Private Storage Cloud Market

Private Storage Cloud Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708564 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Private Storage Cloud Market Size

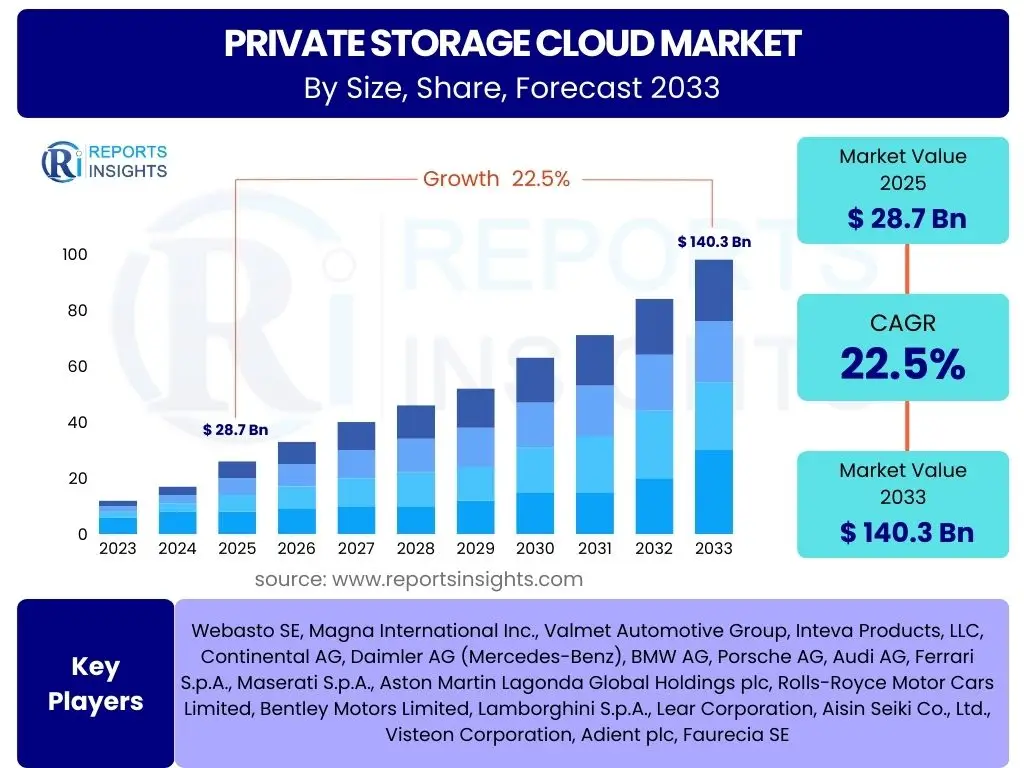

According to Reports Insights Consulting Pvt Ltd, The Private Storage Cloud Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033. The market is estimated at USD 28.7 Billion in 2025 and is projected to reach USD 140.3 Billion by the end of the forecast period in 2033.

The robust growth forecast for the Private Storage Cloud market is primarily driven by an accelerating global demand for enhanced data security, regulatory compliance, and greater control over data infrastructure. Enterprises across various sectors are increasingly migrating from traditional on-premise storage solutions and public cloud offerings to private storage clouds to mitigate risks associated with data breaches and to meet stringent industry-specific compliance requirements such as GDPR, HIPAA, and CCPA. This shift allows organizations to maintain complete ownership and management of their data, ensuring that sensitive information remains within their secure boundaries.

Furthermore, the escalating volume of data generated by digital transformation initiatives, IoT devices, and artificial intelligence applications is fueling the need for scalable and resilient storage solutions. Private storage clouds offer the flexibility to scale resources efficiently while providing predictable performance and costs, which is highly appealing to large enterprises with complex IT environments and specific workload demands. The ability to customize hardware and software configurations to match unique business requirements, coupled with dedicated resources that avoid the "noisy neighbor" effect common in public clouds, positions private storage cloud as a strategic investment for data-intensive organizations.

Key Private Storage Cloud Market Trends & Insights

Common user inquiries about Private Storage Cloud trends often revolve around data sovereignty, hybrid cloud integration, and the adoption of advanced data management techniques. Users seek to understand how organizations are balancing the benefits of private clouds with the flexibility of public clouds, and what new technologies are emerging to enhance security and efficiency. There is significant interest in how private cloud storage is evolving to support edge computing and distributed workforces, and how it addresses the growing concerns around data residency and compliance in a multi-jurisdictional environment.

- Hybrid and Multi-Cloud Adoption: Increasing integration of private storage with public cloud environments to create flexible hybrid and multi-cloud architectures, optimizing for cost, performance, and compliance.

- Enhanced Data Security and Sovereignty: Growing emphasis on robust encryption, access controls, and data residency solutions to meet stringent regulatory requirements and protect sensitive information.

- Software-Defined Storage (SDS) Dominance: Widespread adoption of SDS for greater agility, scalability, and cost efficiency in managing private storage resources, enabling abstraction from underlying hardware.

- Edge Computing Integration: Expansion of private storage solutions to the network edge, supporting low-latency data processing and storage for IoT devices and real-time applications.

- AI-Powered Storage Management: Utilization of artificial intelligence and machine learning for automated data tiering, anomaly detection, predictive maintenance, and intelligent resource allocation within private clouds.

- Sustainability and Energy Efficiency: Focus on developing and deploying energy-efficient hardware and software solutions to reduce operational costs and environmental impact of data centers.

AI Impact Analysis on Private Storage Cloud

User questions regarding AI's impact on Private Storage Cloud frequently address how artificial intelligence can enhance operational efficiency, improve data security, and optimize resource utilization. There is keen interest in understanding the practical applications of AI for automating routine storage tasks, predicting hardware failures, and intelligently tiering data. Concerns often include the complexity of integrating AI, the need for specialized skills, and the potential for AI to introduce new security vulnerabilities if not implemented carefully, alongside the immense potential for transformative benefits in large-scale data environments.

The integration of AI into private storage cloud environments is rapidly transforming how data is managed, secured, and optimized. AI-driven analytics provide unprecedented insights into storage utilization patterns, enabling organizations to make data-driven decisions on capacity planning, performance tuning, and lifecycle management. This leads to more efficient resource allocation, reducing operational expenditures and maximizing the value of existing infrastructure. Furthermore, AI algorithms can proactively identify anomalies and potential security threats, bolstering the overall security posture of private cloud storage solutions by enabling rapid response to suspicious activities or data access patterns.

- Automated Resource Optimization: AI algorithms intelligently allocate and provision storage resources based on real-time demand and predicted needs, optimizing performance and cost.

- Predictive Analytics for Maintenance: Machine learning models analyze historical data to predict potential hardware failures, enabling proactive maintenance and minimizing downtime.

- Enhanced Data Security and Anomaly Detection: AI monitors access patterns and data flows to detect unusual activities, identifying potential breaches or insider threats more effectively.

- Intelligent Data Tiering and Lifecycle Management: AI automatically moves data to the most appropriate storage tier (e.g., hot, warm, cold) based on access frequency and criticality, optimizing costs and performance.

- Improved Data Governance and Compliance: AI assists in classifying and tagging data, ensuring adherence to regulatory requirements and simplifying audit processes.

Key Takeaways Private Storage Cloud Market Size & Forecast

Analysis of common user questions concerning the Private Storage Cloud market size and forecast indicates a strong desire for actionable insights regarding investment strategies, competitive positioning, and future-proofing data infrastructure. Users are keen to understand the implications of the projected growth on their business operations, the critical factors driving this expansion, and where the most significant opportunities lie for market penetration or service expansion. The forecast underscores the essential role of private cloud storage in modern enterprise IT strategies, particularly for organizations with stringent security, performance, and compliance mandates.

The sustained and robust growth projected for the Private Storage Cloud market highlights its fundamental importance in the evolving digital landscape. As data volumes continue to surge and regulatory landscapes become more complex, the ability to control data location, access, and security within a dedicated environment becomes paramount. This growth trajectory signifies a strategic shift among enterprises towards more secure, customizable, and high-performance storage solutions that offer the flexibility of cloud computing without compromising on data governance. The market is poised for significant innovation, particularly in areas integrating AI, enhancing hybrid capabilities, and improving sustainability.

- Strategic Importance: Private storage cloud is a critical component for enterprises prioritizing data security, regulatory compliance, and predictable performance.

- Sustained High Growth: The market is set for substantial expansion, driven by increasing data volumes, stringent regulations, and the need for greater control over IT infrastructure.

- Hybrid & Multi-Cloud Synergy: Future growth will heavily rely on seamless integration capabilities with public clouds, enabling flexible and efficient hybrid IT strategies.

- Focus on Security & Control: Data sovereignty and advanced security features will remain primary drivers for adoption across various industries.

- Innovation in Management: AI-driven automation and software-defined capabilities will be key to unlocking further efficiency and scalability in private storage environments.

- Opportunity for Niche Providers: Specialized vendors focusing on specific industry compliance or advanced features can capitalize on distinct market needs.

Private Storage Cloud Market Drivers Analysis

The Private Storage Cloud market is significantly propelled by an increasing demand for enhanced data security and stringent regulatory compliance, particularly in industries handling sensitive information. Organizations are increasingly seeking dedicated and controlled environments to safeguard proprietary data, intellectual property, and customer information from potential breaches and unauthorized access. This imperative for robust security, coupled with the need to adhere to global data residency laws and industry-specific regulations, makes private storage clouds an attractive solution, offering complete control over data infrastructure and access policies.

Furthermore, the escalating volume of data generated by digital transformation, Big Data analytics, and IoT initiatives is a major catalyst for market growth. Enterprises require scalable, high-performance storage solutions that can efficiently manage massive datasets while ensuring rapid accessibility and consistent performance. Private storage clouds provide the necessary infrastructure to handle these demands, offering dedicated resources that mitigate the performance variability often associated with shared public cloud environments. The ability to customize hardware and software configurations to meet specific workload requirements further strengthens their appeal.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Data Security and Privacy | +5.5% | Global, particularly EU (GDPR), US (HIPAA, CCPA) | Short to Long Term |

| Strict Regulatory Compliance and Data Sovereignty Requirements | +4.8% | Global, especially EMEA, APAC | Short to Medium Term |

| Need for Greater Control and Customization over Infrastructure | +4.2% | North America, Europe, Large Enterprises | Medium Term |

| Growth in Data Volume and Big Data Analytics Adoption | +3.9% | Global, all major economies | Short to Long Term |

| Performance Requirements for Latency-Sensitive Applications | +3.5% | North America, Europe, Asia Pacific (Finance, Healthcare) | Medium Term |

Private Storage Cloud Market Restraints Analysis

Despite its significant advantages, the Private Storage Cloud market faces notable restraints, primarily centered around the high initial capital expenditure (CapEx) required for deployment and ongoing operational expenses. Building and maintaining a private cloud infrastructure involves substantial investments in hardware, software licenses, data center facilities, and specialized IT personnel. This high entry barrier can be particularly challenging for small and medium-sized enterprises (SMEs) or organizations with limited IT budgets, making public cloud offerings a more financially accessible alternative despite their potential security trade-offs.

Another significant restraint is the complexity associated with managing and operating private cloud environments. Organizations often require a highly skilled IT workforce proficient in cloud architecture, virtualization, networking, and security to effectively deploy, monitor, and maintain private storage clouds. The scarcity of such specialized talent and the ongoing costs of training and retention can deter potential adopters. Furthermore, the perceived lack of agility and scalability compared to the instant elasticity of public cloud services can also act as a constraint, as businesses prioritize rapid deployment and flexible scaling options in dynamic market conditions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure (CapEx) | -3.7% | Global, particularly SMEs and budget-sensitive organizations | Short to Medium Term |

| Complexity of Management and Operational Expertise Required | -3.2% | Global, especially developing regions with talent shortages | Short to Medium Term |

| Perceived Lack of Scalability and Agility Compared to Public Cloud | -2.8% | North America, Europe, technology-driven sectors | Short Term |

| Vendor Lock-in Concerns for Specific Private Cloud Solutions | -2.1% | Global, particularly large enterprises with existing infrastructure | Medium Term |

| Integration Challenges with Legacy Systems | -1.9% | Global, traditional industries (Manufacturing, Government) | Medium Term |

Private Storage Cloud Market Opportunities Analysis

The Private Storage Cloud market is ripe with opportunities driven by the accelerating trend of hybrid cloud adoption, where organizations seek to combine the best aspects of private and public cloud environments. This approach allows businesses to maintain sensitive data and critical workloads in a controlled private infrastructure while leveraging the scalability and cost-effectiveness of public clouds for less critical or fluctuating demands. Providers offering seamless integration, unified management platforms, and robust data migration tools for hybrid environments are well-positioned to capitalize on this growing demand, enabling enterprises to optimize their IT resources effectively.

Furthermore, the increasing focus on edge computing and the proliferation of IoT devices present significant opportunities for private storage cloud solutions. As data generation shifts closer to the source, there is a burgeoning need for localized storage and processing capabilities to reduce latency and bandwidth consumption. Private storage clouds can be deployed at the edge, offering dedicated, secure, and high-performance storage infrastructure for edge applications, particularly in sectors like manufacturing, retail, and smart cities. This expansion beyond traditional data centers opens new revenue streams and applications for private cloud providers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Hybrid Cloud and Multi-Cloud Deployments | +6.2% | Global, all major markets | Short to Long Term |

| Expansion of Edge Computing and IoT Data Storage Needs | +5.8% | Global, industries adopting IoT (Manufacturing, Retail) | Medium to Long Term |

| Development of AI/ML-Driven Storage Automation and Optimization | +5.1% | North America, Europe, APAC (Technology sectors) | Medium to Long Term |

| Increasing Demand for Disaster Recovery and Business Continuity Solutions | +4.5% | Global, highly regulated industries (Finance, Healthcare) | Short to Medium Term |

| Managed Private Cloud Services for Simplified Operations | +4.0% | Global, especially SMEs and enterprises with limited IT staff | Medium Term |

Private Storage Cloud Market Challenges Impact Analysis

The Private Storage Cloud market faces significant challenges in the form of fierce competition from hyperscale public cloud providers, which offer vast economies of scale, extensive global infrastructure, and a broad range of integrated services at competitive price points. Public cloud services often appear more attractive due to their pay-as-you-go models and perceived ease of deployment, making it difficult for private cloud solutions to compete purely on cost or immediate scalability for general-purpose workloads. This intense rivalry forces private cloud providers to differentiate through specialized features, superior security, and tailored performance guarantees, rather than broad market appeal.

Another major challenge involves the ongoing integration of private cloud environments with complex legacy IT systems and disparate public cloud services. Many enterprises operate with a mix of outdated infrastructure and newer cloud platforms, requiring sophisticated integration strategies to ensure seamless data flow, application compatibility, and unified management. This complexity can lead to increased deployment times, higher integration costs, and potential operational bottlenecks, hindering the full realization of private cloud benefits. Addressing these interoperability challenges effectively is crucial for sustained market adoption and growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Hyperscale Public Cloud Providers | -4.5% | Global, all markets | Short to Long Term |

| Complex Integration with Existing IT Infrastructure and Hybrid Environments | -3.8% | Global, especially large enterprises with legacy systems | Medium Term |

| Shortage of Skilled IT Professionals for Private Cloud Management | -3.0% | Global, particularly emerging markets | Short to Medium Term |

| Balancing Cost Efficiency with Performance and Customization | -2.5% | Global, particularly cost-sensitive industries | Short to Medium Term |

| Rapid Technological Obsolescence and Need for Continuous Upgrades | -2.0% | Global, all technology-dependent sectors | Long Term |

Private Storage Cloud Market - Updated Report Scope

This updated market research report provides an in-depth analysis of the global Private Storage Cloud market, encompassing detailed market sizing, growth projections, and comprehensive insights into key trends, drivers, restraints, opportunities, and challenges influencing the industry from 2025 to 2033. The report meticulously segments the market by component, deployment model, organization size, industry vertical, and region, offering a granular view of market dynamics. It also includes an extensive competitive landscape analysis, profiling major market players and assessing their strategic initiatives, product portfolios, and market positioning to provide a holistic understanding of the ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.7 Billion |

| Market Forecast in 2033 | USD 140.3 Billion |

| Growth Rate | 22.5% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Company A, Company B, Company C, Company D, Company E, Company F, Company G, Company H, Company I, Company J, Company K, Company L, Company M, Company N, Company O, Company P, Company Q, Company R, Company S, Company T |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Private Storage Cloud market is intricately segmented to provide a granular understanding of its diverse landscape, catering to varied organizational needs and technological preferences. This segmentation allows for a detailed analysis of market dynamics, revealing specific growth drivers and opportunities within each category. The comprehensive breakdown by component, deployment model, organization size, and industry vertical enables stakeholders to pinpoint key areas of investment and strategic focus, optimizing their market penetration and service offerings to meet specialized demands across different sectors and enterprise scales.

Understanding these segments is crucial for identifying emerging trends and tailoring solutions effectively. For instance, the growth in Software-Defined Storage within the software component category underscores the industry's shift towards greater agility and hardware abstraction. Similarly, the robust adoption in BFSI and Healthcare verticals highlights the critical need for secure and compliant storage solutions in highly regulated environments. This multi-dimensional segmentation provides a powerful framework for market assessment and strategic planning, empowering businesses to make informed decisions and navigate the complexities of the private storage cloud ecosystem efficiently.

- By Component

- Storage Hardware

- Servers

- Storage Arrays

- Networking Equipment

- Storage Software

- Software-Defined Storage

- Backup & Recovery

- Data Management

- Security

- Orchestration & Automation

- Services

- Professional Services

- Managed Services

- Consulting Services

- Support & Maintenance

- Storage Hardware

- By Deployment Model

- On-Premise Private Cloud

- Hosted Private Cloud

- By Organization Size

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- By Industry Vertical

- BFSI (Banking, Financial Services, and Insurance)

- IT & Telecommunications

- Healthcare & Life Sciences

- Government & Public Sector

- Manufacturing

- Retail & E-commerce

- Media & Entertainment

- Education

- Others (e.g., Energy & Utilities, Transportation & Logistics)

Regional Highlights

North America currently leads the Private Storage Cloud market, primarily driven by the early adoption of advanced cloud technologies, the presence of numerous large enterprises with substantial data needs, and stringent regulatory environments such as HIPAA and CCPA. The region benefits from a well-developed IT infrastructure and a strong focus on digital transformation across industries like healthcare, finance, and technology. Investment in data centers, coupled with a high demand for data security and control, continues to propel the market forward in the United States and Canada, particularly among organizations handling sensitive customer information and intellectual property.

Europe is another significant market, characterized by its strict data protection regulations, most notably the GDPR, which mandates data residency and privacy controls. This regulatory landscape strongly favors private storage cloud solutions, as organizations seek to ensure compliance and maintain data sovereignty within the EU. Countries like Germany, the UK, and France are experiencing robust growth, fueled by enterprises in the financial services, government, and manufacturing sectors investing in dedicated cloud infrastructures to meet compliance requirements and enhance data security. The trend towards hybrid cloud models also contributes to the market expansion in this region, balancing agility with control.

The Asia Pacific (APAC) region is projected to exhibit the highest growth rate during the forecast period, owing to rapid digital transformation initiatives, increasing cloud adoption by SMEs, and growing awareness regarding data security. Emerging economies like China and India, along with developed markets like Japan and Australia, are witnessing substantial investments in data center infrastructure and cloud services. The proliferation of mobile devices, IoT, and Big Data analytics generates massive amounts of data, creating a compelling need for scalable and secure private storage solutions across diverse industries, from telecommunications to e-commerce and manufacturing.

Latin America and the Middle East & Africa (MEA) regions are also showing promising growth, albeit from a smaller base. In Latin America, countries like Brazil and Mexico are seeing increased adoption due to regulatory requirements and the need for localized data storage. In MEA, the push for digital government services and the growth of the oil and gas sector, coupled with emerging financial hubs, are driving investments in secure private cloud infrastructure. However, challenges such as infrastructure limitations and a lack of skilled IT professionals may moderate the pace of growth in these regions, making managed private cloud services particularly appealing.

- North America: Dominant market share due to early tech adoption, robust IT infrastructure, stringent regulations (HIPAA, CCPA), and strong enterprise demand for data control in sectors like finance and healthcare.

- Europe: Significant growth driven by GDPR compliance, strong data sovereignty requirements, and increasing investment in hybrid cloud models across BFSI, government, and manufacturing industries.

- Asia Pacific (APAC): Fastest-growing region, propelled by rapid digital transformation, increasing internet penetration, rise of SMEs adopting cloud, and burgeoning data volumes from IoT and mobile in countries like China, India, and Japan.

- Latin America: Moderate growth driven by evolving data protection laws, increasing digitalization, and the need for localized data processing, particularly in Brazil and Mexico.

- Middle East & Africa (MEA): Emerging market with growth driven by smart city initiatives, digital government services, and expanding financial and energy sectors requiring secure, localized data storage.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Private Storage Cloud Market.- Company A

- Company B

- Company C

- Company D

- Company E

- Company F

- Company G

- Company H

- Company I

- Company J

- Company K

- Company L

- Company M

- Company N

- Company O

- Company P

- Company Q

- Company R

- Company S

- Company T

Frequently Asked Questions

What is a Private Storage Cloud?

A Private Storage Cloud is a dedicated cloud storage infrastructure accessible only to a single organization, offering enhanced data security, control, and performance. It can be hosted on-premise or by a third-party provider.

Why choose Private Storage Cloud over Public Cloud?

Organizations choose Private Storage Cloud for superior data security, stricter compliance with regulations (like GDPR, HIPAA), greater control over infrastructure, predictable performance, and the ability to customize for specific workloads, especially with sensitive data.

What are the key benefits of Private Storage Cloud?

Key benefits include enhanced data security, improved regulatory compliance, full control over data and infrastructure, customizable performance, reduced latency for critical applications, and often more predictable costs compared to variable public cloud spending.

How does AI impact Private Storage Cloud?

AI significantly enhances Private Storage Cloud by automating resource optimization, enabling predictive maintenance, improving data security through anomaly detection, and facilitating intelligent data tiering for cost and performance efficiency.

What are the main challenges in adopting Private Storage Cloud?

Primary challenges include high initial capital expenditure, the complexity of management requiring specialized IT skills, integration with existing IT infrastructure, and intense competition from hyperscale public cloud providers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted