Property Insurance Market

Property Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705679 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

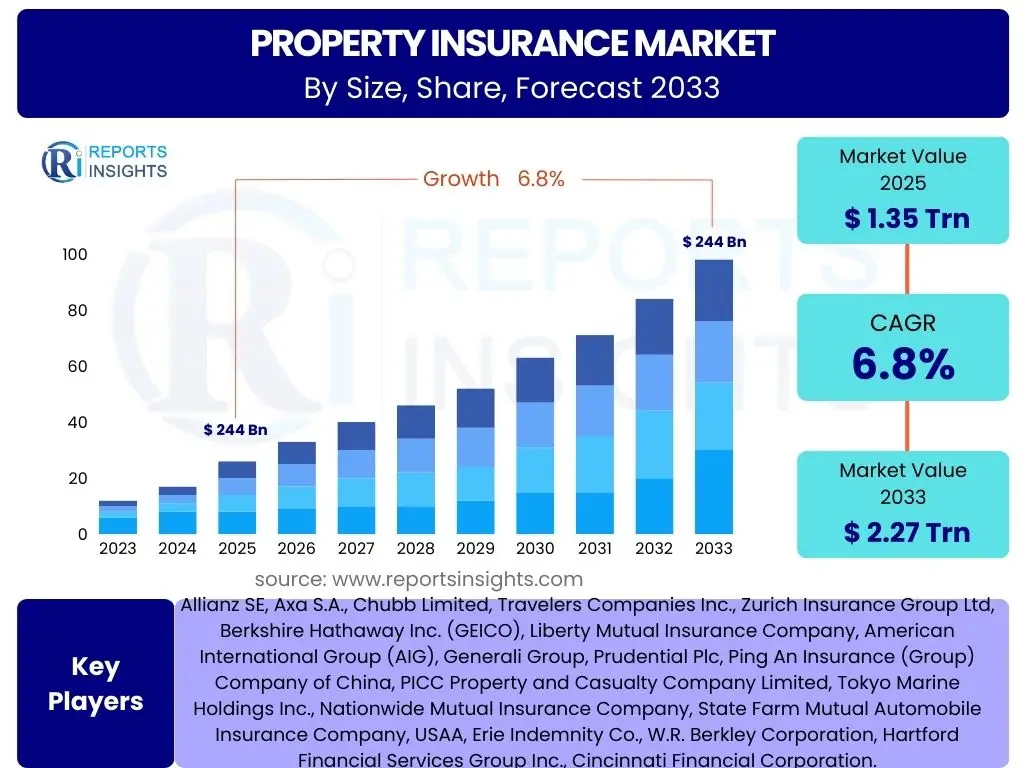

Property Insurance Market Size

According to Reports Insights Consulting Pvt Ltd, The Property Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.35 Trillion in 2025 and is projected to reach USD 2.27 Trillion by the end of the forecast period in 2033. This robust growth is primarily driven by increasing urbanization, rising property values globally, and a heightened awareness of the financial risks associated with various perils, including natural disasters and human-made calamities.

The consistent expansion reflects a resilient demand for protection against unforeseen events affecting residential, commercial, and industrial properties. Furthermore, evolving regulatory landscapes in various regions are contributing to the mandatory adoption of property insurance, particularly for mortgaged properties. The market's upward trajectory is also supported by technological advancements enabling more precise risk assessment and efficient claims processing, which enhance the overall value proposition for policyholders.

Key Property Insurance Market Trends & Insights

The property insurance market is experiencing significant transformation, driven by technological innovation, evolving risk landscapes, and shifting consumer expectations. Users frequently inquire about the impact of climate change, digitalization of services, and the emergence of new coverage types. The industry is responding by integrating advanced analytics, artificial intelligence, and IoT devices to better understand and mitigate risks, while simultaneously enhancing customer engagement through personalized offerings and seamless digital experiences. Furthermore, a growing emphasis on sustainability and resilience is influencing underwriting practices and encouraging preventative measures.

- Climate Change Adaptation: Insurers are increasingly incorporating climate risk models into underwriting, pricing, and claims management, with a focus on perils like floods, wildfires, and severe storms.

- Digital Transformation & Automation: Accelerated adoption of online platforms, mobile applications, and automated processes for policy issuance, claims submission, and customer service.

- Parametric Insurance: Growing interest in parametric policies that offer quicker payouts based on predefined triggers (e.g., wind speed, rainfall levels) rather than traditional damage assessment.

- IoT & Telematics Integration: Utilization of smart home devices and sensors to monitor property conditions, offer preventative insights, and potentially reduce premiums for proactive policyholders.

- Embedded Insurance: Integration of insurance products directly into non-insurance purchase processes, such as property transactions or smart home device sales, for seamless customer experience.

- Hyper-Personalization of Policies: Leveraging data analytics to offer tailored coverage and pricing based on individual risk profiles and property characteristics.

AI Impact Analysis on Property Insurance

Artificial intelligence is profoundly reshaping the property insurance landscape, addressing key user concerns about efficiency, accuracy, and customer experience. Users frequently ask how AI can improve claims processing, underwriting, and risk assessment. AI technologies are enabling insurers to move from reactive indemnification to proactive risk management and prevention. By analyzing vast datasets, AI facilitates more precise risk segmentation, dynamic pricing, and accelerated claims resolutions, thereby enhancing operational efficiency and potentially lowering costs for both insurers and policyholders.

Moreover, AI-driven solutions are improving fraud detection capabilities, reducing financial losses, and ensuring fairer outcomes for legitimate claims. The integration of machine learning algorithms allows for continuous learning and adaptation to new data patterns, making the insurance process more intelligent and responsive to changing market conditions and emerging risks. While concerns about data privacy and algorithmic bias exist, the overarching sentiment points towards AI as a critical enabler for the future of property insurance, offering capabilities that were previously unattainable.

- Enhanced Risk Assessment & Underwriting: AI algorithms analyze historical data, satellite imagery, geospatial data, and real-time sensor information to provide more accurate and granular risk profiles, leading to optimized pricing.

- Automated Claims Processing: AI-powered systems can quickly process claims by analyzing damage photos/videos, identifying patterns, and automating approvals for straightforward cases, significantly reducing cycle times.

- Fraud Detection & Prevention: Machine learning models can identify suspicious patterns and anomalies in claims data, flagging potential fraudulent activities for human review.

- Personalized Customer Experience: AI-driven chatbots and virtual assistants provide instant support, answer queries, and guide customers through policy selection or claims submission, improving satisfaction.

- Predictive Maintenance & Prevention: AI analyzes IoT data from smart homes/buildings to predict potential issues (e.g., water leaks, electrical faults) and alert property owners, preventing losses before they occur.

Key Takeaways Property Insurance Market Size & Forecast

The property insurance market is poised for significant and sustained growth through 2033, a critical insight for stakeholders seeking to understand its future trajectory. Users often inquire about the main drivers of this growth and what defines the market's resilience. The primary takeaway is the market's inherent necessity in an increasingly complex and risk-prone world, reinforced by global urbanization, rising property values, and an escalating frequency of extreme weather events. This foundational demand, coupled with technological advancements, underscores a future characterized by innovation, efficiency, and expanded coverage options.

Another key insight is the profound impact of digitalization and AI, which are not merely trends but foundational shifts transforming how property insurance is delivered, underwritten, and claims are managed. The industry is evolving towards more predictive, personalized, and efficient models. This adaptation ensures market resilience, offering substantial opportunities for companies that embrace these changes and address emerging risks effectively. The forecast indicates a robust environment for investment and strategic development, driven by both intrinsic market needs and external technological forces.

- Sustained Growth Trajectory: The market is set for consistent expansion, driven by urbanization, increasing property values, and heightened risk awareness.

- Technological Imperative: Digitalization, AI, and IoT are not optional but essential for competitiveness, driving efficiency and new service models.

- Climate Risk Centrality: Climate change is a primary long-term driver of risk and innovation, pushing insurers to develop new models and products.

- Focus on Prevention & Mitigation: The industry is shifting towards proactive risk management rather than solely reactive payouts.

- Customer-Centric Evolution: Personalization and seamless digital experiences are becoming critical differentiators in a competitive market.

Property Insurance Market Drivers Analysis

The Property Insurance Market is propelled by several fundamental drivers that reinforce its growth and stability. A significant factor is the consistent increase in global property values and construction activities, which naturally expands the insurable base. Alongside this, the escalating frequency and intensity of natural catastrophes, such as hurricanes, floods, and wildfires, heighten awareness among property owners about the critical need for financial protection against devastating losses. Regulatory requirements, particularly mortgage lending stipulations, often mandate property insurance, further bolstering demand. Additionally, a growing global population and rapid urbanization contribute to the development of new residential and commercial properties, each requiring comprehensive insurance coverage.

Technological advancements also play a crucial role as a market driver. The integration of smart home technologies and IoT devices offers insurers richer data for more accurate risk assessment and enables policyholders to implement preventative measures, potentially reducing claims. Furthermore, increased public awareness regarding various types of property risks and the financial implications of unmitigated losses, often fueled by media coverage of catastrophic events, encourages more widespread adoption of property insurance policies. This confluence of economic growth, environmental challenges, regulatory frameworks, and technological innovation collectively drives the expansion of the property insurance sector.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Property Values & Construction | +1.5% | Global, particularly Emerging Economies | Mid- to Long-term |

| Rising Frequency of Natural Catastrophes | +1.2% | Coastal Regions, Disaster-Prone Areas (e.g., North America, APAC) | Short- to Long-term |

| Mandatory Mortgage Requirements | +0.8% | Globally, wherever mortgage financing is prevalent | Consistent, Ongoing |

| Urbanization & Population Growth | +0.9% | Asia Pacific, Africa, Latin America | Long-term |

| Technological Advancements (IoT, AI) | +0.7% | Developed Markets (North America, Europe) | Mid- to Long-term |

Property Insurance Market Restraints Analysis

Despite robust growth, the Property Insurance Market faces several significant restraints that could temper its expansion. Economic downturns and inflationary pressures can reduce disposable income, making property owners hesitant to purchase or renew comprehensive policies due to high premium costs. The perception of excessive premium rates, often driven by increasing claims costs related to natural disasters, can lead to underinsurance or non-insurance, particularly in price-sensitive markets. Furthermore, regulatory complexities and varying legal frameworks across different regions can create compliance burdens for insurers, hindering their ability to operate efficiently across borders and offer standardized products.

Another key restraint is the issue of climate change making certain high-risk areas increasingly uninsurable or prohibitively expensive to insure. As climate-related risks intensify, some properties may become too risky for insurers to cover at affordable rates, leading to coverage gaps. Additionally, intense competition within the insurance sector can lead to price wars, impacting profitability and discouraging innovation, especially for smaller market participants. The lack of awareness or understanding of insurance products, particularly in developing regions, also acts as a restraint, as potential customers may not fully grasp the benefits of comprehensive coverage until it is too late.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Premium Costs & Affordability Issues | -1.0% | Globally, particularly price-sensitive markets | Short- to Mid-term |

| Economic Volatility & Inflation | -0.8% | Global, impacting consumer spending | Short-term |

| Regulatory Complexities & Compliance Burden | -0.5% | Europe, highly regulated markets | Ongoing |

| Uninsurability in High-Risk Climate Zones | -0.7% | Specific coastal, flood-prone, or wildfire-prone regions | Long-term |

| Lack of Awareness in Developing Regions | -0.6% | Asia Pacific, Africa, Latin America | Mid- to Long-term |

Property Insurance Market Opportunities Analysis

Significant opportunities are emerging within the Property Insurance Market, driven by evolving consumer needs and technological advancements. One key area is the expansion into underserved and emerging markets, particularly in Asia Pacific and Africa, where rising economic prosperity and increasing property ownership present a vast untapped customer base. The development of specialized insurance products for novel risks, such as cyber threats affecting smart home systems or tailored coverage for climate change impacts like subsidence or specific catastrophic events, offers new revenue streams. Furthermore, the burgeoning demand for parametric insurance, which provides rapid payouts based on predefined triggers rather than traditional claims assessments, represents a significant growth opportunity by improving efficiency and customer satisfaction.

The continuous evolution of digital distribution channels, including direct-to-consumer online platforms and partnerships with proptech companies, enables insurers to reach a wider audience and streamline the customer journey. Leveraging data analytics and artificial intelligence for hyper-personalization of policies allows insurers to offer more accurate pricing and tailored coverage, catering to individual risk profiles and fostering stronger customer relationships. Additionally, opportunities exist in offering value-added services focused on risk prevention and mitigation, such as smart home device subsidies or real-time alerts for potential hazards, shifting the insurer's role from merely indemnifying losses to actively preventing them. This proactive approach not only enhances customer loyalty but also improves overall loss ratios for insurers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Underserved & Emerging Markets | +1.5% | Asia Pacific, Africa, Latin America | Mid- to Long-term |

| Development of Specialized & Parametric Policies | +1.0% | Global, particularly developed markets | Mid- to Long-term |

| Digital Distribution Channels & Partnerships | +0.9% | Global, especially tech-savvy regions | Short- to Mid-term |

| Data-Driven Personalization & Prevention Services | +0.8% | North America, Europe | Mid-term |

| Integration with Real Estate & Proptech Ecosystems | +0.7% | Urban areas, high-tech adoption regions | Mid-term |

Property Insurance Market Challenges Impact Analysis

The Property Insurance Market faces several significant challenges that necessitate strategic adaptation from market players. Foremost among these is the escalating impact of climate change, leading to more frequent and severe extreme weather events, which results in higher claims payouts and increased reinsurance costs, pressuring insurer profitability. Adapting to rapid technological advancements, such as integrating IoT devices and AI into existing legacy systems, presents significant investment and operational hurdles for many traditional insurers. Additionally, data privacy concerns and cybersecurity threats associated with collecting and analyzing extensive customer and property data are becoming increasingly critical, demanding robust security protocols and compliance measures.

Another major challenge is maintaining profitability amidst intense competition and the pressure to keep premiums affordable, especially when combined with rising claims costs. The complexity of accurately pricing risk in an increasingly volatile environment, coupled with regulatory scrutiny and the need for new capital for catastrophe coverage, adds further pressure. Furthermore, a shortage of skilled talent in areas like data science, AI, and climate risk modeling within the insurance sector poses a challenge to implementing advanced solutions and driving innovation effectively. Addressing these multifaceted challenges requires significant investment in technology, human capital, and adaptive business models to ensure long-term sustainability and growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Impact of Climate Change (Claims/Reinsurance) | -1.2% | Globally, particularly high-risk zones | Long-term |

| Technological Integration & Legacy Systems | -0.8% | Developed markets with established insurers | Mid-term |

| Data Privacy & Cybersecurity Risks | -0.7% | Global, especially regions with strict data regulations (e.g., EU) | Ongoing |

| Intense Competition & Pressure on Profitability | -0.6% | Globally, highly saturated markets | Short- to Mid-term |

| Shortage of Specialized Talent | -0.5% | Global, particularly for data science/AI roles | Long-term |

Property Insurance Market - Updated Report Scope

This report offers a comprehensive analysis of the Property Insurance Market, delving into its current landscape, historical trends, and future projections. The scope encompasses detailed market sizing, segmentation across various types of property coverage and distribution channels, and an in-depth examination of the key drivers, restraints, opportunities, and challenges shaping the industry. Special emphasis is placed on the transformative impact of artificial intelligence and emerging technological trends that are redefining risk assessment, underwriting, and claims management processes. The report also provides a thorough regional analysis, highlighting growth pockets and regulatory environments across major geographies, coupled with profiles of leading market participants to offer a holistic view of the competitive dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 Trillion |

| Market Forecast in 2033 | USD 2.27 Trillion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Allianz SE, Axa S.A., Chubb Limited, Travelers Companies Inc., Zurich Insurance Group Ltd, Berkshire Hathaway Inc. (GEICO), Liberty Mutual Insurance Company, American International Group (AIG), Generali Group, Prudential Plc, Ping An Insurance (Group) Company of China, PICC Property and Casualty Company Limited, Tokyo Marine Holdings Inc., Nationwide Mutual Insurance Company, State Farm Mutual Automobile Insurance Company, USAA, Erie Indemnity Co., W.R. Berkley Corporation, Hartford Financial Services Group Inc., Cincinnati Financial Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Property Insurance Market is extensively segmented to provide granular insights into its diverse components, allowing for a detailed understanding of market dynamics across various categories. These segmentations enable stakeholders to identify specific growth areas, understand market preferences, and tailor strategies to address distinct consumer and commercial needs. The primary classifications include the type of property coverage, the nature of covered perils, the application of the insurance (residential or commercial), and the channels through which policies are distributed. This detailed breakdown facilitates targeted marketing efforts and product development, ensuring that a wide range of property protection needs are met across the globe.

Understanding these segments is crucial for both established insurers and new entrants to pinpoint niches, optimize their offerings, and gain a competitive edge. For instance, the growing demand for specialized coverage like cyber property insurance reflects the evolving risk landscape, while the shift towards direct digital channels highlights changing consumer purchasing behaviors. Each segment holds unique opportunities and challenges, influencing pricing strategies, regulatory compliance, and market penetration approaches. Comprehensive analysis of these segmentations reveals the intricate structure of the property insurance ecosystem and its potential for future evolution.

- By Type:

- Homeowners Insurance

- Standard Homeowner Policies

- Renters Insurance

- Condo Insurance

- Commercial Property Insurance

- Business Owner's Policy (BOP)

- Commercial General Liability

- Property Specific Policies (e.g., Commercial Auto, Inland Marine)

- Specialty Property Insurance

- Flood Insurance

- Earthquake Insurance

- Title Insurance

- Cyber Property Insurance

- Terrorism Insurance

- Homeowners Insurance

- By Coverage Type:

- Fire Insurance

- Burglary Insurance

- Natural Hazard Insurance (Flood, Earthquake, Windstorm, Hail)

- Liability Coverage (for property-related incidents)

- All-Risk Coverage

- Named Perils Coverage

- By Application:

- Residential

- Single-Family Homes

- Multi-Family Dwellings

- Apartments/Condominiums

- Commercial

- Office Buildings

- Retail Spaces

- Manufacturing Facilities

- Warehouses & Logistics

- Hospitality (Hotels, Restaurants)

- Healthcare Facilities

- Educational Institutions

- Industrial

- Factories

- Plants

- Specialized Industrial Facilities

- Residential

- By Distribution Channel:

- Agents & Brokers

- Direct (Online, Company Websites, Call Centers)

- Bancassurance

- Partnerships (e.g., with real estate firms, proptech companies)

- Others (e.g., Affinity Groups, Employer-sponsored)

Regional Highlights

- North America: This region represents a mature and highly developed property insurance market, characterized by high adoption rates, strong regulatory frameworks, and significant technological integration. The market here is driven by substantial property values, frequent natural disaster events (hurricanes, wildfires in the US; floods in Canada), and a strong emphasis on digital transformation and AI adoption in underwriting and claims processing. The United States accounts for the largest share due to its vast property base and comprehensive insurance requirements.

- Europe: The European property insurance market is robust, influenced by stringent regulatory compliance (e.g., Solvency II), diverse national markets, and a growing focus on sustainability and climate change adaptation. Western European countries like Germany, the UK, and France are key contributors, demonstrating high penetration and a push towards innovative products such as parametric insurance for specific climate risks. Eastern Europe presents emerging opportunities as economies develop and property ownership increases.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by rapid urbanization, significant infrastructure development, and increasing disposable incomes leading to higher property ownership rates in countries like China, India, and Southeast Asian nations. The region is highly susceptible to natural disasters (earthquakes, typhoons, floods), which drives demand for insurance awareness and penetration, albeit from a lower base in many areas. Digitalization and mobile-first strategies are crucial for market expansion.

- Latin America: This region exhibits considerable growth potential, primarily driven by expanding economies, increasing middle-class populations, and ongoing urbanization. Countries like Brazil, Mexico, and Argentina are key markets, though they face challenges related to economic volatility and a lower overall insurance penetration compared to developed regions. Awareness campaigns and accessible product offerings are vital for unlocking the full market potential.

- Middle East and Africa (MEA): The MEA region is an emerging market for property insurance, characterized by varying levels of economic development and regulatory maturity. Growth is primarily driven by large-scale construction projects, infrastructure development, and increasing foreign investments, particularly in the Gulf Cooperation Council (GCC) countries. African nations are seeing gradual increases in property ownership and awareness, though the market remains largely untapped with significant scope for growth as economic stability improves and regulatory frameworks evolve.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Property Insurance Market.- Allianz SE

- Axa S.A.

- Chubb Limited

- Travelers Companies Inc.

- Zurich Insurance Group Ltd

- Berkshire Hathaway Inc.

- Liberty Mutual Insurance Company

- American International Group (AIG)

- Generali Group

- Prudential Plc

- Ping An Insurance (Group) Company of China

- PICC Property and Casualty Company Limited

- Tokyo Marine Holdings Inc.

- Nationwide Mutual Insurance Company

- State Farm Mutual Automobile Insurance Company

- USAA

- Erie Indemnity Co.

- W.R. Berkley Corporation

- Hartford Financial Services Group Inc.

- Cincinnati Financial Corporation

Frequently Asked Questions

Analyze common user questions about the Property Insurance market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is property insurance and why is it important?

Property insurance provides financial protection against risks to property, such as damage from natural disasters, fire, theft, or vandalism. It is crucial because it safeguards significant investments in homes or businesses, covering repair or replacement costs and providing peace of mind against unforeseen financial losses.

What factors influence property insurance premiums?

Premiums are influenced by multiple factors including the property's location (e.g., proximity to coast, flood zones), construction type and age, the value of the property, claims history, the specific coverage limits and deductibles chosen, and the implementation of safety features like security systems.

How is climate change impacting the property insurance market?

Climate change is leading to more frequent and intense extreme weather events, increasing the risk of property damage and subsequently driving up claims costs and reinsurance expenses. This impact is prompting insurers to reassess risk models, adjust premiums, and develop new policies to address emerging climate-related perils like wildfires and severe flooding.

What role does technology play in modern property insurance?

Technology, including AI, IoT, and data analytics, is transforming property insurance by enabling more accurate risk assessment and personalized pricing, automating claims processing for faster payouts, enhancing fraud detection, and facilitating proactive risk prevention through smart home devices. It also streamlines policy management and customer interactions.

What are the key trends shaping the future of property insurance?

Key trends include the widespread adoption of digitalization and automation, a shift towards parametric insurance for quicker payouts, the integration of IoT for preventative risk management, and hyper-personalization of policies using data analytics. A growing focus on sustainability and resilience is also influencing product development and underwriting practices.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted