Property and Casualty Reinsurance Market

Property and Casualty Reinsurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704915 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Property and Casualty Reinsurance Market Size

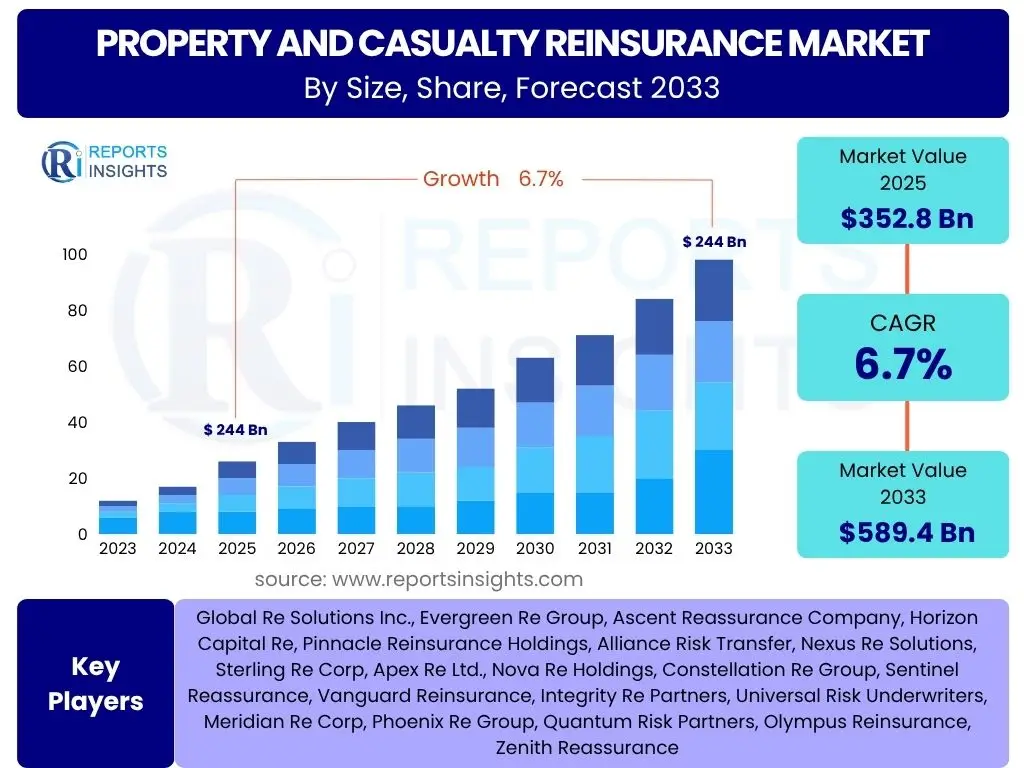

According to Reports Insights Consulting Pvt Ltd, The Property and Casualty Reinsurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 352.8 Billion in 2025 and is projected to reach USD 589.4 Billion by the end of the forecast period in 2033.

Key Property and Casualty Reinsurance Market Trends & Insights

The Property and Casualty (P&C) Reinsurance market is experiencing significant transformation driven by a confluence of evolving risk landscapes, technological advancements, and shifting global economic dynamics. Common user inquiries often revolve around how climate change, digital innovation, and increasing market complexity are reshaping the industry. Stakeholders are keen to understand the implications of rising natural catastrophe frequency and severity, the expanding cyber risk landscape, and the growing demand for specialized coverage.

Furthermore, there is considerable interest in how reinsurance capital is being deployed to cover these new and amplified risks, as well as the role of alternative capital in influencing market dynamics. Regulatory developments and geopolitical uncertainties also frequently emerge as areas of concern, influencing capacity deployment and pricing. The market's resilience in absorbing large-scale losses while maintaining profitability remains a core focus of analysis.

- Increased frequency and severity of natural catastrophes driving demand for robust reinsurance protection.

- Growth in alternative capital, such as catastrophe bonds and collateralized reinsurance, diversifying funding sources.

- Digitalization and advanced analytics transforming risk assessment, underwriting, and claims management processes.

- Emergence of new risk classes, including cyber risks, pandemic-related business interruption, and supply chain disruptions.

- Emphasis on environmental, social, and governance (ESG) factors influencing investment strategies and risk selection.

- Convergence of insurance and capital markets creating innovative risk transfer solutions.

- Development of parametric insurance solutions for faster payout and increased transparency, especially for climate-related events.

AI Impact Analysis on Property and Casualty Reinsurance

The integration of Artificial Intelligence (AI) within the Property and Casualty Reinsurance sector is a subject of intense interest and frequent user questions. Common themes include how AI can enhance risk modeling accuracy, streamline operational efficiencies, and improve claims processing. Users are particularly interested in AI's potential to analyze vast datasets for more precise underwriting, identify emerging risk patterns, and automate routine tasks, thereby freeing up human capital for complex decision-making.

Concerns often raised pertain to data privacy, the ethical implications of AI in decision-making, and the need for robust data governance frameworks. There is also curiosity about how AI will influence the traditional roles of actuaries and underwriters, suggesting a shift towards more data-driven and technology-enabled expertise. The expectation is that AI will not only optimize current processes but also unlock new avenues for product innovation, such as dynamic pricing and highly personalized coverage, ultimately enhancing the reinsurers' ability to manage volatility and uncertainty.

- Enhanced predictive analytics for risk assessment and pricing, leveraging machine learning algorithms.

- Automated claims processing through natural language processing (NLP) and computer vision, accelerating resolution times.

- Improved fraud detection capabilities using AI-powered pattern recognition and anomaly detection.

- Development of sophisticated catastrophe models incorporating real-time data and AI for more accurate projections.

- Personalized risk insights and customized reinsurance solutions based on granular data analysis.

- Operational efficiency gains through automation of underwriting support, policy administration, and compliance checks.

- Facilitation of parametric triggers using AI to analyze external data, enabling faster payout for defined events.

Key Takeaways Property and Casualty Reinsurance Market Size & Forecast

The Property and Casualty Reinsurance market is poised for sustained growth over the forecast period, reflecting its critical role in absorbing and distributing global risks. Key takeaways frequently highlighted by market participants and in common user questions underscore the market's resilience in the face of increasing volatility from both natural and man-made perils. The projected expansion signifies a robust demand for capital and expertise to manage growing exposures, particularly those driven by climate change and evolving technological risks.

Furthermore, the market's size and forecast indicate a strategic shift towards more data-driven and technology-enabled risk management. Reinsurers are increasingly investing in advanced analytics and artificial intelligence to enhance underwriting precision, optimize capital deployment, and improve claims efficiency. The emphasis on tailored solutions for complex and emerging risks, alongside a continued focus on core property and casualty lines, will define the trajectory of this essential financial sector.

- The P&C Reinsurance market demonstrates significant growth potential, driven by global risk accumulation and capital needs.

- Rising natural catastrophe losses are a primary catalyst for increased demand for reinsurance capacity.

- Technological integration, particularly AI and data analytics, is crucial for market efficiency and competitive advantage.

- Alternative capital continues to play an expanding role, influencing market pricing and capacity.

- Emerging markets present substantial opportunities for growth, necessitating localized risk transfer solutions.

Property and Casualty Reinsurance Market Drivers Analysis

The Property and Casualty Reinsurance market is propelled by several potent forces that consistently create demand for risk transfer solutions. A significant driver is the escalating frequency and severity of natural catastrophes globally, necessitating greater financial backing for primary insurers. Additionally, the increasing value and concentration of insurable assets, coupled with urbanization and climate change impacts, amplify potential losses and subsequently the need for robust reinsurance. Regulatory requirements, often mandating higher capital reserves for insurers, further stimulate reinsurance demand as a capital management tool.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Frequency and Severity of Natural Catastrophes | +1.5% | Global, particularly coastal regions and disaster-prone zones (e.g., USA, Japan, Caribbean) | Short to Long-term (Ongoing) |

| Growing Global Insurable Exposure and Urbanization | +1.2% | Asia Pacific (China, India), North America, Europe | Medium to Long-term |

| Stricter Regulatory Capital Requirements for Insurers | +0.8% | Europe (Solvency II), North America (NAIC Risk-Based Capital), Global | Medium-term |

| Emergence of New and Complex Risks (e.g., Cyber, Pandemic) | +1.0% | Global, with emphasis on developed economies and digitalized sectors | Short to Medium-term |

| Expansion in Developing Economies and Infrastructure Projects | +0.7% | Asia Pacific, Latin America, Africa | Long-term |

Property and Casualty Reinsurance Market Restraints Analysis

Despite its inherent growth drivers, the Property and Casualty Reinsurance market faces several significant restraints that can impede its expansion and profitability. High capital requirements for reinsurers can act as a barrier to entry for new players and limit the capacity of existing ones, particularly in volatile market conditions. Persistent low investment yields in a prolonged low-interest rate environment also challenge reinsurers' ability to generate sufficient returns from their investment portfolios, putting pressure on underwriting profitability. Furthermore, the complexities of navigating diverse and evolving regulatory frameworks across different jurisdictions add to operational costs and compliance burdens.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Requirements and Financial Volatility | -0.9% | Global, especially for new entrants and smaller players | Short to Medium-term |

| Prolonged Low Investment Yields | -0.7% | Global, particularly in mature economies | Medium to Long-term |

| Intense Competition and Market Softening Cycles | -0.5% | Global, affecting pricing and terms | Short to Medium-term |

| Regulatory Complexity and Jurisdictional Fragmentation | -0.6% | Europe, Asia Pacific, various developing markets | Ongoing |

| Difficulty in Accurately Modeling Emerging Systemic Risks | -0.4% | Global, especially for cyber, pandemics, and geopolitical events | Long-term |

Property and Casualty Reinsurance Market Opportunities Analysis

The Property and Casualty Reinsurance market is ripe with opportunities arising from evolving risk landscapes and technological innovation. The growing demand for specialized coverages for emerging risks like cyber warfare, supply chain disruptions, and intangible assets presents new avenues for product development and market penetration. The increasing adoption of advanced analytics, artificial intelligence, and blockchain technology can enhance operational efficiency, improve risk assessment, and foster new business models, creating competitive advantages. Furthermore, the expanding middle class and rapid economic development in emerging markets offer significant untapped potential for primary insurance and, consequently, reinsurance services.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Cyber Reinsurance Solutions | +1.3% | North America, Europe, Asia Pacific (developed economies) | Short to Long-term |

| Expansion of Parametric Insurance Offerings | +1.1% | Global, especially for climate-related risks and developing regions | Medium to Long-term |

| Leveraging AI and Advanced Analytics for Enhanced Underwriting | +1.0% | Global | Medium-term |

| Growth in Emerging Markets (e.g., Asia Pacific, Latin America, Africa) | +0.9% | China, India, Brazil, Indonesia, Nigeria | Long-term |

| Providing Reinsurance for Renewable Energy and Green Infrastructure Projects | +0.8% | Global, with focus on regions investing in green initiatives | Medium to Long-term |

Property and Casualty Reinsurance Market Challenges Impact Analysis

The Property and Casualty Reinsurance market faces formidable challenges that demand strategic foresight and adaptability. One of the most pressing challenges is the increasing uncertainty and complexity in accurately modeling and pricing systemic risks, such as pandemics, climate change impacts, and widespread cyberattacks, which can result in unpredictable aggregated losses. Furthermore, the persistent threat of market softening, driven by abundant capital and intense competition, can compress premium rates and undermine profitability. Attracting and retaining top talent, particularly those with expertise in data science, AI, and emerging risks, also remains a significant hurdle for reinsurers looking to innovate and stay competitive.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Uncertainty in Climate Change Modeling and Aggregation Risk | -0.8% | Global | Long-term |

| Systemic Risks (e.g., Cyber Warfare, New Pandemics, Geopolitical Instability) | -0.7% | Global | Short to Medium-term |

| Market Softening and Pricing Pressure due to Excess Capacity | -0.6% | Global, cyclical impact | Short-term |

| Talent Shortage in Analytics, AI, and Specialized Underwriting | -0.5% | North America, Europe, developed Asia | Medium to Long-term |

| Regulatory Scrutiny and Interoperability of Data Standards | -0.4% | Global, particularly cross-border operations | Ongoing |

Property and Casualty Reinsurance Market - Updated Report Scope

This report provides a comprehensive analysis of the global Property and Casualty Reinsurance Market, offering detailed insights into its current size, growth trajectories, and future outlook. It meticulously examines key market trends, significant drivers, restraints, opportunities, and challenges that shape the industry landscape. The scope encompasses an in-depth segmentation analysis, covering various types of reinsurance, coverage forms, and end-use applications, alongside a thorough regional assessment to provide a holistic understanding of market dynamics across different geographies. Furthermore, the report highlights the competitive landscape by profiling leading market players and their strategic initiatives, all while integrating the transformative impact of artificial intelligence and other technological advancements on the sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 352.8 Billion |

| Market Forecast in 2033 | USD 589.4 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Re Solutions Inc., Evergreen Re Group, Ascent Reassurance Company, Horizon Capital Re, Pinnacle Reinsurance Holdings, Alliance Risk Transfer, Nexus Re Solutions, Sterling Re Corp, Apex Re Ltd., Nova Re Holdings, Constellation Re Group, Sentinel Reassurance, Vanguard Reinsurance, Integrity Re Partners, Universal Risk Underwriters, Meridian Re Corp, Phoenix Re Group, Quantum Risk Partners, Olympus Reinsurance, Zenith Reassurance |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Property and Casualty Reinsurance market is segmented to provide a granular understanding of its diverse components and the distinct risk transfer solutions offered. This segmentation allows for a precise analysis of market dynamics across different lines of business, coverage structures, and end-user applications. The various segments reflect the specialized nature of reinsurance, enabling both primary insurers and reinsurers to manage and underwrite specific risk profiles effectively. Understanding these segments is crucial for identifying areas of growth, market saturation, and evolving client needs within the complex global risk landscape.

- By Type:

- Property Reinsurance: Covers risks related to physical assets (e.g., buildings, contents) against perils like fire, natural catastrophes, and other property damage.

- Casualty Reinsurance: Focuses on liability risks, including general liability, professional indemnity, motor liability, and workers' compensation.

- Specialty Reinsurance: Encompasses niche and complex risks such as marine, aviation, credit and surety, political risks, and cyber.

- By Coverage Type:

- Treaty Reinsurance: An agreement between the reinsurer and the ceding insurer to automatically reinsure a specific class or portfolio of business.

- Facultative Reinsurance: A single, specific risk or a defined group of risks offered by the ceding insurer and accepted or rejected by the reinsurer on a case-by-case basis.

- By Application:

- Commercial Lines: Reinsurance for business-related risks, including commercial property, general liability, professional indemnity, marine, aviation, and cyber insurance for businesses.

- Personal Lines: Reinsurance for individual-related risks such as homeowners' insurance, automobile insurance, and personal accident coverage.

- By Distribution Channel:

- Brokers: Reinsurance placed through intermediaries who facilitate transactions between ceding insurers and reinsurers.

- Direct Channels: Reinsurance placed directly between the ceding insurer and the reinsurer without an intermediary.

- Digital Platforms: Emerging channels leveraging online platforms and technology for placing reinsurance.

Regional Highlights

- North America: Continues to be the largest market due to high property values, significant exposure to natural catastrophes (hurricanes, wildfires, tornadoes), and a well-established regulatory framework. The United States leads in both premium volume and innovation, particularly in areas like cyber reinsurance and alternative capital. Canada also contributes significantly with its stable market and exposure to specific climate risks.

- Europe: A mature and highly competitive market characterized by robust regulatory oversight (e.g., Solvency II). Demand is driven by diverse risks including climate-related events, industrial liabilities, and geopolitical uncertainties. Key markets include Germany, Switzerland (a global reinsurance hub), the UK, and France, each contributing to market sophistication and capital supply.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid economic development, increasing insurable assets, and a growing middle class. Exposure to high-frequency natural disasters (earthquakes, typhoons, floods) drives demand for catastrophe reinsurance. China, Japan, India, and Australia are pivotal markets, with significant potential for growth in commercial and specialty lines as economies develop.

- Latin America: Experiences substantial growth opportunities, albeit with higher volatility due to economic and political instability in some countries. The region is highly exposed to natural perils, leading to strong demand for catastrophe and property reinsurance. Brazil, Mexico, and Chile are key markets, demonstrating increasing sophistication in risk management.

- Middle East and Africa (MEA): A developing market with diverse risk profiles ranging from energy and infrastructure projects in the Middle East to political risks and natural catastrophes in Africa. Growth is driven by large-scale development projects, increasing insurance penetration, and the need for international reinsurance capacity to cover complex regional risks.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Property and Casualty Reinsurance Market.- Global Re Solutions Inc.

- Evergreen Re Group

- Ascent Reassurance Company

- Horizon Capital Re

- Pinnacle Reinsurance Holdings

- Alliance Risk Transfer

- Nexus Re Solutions

- Sterling Re Corp

- Apex Re Ltd.

- Nova Re Holdings

- Constellation Re Group

- Sentinel Reassurance

- Vanguard Reinsurance

- Integrity Re Partners

- Universal Risk Underwriters

- Meridian Re Corp

- Phoenix Re Group

- Quantum Risk Partners

- Olympus Reinsurance

- Zenith Reassurance

Frequently Asked Questions

What is Property and Casualty Reinsurance?

Property and Casualty (P&C) Reinsurance is the insurance purchased by insurance companies (ceding insurers) from other insurance companies (reinsurers) to protect themselves from large losses arising from the policies they write. It covers risks related to physical assets (property) and liabilities (casualty) for both commercial and personal lines, helping insurers manage capital, stabilize earnings, and expand capacity.

What are the main drivers of the P&C reinsurance market's growth?

The primary drivers include the escalating frequency and severity of natural catastrophes, increasing global insurable exposures due to economic development and urbanization, stricter regulatory capital requirements for primary insurers, and the emergence of complex, systemic risks like cyber threats and pandemics. These factors collectively necessitate robust risk transfer mechanisms.

How does climate change impact the Property and Casualty Reinsurance market?

Climate change significantly impacts the P&C reinsurance market by increasing the frequency and intensity of extreme weather events, leading to higher catastrophe losses. This drives demand for reinsurance, influences pricing, and necessitates improved climate modeling and adaptation strategies to accurately assess and price escalating natural catastrophe risks.

What role does technology, specifically AI, play in Property and Casualty Reinsurance?

Technology, particularly Artificial Intelligence (AI) and advanced analytics, plays a transformative role by enhancing risk modeling, enabling more precise underwriting, automating claims processing, and improving fraud detection. AI helps reinsurers analyze vast datasets for better decision-making, optimize capital deployment, and develop innovative risk transfer solutions like parametric insurance.

What is the future outlook for the Property and Casualty Reinsurance market?

The future outlook for the P&C reinsurance market is positive, with projected sustained growth driven by persistent demand for risk transfer, especially for evolving perils. The market is expected to continue its adoption of technology for efficiency and new product development, while navigating challenges posed by climate change, systemic risks, and intense competition, fostering innovation and resilience.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted