America | Short-term |

| Competition from alternative materials/processes | -0.3% | Global | Mid-term |

Propylene Oxide Market Opportunities Analysis

The propylene oxide market is characterized by several promising opportunities that could accelerate its growth trajectory. One significant avenue lies in the burgeoning demand for specialized and high-performance polyurethanes across diverse industries. Beyond traditional automotive and construction applications, there is an increasing need for polyurethanes in consumer goods, sports equipment, medical devices, and footwear, driven by their superior durability, flexibility, and insulation properties. Developing innovative propylene oxide derivatives tailored for these niche applications, such as bio-based polyols or those with enhanced fire resistance, presents a lucrative pathway for market expansion and value creation.

Another substantial opportunity resides in the continuous investment in research and development for sustainable production methods. The industry's shift towards cleaner technologies like HPPO and further exploration of bio-based feedstocks and catalysts for propylene oxide synthesis can unlock new markets and meet evolving regulatory and consumer demands for environmentally friendly products. Companies that successfully commercialize these green technologies can establish a strong competitive advantage, reduce their environmental footprint, and potentially access carbon credit markets, appealing to a growing segment of environmentally conscious consumers and investors. This focus on sustainability offers both reputational and economic benefits.

Furthermore, the rapid industrialization and urbanization in emerging economies, particularly in Asia Pacific, Latin America, and Africa, present significant untapped potential. These regions are experiencing substantial growth in construction, automotive, and manufacturing sectors, creating a robust demand for propylene oxide and its derivatives. Strategic investments in new production capacities, distribution networks, and localized research capabilities within these regions can allow market players to capture a larger share of these rapidly expanding markets. The growing middle class and increasing disposable incomes in these areas further amplify the consumption of products that utilize propylene oxide, such as appliances, furniture, and personal care items.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of specialized polyurethanes for new applications | +1.0% | Global | Mid-term to Long-term |

| Increased adoption of sustainable (e.g., bio-based) propylene oxide | +0.9% | Europe, North America, Asia Pacific | Mid-term to Long-term |

| Expansion in emerging economies (Asia Pacific, Latin America, Africa) | +1.3% | Asia Pacific, Latin America, Africa | Short-term to Long-term |

| Innovation in catalytic processes for improved efficiency | +0.7% | Global | Mid-term |

| Rising demand from personal care and pharmaceutical sectors | +0.6% | North America, Europe | Mid-term |

Propylene Oxide Market Challenges Impact Analysis

The propylene oxide market is confronted by several complex challenges that necessitate strategic responses from industry participants. A significant hurdle is the increasing regulatory scrutiny concerning environmental and health impacts. Propylene oxide is classified as a hazardous substance, and its production and handling are subject to strict regulations regarding emissions, waste management, and worker safety. Compliance with these evolving standards, particularly in regions with advanced environmental policies, often requires substantial investments in pollution control technologies and safety protocols, increasing operational costs and potentially delaying project timelines for new facilities or expansions. Non-compliance can result in hefty fines and reputational damage.

Another prominent challenge involves the technological complexity and high capital intensity associated with advanced propylene oxide production processes. While methods like HPPO offer environmental advantages, they demand significant upfront investment in specialized equipment, advanced catalysis, and sophisticated engineering. The long lead times for construction and commissioning of such plants, coupled with the need for highly skilled labor, can act as barriers to entry for new players and pose financial risks for existing ones. This high investment requirement can slow down the adoption of cleaner technologies, particularly for smaller and medium-sized enterprises, limiting the overall market's transition to more sustainable practices.

Furthermore, the market faces intense competition and potential commoditization of certain propylene oxide derivatives. As production capacities expand globally, particularly in cost-advantageous regions, price wars and margin compression can become prevalent. This commoditization pressures manufacturers to differentiate their products through quality, service, or specialized applications, which requires continuous innovation and R&D investment. Additionally, the fluctuating global economic climate, including trade tensions and supply chain disruptions, can further exacerbate these challenges by impacting demand from end-use industries and hindering efficient logistics, making it difficult to maintain stable market conditions and consistent profitability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent environmental and health safety regulations | -0.8% | Global | Long-term |

| High capital intensity and technological complexity of new plants | -0.7% | Global | Long-term |

| Intense market competition and potential commoditization | -0.6% | Asia Pacific, Europe | Short-term to Mid-term |

| Supply chain disruptions and logistics complexities | -0.5% | Global | Short-term |

| Slower economic growth in key end-use regions | -0.4% | Europe, North America | Short-term |

Propylene Oxide Market - Updated Report Scope

This market insights report offers an exhaustive analysis of the global propylene oxide market, encapsulating comprehensive data from historical trends to future projections. The scope includes an in-depth examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographies. Special emphasis is placed on technological advancements in production processes and the evolving landscape of end-use applications, providing stakeholders with critical intelligence to navigate the dynamic market environment. The report also addresses the impact of AI and sustainability initiatives on the industry's future trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 44.5 Billion |

| Market Forecast in 2033 | USD 70.0 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, The Dow Chemical Company, LyondellBasell Industries N.V., SABIC, SKC Co. Ltd., Shell plc, Repsol S.A., Sumitomo Chemical Co. Ltd., Mitsui Chemicals Inc., China National Offshore Oil Corporation (CNOOC), TOHSO Corporation, AGC Inc., Wanhua Chemical Group Co. Ltd., Covestro AG, Kumho Petrochemical Co. Ltd., S-OIL Corporation, Sinopec, Hanwha Chemical Corporation, Reliance Industries Limited, PTT Global Chemical Public Company Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The propylene oxide market is extensively segmented by application, production process, and end-use industry, reflecting the diverse utility and complex manufacturing landscape of this vital chemical intermediate. Each segment plays a crucial role in shaping the overall market dynamics, influenced by specific market drivers, technological advancements, and regional demands. Understanding these segmentations is key to identifying growth pockets and developing targeted market strategies, as different applications and processes exhibit varying levels of maturity, profitability, and environmental impact.

The application segment, predominantly driven by polyether polyols, underpins the robust demand for propylene oxide due to its widespread use in polyurethane production. Polyols are critical components in flexible and rigid foams essential for automotive interiors, building insulation, and furniture. Meanwhile, the production process segmentation highlights the industry's gradual shift from traditional, co-product-intensive methods to more sustainable and efficient technologies like HPPO. This transition is not only driven by environmental regulations but also by the pursuit of enhanced operational efficiency and cost-effectiveness, signifying a significant trend in manufacturing innovation.

Furthermore, the end-use industry segmentation provides a granular view of where propylene oxide's demand originates, with automotive and building & construction sectors leading the charge. These industries' growth trajectories directly correlate with the propylene oxide market's performance, as they are major consumers of polyurethane and propylene glycol derivatives. Analyzing these segments helps in forecasting future demand, understanding consumer preferences, and identifying emerging opportunities in sectors such as personal care and pharmaceuticals, which are increasingly incorporating propylene oxide derivatives for their unique properties.

- By Application:

- Polyether Polyols: Largest segment, crucial for polyurethane foams.

- Propylene Glycol (PG): Used in coolants, de-icers, and unsaturated polyester resins.

- Polypropylene Glycol (PPG): Essential in lubricants, surfactants, and cosmetics.

- Solvents: Applied in paints, coatings, and industrial cleaners.

- Other Derivatives: Includes butanols, allyl alcohol, and specialty chemicals.

- By Production Process:

- Chlorohydrin Process: Traditional method, but environmentally challenged.

- PO/SM (Styrene Monomer) Process: Co-produces styrene, economically viable.

- HPPO (Hydrogen Peroxide to Propylene Oxide) Process: Environmentally friendly, no significant co-products.

- Cumene Hydroperoxide Process: Emerging process with fewer by-products.

- Other Processes: Includes direct oxidation and biological methods.

- By End-Use Industry:

- Automotive: For seats, interior components, and lightweighting solutions.

- Building & Construction: For insulation, sealants, and adhesives.

- Packaging: For flexible foams and protective materials.

- Furniture & Bedding: For upholstery, mattresses, and cushions.

- Textiles & Carpets: For synthetic fibers and backings.

- Food & Beverages: As an additive or processing aid for packaging.

- Pharmaceuticals: As an excipient or solvent.

- Cosmetics & Personal Care: In emollients and humectants.

- Other Industries: Including electronics, aerospace, and marine.

Regional Highlights

The global propylene oxide market exhibits distinct regional dynamics, with Asia Pacific standing out as the dominant and fastest-growing region. This prominence is primarily attributed to rapid industrialization, burgeoning construction activities, and a flourishing automotive sector across countries like China, India, and Southeast Asian nations. The region benefits from significant manufacturing capacities and a large consumer base, driving both production and consumption of propylene oxide and its derivatives. Furthermore, governmental support for infrastructure development and the increasing adoption of energy-efficient building materials fuel the demand for polyurethane foams, cementing Asia Pacific's leadership in the market.

North America and Europe represent mature markets for propylene oxide, characterized by advanced technological adoption and stringent environmental regulations. In North America, the robust automotive industry and steady demand from the construction sector, particularly for high-performance insulation, maintain a stable market presence. The region is also at the forefront of investing in sustainable production technologies, like HPPO, to meet environmental compliance and enhance operational efficiency. Similarly, Europe emphasizes sustainability and circular economy initiatives, fostering innovation in bio-based propylene oxide and driving demand for high-value applications in specialized chemicals and advanced materials.

Latin America, and the Middle East and Africa (MEA) regions, while smaller in market share, offer significant growth potential due to ongoing industrial development and increasing investments in manufacturing infrastructure. Latin America's growth is often linked to its expanding automotive sector and agricultural industries. The MEA region is witnessing increased demand driven by diversification efforts from oil-dependent economies into manufacturing, construction, and infrastructure projects. These regions are likely to attract future investments in production capacities and distribution networks as global players seek to tap into new markets and diversify their supply chains.

- Asia Pacific: Dominant market share and fastest growth, driven by China, India, and Southeast Asia's industrialization, construction boom, and automotive production. Significant investments in new production capacities.

- North America: Mature market with steady demand from automotive and construction, strong focus on technological advancements (e.g., HPPO) and sustainable practices.

- Europe: Established market characterized by stringent environmental regulations, high demand for specialty chemicals, and increasing focus on bio-based propylene oxide and circular economy initiatives.

- Latin America: Emerging market with growth potential driven by expanding automotive and construction industries, along with a growing middle class.

- Middle East & Africa (MEA): Growth attributed to economic diversification, infrastructure development, and increasing industrial activities in the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Propylene Oxide Market.- BASF SE

- The Dow Chemical Company

- LyondellBasell Industries N.V.

- SABIC

- SKC Co. Ltd.

- Shell plc

- Repsol S.A.

- Sumitomo Chemical Co. Ltd.

- Mitsui Chemicals Inc.

- China National Offshore Oil Corporation (CNOOC)

- TOHSO Corporation

- AGC Inc.

- Wanhua Chemical Group Co. Ltd.

- Covestro AG

- Kumho Petrochemical Co. Ltd.

- S-OIL Corporation

- Sinopec

- Hanwha Chemical Corporation

- Reliance Industries Limited

- PTT Global Chemical Public Company Limited

Frequently Asked Questions

Analyze common user questions about the Propylene Oxide market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is propylene oxide (PO) and its primary uses?

Propylene oxide (PO) is a key chemical intermediate derived from propylene, primarily used in the production of polyether polyols for polyurethane foams, which are essential in automotive, construction, and furniture industries. It also serves as a precursor for propylene glycol and other derivatives.

What are the main production processes for propylene oxide?

The main production processes include the Chlorohydrin process, the PO/SM (Styrene Monomer) co-production process, and the HPPO (Hydrogen Peroxide to Propylene Oxide) process, with HPPO gaining traction due to its environmental benefits of fewer by-products.

Which regions are leading the growth in the propylene oxide market?

Asia Pacific, particularly countries like China and India, leads the growth in the propylene oxide market due to rapid industrialization, burgeoning construction activities, and a thriving automotive sector.

What are the key drivers for the propylene oxide market?

The key drivers include the rising demand for polyurethanes in automotive and construction sectors, technological advancements in greener production processes, and increasing applications of propylene glycol and its derivatives in various industries.

What are the major challenges facing the propylene oxide market?

Major challenges include volatility in raw material prices, stringent environmental regulations on production and emissions, high capital expenditure for new and cleaner technologies, and intense market competition from existing and new players.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted